- Inks, Coatings, Adhesives & Sealants (ICAS)

- Plastic Additives Market

Plastic Additives Market Size, Share, and Growth Forecast, 2025 - 2032

Plastic Additives Market by Polymer Type (Polyethylene (PE), Polypropylene (PP), Polyvinyl Chloride (PVC), Polystyrene (PS), Polyethylene Terephthalate (PET), Acrylonitrile Butadiene Styrene (ABS), Polycarbonate (PC), Polyamide (Nylon), Others), Source, Application, and Regional Analysis for 2025 - 2032

Plastic Additives Market Share and Trends Analysis

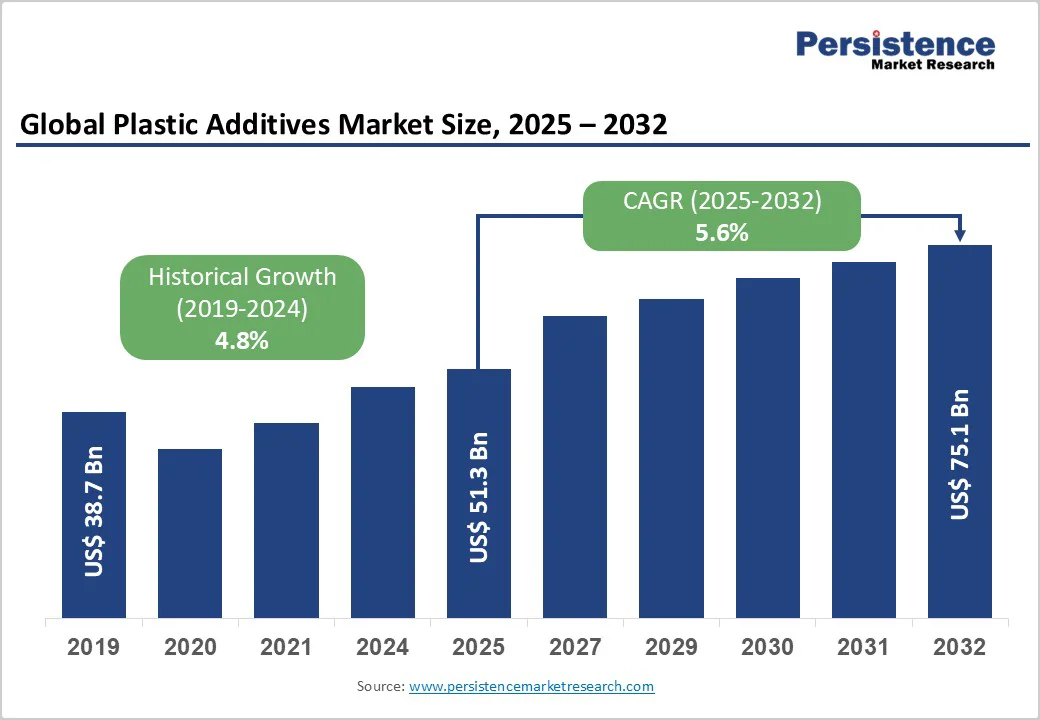

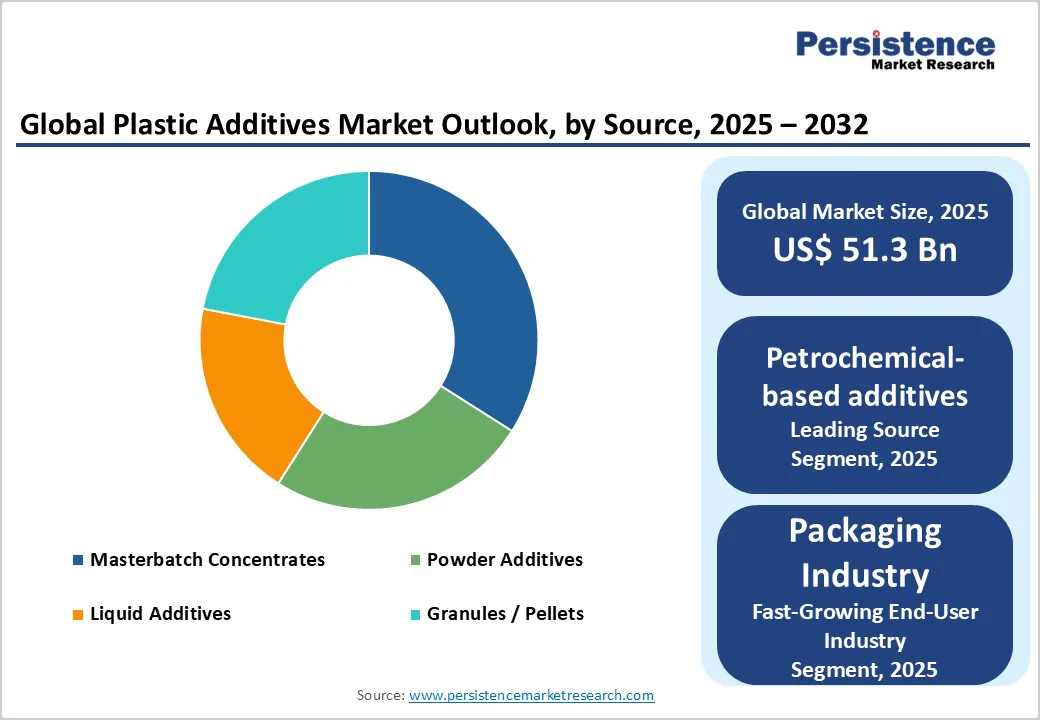

The global plastic additives market size is likely to be valued at US$ 51.3 billion in 2025, and is projected to reach US$ 75.1 billion by 2032, growing at a CAGR of 5.6% during the forecast period 2025 - 2032.

The demand for plastic additives is driven by the accelerating shift toward lightweight, high-performance polymers in industries such as packaging and automotive.

As manufacturers pursue cost reduction and sustainability, additives that enhance recyclability, enable bio-based formulations, and deliver flame retardance, UV protection, and improved mechanical performance are likely to experience high demand.

