- Healthcare Services

- Pharmaceutical Contract Manufacturing Organization (CMO) Market

Pharmaceutical Contract Manufacturing Organization (CMO) Market Size, Share, and Growth Forecast, 2026 - 2033

Pharmaceutical Contract Manufacturing Organization (CMO) Market by Service Type (Drug Substance Manufacturing, Drug Product Manufacturing, Packaging & Fill-Finish Services, Integrated CDMO Services), Molecule Type (Small Molecules, Biologics, Cell & Gene Therapies, Peptides & Oligonucleotides, Vaccines), Development Stage (Preclinical, Clinical, Commercial), and Regional Analysis for 2026 - 2033

Pharmaceutical Contract Manufacturing Organization (CMO) Market Share and Trends Analysis

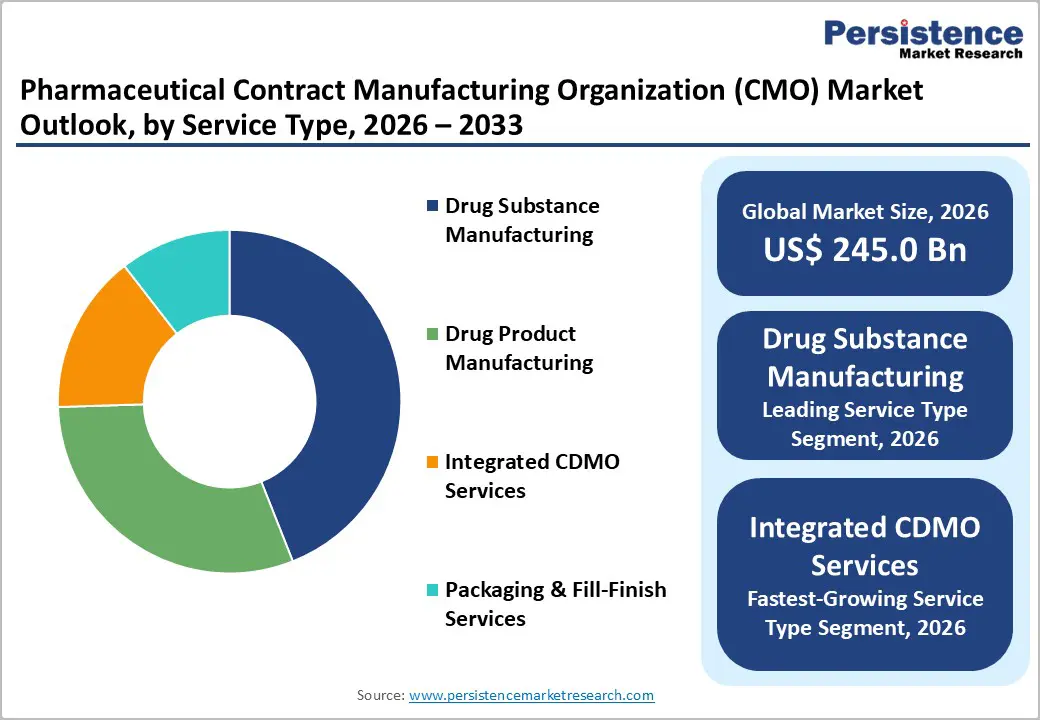

The global pharmaceutical contract manufacturing organization (CMO) market size is likely to be valued at US$ 245.0 billion in 2026, and is estimated to reach US$ 405.0 billion by 2033, growing at a CAGR of 7.4% during the forecast period 2026 - 2033.

The market is experiencing sustained expansion as pharmaceutical companies are increasingly adopting outsourced production models across biologics, specialty therapeutics, and advanced drug delivery systems. Integrated contract development and manufacturing organization (CDMO) partnerships are increasingly replacing internal manufacturing strategies as firms prioritize operational flexibility, capital efficiency, and faster commercialization timelines. The growth trajectory of the market is being charted by rising biologics approvals, increasing demand for glucagon-like peptide-1 (GLP-1) therapies, and evolving regulatory requirements that are making internal manufacturing expansion more complex.

