- Semiconductor Materials & Components

- Semiconductor Test Equipment Market

Semiconductor Test Equipment Market Size, Share and Growth Forecast, 2026 - 2033

Semiconductor Test Equipment Market by Product Type (Automated Test Equipment (ATE), Burn-in Systems, Handlers, Probes, Others), Technology (Analog Testing, Digital Testing, Mixed-Signal Testing, Radio Frequency (RF) Testing, Power Semiconductor Testing), End-Use Industry (Semiconductor Manufacturing, Consumer Electronics, Automotive, Military & Defense, IT & Telecom, Others), and Regional Forecast for 2026 - 2033

Semiconductor Test Equipment Market Share and Trends Analysis

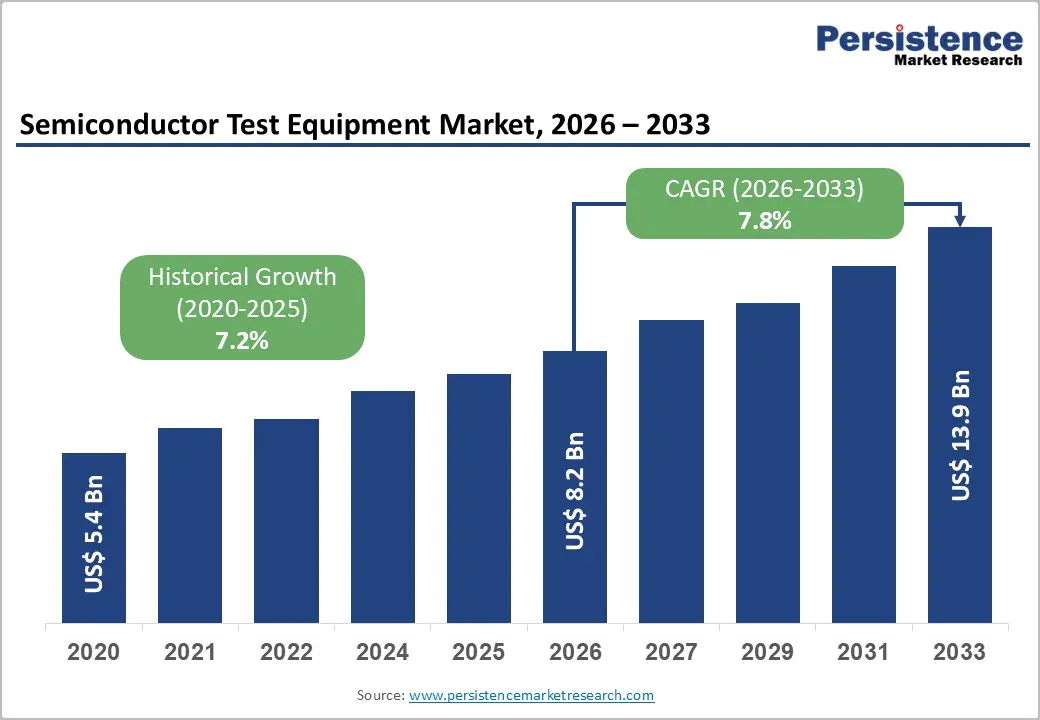

The global semiconductor test equipment market size is likely to be valued at US$ 8.2 billion in 2026, and is projected to reach US$ 13.9 billion by 2033, growing at a CAGR of 7.8 % during the forecast period of 2026-2033. The expansion of semiconductor manufacturing facilities drives this upward trajectory, the rising complexity of integrated circuits, and the growing demand in automotive, artificial intelligence (AI), communications, and consumer electronics sectors.

Technological innovations in automated and high-precision testing systems have enabled faster, more accurate validation of chips, meeting the evolving requirements of next-generation devices. Supportive government policies and incentives for localizing semiconductor supply chains are further accelerating investment in test equipment, particularly in the Asia Pacific and North America. Capital expenditure on advanced testing infrastructure is increasing as manufacturers prioritize quality assurance and reliability in high-volume production environments. Strategic regional expansions and partnerships will sustain market momentum, positioning organizations to address future challenges in semiconductor innovation and global competitiveness.

