- Specialty & Fine Chemicals

- Synthetic Zeolite Y Adsorbent Market

Synthetic Zeolite Y Adsorbent Market Size, Share, and Growth Forecast, 2026-2033

Synthetic Zeolite Y Adsorbent Market by Product Type (NaY Zeolite, Ultrastable Y (USY) Zeolite, Rare-Earth Exchanged (REY) Zeolite, Others), Application (Water Treatment, Gas Separation, VOC Emission Control, Others), End-Use Industry (Petrochemical, Oil, Water Treatment, Others), and Regional Analysis for 2026-2033

Synthetic Zeolite Y Adsorbent Market Share and Trends Analysis

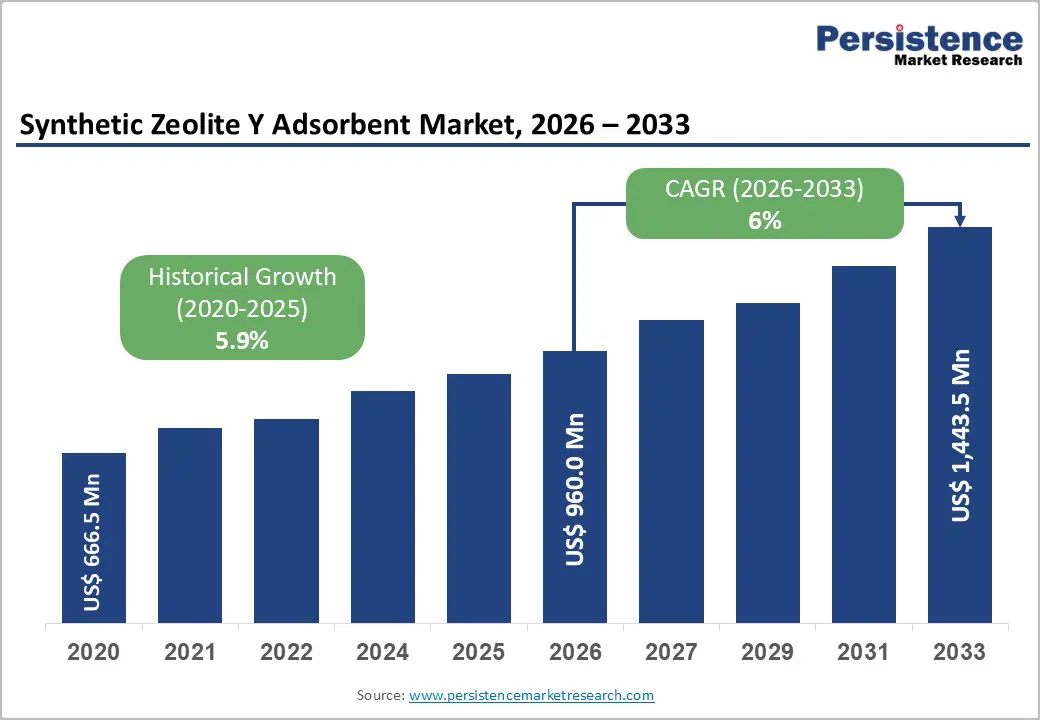

The global synthetic zeolite Y adsorbent market size is likely to be valued at US$ 960.0 million in 2026, and is projected to reach US$ 1,443.5 million by 2033, growing at a CAGR of 6% during the forecast period of 2026–2033.

The market continues to demonstrate stable expansion, supported by sustained demand from refinery catalyst applications, industrial gas purification systems, and increasingly stringent environmental regulations targeting volatile organic compound (VOC) emissions. Refinery modernization programs across Asia Pacific are accelerating adoption of high-performance fluid catalytic cracking (FCC) catalysts containing Ultrastable Y variants. At the same time, wastewater treatment investments aligned with United Nations Sustainable Development Goals (UN SDGs) are strengthening demand for adsorption-based purification technologies. Industrial decarbonization policies in North America and Europe further reinforce market stability, as regulatory compliance, energy efficiency mandates, and emissions control frameworks drive consistent integration of advanced zeolite-based solutions across multiple industrial sectors.

Key Industry Highlights

- Dominant Product Types: USY zeolite is set to command around 50% revenue share in 2026, while REUSY zeolite is likely to grow at the highest 2026-2033 CAGR, driven by higher efficiency requirements in modern FCC units.