Pharmaceutical manufacturers are actively outsourcing production to reduce capital expenditure burdens. Fledgling biotechnology firms are also contributing a majority of the clinical pipeline, with more than 70% of molecules under development originating from small and mid-size biopharma companies, according to industry data. Regulatory frameworks across major markets are strengthening quality standards, serialization requirements, and supply chain security expectations, which are increasing compliance costs and encouraging outsourcing partnerships with specialized manufacturers. Concurrently, technological advancements are transforming production economics and service offerings. Innovations such as continuous manufacturing systems, single-use bioprocessing technologies, and personalized medicine production platforms are expanding the addressable scope of CMO services beyond traditional batch manufacturing.

Key Industry Highlights

- Leading Service Type: Drug substance manufacturing is expected to account for roughly 44% of revenue share in 2026, driven by increasing outsourcing of biologics and complex-molecule production, which require specialized infrastructure.

- Top Development Stage: Commercial manufacturing is anticipated to dominate with an estimated 63% revenue share in 2026, reflecting higher production volumes and long-term supply agreements.

- Dominant Region: North America is projected to command approximately 38% market share in 2026, supported by strong pharmaceutical innovation activity and advanced regulatory frameworks.

- Fastest-Growing Service Type: Integrated CDMO services are expected to register a CAGR of around 9.1% from 2026 to 2033, owing to pharmaceutical companies consolidating vendors to accelerate development-to-commercialization timelines.

- Fastest-Growing Market: Asia Pacific is anticipated to expand at a CAGR of about 9.2% from 2026 to 2033, aided by improving regulatory compliance standards and government incentives promoting pharmaceutical manufacturing investments.

- September 2025: Samsung Biologics signed a CMO agreement worth approximately US$ 1.29 billion with a U.S.-based pharmaceutical company, reinforcing the strong global demand for large-scale biologics manufacturing capacity.

| Key Insights | Details |

|---|---|

| Pharmaceutical Contract Manufacturing Organization Market Size (2026E) | US$ 245.0 Bn |

| Market Value Forecast (2033F) | US$ 405.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Biologics Capacity Shortages and GLP-1 Manufacturing Expansion

Biologics manufacturing demand is outpacing available global production capacity, particularly for modalities such as monoclonal antibodies (mAbs), antibody-drug conjugates (ADCs), and peptide-based metabolic therapies, such as glucagon-GLP-1 agonists. Regulatory data from the United States Food and Drug Administration (FDA) indicate that biologics approvals have represented more than 40% of new molecular entity authorizations in recent years, reflecting a structural shift toward complex therapeutics. At the same time, the World Health Organization (WHO) is reporting a rising global prevalence of obesity and metabolic disorders, which is accelerating commercial demand for diabetes and weight management treatments. Pharmaceutical companies are therefore increasingly outsourcing biologics production to CMOs to secure manufacturing capacity while avoiding the financial risk associated with constructing large-scale biologics facilities.

The commercial implications are significant, given that biologics manufacturing agreements typically generate higher margins and longer contract durations compared with traditional small-molecule production contracts. High-value therapies require specialized infrastructure, encouraging pharmaceutical companies to establish long-term partnerships and capacity-reservation agreements with CDMOs. These arrangements are improving revenue predictability for service providers and are strengthening client retention rates. The concentration of demand around complex biologics is also accelerating industry consolidation, as larger CMOs are acquiring specialized firms to expand technological capabilities and geographic reach.

Emerging Biotech Dominance in Drug Pipelines

The global drug development pipeline is increasingly being driven by small and mid-size biotechnology companies that often lack internal manufacturing infrastructure and operational scale. Industry data show that emerging biopharma firms are contributing a majority share of innovative clinical assets worldwide, particularly in advanced modalities such as biologics and precision therapies. These organizations are relying extensively on CMOs throughout both clinical development and commercial production stages because outsourcing enables faster progression through regulatory milestones without the capital burden of facility construction. The growing dependence on external manufacturing partners is also reflecting the financial constraints faced by early-stage biotechnology firms, which are prioritizing research investment over infrastructure ownership.

