- Semiconductor Materials & Components

- Semiconductor Lift-off Resists Market

Semiconductor Lift-off Resists Market Size, Share, and Growth Forecast, 2026 - 2033

Semiconductor Lift-off Resists Market by Product Type (Software, Services, Hardware), Technology Node (EUV, DUV (ArF/KrF), i-line/g-line, Misc.), Application (Logic Devices, Memory Devices, Analog & Mixed Signal, Power/Discrete Industry (Consumer Electronics, Automotive, Data Centers/AI, Industrial, Misc.) and Regional Analysis for 2026 - 2033

Semiconductor Lift-off Resists Market Size and Trends Analysis

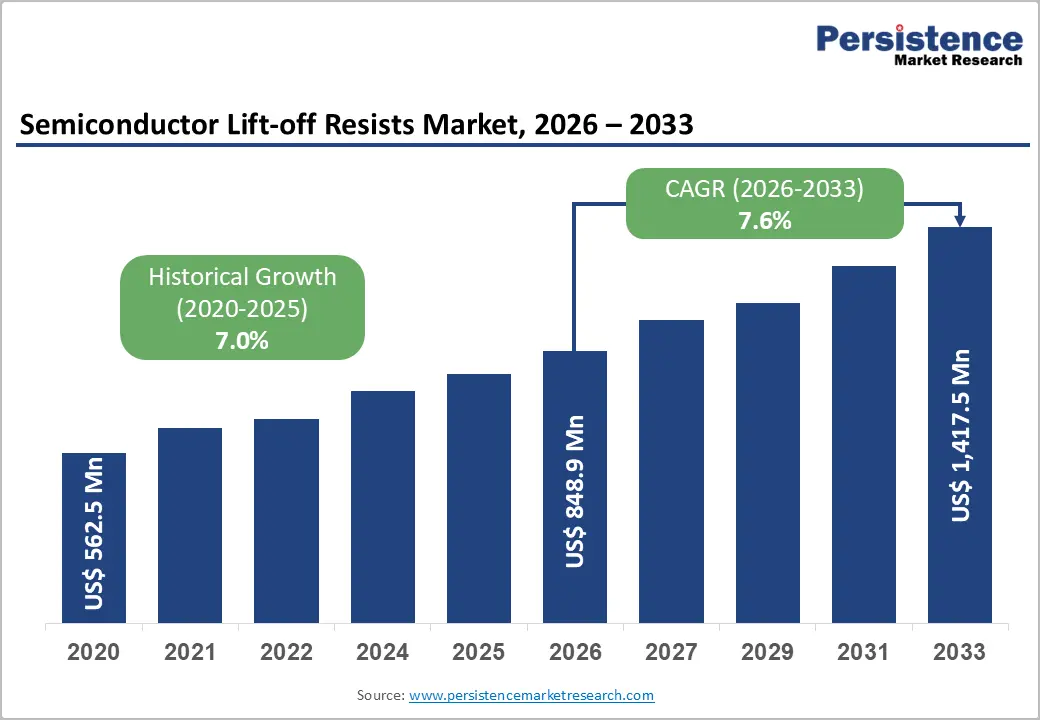

The global semiconductor lift-off resists market size is likely to be valued at US$ 848.9 Million in 2026 and is projected to reach US$ 1,417.5 Million by 2033, growing at a CAGR of 7.6% between 2026 and 2033.

The Market continues to experience robust expansion driven by accelerating demand for advanced semiconductor manufacturing processes, particularly in high-density fabrication and nanoscale patterning technologies. Rising capital commitments to domestic semiconductor production infrastructure, coupled with global semiconductor industry momentum evidenced by record-breaking monthly sales of US$ 75.3 billion in November 2025 are substantially strengthening demand for sophisticated resist materials essential to next-generation lithography.

Enhanced investments in artificial intelligence data centers, electrified automotive platforms, and advanced computing applications are fundamentally increasing chip complexity and manufacturing precision requirements, necessitating sophisticated lift-off resist solutions across leading-edge production facilities.

