- Processed Food

- Food Pathogen Testing Market

Food Pathogen Testing Market Size, Share, and Growth Forecast, 2026 – 2033

Food Pathogen Testing Market by Pathogen Type (Salmonella, Listeria, E. coli), Technology (Rapid, Traditional), Food Type (Meat & Poultry, Processed Foods, Dairy), End-user (Food Manufacturers, Testing Labs, Government Bodies), and Regional Analysis 2026 – 2033

Food Pathogen Testing Market Size and Trends Analysis

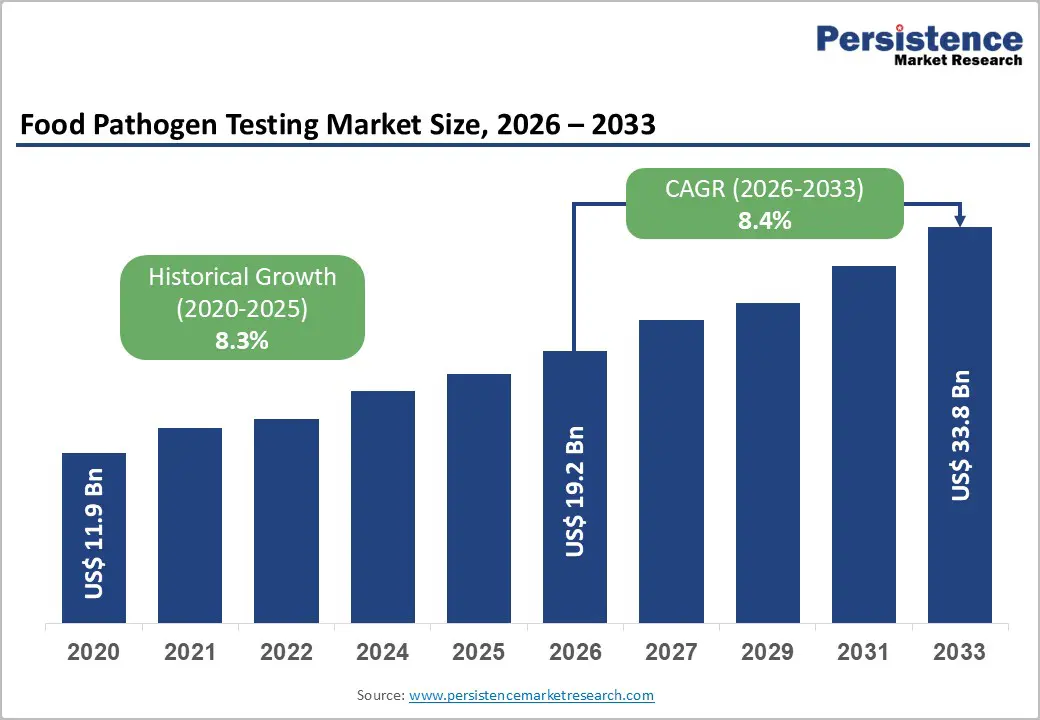

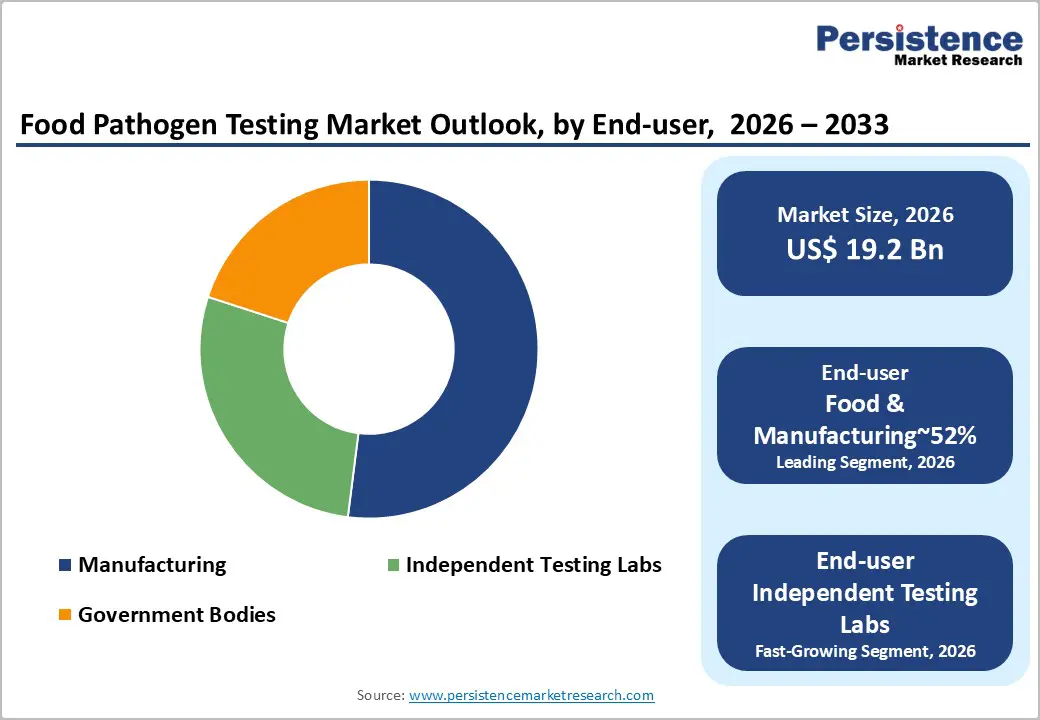

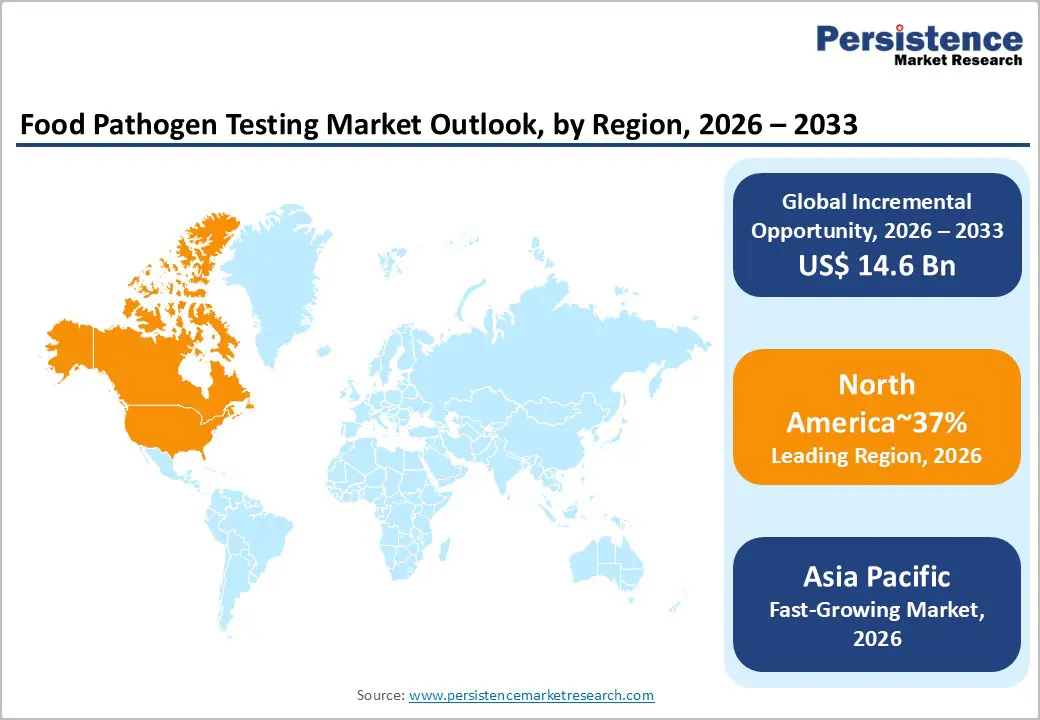

The global food pathogen testing market size is likely to be valued at US$19.2 billion in 2026 and is expected to reach US$33.8 billion by 2033, growing at a CAGR of 8.4% between the forecast period 2026 to 2033, driven by the rising foodborne illnesses, stricter regulations, and demand for rapid testing technologies. The industry is currently undergoing a pivotal shift from reactive product testing to proactive, data-driven environmental monitoring, fueled by the rapid adoption of automation and next-generation sequencing (NGS) technologies.

Key Industry Highlights:

- Leading Region: North America is expected to lead with around 37% share in 2026, supported by stringent regulatory frameworks, high adoption of rapid testing technologies, and strong consumer safety awareness.

- Leading Pathogen Type: Salmonella is anticipated to remain the leading pathogen type, holding around 29% share, due to its high prevalence in meat, poultry, and processed foods and the regulatory emphasis on controlling outbreaks.