This structural transformation is converting outsourcing from an optional operational decision into a core strategic requirement across the pharmaceutical ecosystem. CDMOs are evolving into integrated partners that are offering end-to-end services spanning process development, clinical manufacturing, regulatory support, and commercial supply. Such integrated relationships are increasing switching costs because technology transfer between manufacturers remains complex and time-consuming once development has progressed. As a result, client retention rates are strengthening, and long-term supply agreements are becoming more common.

Regulatory Compliance Cost Inflation and Quality Risk Exposure

Pharmaceutical manufacturing compliance requirements are becoming increasingly rigorous across major regulatory jurisdictions as authorities are strengthening oversight of product quality, data integrity, and supply chain traceability. Prime regulatory agencies such as the U.S. FDA and the European Medicines Agency (EMA) frequently update current Good Manufacturing Practice (cGMP) standards while intensifying inspection and enforcement actions. CMOs are therefore operating in an environment where compliance gaps can rapidly trigger warning letters, import restrictions, or production suspensions. These regulatory pressures are increasing operational complexity because manufacturers must maintain advanced quality management systems, validated digital records, and continuous monitoring processes to meet evolving expectations.

The financial ramifications of non-compliance are substantial, extending beyond direct remediation costs. Corrective actions following enforcement measures can require facility upgrades, process revalidation, and third-party consulting support, often resulting in expenses exceeding tens of millions of United States dollars. Production interruptions simultaneously reduce revenue and disrupt pharmaceutical clients' supply chains, potentially damaging long-term business relationships. Smaller CMOs face disproportionate exposure because they typically have limited financial reserves to absorb compliance-related shocks, making them more vulnerable to market exit or acquisition. Pharmaceutical sponsors are also becoming more selective in vendor qualification, prioritizing manufacturers with strong compliance track records and global regulatory approvals to minimize the risk of supply disruption.

Capital Intensity and Technology Obsolescence Risk

Biologics and advanced therapy manufacturing facilities require considerable upfront capital investment while facing accelerated technology evolution cycles, increasing the risk of infrastructure obsolescence. Production platforms such as single-use bioreactor systems, modular cleanroom environments, and continuous manufacturing technologies are improving operational flexibility and reducing long-term operating costs. CMOs, therefore, need to make frequent capital-allocation decisions to remain technologically competitive while complying with evolving regulatory expectations for advanced therapeutics, such as cell and gene therapies. Companies that delay modernization are facing declining competitiveness, particularly when pharmaceutical sponsors are prioritizing partners with flexible and digitally integrated manufacturing capabilities.

This environment is creating sustained financial pressure because CMOs must balance ongoing capital reinvestment with maintaining high facility utilization rates to preserve profitability. Manufacturing economics in this sector are heavily influenced by fixed costs, including equipment depreciation, facility maintenance, and regulatory compliance overhead. Underutilized production lines are rapidly eroding margins, particularly for large biologics facilities where operating leverage is significant. Capacity planning is therefore becoming a critical strategic function, as misalignment between investment timing and client demand can lead to prolonged periods of low utilization. These risks are encouraging CMOs to pursue long-term contracts, capacity reservation agreements, and diversified client portfolios to stabilize revenue streams.

Cell and Gene Therapy Commercialization Platforms

Cell and gene therapy manufacturing is moving toward early commercial deployment, driving demand for highly specialized CDMO infrastructure. The EMA and the U.S. FDA are refining approval pathways for advanced therapy medicinal products, which is supporting a gradual rise in market authorizations for gene therapies and cell-based treatments. These therapies require complex production processes involving viral vector engineering, plasmid deoxyribonucleic acid (DNA) preparation, and controlled cell expansion under stringent quality standards. Pharmaceutical developers are therefore seeking manufacturing partners with specialized facilities and regulatory expertise to accelerate commercialization timelines while managing operational risk. The shift toward personalized medicine and rare disease treatments is further reinforcing demand because many therapy developers lack internal manufacturing capabilities.

The commercial opportunity is significant, as advanced therapy manufacturing services are expected to generate tens of billions in revenue by the early 2030s as clinical pipelines mature into approved products. Global capacity remains constrained due to technical complexity, regulatory compliance requirements, and long facility construction timelines, which is creating favorable pricing conditions for early investors in the sector. CMOs that are investing in viral vector production platforms, plasmid manufacturing capacity, and automated cell processing technologies are positioning themselves to capture high-margin revenue streams. High barriers to entry are also limiting competitive intensity, enabling specialized providers to secure long-term contracts and strategic partnerships with biotechnology innovators.