Key Industry Highlights:

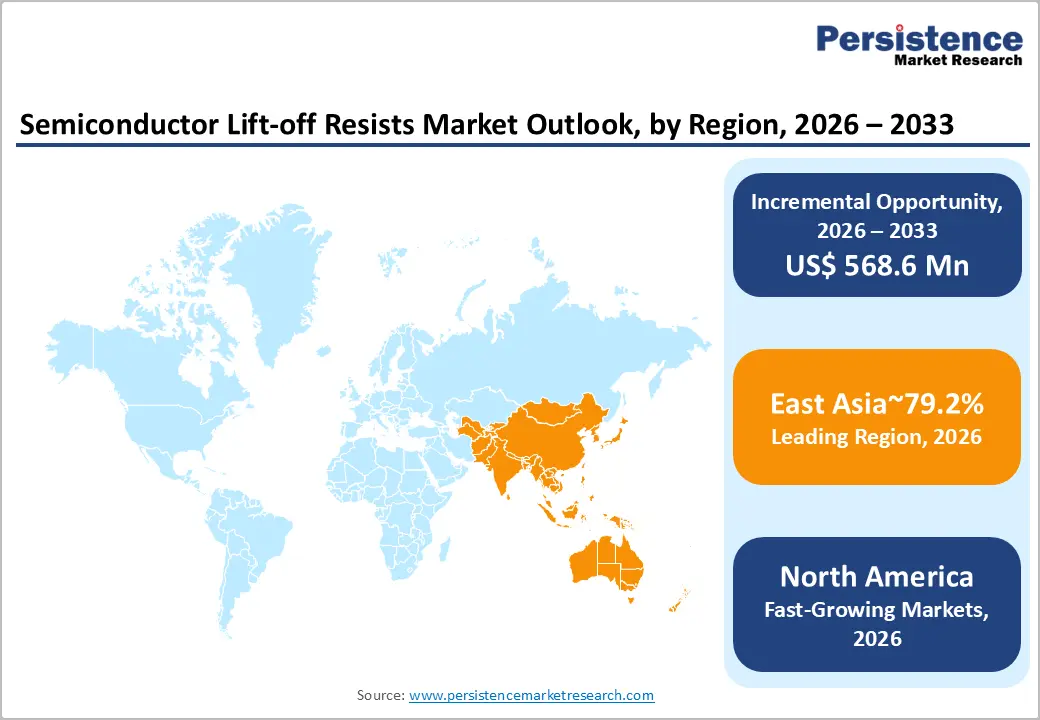

- Regional Leadership: East Asia leads the Global Semiconductor Lift-off Resists Market with 79.2% share, driven by concentrated advanced-node fabrication in Taiwan, South Korea, and China, alongside heavy EUV adoption and large-scale foundry capacity expansions.

- Emerging North American Hub: North America holds a 9% share, supported by CHIPS Act incentives, over 100 new fab projects, and multi-billion-dollar investments from Intel, TSMC, and Samsung, which are accelerating domestic materials demand.

- Strategic European Presence: Europe accounts for 6% share, driven by specialized manufacturing in automotive, analog, and power semiconductors, with a growing focus on advanced packaging and research-led fabrication initiatives.

- Leading Product Segment: Positive Photoresists dominate with 62.3% share, benefiting from process maturity, high reliability, and broad compatibility with DUV and immersion lithography platforms.

- Fastest-Growing Product Segment: Negative Photoresists are the fastest-growing, supported by superior line-width control and increasing adoption in nanoimprint and next-generation EUV patterning applications.