- Leading Technology: Rapid testing technologies are expected to remain the leading technology, accounting for roughly 76% share, as they enable faster, automated detection, high-throughput screening, and real-time quality assurance across food supply chains.

- Leading Food Type: Meat & poultry products are anticipated to remain the leading food type segment, holding around 30% share, as these categories are highly susceptible to contamination and heavily monitored by food safety authorities.

- Leading End-user: Food manufacturers are expected to remain the leading end-user segment, accounting for approximately 52% of the market, owing to their primary responsibility for in-house quality assurance, regulatory compliance, and continuous product monitoring.

| Report Attribute | Details |

|---|---|

|

Food Pathogen Testing Market Size (2026E) |

US$19.2 Bn |

|

Market Value Forecast (2033F) |

US$33.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Technological Evolution toward Rapid Diagnostics

The food pathogen testing market is being reshaped by the shift from culture-based methods to rapid diagnostics. Technologies such as PCR, immunoassays, and next-generation biosensors cut detection time from days to hours, reducing production delays, inventory risk, and the chance of contaminated products reaching consumers. As a result, time-to-result is now a core performance metric, making rapid testing a strategic investment for operational efficiency and cost control.

Beyond speed, molecular diagnostics deliver higher sensitivity and specificity, enabling strain-level identification and precise outbreak tracing. Automation and AI streamline sample prep, data analysis, and reporting, increasing throughput while minimizing human error. Portable biosensors and predictive analytics enable on-site, real-time monitoring, supporting proactive contamination prevention. Blockchain integration further strengthens traceability, allowing faster, more targeted recalls. Together, these advances are transforming quality assurance workflows and giving early adopters a competitive edge. For example, in August 2025, Gold Standard Diagnostics launched the BACGene GO RT-PCR Kit, a two-step rapid workflow designed to accelerate routine food screening and boost lab productivity.

Rising Foodborne Illness Outbreaks

The food pathogen testing market is driven by the rising frequency and complexity of foodborne illness outbreaks. Pathogens such as Salmonella, Listeria, and E. coli continue to impact meat, poultry, dairy, ready-to-eat, and plant-based foods. As supply chains lengthen and fragment, cross-contamination risks increase, prompting manufacturers and distributors to adopt proactive testing strategies. Growing consumer scrutiny and the financial and reputational damage linked to outbreaks further reinforce the need for continuous, end-to-end monitoring.

This urgency is accelerating the adoption of rapid molecular diagnostics and automated microbiological testing to detect contamination early and prevent recalls. High-throughput platforms and real-time monitoring tools are increasingly embedded in processing facilities to protect operational continuity. Hybrid approaches that combine culture-based methods with AI-driven predictive analytics enable manufacturers to anticipate contamination events and optimize interventions. The convergence of speed, accuracy, and efficiency strengthens the business case for widespread adoption, positioning pathogen testing as a critical investment in brand protection and public health. For example, in January 2025, Neogen Corporation launched the MDA2 Quantitative Salmonella Molecular Detection Assay, enabling poultry producers to quantify Salmonella, verify intervention effectiveness, and strengthen supply chain safety.

Barrier Analysis - High Costs of Advanced Pathogen Testing

The adoption of rapid diagnostics in the food pathogen testing market is constrained by high capital and operating costs. Technologies such as PCR, whole genome sequencing (WGS), and other molecular assays require significant upfront investment in specialized instruments, laboratory infrastructure, and skilled personnel. Ongoing costs for proprietary reagents, consumables, software licenses, and equipment maintenance further increase the total cost of ownership compared to traditional culture-based methods. These financial pressures disproportionately affect small and medium-sized enterprises (SMEs), which account for a large share of the global food supply chain.

As a result, many SMEs are unable to deploy rapid testing in-house and rely on slower, lower-cost conventional methods or limited third-party testing services. This creates inconsistencies in testing frequency and coverage, increasing the risk of undetected contamination. High CAPEX and OPEX also restrict adoption in cost-sensitive regions, slowing overall market penetration despite clear advantages in speed and accuracy. For example, in December 2025, Hardy Diagnostics partnered with NEMIS Technologies to introduce rapid, on-site pathogen detection in North America, reducing reliance on labs and helping mitigate cost barriers through point-of-need testing.