Key Industry Highlights

- Dominant Product Types: ATE is projected to lead with the largest market share in 2026, while probes are expected to grow fastest, with a 2026-2033 CAGR of 9.1%, driven by demand for wafer-level testing.

- Leading Technologies: Digital testing is expected to dominate in 2026, while mixed-signal and RF testing are likely to grow the fastest, with a CAGR of 10.2% during 2026–2033, driven by 5G, automotive radar, and IoT device growth.

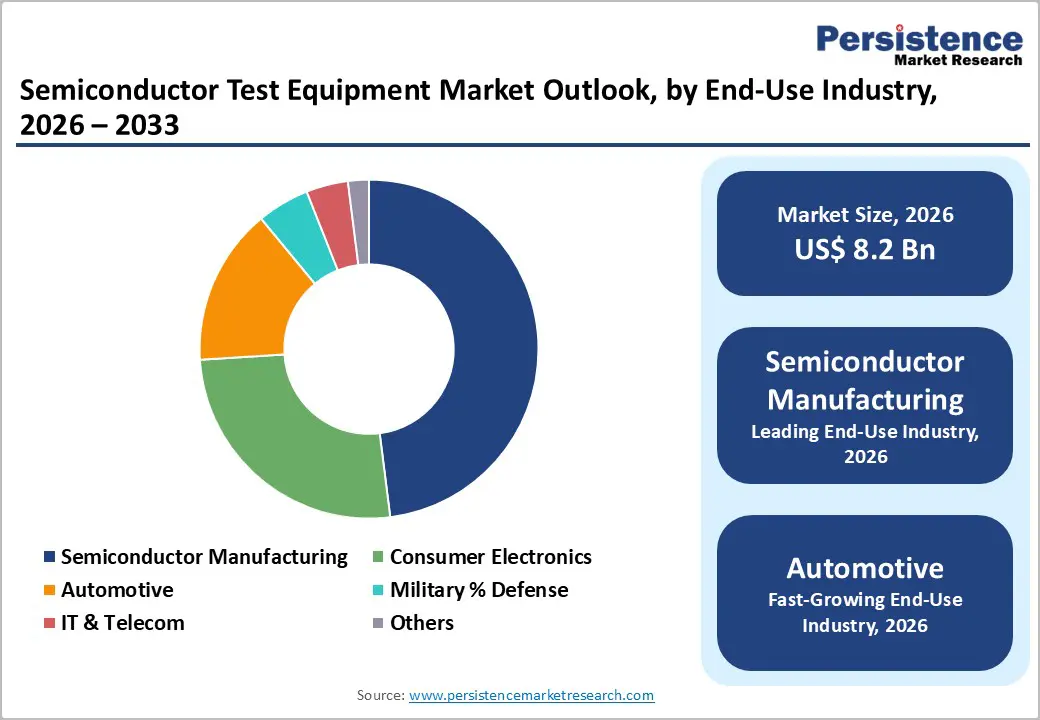

- End-Use Industry Dominance: Semiconductor manufacturing is expected to dominate at about 48% in 2026, with automotive forecast to register the fastest growth at 11% CAGR through 2033 due to strong demand for chips enabling advanced driver assistance systems (ADAS).