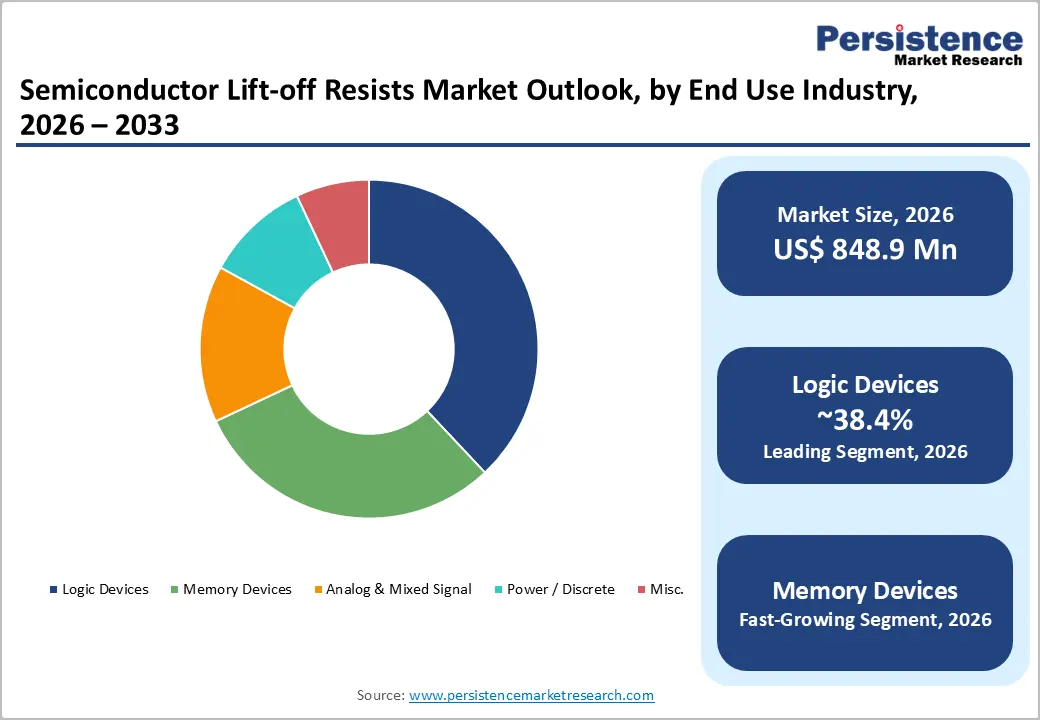

- Leading Application Segment: Logic Devices command a 38.4% share, driven by rising demand for AI processors, GPUs, and advanced computing chips that require ultra-high-resolution lithography.

| Key Insights | Details |

|---|---|

| Semiconductor Lift-off Resists Market Size (2026E) | US$ 848.9 Mn |

| Market Value Forecast (2033F) | US$ 1,417.5 Mn |

| Projected Growth (CAGR 2026 to 2033) | 7.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.0% |

Market Dynamics

Drivers - Advanced Lithography Process Adoption and Nanoscale Fabrication Precision

The semiconductor industry's transition toward increasingly sophisticated lithography technologies, particularly extreme ultraviolet (EUV) and nanoimprint lithography, represents a fundamental structural driver for the Semiconductor Lift-off Resists Market. Advanced nodes below 7 nanometers require exceptionally high-resolution photoresists capable of achieving sub-20-nanometer critical dimensions with minimal line-width roughness and defect-free pattern transfer. Fujifilm Corporation's February 2025 presentation at SPIE Advanced Lithography plus Patterning demonstrated advanced EUV resist and developer innovations, including negative-tone and nanoimprint resist technologies that deliver improved high-resolution patterning with reduced line fluctuation, directly strengthening next-generation semiconductor resist material applications.

The global semiconductor industry's record-breaking monthly sales of US$ 75.3 billion in November 2025 representing a 29.8 percent year-over-year increase compared to November 2024 reflects extraordinary demand acceleration across consumer electronics, artificial intelligence infrastructure, and automotive segments, all requiring advanced fabrication technologies.

