- Plastics, Polymers & Resins

- Synthetic and Bio Emulsion Polymer Market

Synthetic and Bio Emulsion Polymer Market Size, Share, and Growth Forecast, 2025 - 2032

Synthetic and Bio Emulsion Polymer Market by Product Type (Synthetic Emulsion Polymers, Bio-Based Emulsion Polymers), Application (paints & coatings, adhesives & sealants, paper & paperboard, textiles & nonwovens, construction additives, leather finishing & fabric, others.), and Regional Analysis for 2025 - 2032

Synthetic and Bio Emulsion Polymer Market Size and Trends Analysis

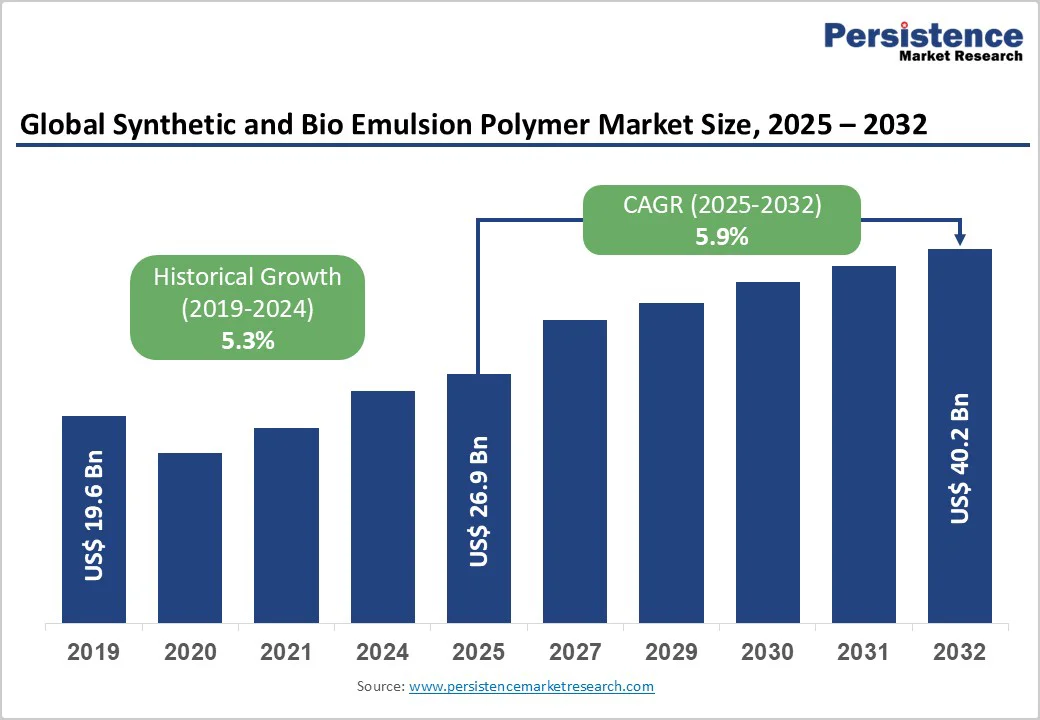

The global synthetic and bioemulsion polymer market size is likely to be valued at US$26.9 billion in 2025 and is projected to reach US$40.2 billion, growing at a CAGR of 5.9% between 2025 and 2032.

The acceleration from historical to forecast CAGR indicates strengthening market fundamentals driven by environmental regulations mandating low-VOC formulations, expanding infrastructure investments across emerging economies, and technological advancements in bio-based polymer development.

The transition toward water-based emulsion polymers has gained significant momentum as industries prioritize sustainability and regulatory compliance, with architectural coatings output in China increasing by 12.5% in 2023 due to aggressive urban development and green building mandates.

Key Industry Highlights:

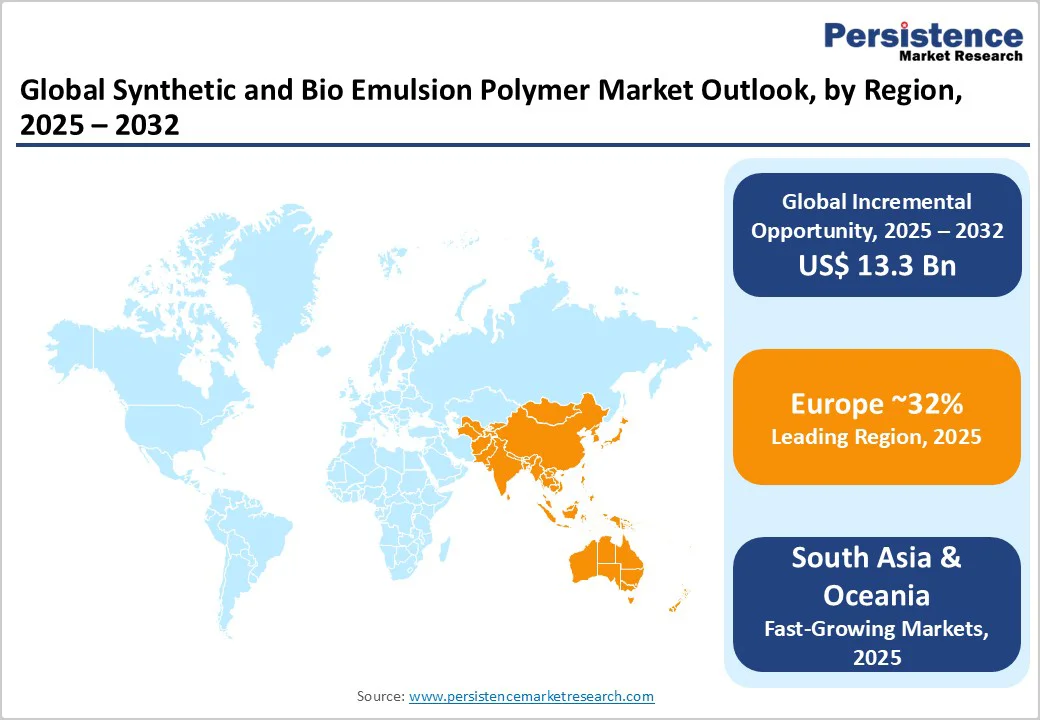

- East Asia leads the global synthetic and bio emulsion polymer market with over 32% share, driven by rapid industrialization, large-scale infrastructure projects in China and India, and strong demand from construction and automotive sectors.

- Synthetic emulsion polymers dominate the Synthetic and Bio Emulsion Polymer market, accounting for nearly 88% of global consumption due to their proven performance, cost-effectiveness, and extensive use in paints, coatings, and adhesives.

- Stringent environmental regulations and VOC emission standards across North America and Europe are shaping the Synthetic and Bio Emulsion Polymer market landscape, accelerating the shift toward low-VOC, water-based, and bio-based formulations.

- Bio-based emulsion polymers are the fastest-growing segment within the Synthetic and Bio Emulsion Polymer market, supported by sustainability mandates, innovation in renewable raw materials, and growing consumer preference for eco-friendly solutions.

- Rising investments in green construction and advanced coating technologies are expected to sustain long-term growth opportunities in the Synthetic and Bio Emulsion Polymer market globally.

| Key Insights | Details |

|---|---|

| Synthetic and Bio Emulsion Polymer Market Size (2025E) | US$26.9 Bn |

| Market Value Forecast (2032F) | US$40.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.3% |

Market Dynamics

Driver - Stringent Environmental Regulations and VOC Emission Standards

Environmental regulations requiring reductions in volatile organic compound (VOC) emissions represent the primary growth catalyst for emulsion polymers globally. The U.S. Environmental Protection Agency (EPA) finalized amendments to national VOC emission standards for aerosol coatings in January 2025, extending compliance deadlines to January 2027 and requiring manufacturers to reformulate products to meet lower VOC thresholds.

The European Union's Commission Regulation (EU) 2023/2055, effective October 2023, restricts synthetic polymer microparticles and mandates compliance documentation for industrial-use emulsion polymers by October 2025.

In Europe, the VOC Directive (2004/42/EC) sets VOC content limits, expressed as grams per liter, for different coating types, while new GB standards in China align with EU VOC benchmarks to promote waterborne and UV-cured coatings.

These regulatory frameworks have accelerated the substitution of solvent-based polymers with water-based emulsion alternatives.

According to the U.S. Census Bureau, construction sector growth of approximately 4% annually from 2024 to 2028 directly benefits acrylic emulsion demand in architectural coatings and adhesive applications, as these formulations offer superior durability, weather resistance, and versatility while meeting stringent environmental standards. The global paints and coatings market is experiencing steady growth, with water-based formulations holding a leading share, creating substantial downstream demand for environmentally compliant emulsion polymers.

Infrastructure Development and Construction Industry Expansion

Massive infrastructure investments across Asia-Pacific, particularly in China and India, serve as fundamental demand drivers for emulsion polymers in construction applications.