Supply Chain Reshoring and Regional Manufacturing Incentives

Governments are actively implementing pharmaceutical manufacturing localization strategies to strengthen supply chain resilience following disruptions observed during the COVID-19 pandemic. Policy frameworks across the U.S., the European Union (EU), India, and Japan are encouraging domestic drug production through financial incentives, regulatory support, and public procurement initiatives aligned with guidance from the WHO and national health authorities. These programs are prioritizing essential medicines, biologics, and vaccine manufacturing capacity to reduce dependence on cross-border supply networks. Pharmaceutical companies are responding by diversifying production footprints and collaborating with CMOs that possess regional regulatory expertise and established infrastructure. Localization policies are also emphasizing quality compliance and supply chain transparency, which is heightening the need for qualified manufacturing partners capable of meeting international regulatory standards.

This policy-driven environment is creating substantial opportunities for CMOs to establish regional manufacturing hubs and participate in public-private partnership models that support long-term capacity utilization. Emerging markets are attracting investment due to favorable cost structures, skilled technical labor availability, and supportive industrial policies, particularly across the Asia Pacific. Countries investing in pharmaceutical clusters and biotechnology parks are positioning themselves as competitive outsourcing destinations, accelerating global capacity redistribution. Contract manufacturers that expand geographically while maintaining consistent quality systems are likely to secure strategic contracts from multinational pharmaceutical companies seeking supply diversification.

Category-Wise Analysis

Service Type Insights

Drug substance manufacturing is likely to account for approximately 44% of the pharmaceutical contract manufacturing organization market revenue share, supported by sustained outsourcing demand for biologics and high-potency active pharmaceutical ingredients (HPAPIs). Pharmaceutical companies are increasingly outsourcing the production of complex molecules to external partners because regulatory compliance requirements and the intensity of capital expenditure are making internal capacity expansion less attractive. Manufacturing facilities for biologics and specialized small molecules require advanced containment systems, validated processes, and highly skilled technical personnel, which are raising operational barriers. Companies are therefore prioritizing partnerships with CMOs to accelerate development timelines and secure scalable production capacity without delaying commercialization.

Integrated CDMO services are projected grow the fastest between 2026 and 2033, with an estimated CAGR of 9.1%. Pharmaceutical companies are increasingly consolidating vendor relationships to reduce coordination complexity, improve project management efficiency, and shorten time-to-market across development and commercialization stages. Integrated service providers are offering end-to-end solutions that include process development, clinical manufacturing, regulatory support, and commercial production, improving operational continuity and reducing technology transfer risks. As a result, integrated CDMOs are benefiting from long-term contracts, higher client retention rates, and improved revenue predictability. Organizations that invest in flexible manufacturing platforms and digital integration capabilities are likely to strengthen competitive positioning as the demand for consolidated outsourcing models is slated to increase rapidly.

Development Stage Insights

Commercial manufacturing is set to dominate the pharmaceutical CMO market revenue in 2026 at approximately 63%, reflecting the large production volumes and multi-year supply agreements associated with approved and marketed therapies. Pharmaceutical companies are outsourcing manufacturing of mature products to optimize internal resource allocation and to focus capital deployment on research, innovation, and portfolio expansion. Established products often require stable, cost-efficient production rather than advanced development capabilities, which makes external manufacturing partnerships economically attractive. Contract manufacturers are providing scale efficiency, regulatory expertise, and supply chain continuity, enabling sponsors to maintain product availability while reducing operational complexity. Outsourcing is also supporting lifecycle management strategies, including formulation improvements and geographic expansion, which are sustaining long-term commercial production demand across multiple therapeutic categories.

Clinical manufacturing is expected to register the fastest growth between 2026 and 2033, driven by expanding clinical pipelines and increasing participation from emerging biotechnology firms. Early engagement with CDMOs is becoming commonplace as companies are seeking rapid scale-up capabilities, flexible production volumes, and regulatory guidance throughout development phases. Clinical-stage production requires specialized expertise in process optimization, small-batch manufacturing, and compliance documentation, which several biotechnology companies prefer to access externally rather than build internally. This trend is strengthening the strategic role of CMOs during early drug development and is creating opportunities for long-term partnerships that extend into commercial manufacturing once products receive regulatory approval.