The semiconductor lift-off resists market benefits directly from this manufacturing complexity expansion, as more manufacturers pursue advanced node production and higher integration densities. Projections for U.S. fabrication capacity expansion of more than 200 percent by 2032, effectively tripling domestic output, signal sustained investment in manufacturing facilities requiring sophisticated lift-off resist solutions throughout multi-year facility buildouts.

Expansion of Semiconductor Manufacturing Capacity and CHIPS Act Investments

Landmark policy initiatives and substantial capital commitments are fundamentally reshaping semiconductor manufacturing geography and production volumes, creating direct demand acceleration for supporting chemical materials including lift-off resists. The U.S. semiconductor industry is experiencing unprecedented momentum, with over 100 new fabrication, research, and packaging projects announced across 28 states, representing over half-a-trillion dollars in private-sector commitments and projected to generate hundreds of thousands of high-skilled manufacturing positions. By 2032, U.S. fabrication capacity is projected to expand by more than 200 percent, increasing the nation's share of global fab capacity from approximately 10 percent to 14 percent, marking the first sustained reversal of manufacturing decline in decades.

The Semiconductor Lift-off Resists Market directly benefits from this capacity expansion, as each new fabrication facility requires substantial quantities of specialized resist materials throughout construction, qualification, and production ramp phases. China's announcement of plans to install over 30 GW of energy storage capacity by 2025 correlates with expanded advanced semiconductor manufacturing requirements for power management and analog circuits, creating additional lift-off resist demand.

The U.S. is positioned to capture more than one-quarter of global semiconductor capital expenditures over the next several years, second only to Taiwan, reflecting confidence in domestic production resilience and long-term manufacturing sustainability that necessitates reliable supply chains for critical materials like lift-off resists.

Restraint - High Manufacturing Complexity and Specialized Process Requirements

The Semiconductor Lift-off Resists Market faces significant structural challenges related to the extraordinary technical precision and manufacturing control required for advanced resist formulation and qualification. Development and qualification of new resist materials for cutting-edge lithography processes typically requires 18-36 months of rigorous testing, validation, and integration with customer fabrication equipment systems, creating substantial barriers to market entry and limiting competitive supplier proliferation.

Technical compatibility requirements across diverse lithography platforms EUV systems, 193 nm immersion lithography, nanoimprint lithography, and e-beam systems necessitate specialized formulation expertise and significant R&D investment that only established chemical suppliers can sustain. Supply chain constraints for critical raw materials and the environmental regulatory complexity surrounding resist manufacturing create additional cost pressures and operational challenges. These structural barriers limit market supplier numbers and constrain production scaling, particularly for emerging resist technologies required for advanced nodes.

Opportunities - Next-Generation Lithography Technology Enablement and Advanced Node Proliferation

The transition toward increasingly advanced semiconductor manufacturing nodes below 3 nanometers, driven by AI computing requirements and high-performance automotive systems, creates substantial opportunities for specialized lift-off resist suppliers capable of developing innovative materials supporting next-generation lithography platforms.

Globally, chipmakers are investing heavily in advanced node production capacity to satisfy explosive demand for AI accelerators, data center processors, and edge computing devices, necessitating continuous innovation in resist materials to enable smaller feature sizes, improved pattern fidelity, and enhanced manufacturing yields. The market benefits directly from these technology transitions, as companies like Fujifilm Corporation have demonstrated through their February 2025 SPIE Advanced Lithography presentation showcasing advanced EUV resist innovations that deliver improved high-resolution patterning with reduced line fluctuation. Suppliers demonstrating clear performance advantages in resolution, line-width roughness control, and process compatibility with cutting-edge lithography systems will capture premium pricing and expanded market share as advanced node production accelerates.

The global semiconductor industry's strong growth momentum, with record-breaking monthly sales of US$ 75.3 billion in November 2025, indicates sustained capital investment in manufacturing facilities and technology development, creating expanding opportunities for lift-off resist suppliers capable of supporting process node advancement.