China's 14th Five-Year Plan (2021 - 2025) allocated approximately US$4.2 trillion to infrastructure development, with the National Highway Network Planning document targeting the construction of 461,000 km of highways, including 162,000 km of expressways, by 2035.

China's Belt and Road Initiative recorded unprecedented engagement of USD 124 billion through construction contracts and investments in H1 2025 alone, nearly doubling the total 2024 engagement of USD 122 billion, with cumulative BRI engagement reaching USD 1.308 trillion since 2013.

India's infrastructure engagement through the "Neighbourhood First" and "Act East" policies emphasizes transparency and people-centric development, with over USD 4 billion in credit lines supporting Sri Lanka's economy and a USD 110 million sanitation project covering 28 Maldivian islands in 2024.

The Asia-Pacific construction additives market, valued at USD 35 billion in 2022, is projected to drive polymer emulsion consumption as these materials enhance durability, waterproofing, and surface treatments in cement modification applications.

In the United States, single-family building permits increased 6.7% to 981,911 units in 2024. However, multifamily permits declined 16.1% to 496,089 units, reflecting shifting residential construction patterns that nonetheless sustain demand for architectural coatings containing emulsion polymers.

Technological Innovation in Bio-Based Emulsion Polymers

Advancements in bio-based emulsion polymer technology are unlocking new market opportunities while addressing sustainability imperatives. Driven by improved polymerization processes that enhance performance characteristics such as higher solid content and reduced water sensitivity, the market is witnessing accelerated innovation.

In September 2023, BASF launched industry-first biomass balance plastic additives that reduce fossil feedstock demand and cut carbon footprints by up to 60%, supporting corporate sustainability goals.

The European Commission's comprehensive policy framework, initiated in November 2022, addresses sourcing, labeling, and utilization of bio-based, biodegradable, and compostable plastics, with the Circular Bio-based Europe Joint Undertaking (CBE JU) allocating €215.5 million for 18 funding topics in 2023, including €10 million dedicated to developing novel, high-performance bio-based polymers.

These innovations enable manufacturers to produce emulsions with improved film-forming properties, enhanced adhesion to challenging substrates, and greater environmental resistance. The development of bio-based catalyst technologies has improved over 25% of production formulas, boosting overall durability and performance while ensuring greener output in industrial applications.

Consumer preference for low-VOC, eco-friendly products continues to drive nearly 40% of businesses toward environmentally safer polymer alternatives, creating sustained momentum for the adoption of bio-based emulsion polymers.

Restraint - Raw Material Price Volatility and Production Cost Pressures

Fluctuations in the prices of key feedstocks, including acrylic acid, methacrylic acid, acrylates, and styrene, create significant cost pressures on polymer emulsion. In 2024 and 2025, volatile pricing for these petroleum-derived raw materials directly impacted emulsion polymer pricing structures, limiting adoption in price-sensitive markets, particularly across developing countries.

The high production costs associated with bio-based emulsion polymers remain a critical barrier, as renewable feedstock sourcing, advanced manufacturing processes, and extensive R&D requirements contribute to overall price premiums compared to conventional petroleum-based alternatives.

Supply chain disruptions and petroleum price fluctuations compound these challenges, leaving manufacturers struggling to maintain competitive pricing while meeting performance standards.

The availability of bio-based raw materials such as renewable plant-based feedstocks is not always consistent or sufficient to meet rising demand, leading to supply chain vulnerabilities that can disrupt bio-based emulsion polymer production in certain regions. These economic constraints slow market penetration in cost-conscious industries, where buyers hesitate despite the environmental and performance benefits of advanced polymer emulsion formulations.

Opportunity - Expansion in Emerging Markets and Infrastructure Megaprojects

Emerging economies offer substantial growth opportunities for emulsion polymer suppliers as urbanization and industrialization drive demand for construction materials. Asia-Pacific, led by China and India, is experiencing rapid industrial expansion, with China intending to increase electric vehicle production to 7 million units per year by 2025, creating demand for automotive-grade emulsion polymers used in coatings and adhesives.

India's paper industry, with 900 mills and 22.73 million tons operating capacity producing 18.91 million tons annually, presents opportunities for emulsion polymers in paper coating applications, which consumed 46% of polymer emulsion demand, equivalent to USD 13.40 billion in 2025.