Regional Insights

North America Pharmaceutical Contract Manufacturing Organization (CMO) Market Trends

North America is poised to command an estimated 38% of the pharmaceutical contract manufacturing organization market share in 2026, primarily led by the U.S. due to its strong pharmaceutical innovation ecosystem, extensive biologics manufacturing infrastructure, and well-established regulatory framework. The region hosts a high concentration of biotechnology companies, research institutions, and multinational pharmaceutical corporations, which is generating sustained demand for outsourced manufacturing services. Federal policies that are encouraging domestic pharmaceutical production and supply chain resilience are reinforcing investment in local CDMO capacity, particularly for biologics, vaccines, and advanced therapies. Companies are also benefiting from access to skilled technical labor, advanced automation technologies, and proximity to major pharmaceutical clients, strengthening North America’s leadership position.

The growth of the regional market is also boosted by continued biologics commercialization, expansion of advanced therapy medicinal products, and increasing outsourcing activity among large pharmaceutical firms. Demand is being driven by the need for specialized manufacturing platforms such as cell and gene therapy production, sterile fill-finish capabilities, and high-potency containment systems. The regulatory environment remains rigorous but predictable, with the U.S. FDA providing clear guidance pathways that are supporting long-term investment planning. This regulatory certainty is encouraging capital deployment in new facilities and technology upgrades while maintaining strong investor confidence.

Europe Pharmaceutical Contract Manufacturing Organization (CMO) Market Trends

In Europe, the pharmaceutical CMO market growth is bolstered by a strong manufacturing ecosystem across Germany, Switzerland, Ireland, and the U.K. These nations are home to some of the most advanced pharmaceutical production clusters, powered by the availability of a highly skilled workforce, established research infrastructure, and regulatory systems that are closely aligned with international quality standards. The presence of multinational pharmaceutical headquarters and biotechnology innovation hubs is also generating consistent outsourcing demand across both clinical and commercial manufacturing stages. Regulatory oversight from the EMA provides a harmonized compliance framework across member states, which is enabling cross-border manufacturing operations and facilitating market access within the EU bloc.

The prospects of the market in Europe are brightening as a result of increasing biosimilar production, expansion of biologics pipelines, and government initiatives that are encouraging pharmaceutical manufacturing investment. Biosimilar development is particularly prominent in Europe due to supportive regulatory pathways and strong healthcare system adoption, which is creating sustained outsourcing demand for manufacturing services. European CDMOs are also leveraging deep expertise in complex biologics production, sterile fill-finish operations, and advanced formulation technologies to maintain competitive differentiation. Public funding programs and industrial policies that support biotechnology innovation are further reinforcing investment in manufacturing capacity upgrades.

Asia Pacific Pharmaceutical Contract Manufacturing Organization (CMO) Market Trends

The Asia Pacific pharmaceutical CMO market is anticipated to record the fastest 2026 - 2033 growth at an estimated CAGR of 9.2%, aided by favorable production economics and expanding technical capabilities. China, India, South Korea, and Singapore are attracting pharmaceutical outsourcing activity as they offer competitive operating costs, a growing pool of skilled scientific professionals, and supportive government policies that encourage biotechnology investment. National initiatives aimed at strengthening domestic pharmaceutical manufacturing capacity are improving infrastructure development, regulatory alignment, and research collaboration networks across the region. The presence of established API manufacturing bases in India and China, combined with increasing biologics expertise in South Korea and Singapore, is creating a diversified outsourcing ecosystem that appeals to multinational pharmaceutical companies seeking cost efficiency and supply chain diversification.

Regulatory agencies across the region are strengthening quality frameworks to align with international GMP requirements, which is improving global confidence in locally manufactured pharmaceutical products. Governments are also offering financial incentives, tax benefits, and infrastructure support to attract foreign investment in pharmaceutical production facilities. Rapid expansion of biologics capacity, including monoclonal antibody and vaccine manufacturing, is positioning Asia Pacific as a critical growth engine within the global outsourcing landscape. CDMOs that combine cost competitiveness with regulatory credibility are likely to capture substantial market share as pharmaceutical companies continue to diversify manufacturing footprints across geographies.