- Leading Applications: Gas separation is expected to lead in 2026, while water treatment is projected to be the fastest-growing through 2033, supported by tightening environmental discharge regulations.

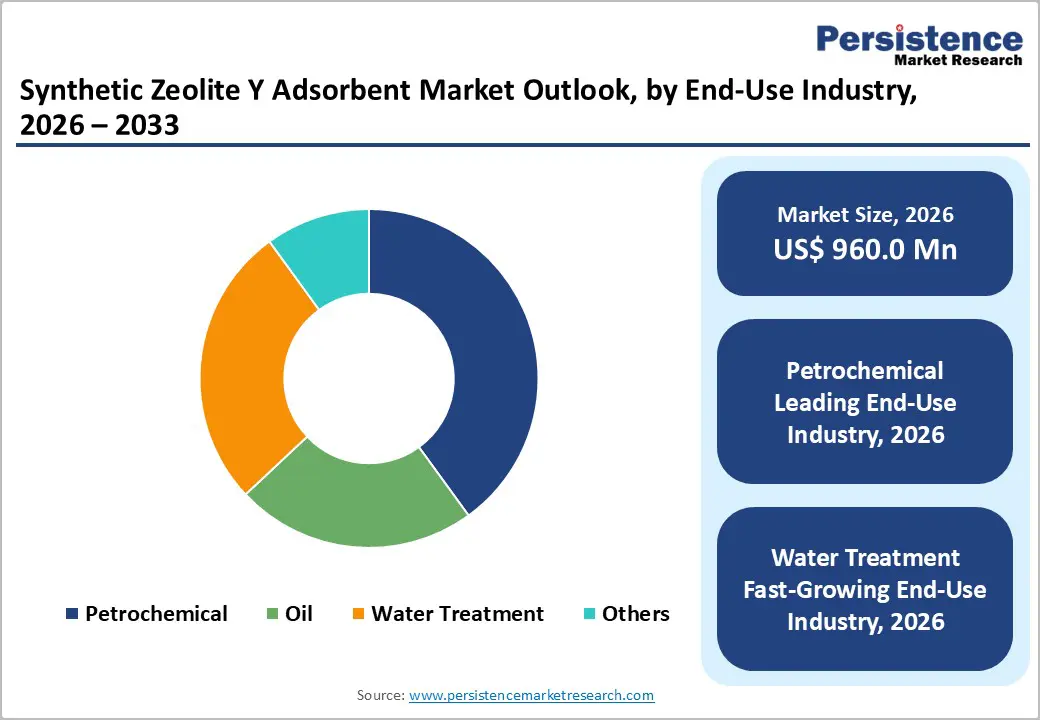

- Dominant End-Use Industry: The petrochemical industry is anticipated to account for over 40% of the market demand in 2026, reflecting refinery integration strategies.