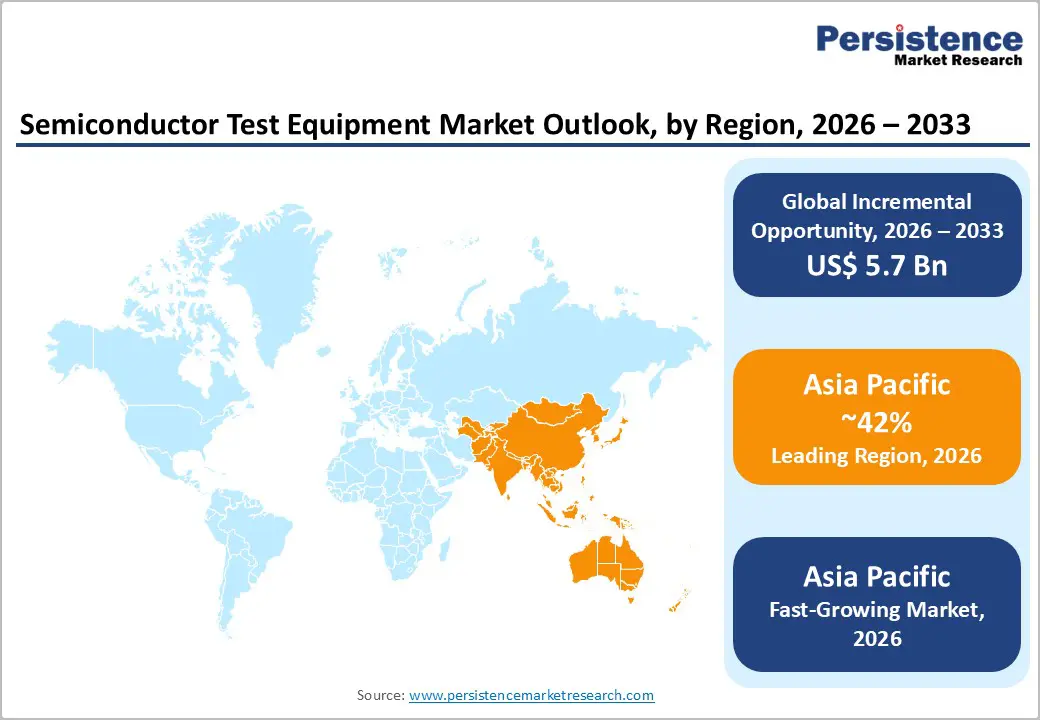

- Regional Leadership: Asia Pacific is poised to dominate with roughly 42% in 2026, led by China, Japan, and India’s semiconductor manufacturing expansion.

- Competitive Developments: Key strategic initiatives include the launch of multi-domain test platforms, the acquisition of advanced AI software, and partnerships aimed at fostering innovation and enhancing product portfolios.

- September 2025: India’s Cyient Semiconductors and U.S.-based Anora formed a production partnership in Bangalore for integrated design, testing, and validation of custom chips.

| Key Insights | Details |

|---|---|

|

Semiconductor Test Equipment Market Size (2026E) |

US$ 8.2 Bn |

|

Market Value Forecast (2033F) |

US$ 13.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Complexity and Strategic Investments Driving Demand

The growing intricacy of semiconductor devices is a key driver for the test equipment market. Modern chips integrate analog, digital, RF, and mixed-signal functionalities within a single package, while advanced architectures such as system-on-chip (SoC), 3D stacking, and heterogeneous integration demand highly sophisticated verification. To manage these complexities, manufacturers are deploying high-throughput automated and adaptive test systems that ensure functionality across multiple domains and operating conditions. This shift is particularly evident in wafer-level and final-test environments, where precision testing reduces defects and enhances overall production yield. The leading semiconductor manufacturers, such as Intel, announced upgrades to their Arizona fabs, incorporating multi-domain automated testers to accommodate next-generation SoC and AI accelerator production.

The strategic investments and government policies are reinforcing market growth. Governments in North America and the Asia Pacific are actively supporting semiconductor sovereignty and local manufacturing, offering incentives for capital expenditure on testing tools and infrastructure. For instance, in mid-2025, the U.S. Department of Commerce approved funding to expand domestic semiconductor testing and manufacturing capabilities. At the same time, China launched initiatives to promote the adoption of locally produced test equipment in its semiconductor fabs. The combination of industry-led investments in AI, automotive, and 5G chip testing is creating a sustained increase in demand for advanced 5G test equipment, fostering innovation and ensuring alignment with regional regulatory standards.

High Capital Requirements and Talent Shortages Limiting Test Equipment Adoption

The high cost of advanced semiconductor test systems continues to constrain market adoption, particularly for smaller design houses and emerging foundries. State-of-the-art automated testers, probe systems, and multi-domain platforms often require capital investments ranging from US$ 3–10 million per unit, with additional expenditures for maintenance, calibration, and software updates adding 10–15% annually to operating costs. These significant financial commitments can delay procurement and impact operational efficiency, especially for mid-tier players navigating cyclical semiconductor demand. Several mid-sized fab operators in Southeast Asia postponed expansion plans due to the inability to justify these capital-intensive upgrades.