Key Industry Highlights

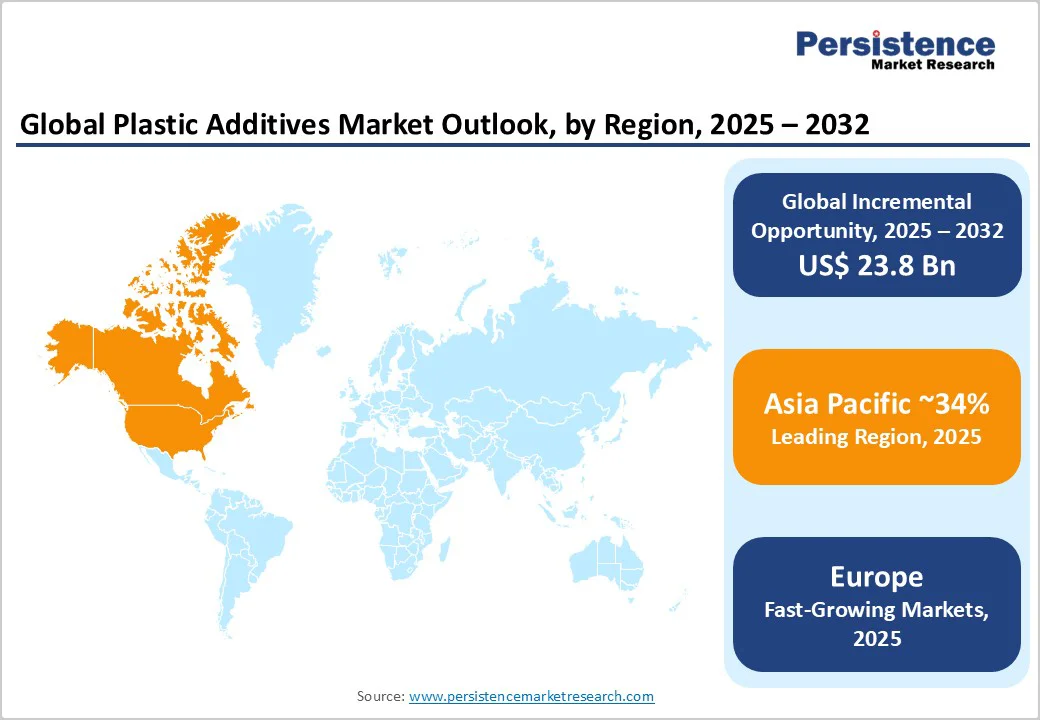

- Leading Region: Asia Pacific is set to dominate with over 55% share in 2025, driven by China’s petrochemical scale-up and India’s growing converter base.

- Fastest-growing Regional Market: Europe is likely to be the fastest-growing regional market through 2032, propelled by stringent recyclability and compostability mandates and robust sustainable additive R&D.

- Dominant Product Type: Polyethylene additives are expected to lead the market with 22% share in 2025, underpinned by high volumes in packaging and geomembrane applications.

- Fastest-growing Source: Bio-based additives are projected to grow at a 9% CAGR through 2032, driven by circular-economy policies and consumer eco-preferences.

- Key Market Opportunity: Development of compostable masterbatches for PLA and PHA blend packaging, aligned with Europe’s 2030 recyclability requirements, presents an excellent opportunity for market players.

| Key Insights | Details |

|---|---|

| Plastic Additives Market Size (2025E) | US$51.3 Bn |

| Market Value Forecast (2032F) | US$75.1 Bn |

| Projected Growth CAGR (2025 - 2032) | 5.6% |

| Historical Market Growth (2019-2024) | 4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growing Need for Electric Vehicle (EV) Lightweighting

The global pivot to electric vehicles as automakers strive to meet CO2 reduction targets is driving significant uptake of plastics in powertrain components, battery enclosures, interior panels, and crash-absorbing structures. The average plastics content per EV is expected to rise from 100 kg in 2020 to over 160 kg by 2030, accounting for roughly 25% of total vehicle mass.

Consequently, the demand for impact modifiers, flame retardants, and thermal stabilizers is surging as plastics must satisfy stringent safety, performance, and longevity requirements. Flame-retardant additives tailored for polyamide battery housings must achieve UL 94 V-0 ratings under elevated thermal cycles, while impact modifiers for polycarbonate blends ensure crash resilience.

Global policies are mandating higher recycled content in plastic products, with the European Union (EU) targeting 50% recycled content in plastic packaging by 2030 and California requiring 65% post-consumer recycled content in rigid plastic containers by 2025. To meet these goals, manufacturers are leveraging compatibilizers and decontamination additives that restore performance characteristics to recycled resins.

Compatibilizers, such as maleic anhydride-grafted polymers, facilitate blending of polyolefins with varying molecular weights, enabling mixed plastic streams to achieve virgin-equivalent tensile strength. In China, government subsidies for r-PET production can boost growth in the plastic additives market, aided by soaring demand for intrinsic viscosity enhancers and color-corrective masterbatches.

Regulatory Constraints on Hazardous Chemistries

Stringent bans on legacy additives are reshaping formulation strategies. The EU’s REACH regulation phased out all chlorinated paraffins above C14 for plasticizers in 2021, while the U.S. Environmental Protection Agency (EPA) restricted certain phthalates in children’s toys and food contact applications.

The phase-out of bisphenol A (BPA) for polycarbonate food packaging in numerous jurisdictions has generated a surge in demand for alternative plasticizers and impact modifiers, increasing compliance costs. Suppliers must invest in toxicological testing and regulatory filings to introduce non-regulated chemistries, which adds R&D expenditure and delays time-to-market.

Feedstock costs for additive manufacturing, particularly specialist intermediates such as halogenated flame retardants, stabilizers, and specialty surfactants, are tied to fluctuations in crude oil and natural gas prices. Between 2021 and 2023, average petrochemical feedstock prices spiked by 30%, resulting in additive resin costs increasing by 15-25%.