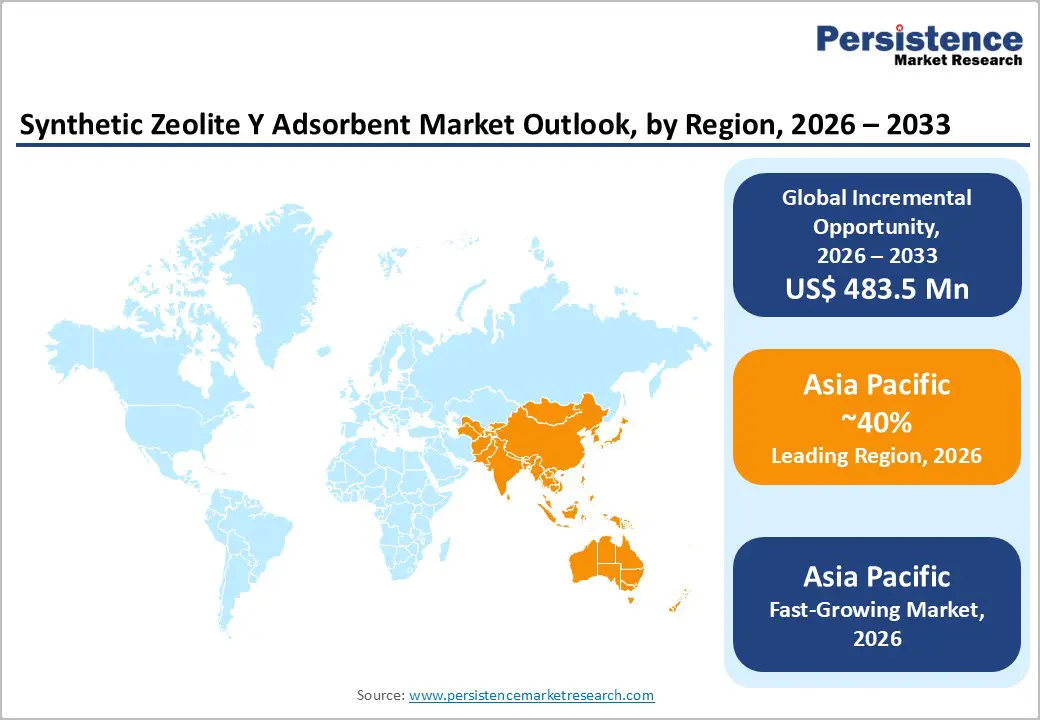

- Regional Leadership: Asia Pacific is poised to dominate with nearly 40% market share in 2026 and register the highest growth through 2033, led by refinery expansions in China and India.

- Competitive Environment: Market competition centers on refinery upgrade collaborations, advanced catalyst innovation, VOC compliance solutions, and hydrogen economy integration strategies.

| Key Insights | Details |

|---|---|

|

Synthetic Zeolite Y Adsorbent Market Size (2026E) |

US$ 960.0 Mn |

|

Market Value Forecast (2033F) |

US$ 1,443.5 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Refinery Capacity Expansion and Cleaner Fuel Mandates Driving Catalyst Demand

According to the International Energy Agency (IEA), global refinery capacity surpassed 102 million barrels per day in 2024, with expansions concentrated in China, India, and the Middle East. FCC units account for nearly 35% of global gasoline production capacity and rely heavily on USY zeolite catalysts. Zeolite Y serves as the core active component in FCC catalysts due to its optimized pore geometry and acidity profile. Refinery modernization programs aimed at improving conversion efficiency are increasing catalyst replacement cycles. Upgrades aligned with Euro VI and equivalent emission standards further reinforce demand. This structural reliance ensures steady consumption across large-scale refining operations.

The U.S. Environmental Protection Agency (EPA) outlined revisions to wastewater rules for the oil and gas sector, promoting sustainable reuse of produced water in industrial settings. These regulatory shifts encourage investment in advanced treatment technologies at refineries, including adsorption-based purification solutions that leverage zeolite catalysts and adsorbents to meet reuse and emissions targets. At the same time, tightening global fuel-quality standards for sulfur and nitrogen emissions continue to push refiners toward higher-performance catalyst systems, reinforcing demand for zeolite-based cracking solutions.

Environmental Regulations Accelerating Water Treatment and VOC Control Investments

The 2024 UN Water Development Report states that over 2 billion people live in water-stressed regions, prompting significant infrastructure investments in adsorption-based treatment technologies. Governments in India and Southeast Asia increased water treatment budget allocations by 12–18% between 2022 and 2025. Zeolite Y demonstrates strong ion-exchange capabilities for heavy metal removal and ammonium adsorption. Municipal plants are increasingly incorporating synthetic zeolites in tertiary polishing stages. Regulatory tightening under revised wastewater directives in Europe is reinforcing adoption. These compliance-driven upgrades are expanding the addressable market for high-performance adsorbents.

Recent developments indicate rapid growth in industrial water reuse and zero liquid discharge (ZLD) installations, driven by regulatory pressure and sustainability targets. Government programs such as Swachh Bharat Mission and AMRUT 2.0 are supporting integrated wastewater infrastructure upgrades across India, significantly expanding demand for advanced tertiary treatment solutions capable of removing trace contaminants. Additionally, global industrial water treatment systems are evolving to integrate smart monitoring and digital optimization tools that improve efficiency and reduce chemical usage, reinforcing demand for high-selectivity adsorbents such as synthetic zeolites.

Volatility in Raw Material and Energy Costs Impacting Production Economics

Synthetic zeolite Y production depends on sodium silicate and alumina sources. In 2025, global alumina prices experienced fluctuations exceeding 15% due to energy price variability and supply chain disruptions in bauxite-producing countries. Rising electricity tariffs also increase hydrothermal synthesis costs. The manufacturing process is energy-intensive, particularly during crystallization and calcination stages. Any instability in upstream raw material availability directly affects production scheduling. These cost pressures are particularly pronounced in regions dependent on imported alumina feedstock.