Competitive Landscape

The global pharmaceutical contract manufacturing organization market structure is likely to remain moderately fragmented, with Lonza, Catalent, Samsung Biologics, and WuXi dominating revenues. Integrated CDMOs are steadily gaining market share because they offer scale advantages, established regulatory compliance frameworks, and comprehensive service portfolios that span development through commercial production. Competitive differentiation is increasingly being shaped by access to biologics manufacturing capacity, expertise in advanced therapy modalities such as cell and gene therapies, and the ability to operate across multiple geographic regions while maintaining consistent quality standards. Cost competitiveness continues to influence procurement decisions; however, pharmaceutical companies are prioritizing reliability, speed, and technical capabilities when selecting manufacturing partners, particularly for complex therapeutics that require specialized infrastructure.

Strategic collaborations between pharmaceutical sponsors and CDMOs are becoming more prevalent as companies seek long-term manufacturing security and operational flexibility. Multi-year supply agreements, capacity reservation contracts, and co-investment partnerships are improving revenue predictability for service providers while reducing supply chain risk for pharmaceutical clients. Industry consolidation is expected to continue because organizations are pursuing acquisitions to expand technology capabilities, strengthen geographic reach, and access new therapeutic modalities. Larger firms with strong balance sheets are increasingly acquiring niche manufacturers with specialized expertise to enhance service offerings and capture higher-value contracts.

Key Industry Developments

- In January 2026, Symbiosis Pharmaceutical Services initiated commercial manufacturing at its new U.S.FDA-inspected and Medicines and Healthcare products Regulatory Agency (MHRA)-licensed facility in Stirling, U.K., producing its first 10,000-vial batch to support a Phase III cancer immunotherapy program. The expansion increases sterile fill-finish capacity and enables seamless support from late-stage clinical development to commercial supply for global clients.

- In December 2025, Buckland Group launched a new CMO, Quvara Medical, following the acquisition of Becton Dickinson’s Swindon facility, establishing a U.K. and EU-based manufacturing hub capable of supporting both clinical and commercial production for pharmaceutical and medical technology companies. The new entity offers GMP and International Organization for Standardization (ISO)-certified capabilities.

- In October 2025, Eli Lilly and Company announced plans to invest more than US$ 1.0 billion to expand manufacturing and supply capabilities in India, including establishing a manufacturing and quality hub in Hyderabad to oversee regional production and contract manufacturing partners. The investment is intended to strengthen global supply resilience and support therapies across areas such as obesity, diabetes, cancer, and autoimmune diseases.

Companies Covered in Pharmaceutical Contract Manufacturing Organization (CMO) Market

- Lonza Group AG

- Catalent, Inc.

- Samsung Biologics Co., Ltd.

- WuXi AppTec Co., Ltd.

- WuXi Biologics (Cayman) Inc.

- Thermo Fisher Scientific Inc.

- Recipharm AB

- Siegfried Holding AG

- Cambrex Corporation

- Boehringer Ingelheim International GmbH

- Fujifilm Diosynth Biotechnologies U.S.A., Inc.

- PCI Pharma Services

- Vetter Pharma-Fertigung GmbH & Co. KG

- Almac Group Limited

- Aenova Holding GmbH

Frequently Asked Questions

The global pharmaceutical contract manufacturing organization (CMO) market is projected to reach US$ 245.0 billion in 2026.

Increasing adoption of outsourced production models across biologics, specialty therapeutics, and advanced drug delivery systems by pharmaceutical companies, and growing number of integrated CDMO partnerships are driving the market.

The market is poised to witness a CAGR of 7.4% from 2026 to 2033.

Strengthening of quality standards, serialization requirements, and supply chain security expectations, which are spiking compliance costs, by regulatory bodies, and innovations such as continuous manufacturing systems and single-use bioprocessing technologies are creating new market opportunities.

Lonza Group, Catalent, Samsung Biologics, and WuXi AppTec are some of the key players in the market.