Such volatility compresses downstream margins for masterbatch and concentrate producers, who face pressure to absorb cost increases or risk volume declines. Given the fragmented market and limited pricing power among smaller formulators, price swings remain a significant financial risk.

Bio-based and Green Additives

Consumer preferences and legislated mandates for sustainable materials are accelerating the development of bio-plasticizers, natural antioxidants, and enzyme-based stabilizers.

The bio-based additives segment accounted for less than 10% of total market volumes in 2024 but is expected to grow at a 9% CAGR through 2032. Innovations include epoxidized soybean oil as a non-phthalate plasticizer for PVC and mono- and diglyceride compatibilizers for PLA blends.

Major petrochemical companies have established dedicated green chemistry units, investing millions of dollars annually in the process-scale-up of renewable feedstock-derived intermediates.

Europe’s forthcoming Packaging and Packaging Waste Regulation mandates that all plastic packaging be recyclable or compostable. This requirement is creating demand for compostable masterbatches compatible with PLA, PHA, and starch blends.

Antimicrobial additives that preserve food safety during extended shelf life are also in development. Early adopters of ASTM D6400-certified masterbatches have secured supply agreements with major FMCG companies, projecting 18% year-on-year revenue growth for compostable grades through 2026.

Category-wise Analysis

Polymer Type Analysis

Among polymer types, polyethylene (PE) is set to command the largest share at 22% in 2025, owing to its dominance in packaging films, geomembranes, and piping. Additives for PE include antioxidants to prevent thermo-oxidative degradation during processing, slip agents for improved film handling, and UV stabilizers to extend the outdoor durability of agricultural and geomembrane applications.

In 2024, global PE resin production reached 110 million tons, with packaging accounting for 62%. The high volume of use translates to a proportional increase in additive consumption, cementing PE’s leading position.

Source Insights

Petrochemical-based additives account for approximately 85% of the total volume, benefiting from established global supply chains and cost efficiencies. However, bio-based additives are gaining ground, with their share forecast to increase to 15% by 2032 as regulatory pressures and consumer preferences shift toward sustainability.

For businesses closely tied to the plastics industry, addressing sustainability concerns is a critical step toward attracting investments, making bio-based additives even more important for market development. Moreover, bio-based plasticizers and antioxidants are particularly prevalent in food-contact and personal care applications, where non-toxic claims are critical.

Application Insights

The packaging application is poised to dominate, with a 31% share of the plastic additives market in 2025, reflecting the high volume of plastic film and rigid packaging worldwide. Additives such as slip agents, anti-fog additives, and nucleating agents improve clarity, handling, and stiffness, respectively.

With global plastic packaging volumes exceeding 100 million tons in 2024 and a recycling rate of only 32%, packaging stakeholders are investing in additives that enhance recyclate performance and meet circular-economy goals, further driven by policy directives and investor sentiment.

Regional Insights

North America Plastic Additives Market Trends

The North American market, led by the United States, benefits from a robust innovation ecosystem and early adoption of advanced flame retardants for electronics, appliances, and EV applications. Federal and state-level bans on PFAS and certain phthalates have prompted formulators to accelerate the development of non-regulated alternatives.

The incentives offered under the Inflation Reduction Act for the use of recycled plastic in packaging —tax credits up to 20% —are catalyzing investments in compatibilizers and decontamination additives. Similarly, in Canada, provincial bans on chlorinated additives in children's products have further nourished the demand for novel flame-retardant technologies.

Europe Plastic Additives Market Trends

Europe is at the forefront of regulatory harmonization and circular economy initiatives. The Packaging and Packaging Waste Regulation, effective in 2025, requires that 100% of plastic packaging be reusable or recyclable by 2030.