The European Union's Green Building Pact aims to renovate 35 million buildings by 2030, doubling renovation rates and creating 160,000 new green jobs in the construction sector, driving demand for high-performance, sustainable coatings and construction materials containing emulsion polymers.

Germany received record EUR 57 billion allocation for green infrastructure in 2024, including EUR 18.6 billion for the hydrogen industry and EUR 12.5 billion for rail network expansion through 2027, supporting increased emulsion polymer consumption in industrial and transportation applications.

Governments worldwide are introducing policies to stimulate eco-friendly building construction, with India adopting EU-style REACH frameworks and several Indian states imposing lead paint bans while promoting low-VOC and eco-label paint formulations.

Development of Specialized High-Performance Formulations

Innovation in specialized emulsion polymer formulations for niche applications offers manufacturers opportunities for differentiation and premium pricing. There is a notable shift toward high-performance emulsions designed for specific applications, such as high-gloss coatings, flexible packaging adhesives, and textile binders with improved wash fastness.

The integration of nanotechnology to enhance properties such as scratch resistance, UV durability, and hydrophobicity is expanding the performance envelope of emulsion polymers, positioning suppliers at the forefront of sustainable chemical innovation.

In the medical and industrial sectors, bio-based emulsion polymers are increasingly favored for their biodegradability, non-toxic composition, and excellent film-forming capabilities, making them ideal for sensitive medical applications, including wound care, drug delivery systems, and tissue engineering.

The adhesives and sealants segment represents a substantial growth opportunity as manufacturers replace traditional mechanical fasteners with advanced adhesive solutions that provide weight reduction, improved fuel efficiency, and enhanced safety.

Strategic investments in R&D to develop emulsions with superior adhesion, chemical resistance, and environmental tolerance enable manufacturers to capture premium market segments and differentiate their offerings in increasingly competitive markets.

Category-wise Analysis

Product Type Segment Insights

Synthetic emulsion polymers dominate the global market with an 88.0% share in 2025, reflecting their established performance characteristics, cost-effectiveness, and extensive application versatility across industries.

Acrylic emulsions, a key synthetic polymer category, held a significant share of the global paint and coatings resin market, offering excellent UV resistance, color retention, and quick-drying properties that make them indispensable for architectural and decorative coatings providing superior weather protection.

Styrene-butadiene latex and vinyl acetate polymers complement acrylic formulations, offering specialized performance for applications requiring enhanced flexibility, adhesion, and water resistance. Asia Pacific demonstrates robust growth driven by synthetic polymer consumption in automotive, paint and coatings, and construction industries, supported by rising demand from construction, automotive, and packaging sectors requiring advanced adhesive technologies.

Bio-based emulsion polymers represent the fastest-growing segment, driven by environmental consciousness, regulatory pressures, and technological breakthroughs that enhance performance characteristics while reducing environmental impact.

Bio-based emulsions derived from renewable sources such as plants, crops, and biomass offer reduced carbon footprints and contribute to circular economy initiatives by replacing non-renewable resources with biodegradable alternatives.