Opportunity Analysis - Outsourcing to Independent Testing Labs

Outsourcing food pathogen testing to independent laboratories presents a strong growth opportunity, driven by manufacturers’ need to control costs while accessing advanced diagnostic capabilities. Outsourcing eliminates the capital burden of investing in high-end instruments and in-house laboratories, while providing access to specialized expertise in rapid molecular testing, next-generation sequencing, and AI-enabled data analysis. Independent labs also deliver validated, third-party results that strengthen quality assurance, reduce liability risk, and enhance brand credibility across the supply chain.

Strategically, outsourcing supports compliance with evolving food safety regulations and expands beyond routine testing into value-added services. Many laboratories now offer environmental monitoring, pathogen mapping, and root-cause analysis to identify contamination hotspots and guide preventive actions. This model is especially attractive for small and medium-sized enterprises that lack the scale to maintain dedicated microbiology facilities. Market consolidation further accelerates growth, as global testing companies acquire regional labs to expand geographic coverage and capacity. Economically, outsourcing lowers total testing costs and improves turnaround times compared to maintaining in-house operations. For example, in February 2025, the USDA-FSIS adopted bioMérieux’s LPT broth for Listeria testing, reflecting the type of standardized, regulator-approved protocols commonly delivered through independent laboratory services.

Integration of AI and Blockchain for Predictive Food Safety

The convergence of artificial intelligence (AI) and blockchain presents a transformative opportunity for the food pathogen testing market, shifting it from reactive detection to proactive safety intelligence. AI enables predictive risk modeling by analyzing environmental, production, and logistics data to identify contamination hotspots before pathogens enter the supply chain. Blockchain secures these insights in an immutable ledger, delivering end-to-end traceability and a single, trusted data source for manufacturers, suppliers, and regulators.

Together, these technologies accelerate rapid diagnostics by reducing interpretation time for PCR and sequencing results, while blockchain timestamps and verifies test data for instant regulatory sharing. Recall management becomes more precise, allowing affected batches to be isolated without large-scale product withdrawals. AI-driven supplier risk scoring combined with blockchain-linked IoT sensor data further improves transparency and consumer trust. In September 2025, LuminUltra partnered with Kikkoman Biochemifa to expand distribution of advanced ATP/ADP/AMP hygiene monitoring and Easy Plate™ tests, improving data speed and accuracy, key inputs for AI analytics, and traceable, digital food safety records.

Category–wise Analysis

Pathogen Type Insights

Salmonella is expected to lead, accounting for roughly 30% of the market share in 2026, driven by its high incidence in global foodborne illness and broad presence across meat, poultry, eggs, animal feed, and herbal supplements. Regulatory shifts, including the USDA-FSIS withdrawal of a mandatory poultry framework, have increased dependence on voluntary private testing to manage legal and commercial risk. Expanded capacity in accredited laboratories across India and consolidation among global testing providers are strengthening surveillance in high-growth regions. Testing intensity is also rising in animal feed following antibiotic growth promoter bans, while export-oriented producers are increasing third-party verification to meet US and EU compliance standards.

Thermo Fisher Scientific’s SureTect™ Salmonella PCR assays are widely used in high-throughput facilities, bioMérieux’s GENE-UP® Salmonella supports routine screening in contract labs, and Neogen’s MDA2 Quantitative Salmonella kit is shifting plant decisions by measuring pathogen load to guide targeted sanitation.

Listeria is projected to be the fastest-growing pathogen segment, driven by zero-tolerance policies in ready-to-eat foods and elevated risk in chilled and frozen supply chains. High-profile outbreaks have accelerated mandatory environmental monitoring of food contact surfaces, drains, and equipment, sharply increasing test volumes.

Demand is shifting toward quantitative risk assessment, whole genome sequencing-enabled traceability, and near-line rapid testing to reduce pre-release risk. Growth in convenience foods and stricter FDA oversight are reinforcing the adoption of high-sensitivity molecular diagnostics. bioMérieux’s VIDAS® and GENE-UP® Listeria assays anchor many monitoring programs, while Thermo Fisher’s SureTect™ Listeria PCR supports fast release decisions. Neogen’s Listertest™, Petrifilm™, and Hygiena’s portable systems enable near-line and on-site verification.

End-user Insights

Food manufacturers are expected lead, accounting for approximately 52% of the market share in 2026, as food safety shifts from end-point inspection to prevention-led systems embedded directly into production. Retailers increasingly require near-instant clearance before shipment, driving processors to deploy compact in-house “satellite labs” and compress release cycles. Continuous testing of raw materials, in-process samples, and finished goods generates high, recurring demand for diagnostic kits and consumables, making manufacturers the primary revenue driver.