Germany and France have been investing heavily in R&D for bio-based plasticizers and high-performance flame retardants, while Spain and the U.K. are deepening their focus on compostable additive systems. The recyclability targets of the automotive sector, aimed at reusing 85% of end-of-life vehicles by 2035, are also driving the development of additives that enable polymer recovery and pyrolysis.

Asia Pacific Plastic Additives Market Trends

Asia Pacific is anticipated to dominate the plastic additives market, accounting for about 55% of revenues in 2025, driven by China’s push toward petrochemical self-sufficiency and India’s liberalized foreign investment in specialty chemicals.

Rapid urbanization, infrastructure expansion, and burgeoning middle-class consumption are boosting the demand for additives in packaging and construction. Japan and South Korea lead in high-performance electronics additives, while Southeast Asian nations such as Thailand and Vietnam have emerged as hubs for masterbatch production, supporting regional packaging and automotive converter industries.

Competitive Landscape

The global plastic additives market is highly fragmented, with the top 10 companies accounting for approximately 40% of revenue. Key players such as BASF SE, Clariant AG, Dow Chemical Company, and Evonik Industries AG focus on broad portfolios spanning sustainable and high-performance additives.

Establishing compounding and masterbatch facilities near resin plants in Asia and North America to reduce logistics costs and allocating a sizeable amount of financial resources toward green additive chemistries are the mainstay strategies of these companies.

In addition, collaborative innovation through partnerships with OEMs and academic institutions to co-develop additive solutions certified for medical, automotive, and packaging applications is being leveraged as a major opportunity.

Key Industry Developments

- In October 2025, researchers at Georgia Tech developed a sustainable recycling method that uses mechanical collisions to break down polyethylene terephthalate (PET) plastics into their basic components without heat or harsh chemicals. By impacting PET with metal balls, the process triggers chemical reactions, especially with sodium hydroxide, at room temperature, enabling efficient depolymerization. This "mechanochemical" technique accelerates recycling while reducing energy consumption and environmental impact. Mapping energy distribution from collisions helps optimize the process for industrial applications, potentially closing the loop on plastic waste by enabling repeated recycling of PET and other challenging plastics.

- In October 2025, SI Group announced a partnership with Azelis to expand its plastics additives distribution network across the EMEA region starting in January 2026. This collaboration enhances SI Group’s market reach by leveraging Azelis’ sales expertise and warehousing capabilities in numerous countries, including Nordic states, France, Italy, the U.K., and Eastern Europe. The partnership aims to deliver tailored solutions, improve customer access, and support SI Group’s strategic growth in the evolving plastics industry with a strong focus on innovation and localized service.

- In June 2025, Sumitomo Chemical developed mass-production technology for liquid crystal polymer (LCP) using monomers derived from biomass, aiming to launch bio-based LCP products by fiscal 2027. LCP, known for its heat and fire resistance, is widely used in electronics, automotive parts, and office equipment. The company employs a segregation approach that separately controls biomass content during production, ensuring clear disclosure of biomass use, alongside a mass balance method that blends biomass and fossil materials. This innovation supports sustainable societal goals by reducing reliance on fossil resources and lowering greenhouse gas emissions, leveraging advances in synthetic biology and digital technology integration.

Companies Covered in Plastic Additives Market

- Songwon Industrial Co. Ltd.

- Clariant AG

- BASF SE

- Dow Chemical Company

- Evonik Industries AG

- Kaneka Corporation

- Lanxess AG

- SABIC

- ExxonMobil Chemical

- Mitsui Chemical

- Albemarle Corporation

- Nouryon

Frequently Asked Questions

The global plastic additives market is likely to be valued at US$ 51.3 billion in 2025.

The primary market driver is the increasing lightweighting of electric vehicles, with the incorporation of plastics EVs targeted to reach 25%, boosting the demand for flame retardants and impact modifiers.

The market is poised to witness a CAGR of 5.6% from 2025 to 2032.

The development of compostable masterbatches for PLA blends presents significant upside under the Europe Union (EU)’s 2030 recyclability mandates.

The top market players are BASF SE, Clariant AG, and Dow Chemical Company.