Application Segment Insights

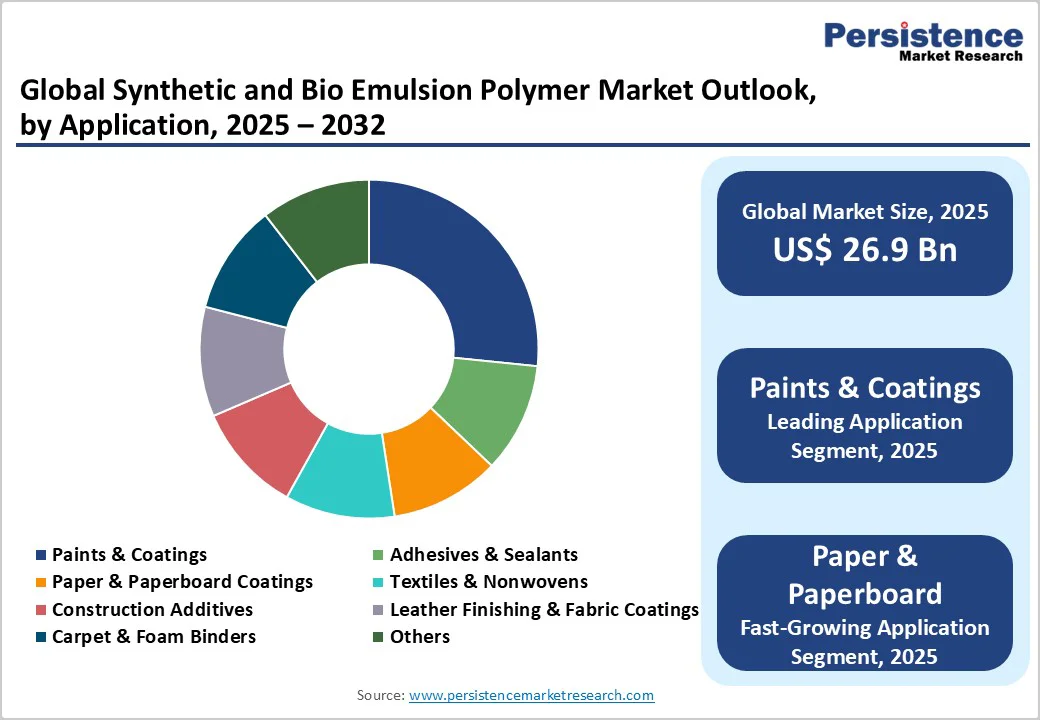

Paints and coatings applications dominate emulsion polymer consumption, holding 38% market share in 2025, reflecting the critical role of polymer binders in enhancing film formation, adhesion, durability, and aesthetic properties. Driven by construction and real estate expansion, automotive industry trends, and stringent environmental regulations, demand for high-performance coatings continues to grow.

Water-based coatings, which rely heavily on emulsion polymers, accounted for 40.8% of the global paints and coatings market revenue in 2024, benefiting from their low-VOC content, ease of application, and minimal odor characteristics. In China, architectural coatings output increased by 12.5% in 2023 due to aggressive urban development and green building mandates, significantly boosting consumption of water-based acrylic emulsions in decorative and protective coatings.

The construction sector's dominance as a consumer of paints and coatings accounting for over 40% of global product demand in 2024 directly translates to sustained emulsion polymer consumption as builders prioritize durable, eco-friendly coating solutions.

The anticipated construction of 600 million urban residents in Chinese cities by 2030 is expected to create demand for 25 million additional housing units, driving long-term emulsion polymer requirements for interior and exterior architectural coatings.

Paper and paperboard applications represent the fastest-growing emulsion polymer segment, driven by expanding packaging demand, increasing paper production capacity, and technological advancements in coating formulations.

India's paper industry operates 900 mills with 22.73 million tons operating capacity, producing 18.91 million tons annually and consuming 22.83 million tons, creating substantial demand for paper coating emulsions that enhance printability, smoothness, and moisture resistance.

Regional Insights and Trends

East Asia Synthetic and Bio Emulsion Polymer Market Trend

East Asia commands the largest regional market share at 32%, driven by China's industrial dominance and rapid urbanization across the region.

The China National Coatings Industry Association reported architectural coatings output increased 12.5% in 2023 due to urban development and green building mandates, significantly boosting water-based emulsion consumption. Government initiatives promoting green chemistry technologies, including Sumitomo Seika (China) Co., Ltd.'s focus on water-soluble polymers and emulsion latex materials offering high sustainability and functionality, support domestic market expansion.

China's Belt and Road Initiative recorded USD 124 billion in construction and investment engagement in H1 2025, nearly doubling the 2024 annual total, with cumulative engagement reaching USD 1.308 trillion since 2013, creating sustained demand for construction materials containing emulsion polymers.

The anticipated urbanization of 600 million people in Chinese cities by 2030, requiring 25 million additional mid-end and affordable housing units, ensures long-term growth trajectories for emulsion polymers in architectural coatings and construction additives. India's growing middle-class population and rising real income are fueling domestic demand, with the country increasingly focusing on trade and investment in domestic markets supported by relatively easy access to finance and a robust local labor market.

North America Synthetic and Bio Emulsion Polymer Market Trend

North America accounts for 20% of the global market, supported by robust construction activity, favorable commercial real estate fundamentals, and increased federal and state funding for infrastructure and institutional buildings.

The United States construction sector is projected to grow steadily from 2024 to 2028, directly benefiting emulsion polymer demand in coatings and adhesive applications. In 2024, U.S. single-family building permits increased across all four regions, sustaining demand for architectural coatings containing emulsion polymers.

The EPA’s amendments to national VOC emission standards for aerosol coatings, finalized in January 2025 with compliance deadlines set for 2027, are accelerating reformulation efforts toward low-VOC water-based emulsions.