Recall risk and brand damage further justify frequent testing, particularly as ready-to-eat meals, salads, and chilled foods expand, where no consumer kill step exists. In response, manufacturers are adopting cloud-connected quality systems, quantitative hygiene monitoring, and predictive analytics that link environmental conditions to contamination risk. Platforms such as bioMérieux’s TEMPO® support high-throughput enumeration in industrial workflows, while Thermo Fisher Scientific’s 3M/Neogen Petrifilm™ plates remain standard for routine indicator testing across raw and finished products.

Independent laboratories are projected to be the fastest-growing end-user segment as food safety oversight becomes more specialized, regulated, and legally sensitive. Cross-border trade has turned third-party test reports into a de facto trade passport, while stricter accreditation requirements make it difficult for in-house labs to maintain multi-method compliance. Advanced techniques such as whole-genome sequencing are increasingly centralized in expert laboratories for outbreak investigation and source attribution.

Expansion near ports and agricultural hubs shortens turnaround times for exporters. Beyond routine testing, labs are expanding into method validation, forensic tracing, and litigation support. Large networks such as Eurofins illustrate scale advantages, while tools such as Bruker’s MALDI Biotyper® enable rapid species-level identification in complex food matrices.

Regional Insights

North America Food Pathogen Testing Market Trends

North America is expected to remain the dominant region in the market, accounting for approximately 38% of global share, driven by a mature regulatory framework, a large-scale processed and packaged food industry, and early adoption of advanced molecular diagnostics across production, distribution, and retail.

The region benefits from dense networks of accredited commercial laboratories, strong federal–state coordination on outbreak surveillance, and mandatory compliance regimes that embed pathogen testing into preventive controls. Structural demand is anchored by zero-tolerance policies for high-risk pathogens in ready-to-eat foods, the high financial and reputational costs of recalls, and growing complexity in food matrices, including alternative proteins, fresh-cut produce, and extended cold chains. Technology deployment is shifting toward standardized PCR, whole genome sequencing for source attribution, and on-site rapid diagnostics to reduce time-to-detection in high-throughput environments.

The U.S. is expected to drive regional performance, supported by its large industrial processing base, concentration of multinational manufacturers, and federal programs linking pathogen testing with digital traceability and preventive control systems. Canada reinforces regional stability through regulatory alignment with U.S. frameworks, cross-border certification practices, and investments in laboratory accreditation and surveillance across meat, dairy, and seafood. Across North America, growth is supported by predictive food safety models, genomic surveillance in private labs, retailer-led testing mandates, and institutionalized environmental monitoring programs, collectively sustaining high testing intensity and long-term demand for advanced detection platforms.

Europe Food Pathogen Testing Market Trends

Europe is expected to remain a stable and systemically important region in the market, supported by a mature regulatory framework, extensive laboratory infrastructure, and institutionalized food safety governance across the agri-food value chain. Harmonized enforcement of the General Food Law, EFSA risk assessment protocols, and routine surveillance programs structurally anchor demand for microbiological and molecular testing across meat, dairy, fresh produce, and processed foods.

High compliance intensity among food processors and retailers, coupled with ongoing surveillance of Salmonella, E. coli, Listeria, and Campylobacter, reinforces market stability. Rapid molecular diagnostics are increasingly integrated into routine quality control workflows, while high-throughput PCR platforms, syndromic testing panels, automated sample preparation, and digital traceability systems improve turnaround, reproducibility, and audit readiness.

Germany is expected to anchor regional performance due to the scale of its accredited laboratory networks, strict federal enforcement, and high testing intensity across meat and dairy clusters. France remains a strong market, driven by clean-label requirements, regulatory scrutiny in fresh and processed foods, and investment in both in-house and outsourced testing programs. Across Europe, market momentum is supported by regulatory tightening on imports, increased outbreak-related analytical workloads, and modernization of laboratory operations through automation, AI-driven data management, and advanced molecular detection platforms integrated into national surveillance and traceability systems.

Asia Pacific Food Pathogen Testing Market Trends

Asia Pacific is expected to remain the fastest-growing region in the market, driven by rapid industrialization of food processing, rising export exposure to stringent Western safety standards, and strengthening regulatory enforcement across key food-producing economies. Mandatory compliance linked to export certification, increased urban consumption of processed and ready-to-eat foods, and government-led capacity building, through laboratory accreditation, mobile testing units, and harmonized protocols, are reshaping the regional food safety ecosystem.