Compounding the challenge is a shortage of a skilled technical workforce capable of operating and maintaining sophisticated test systems. Expertise in high-frequency signal analysis, AI integration, and system diagnostics is limited, which can extend qualification and deployment cycles and slow production ramps. Leading manufacturers, including Samsung and TSMC, have initiated specialized training programs and regional talent development initiatives in recent years to address these gaps, but the widespread adoption of advanced test equipment remains constrained by workforce limitations, which in turn impacts overall market growth and operational scalability.

AI-Enabled and Integrated Test Platforms in Emerging and Advanced Markets

The integration of AI and machine learning into semiconductor test equipment is creating significant growth opportunities. Intelligent test systems enable predictive maintenance, automated calibration, and early fault detection, improving yield and reducing operational inefficiencies. Leading fabs are increasingly adopting self-learning platforms that dynamically adjust parameters during production, allowing faster defect identification and streamlined wafer-level testing. Intel announced plans to implement AI-driven test platforms across its Arizona and Oregon fabs to enhance multi-domain chip verification, demonstrating how major manufacturers are leveraging technology to optimize test workflows and reduce cycle times.

The expansion into emerging semiconductor hubs and the convergence of test and quality assurance systems offer substantial opportunities. Regions such as India, Southeast Asia, and Eastern Europe are investing in local fabs and OSAT facilities, creating demand for modular, cost-efficient, and integrated test solutions. Companies are responding by developing platforms that combine wafer-level testing, optical inspection, and defect analytics in a single system. Samsung and TSMC jointly launched initiatives to expand integrated process control solutions into emerging fabs, reflecting industry focus on scalable, intelligent testing that meets both performance and reliability standards while supporting regional semiconductor ecosystem growth.

Category-wise Insights

Product Type Insights

Automated test equipment is expected to be the dominant product type, holding an estimated 45% of the market revenue share in 2026, and is crucial for validating complex ICs and SoCs across the analog, digital, and mixed-signal domains. Deployed in wafer-level and final-test stages, ATE enables multi-site, high-throughput testing and advanced diagnostics, improving yield and minimizing defects. In 2025, Advantest launched a multi-domain ATE platform for AI accelerators, while Cohu introduced enhanced solutions for automotive ICs in European fabs. R&D, regional fab expansions, and integration of adaptive software, predictive analytics, and high-speed data capture fuel growth. Governments in Asia Pacific are incentivizing domestic fab development, boosting demand, while Rohde & Schwarz partnered with emerging Asian fabs to deploy modular, scalable systems.

Probes are poised to be the fastest-growing product type, projected to grow at a CAGR of 9.1% through 2033, driven by wafer-level testing needs for advanced-node and 3D-stacked chips. These systems enable early defect detection before packaging, reducing costs and improving yield, while high-frequency MEMS-based probe cards support complex multi-site probing. Advantest introduced next-generation wafer probe platforms for 5G and AI chips, and Teradyne launched enhanced adaptive probe solutions for automotive IC testing in North America. Emerging fab investments in India, Eastern Europe, and Southeast Asia are creating new markets, with localized production and service centers enhancing adoption. For example, Keysight Technologies deployed probe systems in Indian and European fabs, reflecting growing demand for precision, modularity, and scalable wafer-level testing solutions.

Technology Insights

Digital testing is anticipated to be the largest technology segment, capturing around 42% of the semiconductor test equipment market revenue share in 2026, owing to its critical role in validating logic chips, microcontrollers, and memory interfaces across fabs and OSAT facilities. Rising AI, HPC, and edge device adoption increases digital core complexity, reinforcing demand. In 2025, for instance, Advantest deployed high-throughput digital test systems in Japanese and U.S. fabs for AI and memory chips, while Teradyne introduced upgraded digital testers for complex logic IC verification in European facilities. Innovations in multi-site testing, predictive diagnostics, and automated calibration improve throughput and reduce cycle times. AI-enabled digital testers further enable early fault detection, while government incentives for fab upgrades in Asia and North America support investment. Samsung implemented AI-assisted digital testing in its Korean fabs, highlighting the synergy among technology, regional investment, and innovation that is driving digital testing leadership.