Recent government data and industry pricing reports highlight continuing volatility in alumina and bauxite supply dynamics. Australia’s Department of Industry Science and Resources warned that global alumina supply was expected to remain under price pressure amid fluctuating trade barriers and uneven demand growt, keeping producers’ input costs unpredictable. Also, alumina producers in China pushed capacity to record levels, creating oversupply conditions that exert downward pressure on prices while cash costs remain elevated for many facilities, indicating tight economics for operational planning. This dual pressure, cost swings and inconsistent raw material pricing, reinforces margin uncertainty for zeolite manufacturers reliant on these feedstock sources.

Competitive Pressure from Alternative Adsorbent Technologies

Activated carbon and advanced metal-organic frameworks (MOFs) compete in gas separation and VOC control applications. Activated carbon remains 10–20% cheaper in bulk procurement for industrial users. In cost-sensitive markets, procurement decisions often prioritize upfront material pricing over lifecycle efficiency. This creates substitution pressure in non-catalytic applications such as solvent recovery and basic gas drying. MOFs, while still emerging, are gaining research attention due to their tunable pore structures and emerging industrial demonstrations of exceptional separation performance. These alternatives intensify competitive dynamics in selected end-use segments.

Further supporting this trend, independent research and materials science news highlighted next-generation activated carbon formulations achieving ultramicroporous selectivity levels previously dominated by other adsorbents. For example, engineered CO-activated carbon materials developed by academic teams have demonstrated ultra-high uptake and selectivity for industrial gas separations at lower regeneration temperatures, potentially narrowing performance gaps with zeolites. Simultaneously, publishing in peer-reviewed materials science outlets has outlined ongoing advances in MOF-based VOC adsorption technologies, showing adsorption capacities competitive with traditional materials. These technological advancements, observable at pilot and research scale, signal increasing competitive pressure on zeolite-centric solutions, particularly where cost sensitivity outweighs extremal thermal or hydrothermal stability requirements.

Hydrogen Economy Expansion and Refinery Modernization Synergies

Hydrogen production capacity globally expanded significantly by 2024, with regulatory frameworks increasingly supporting low-carbon hydrogen deployment. In early 2025, the U.S. Department of the Treasury released final rules for the Clean Hydrogen Production Tax Credit (45V), providing investment certainty and tax incentives that accelerate deployment of hydrogen production projects and clean hydrogen hubs across North America, while ensuring lifecycle emissions standards are met. This enhances long-term demand for high-purity gas separation and adsorption technologies.

Aligned with this momentum, the European Union (EU) launched the Hydrogen Mechanism under its Energy and Raw Materials Platform in January 2026, connecting hydrogen supply offers with industrial off-takers to strengthen renewable hydrogen procurement and market formation. This policy reflects a growing regulatory emphasis on scaling hydrogen supply chains and infrastructure across Europe. Together with refinery modernization programs such as integrated hydrogen infrastructure deployment, these developments expand the adoption landscape for synthetic zeolite adsorbents in gas purification and advanced catalyst systems, supporting zeolite-driven growth trajectories.

Industrial Water Reuse and Advanced Treatment Integration

Advanced wastewater treatment and reuse protocols are now gaining binding legislative force in key industrial economies. On January 1, 2025, the EU’s revised Urban Wastewater Treatment Directive entered into force, setting higher treatment standards, expanded pollutant monitoring requirements, and stronger mandates for treated wastewater reuse across urban and industrial applications. The directive’s provisions, including wider tertiary treatment and expanded reuse promotion, directly support the deployment of adsorption-based polishing technologies capable of removing trace contaminants such as nitrogen, phosphorous, and micro-pollutants.

Supporting this regulatory shift, related EU rules on minimum water reuse requirements have stimulated broader acceptance of treated wastewater applications beyond agriculture, including industrial processes where high-stability adsorbents are critical to meeting quality thresholds. These legislative advances create structural demand for advanced tertiary treatment solutions in industrial reuse frameworks. As companies and municipalities adapt infrastructure to comply with stricter reuse standards, synthetic zeolites capable of selective heavy metal and charged species removal capture an expanding share of the treatment technology ecosystem.