Canada’s construction market is the fastest-growing, supported by population growth and expanding housing demand. The U.S. biobased products industry continues to demonstrate strong economic impact, fostering bio-based emulsion polymer development and commercialization efforts.

Europe Synthetic and Bio Emulsion Polymer Market Trend

Europe holds 24% of the global market, characterized by stringent environmental regulations, mature demand for premium sustainable products, and significant renovation activity targeting energy efficiency improvements.

Reflecting steady demand despite mature market conditions, the region continues to benefit from initiatives such as the European Union's Green Building Pact, which targets renovating 35 million buildings by 2030 to achieve a 60% reduction in building-related greenhouse gas emissions, creating substantial demand for energy-efficient coatings and sustainable construction materials.

Germany, as a market leader, received EUR 57 billion allocation for green infrastructure in 2024, including investments in renewable energy, transportation networks, and sustainable construction, supporting increased emulsion polymer consumption across industrial applications.

France's regulatory programs including RT2012 and RE2020 focus on thermal efficiency and energy balance, with Paris leading green public housing and commercial building renovations supported by heavy government subsidies for energy-efficient upgrades.

The EU's Commission Regulation (EU) 2023/2055, effective October 2023, restricts synthetic polymer microparticles and imposes compliance documentation requirements by October 2025, accelerating the transition to compliant water-based emulsion formulations.

The European construction additives market is expected to reach approximately EUR 24 billion by 2030, with increasing utilization of sustainable construction additives for infrastructure development fueling emulsion polymer demand.

Competitive Landscape

The global synthetic and bio emulsion polymer market is moderately consolidated, with competition dominated by a few multinational chemical companies that hold significant technological and production advantages. BASF and Arkema S.A. lead the market through extensive R&D investments and diversified emulsion polymer portfolios serving coatings, adhesives, and construction industries.

Synthomer and Wacker Chemie maintain strong positions with specialized latex and silicone-based dispersions tailored for performance and sustainability. Celanese leverages its polymer chemistry expertise and integration capabilities to expand across packaging and automotive applications, while AkzoNobel focuses on value-added, eco-friendly formulations aligned with tightening environmental regulations.

Continuous innovation, capacity expansion, and bio-based transitions define competition, with major players focusing on product differentiation and regional expansion to strengthen their market presence.

Key Industry Developments:

- In February 2025, AkzoNobel introduced a new waterborne wood coating under its Sikkens Wood Coatings brand, featuring 20% bio-based content. The product, RUBBOL WF 3350, demonstrates the company’s commitment to sustainable innovation in emulsion polymer-based coatings by incorporating renewable raw materials without compromising performance. This development highlights AkzoNobel’s focus on advancing bio-based emulsion polymer technologies to reduce environmental impact and support the transition toward circular, eco-friendly coating solutions.

- In April 2025, Lubrizol launched Carbopol® BioSense polymer, the first readily biodegradable ingredient in its Carbopol® portfolio, developed in partnership with Suzano. This biopolymer enhances viscosity and texture in emulsions, demonstrating strong synergy with synthetic and natural emulsifying systems. With 98% natural origin content, it represents a major advancement in bio-based emulsion polymer technology, offering sustainable, high-performance alternatives for personal care formulations.

Companies Covered in Synthetic and Bio Emulsion Polymer Market

- AkzoNobel

- DIC Corporation

- Celanese

- Arkema S.A.

- BASF

- Omnova Solution

- Nuplex Industry

- Synthomer

- Styron

- Wacker Chemie

- STI Polymer

- Clariant International Limited

- Asahi Kasei

- Momentive Performance Materials Holdings LLC

- Cytec Industries Inc.

- The Lubrizol Corporation

- Financiera Maderera

- Trinseo S.A.

Frequently Asked Questions

The global Synthetic and Bio Emulsion Polymer Market is projected to be valued at US$ 25.4 Bn in 2025.

The Synthetic Emulsion Polymers segment is expected to hold around 88% market share in 2025, driven by its.

The market is poised to witness a CAGR of 5.9% from 2025 to 2032.

The synthetic and bio emulsion polymer market growth is driven by rising demand for eco-friendly, low-VOC coatings and adhesives across construction, automotive, and packaging industries.

The key market opportunities in the synthetic and bio emulsion polymer market include advancements in bio-based raw materials and increasing adoption of sustainable, waterborne formulations in emerging economies.

The top key market players in the global Synthetic and Bio Emulsion Polymer Market include BASF SE, Dow Inc., Arkema S.A., Celanese Corporation, Trinseo PLC, and Synthomer plc.