Mixed-signal and RF testing are projected to be the fastest-growing technology through 2033, driven by the rapid expansion of 5G, IoT, and automotive radar integrated circuits (ICs). These platforms require high-speed signal measurement, multi-protocol validation, and precise calibration. Innovations in automated calibration and AI-assisted diagnostics improve testing efficiency and reduce cycle times. Regional fab expansions in China, Korea, and Europe are boosting demand for RF and mixed-signal platforms. Modular and scalable solutions allow smaller OSATs to adopt advanced testing capabilities. These trends reflect the integration of technology, regional investment, and innovation, driving market growth.

End-Use Industry Insights

Semiconductor manufacturing is likely to be the leading end-use area, with a 48% share in 2026, due to its foundational need for test infrastructure across fabrication, assembly, and final validation. Multi-domain test solutions ensure high throughput, yield, and reliability. Micron Technology upgraded wafer-level and multi-domain test systems at U.S. and Singapore memory fabs, while SK Hynix expanded testing infrastructure in Korean fabs for advanced-node devices. Investments focus on AI, automotive, and 5G chip validation. Governments in the Asia Pacific and North America are providing incentives for domestic fab upgrades, indirectly supporting test equipment adoption. Integrated test platforms combining functional, reliability, and wafer-level testing enhance efficiency. Continuous fab modernization and regional expansion reinforce semiconductor manufacturing as the primary driver of test equipment demand.

The automotive sector is anticipated to register the highest 2026-2033 CAGR of about 11%, driven by the soaring production of electric vehicles (EVs) and the growing adoption of ADAS and autonomous driving technologies. Automotive ICs integrate analog, digital, and power functions, requiring specialized testing for safety and performance. Infineon Technologies expanded automotive test capabilities in European EV fabs, while NXP Semiconductors upgraded mixed-signal testing platforms in North America for ADAS sensors. Modular and scalable automotive test solutions enable both OEMs and emerging startups to meet rigorous standards. Government incentives for EV and autonomous vehicle production further stimulate demand. Advanced stress, functional, and reliability testing ensures compliance with safety and regulatory norms. These developments highlight the strategic growth potential of automotive semiconductor testing.

Regional Insights

North America Semiconductor Test Equipment Market Trends

North America is projected to hold a significant share of the semiconductor test equipment market in 2026, driven by advanced R&D, high-tech fabs, and government incentives. The CHIPS Act supports upgrades to multi-domain automated test systems and predictive analytics platforms. AI accelerators, EV processors, and HPC ICs are key growth drivers. Regulatory frameworks promote domestic innovation through tax credits and controlled exports. Local OEMs and test solution providers deploy AI-assisted diagnostics and high-throughput platforms. Expansion in automotive, data center, and edge ICs continues to fuel demand. North America remains a hub for innovation and advanced test deployments.

ON Semiconductor deployed mixed-signal testers in Arizona fabs, while SkyWater Technology implemented predictive test systems for specialty foundry ICs. Universities and national labs partnered with fabs to accelerate AI-assisted calibration and fault detection. Modular platforms allow startups access to advanced capabilities. Investments focused on multi-node testing and automotive IC verification. Expansion in EV and HPC chips sustained procurement. Regional collaborations enhanced technology integration. Policy support and specialized investments reinforced North America’s market leadership.

Europe Semiconductor Test Equipment Market Trends

Europe has a moderate presence in the semiconductor test equipment market, primarily owing to Germany, the U.K., France, and Spain. Germany’s automotive and industrial electronics hubs generate strong demand for testing. EU regulatory harmonization simplifies cross-border compliance and investments. Fabs prioritize high-reliability testing for automotive and industrial ICs. Incentives promote local manufacturing and partnerships between domestic OEMs and test solution providers. Modular, energy-efficient, and scalable test systems are emphasized. Europe maintains stable growth through innovation and regulatory compliance.

AMS Semiconductor upgraded analog testers in Austria for automotive sensors, while Nexperia deployed automated wafer-level platforms in the Netherlands for power ICs. Fabs focus on sustainable manufacturing and strict quality norms. Collaborations with automotive OEMs strengthen domain-specific testing. Investment trends target EV and industrial electronics. Regulatory support encourages local production and reduces dependence on imports. Energy-efficient and modular solutions enable incremental growth in output. Europe is positioned for stable long-term adoption of advanced test equipment.