Category-wise Analysis

Product Type Insights

Ultrastable Y (USY) zeolite remains the dominant product type with an estimated 48% share of global demand in 2026, driven by its extensive use in FCC catalysts for modern refineries. Its superior hydrothermal stability allows longer service life under high temperature cracking conditions, improving throughput and fuel yields. In late 2025, the European Union’s Renewable Hydrogen Bank linked renewable hydrogen supplies to industrial off takers, indirectly supporting hydrogen enhanced FCC configurations and reinforcing USY demand. USY’s advantages are further highlighted by projects such as Air Liquide’s 200 MW Normand’Hy renewable hydrogen facility in France, advancing hydrogen integration and refinery decarbonization strategies while leveraging high-performance catalyst architectures.

Rare earth exchanged Y (REUSY) zeolite is projected to grow at a CAGR exceeding 6.5% through 2033, fueled by its enhanced cracking activity that improves gasoline yield and octane ratings. Its balanced acidity and hydrothermal stability make it ideal for high-performance FCC catalysts. The European hydrogen and decarbonization policy frameworks encouraged refiners to adopt higher-performance catalyst variants like REUSY to meet clean fuel standards and optimize output. Rising petrochemical demand and refinery modernization initiatives across Asia Pacific and Europe continue to accelerate REUSY adoption, establishing it as the fastest-growing product segment in the synthetic zeolite Y market.

End-Use Industry Insights

The petrochemical sector is anticipated to account for roughly 40% of the total zeolite Y demand in 2026, driven by FCC catalyst applications for gasoline and light olefin production. Zeolite-based catalysts enable optimal feedstock conversion and product selectivity while supporting refinery decarbonization strategies. In 2025, Air Liquide and TotalEnergies announced multi-billion-euro investments in green hydrogen infrastructure integrated with petrochemical operations in Europe, strengthening catalyst demand for decarbonized refining processes. Growing petrochemical output and environmental compliance requirements ensure that Zeolite Y remains structurally embedded in this end-use segment.

The water treatment industry is slated to be the fastest-growing end user, projected to display a CAGR of 6.5% through 2033, driven by industrial water recycling, zero liquid discharge systems, and stricter discharge standards. Zeolite Y is increasingly used in adsorption polishing units to remove trace contaminants and meet reuse requirements. The industrial water reuse and closed-loop treatment projects across Europe and East Asia highlighted adoption of high-performance tertiary systems that leverage synthetic zeolites. These initiatives, coupled with global focus on sustainable water management, are creating strategic growth opportunities for advanced adsorption solutions.

Regional Insights

North America Synthetic Zeolite Y Adsorbent Market Trends

North America is positioned as a stable market for synthetic zeolite Y, led by the United States, where EPA regulations have broadened compliance requirements for industrial wastewater and emissions. Proposed revisions to wastewater rules under the Clean Water Act and expanded contaminant analysis methods are encouraging facilities to upgrade treatment systems and integrate advanced adsorption technologies. Stricter effluent and VOC emission guidelines continue to drive demand for high-performance adsorbents in industrial and municipal applications. Adoption is particularly strong in sectors with complex chemical effluents, where zeolite Y’s selective adsorption capabilities are critical.

Infrastructure modernization complements regulatory drivers, with state-level frameworks promoting industrial water reuse and closed-loop treatment systems. Revisions to major EPA permitting standards in early 2026 reinforce structural adoption of tertiary and quaternary purification technologies. Investment in hydrogen hubs and carbon capture infrastructure further strengthens zeolite Y demand for gas separation and purification systems. Coupled with technological innovation in catalyst development, North America remains a technologically advanced, regulation-driven market with steady, innovation-led growth prospects.

Europe Synthetic Zeolite Y Adsorbent Market Trends

Europe is a compliance-focused market shaped by decarbonization and clean energy policies, led by Germany, the U.K., France, and Spain. In July 2025, the European Commission launched the EU Energy and Raw Materials Platform, including its Hydrogen Mechanism, to link suppliers and buyers of renewable and low-carbon hydrogen, enhancing industrial competitiveness and decarbonization efforts. By early 2026, over 260 hydrogen project supply offers were submitted, demonstrating active market engagement and reinforcing hydrogen-linked industrial transitions. Industrial sectors are increasingly integrating adsorption systems and advanced FCC catalysts to comply with stricter EU energy and emissions targets.

EU-wide regulatory developments, including pending updates to emissions and water treatment policies, continue to support demand for advanced FCC catalysts and adsorption systems. Expansion of electrolyser manufacturing and green hydrogen auction programs in 2025–2026 promotes adoption of specialized zeolite products. Energy price volatility and raw material costs remain structural constraints, but coordinated policy frameworks provide predictable, compliance-driven adoption paths for zeolite Y technologies in industrial and municipal sectors. Strong cross-border collaboration and harmonized standards enhance long-term market stability.