Specialized Application Development for Memory and Power Device Manufacturing

Memory device manufacturing, identified as the fastest-growing application segment within the Semiconductor Lift-off Resists Market, represents a substantial expansion opportunity as chipmakers scale DRAM and NAND flash production to meet exploding demand from AI data centers, autonomous vehicles, and advanced computing infrastructure. Nanoimprint lithography and specialized resist formulations enabling cost-effective high-volume memory production create differentiated opportunities for suppliers developing application-specific resist solutions optimized for memory manufacturing economics and performance requirements.

The semiconductor lift-off resists market's fastest-growing application segment Memory Devices offers opportunities as artificial intelligence system deployments escalate globally, driving unprecedented demand for high-capacity memory components integrated into AI accelerators and data center infrastructure. Fujifilm's April 2024 introduction of a Nanoimprint Resist specifically designed for nanoimprint lithography demonstrates clear market validation that advanced resist technologies enable significant material usage reduction, throughput improvement, and cost efficiency advantages particularly valuable in high-volume memory manufacturing.

KemLab Inc.'s August 2023 introduction of the APOL-LO 3200 Series resist a high-resolution negative tone photoresist featuring advanced lift-off profiles, improved resolution, and wider process latitude with film thickness customization options shows how specialized resist innovations directly address memory device fabrication requirements. Suppliers capable of developing application-optimized lift-off resists for memory production will capture substantial market share as memory production volumes accelerate through 2033.

Category-wise Analysis

Product Type Insights

Positive photoresist materials represent the dominant product category within the Semiconductor Lift-off Resists Market, commanding 62.3% of market share in 2026 and reflecting decades of process optimization, integration with existing lithography infrastructure, and proven performance in high-volume semiconductor manufacturing. Positive photoresists have achieved market maturity characterized by established chemical suppliers, well-developed manufacturing processes, extensive application history across logic, memory, and analog device production, and broad compatibility with diverse lithography platforms including 193-nanometer immersion lithography and earlier-generation extreme ultraviolet systems.

The established manufacturing infrastructure and proven compatibility with existing fabrication equipment create substantial switching costs for chipmakers, supporting continued positive photoresist market dominance despite emerging competitive technologies.

Negative photoresist materials represent the fastest-growing product category within the Semiconductor Lift-off Resists Market, as advanced nanoimprint lithography platforms and next-generation patterning technologies increasingly rely on negative-tone chemistry offering superior line-width roughness characteristics and enhanced resolution performance at nanoscale dimensions. Negative photoresist adoption is particularly pronounced in advanced node production and emerging lithography applications where superior pattern fidelity and reduced critical-dimension variation directly improve manufacturing yields and device performance.

Application Insights

Logic device manufacturing encompassing microprocessors, application processors, graphics processing units, and specialized computing components represents the largest application category within the Semiconductor Lift-off Resists Market, commanding 38.4% of market share in 2026 and reflecting sustained investment in advanced computing architecture and artificial intelligence infrastructure. Microprocessor and advanced logic component production at leading semiconductor manufacturers require sophisticated lift-off resist solutions enabling exceptional resolution, pattern fidelity, and manufacturing consistency essential to complex digital circuit implementation at sub-5-nanometer process nodes.

Major semiconductor manufacturers including TSMC, Samsung, and Intel continue massive capital investments in advanced logic production capacity to capture expanding AI computing demand, directly supporting sustained lift-off resist consumption for logic device manufacturing throughout the forecast period. Continued process node advancement driven by AI computing requirements will maintain logic devices as the dominant Semiconductor Lift-off Resists Market application through 2033.

Memory device manufacturing encompassing DRAM, NAND flash, and emerging memory technologies represents the fastest-growing application category within the Semiconductor Lift-off Resists Market, as artificial intelligence data center deployments, autonomous vehicle computing systems, and advanced edge computing infrastructure drive unprecedented demand for high-capacity memory components. Memory device production increasingly utilizes advanced nanoimprint lithography and specialized lift-off resist formulations enabling cost-effective high-volume manufacturing essential to satisfying explosive global memory demand.