Asia Pacific Semiconductor Test Equipment Market Trends

Asia Pacific is expected to dominate the semiconductor test equipment market, with 42% of market share in 2026, led by dense fab networks in China, Japan, South Korea, Taiwan, and India. High-volume consumer electronics and original equipment manufacturer (OEM) ecosystems drive strong demand for test systems. Government-backed semiconductor funds and R&D incentives accelerate domestic tool development. Localized supply chains and lower production costs create a competitive edge. OSAT expansions and the adoption of modular test platforms boost regional growth. High fab density supports automated, high-throughput test deployment. Asia Pacific leads global semiconductor testing innovation.

Asia Pacific is also the fastest-growing region, with a CAGR of 8.7% through 2033, fueled by domestic policies and emerging equipment mandates. SMIC deployed multi-domain testers in Shanghai for AI and 5G chips, while GlobalFoundries implemented mixed-signal platforms in Singapore for automotive ICs. Investments in localized manufacturing, joint ventures, and talent development reduce lead times. Export controls encourage regional design and production, improving supply resilience. Fab expansions, modular testing, and government incentives support sustained adoption. Asia Pacific’s growth is reinforced by technological innovation and policy alignment.

Competitive Landscape

The global semiconductor test equipment market structure has maintained moderate consolidation, where leading companies such as Advantest Corporation, Teradyne Inc., Cohu Inc., Tokyo Electron Limited, and Keysight Technologies Inc. have secured a significant revenue portion through enduring partnerships with fabrication plants worldwide. These firms have utilized specialized knowledge and unified hardware-software ecosystems to sustain innovation leadership. Substantial research & development (R&D) commitments have enabled advancements in AI-enabled diagnostics, rapid automation, and validation for mixed-signal and RF components.

Regional specialists, including Rohde & Schwarz GmbH & Co. KG, National Instruments Corporation, and STMicroelectronics N.V., have concentrated on targeted categories and local markets. Compliance demands, integration challenges, and elevated capital needs have effectively deterred newcomers. Planners anticipate progressive mergers as frontrunners pursue buyouts, alliances, and region-specific support to broaden influence.

Key Industry Developments

- In December 2025, Tata Electronics partnered with Japan's ROHM Semiconductor to assemble and test automotive-grade N-channel (Nch) 100V, 300A silicon metal-oxide-semiconductor field-effect transistor (Si MOSFET) in a TOLL package at its facilities in India. The collaboration targets mass production shipments by 2026, with plans to co-develop advanced packaging technologies and market products globally.

- In October 2025, MPI Equipment Europe expanded its presence in Germany with a dedicated probe card repair and service center in Dresden, featuring cleanroom facilities for advanced ultra-fine pitch cantilever, vertical, and micro-electro-mechanical systems (MEMS) probe cards. This facility supports European semiconductor testing needs through installation, training, and maintenance for high-performance wafer probing.

- In October 2025, Teradyne launched the ETS-800 D20, a dual-sector automated test system for power semiconductors on the ETS-800 platform. This flexible solution supports high-volume production with up to eight parallel sites or high-mix/low-volume testing with two instruments, targeting AI, cloud infrastructure, electric vehicles, and data centers.

Companies Covered in Semiconductor Test Equipment Market

- Advantest Corporation

- Teradyne Inc.

- Cohu Inc.

- National Instruments (NI)

- Tokyo Electron Limited

- SPEA S.p.A.

- Astronics Corporation

- Chroma Systems Solutions

- Tokyo Seimitsu Co. Ltd.

- LTX Credence

- Keysight Technologies

- AMEC

- Naura Technology Group

- Bristol Instruments

Frequently Asked Questions

The global semiconductor test equipment market is projected to reach US$ 8.2 billion in 2026.

The rising complexity of semiconductor devices, proliferation of AI, 5G, and automotive electronics, and government incentives for domestic fab and test infrastructure are key growth drivers.

The market is poised to witness a CAGR of 7.8% from 2026 to 2033.

Integration of AI-driven and predictive testing, expansion in emerging semiconductor hubs, and convergence of test and quality assurance platforms are key growth opportunities.

Advantest, Teradyne, Cohu, Tokyo Electron, Keysight Technologies, Rohde & Schwarz, National Instruments, and STMicroelectronics are some of the leading companies in the market.