Asia Pacific Synthetic Zeolite Y Adsorbent Market Trends

Asia Pacific is expected to dominate with over 40% of the synthetic zeolite Y market share in 2026 and is also poised to be the fastest-growing market through 2033, driven by rapid industrialization, refinery expansions, and clean energy policy frameworks. The APEC Green Hydrogen Roadmaps initiative in August 2025 provided the necessary impetus to accelerate hydrogen development across member economies, supporting adoption of advanced gas separation and purification systems. Partnerships between East Asian countries on carbon capture and hydrogen deployment underscore the region’s energy transition momentum. National incentives for low-carbon projects and industrial decarbonization further enhance adoption of high-performance Zeolite Y in gas separation and emission control.

Large-scale production for refining, chemicals, and industrial infrastructure drives adoption of tertiary water treatment and emission control systems. Advanced material deployments in Southeast Asian industrial zones in 2025–2026 are expanding capabilities to meet stricter effluent and reuse standards. Government support for petrochemical expansion and hydrogen infrastructure, coupled with favorable manufacturing economics, reinforces Asia Pacific’s role as the primary global growth engine for synthetic zeolite Y applications. Rapid urbanization, infrastructure modernization, and energy transition policies continue to create new opportunities for industrial adoption.

Competitive Landscape

The global synthetic zeolite Y adsorbent market structure is moderately consolidated, with leading players such as BASF, Zeochem, Honeywell UOP, Grace, and Clariant collectively controlling a significant portion of the total revenues. These established companies leverage their extensive industrial relationships, technical expertise, and integrated catalyst and adsorbent portfolios to maintain leadership. They are also investing heavily in R&D and process optimization, developing high-stability zeolite variants, advanced FCC catalysts, and adsorption systems for VOC control, gas separation, and wastewater treatment applications.

Regional and niche competitors, including Nippon Steel & Sumikin Chemical, Tosoh, and Süd-Chemie, focus on specialized product grades, rare-earth exchanged zeolites, and localized market segments. Barriers such as high production costs, regulatory compliance, and complex process integration limit new entrants. However, trends like industrial decarbonization, hydrogen adoption, and digital monitoring of catalytic performance are enabling technology-focused firms to collaborate with major producers. Market consolidation is likely to grow gradually through strategic acquisitions, technology partnerships, and expansion into emerging regions, while product innovation and process efficiency continue to differentiate market leaders.

Key Industry Developments

- In February 2026, Massachusetts Institute of Technology (MIT) researchers developed a diffusion-based AI model called DiffSyn that predicts optimal synthesis pathways for complex materials such as zeolites, significantly reducing trial-and-error experimentation and accelerating materials discovery timelines. The model has already enabled the successful creation of a new zeolite with improved thermal stability, demonstrating potential to overcome one of the largest bottlenecks in translating theoretical materials into real-world applications.

- In December 2025, researchers at the Australian Nuclear Science and Technology Organisation (ANSTO) engineered a silver-infused zeolite material that selectively captures xenon over krypton with more than 1,600 times higher affinity, offering a reusable and energy-efficient alternative to conventional cryogenic gas separation methods for industrial applications.

- In September 2025, Technip Energies agreed to acquire Ecovyst’s Advanced Materials & Catalysts business, including Zeolyst International and specialty zeolites, for US$ 556 million, enhancing its capabilities in hydrocracking catalysts and advanced material solutions.

Companies Covered in Synthetic Zeolite Y Adsorbent Market

- BASF SE

- W.R. Grace & Co.

- Honeywell UOP

- Clariant AG

- Arkema Group

- Tosoh Corporation

- Zeochem AG

- PQ Corporation

- KNT Group

- Chemiewerk Bad Köstritz

- Sorbead India

- Gujarat Credo Mineral Industries

- Union Showa

Frequently Asked Questions

The global synthetic zeolite Y adsorbent market is projected to reach US$ 960.0 million in 2026.

Key drivers include refinery catalyst demand, industrial gas purification, and stricter environmental regulations on VOC emissions.

The market is poised to witness a CAGR of 6% from 2026 to 2033.

Key Opportunities include hydrogen economy adoption, emerging market refinery upgrades, and advanced wastewater recycling technologies.

BASF, Zeochem, Honeywell UOP, Grace, and Clariant are some of the key players in the market.