Regional Insights and Trends

East Asia Semiconductor Lift-off Resists Market Trend

East Asia represents the dominant regional market for the Semiconductor Lift-off Resists Market, commanding 79.2% of global market share and reflecting the region's unparalleled position as the center of advanced semiconductor manufacturing and fabrication technology leadership. Taiwan's TSMC, South Korea's Samsung and SK Hynix, and China's rapidly expanding domestic fabrication capacity collectively represent the overwhelming majority of global advanced node production, creating concentrated demand for sophisticated lift-off resist materials essential to next-generation device manufacturing.

Taiwan maintains its position as the global leader in advanced logic fabrication, with TSMC commanding approximately 54 Percent of global foundry capacity and continuous investment in cutting-edge manufacturing technology including EUV lithography and next-generation patterning processes requiring advanced lift-off resist solutions. TSMC's strategic positioning serving global AI computing demand, coupled with planned capacity expansions through 2026 and beyond, creates sustained multi-year demand for specialized resist materials. South Korea's memory device manufacturing dominance, led by Samsung and SK Hynix commanding approximately 43 PERCENT of global DRAM production and significant NAND flash capacity, creates substantial lift-off resist demand particularly as next-generation memory technologies incorporating advanced lithography platforms achieve production deployment.

China's semiconductor manufacturing expansion, supported by substantial government investment and policy incentives, is driving rapid capacity growth in advanced packaging, mature node logic, and analog device production. February 2023 developments including RENA Technologies' metal lift-off and resist strip wet processing equipment supply to Silicon Austria Labs, demonstrate the global demand for sophisticated lift-off processing infrastructure supporting advanced microfabrication. East Asian manufacturing dominance is expected to persist through 2033, maintaining the region's overwhelming Semiconductor Lift-off Resists Market share as the undisputed global center of advanced semiconductor production.

North America Semiconductor Lift-off Resists Market Trend

North America represents an emerging but rapidly expanding regional market for the Semiconductor Lift-off Resists Market, commanding approximately 9% of global market share and positioned for substantial growth as domestic fabrication capacity expansion accelerates under CHIPS Act incentives and private-sector investment commitments. The United States semiconductor industry is experiencing unprecedented momentum, with over 100 new fabrication, research, and packaging projects announced across 28 states, representing over half-a-trillion dollars in private-sector capital commitments and projected facility buildouts extending through 2032 and beyond.

U.S. fabrication capacity is projected to expand by more than 200 percent by 2032, effectively tripling domestic output and increasing the nation's share of global fab capacity from approximately 10 percent to 14 percent, creating substantial multi-year demand for lift-off resist materials as new facilities progress through construction, qualification, and production ramp phases. Intel's Arizona and Ohio fabrication facility investments, TSMC's Arizona manufacturing presence expansion, and Samsung's Texas facility development collectively represent extraordinary capital deployment in U.S. semiconductor manufacturing, directly driving lift-off resist consumption as facilities achieve operational status through 2026–2028. The U.S. is positioned to capture more than one-quarter of global semiconductor capital expenditures over the next several years, second only to Taiwan, indicating sustained investment in manufacturing infrastructure requiring sophisticated chemical materials and processing systems including lift-off resists.

Europe Semiconductor Lift-off Resists Market Trends

Europe represents a minor but strategically important regional market for the Semiconductor Lift-off Resists Market, commanding approximately 6% of global market share and characterized by specialized manufacturing capacity focused on analog devices, automotive semiconductors, and advanced packaging technologies. European semiconductor manufacturing, concentrated in Germany, Belgium, and the Netherlands, emphasizes specialized segments less dependent on extremely advanced node logic production compared to Asia Pacific regions.