Structural demand is supported by a higher incidence of foodborne illnesses, intensified scrutiny of dairy, poultry, and infant nutrition supply chains, and modernization of retail channels requiring standardized safety documentation. Technology adoption is expected to favor cost-efficient molecular diagnostics, portable rapid-testing solutions, and AI-enabled hygiene monitoring for high-throughput screening across fragmented manufacturing and distribution networks.

China is anticipated to anchor regional growth through large-scale digitalization of food safety reporting, tighter enforcement of national food safety laws for export-oriented processors, and rapid implementation of traceability systems across seafood and poultry value chains. India is poised to act as a structural demand driver, supported by the expansion of accredited laboratory capacity, formalization of street food and dairy testing regimes, and policy incentives for in-house microbiology capabilities in manufacturing clusters. Across Asia Pacific, market momentum will be reinforced by export-driven compliance, private retailer-led standards, expansion of antibiotic resistance testing, and gradual adoption of harmonized testing frameworks, collectively raising baseline testing intensity across domestic and international supply chains.

Competitive Landscape

The global food pathogen testing market is moderately consolidated, led by Thermo Fisher Scientific, Neogen, bioMérieux, SGS, Eurofins, and Intertek, whose scale, regulatory credibility, and global networks shape competitive dynamics. These leaders influence workflow standards and procurement decisions through their broad portfolios spanning consumables, equipment, and testing services. While top-tier players exert strong control, the wider laboratory services segment remains fragmented, sustaining regional and application-level competition.

Competitive advantage focuses on total workflow solutions, integrating sampling tools, diagnostic platforms, analytics software, and outsourced testing. Leaders differentiate through rapid diagnostics, digital integration, and global footprints, while smaller providers compete via localized service and niche testing. Industry trends include platform integration, cross-border expansion, and service-led consolidation, with continuous investment in faster, automated diagnostics and scaled laboratory networks, driving the market toward more unified, end-to-end testing ecosystems.

Key Industry Highlights:

- In January 2026, DKSH partnered with Thermo Fisher Scientific to distribute SureTect™ rapid pathogen kits in Southeast Asia, expanding access to molecular detection in high-growth APAC markets.

- In July 2025, QuantiPath highlighted GenoPATHx for multi-serovar Salmonella detection, rapidly identifying and quantifying strains to improve control in beef and pet food supply chains.

- In July 2025, Neogen Corporation launched Listeria Right Now™, delivering enrichment-free results in ~2 hours, enabling same-shift corrective actions and reducing Listeria risks in dairy, produce, and ready-to-eat foods.

- In February 2025, bioMérieux launched GENE-UP® TYPER, a PCR-based tool for rapid Listeria strain characterization, supporting root-cause analysis, targeted recalls, and preventive measures, reducing recall scope and costs.

Companies Covered in Food Pathogen Testing Market

- Thermo Fisher Scientific

- Eurofins Scientific

- SGS SA

- bioMérieux S.A.

- Neogen Corporation

- Bio-Rad Laboratories

- Intertek Group plc

- Bureau Veritas S.A.

- Merck KGaA

- ALS Limited

- Mérieux NutriSciences

- TÜV SÜD AG

- Hygiena LLC

- Agilent Technologies

- AsureQuality Ltd.

- Romer Labs

- Microbac Laboratories

Frequently Asked Questions

The global food pathogen testing market is projected to be valued at US$19.2 billion in 2026 and is expected to reach US$33.8 billion by 2033, driven by rising foodborne illnesses, stricter regulations, and the adoption of rapid testing technologies.

The transition from traditional culture-based methods to rapid diagnostic technologies such as PCR and immunoassays is a primary driver, as it significantly reduces detection times from days to hours, improves supply chain efficiency, minimizes recall risks, and enables proactive, data-driven food safety management.

The food pathogen testing market is forecast to grow at a CAGR of 8.4% from 2026 to 2033, reflecting sustained demand for advanced safety testing across the food supply chain.

North America is the leading regional market, accounting for approximately 38% share, supported by stringent regulatory frameworks, high adoption of rapid testing technologies, and strong consumer safety awareness.

The food pathogen testing market is moderately consolidated, with key players including Thermo Fisher Scientific, Eurofins Scientific, SGS SA, bioMérieux S.A., and Neogen Corporation.