The February 2023 RENA Technologies tender award from Silicon Austria Labs to supply metal lift-off and resist strip wet processing equipment demonstrates Europe's continued investment in advanced semiconductor fabrication infrastructure and support systems. Austria's position as a growing center for semiconductor research and advanced manufacturing technology development creates ongoing lift-off resist demand for facility operations and process development. Germany's automotive semiconductor manufacturing, increasingly focused on power management, analog, and mixed-signal components supporting vehicle electrification and autonomous driving systems, creates specialized demand for lift-off resist solutions optimized for automotive device production requirements.

Europe's focus on specialized manufacturing segments, combined with strong automotive industry integration and emphasis on sustainability, positions the region for selective growth in lift-off resist demand, particularly for application-specific resist formulations supporting advanced power device and analog circuit manufacturing. The Semiconductor Lift-off Resists Market in Europe is expected to grow modestly through the forecast period as regional manufacturing capacity remains relatively stable, but utilization intensity increases.

Competitive Landscape

The global Semiconductor Lift-off Resists market exhibits a largely oligopolistic to moderately consolidated structure, where a handful of established material science companies command the majority share due to their deep technical expertise, strong IP portfolios, and long-term supply agreements with semiconductor fabs. Entry barriers are high, as product qualification cycles are lengthy and customers demand extremely consistent performance, which favors experienced players over new entrants.

Merck Group, Tokyo Ohka Kogyo, Fujifilm Electronic Materials, Shin-Etsu Chemical, and JSR Corporation form the competitive core, leveraging advanced R&D capabilities and global distribution networks to maintain leadership. These companies compete primarily on formulation performance, resolution precision, and process compatibility rather than price, making innovation the key differentiator. Smaller specialists like KemLab Inc. operate in niche or customized segments, adding selective competition but not significantly disrupting the dominance of major firms.

Key Industry Developments

- In February 2025, Fujifilm Corporation, presented advanced EUV resist and developer innovations including negative-tone and nanoimprint resist technologies at SPIE Advanced Lithography plus Patterning 2025, demonstrating improved high-resolution patterning and reduced line fluctuation, strengthening next-generation semiconductor resist materials that support advanced lithography and lift-off patterning processes.

- In August 2023, KemLab Inc. introduced the patent-pending APOL-LO 3200 Series resist, a high-resolution negative tone photoresist specifically designed for i-Line and broadband semiconductor applications. Featuring an advanced lift-off profile, the resist offers improved resolution, wider process latitude, and a versatile film thickness range of 2 to10 plus μm, enabling enhanced customization and precision in semiconductor manufacturing and MEMS fabrication.

Companies Covered in Semiconductor Lift-off Resists Market

- Tokyo Ohka Kogyo

- RENA Technologies

- Merck Group

- Kayaku Advanced Materials

- Fujifilm Electronic Materials

- KemLab Inc.

- Shin-Etsu Chemical

- JSR Corporation

- Zeon Corporation

Frequently Asked Questions

The global Semiconductor Lift-off Resists Market is projected to be valued at US$ 848.9 Mn in 2026.

The Positive Photoresist segment is expected to account for approximately 62.3% of the Global Semiconductor Lift-off Resists Market by product type in 2026.

The market is expected to witness a CAGR of 7.6% from 2026 to 2033.

The Semiconductor Lift-off Resists Market Growth is driven by rapid EUV and nanoimprint lithography adoption, sub-7nm fabrication needs, and large-scale global fab expansions supported by CHIPS Act investments, collectively accelerating demand for high-precision semiconductor lift-off resists.

Key opportunities lie in enabling sub-3nm next-generation lithography and EUV processes, alongside developing specialized lift-off resist formulations for high-volume memory and power device manufacturing driven by AI, data center, and automotive semiconductor demand.

Key players in the Semiconductor Lift-off Resists Market include Merck Group, Tokyo Ohka Kogyo, Fujifilm Electronic Materials, Shin-Etsu Chemical, and JSR Corporation.