- Smart Packaging

- Pharmaceutical Secondary Packaging Market

Pharmaceutical Secondary Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Pharmaceutical Secondary Packaging Market by Packaging Type (Folding Cartons, Blister Packs, Others), Material Type (Paperboard, Plastic, Others), Application, and Regional Analysis for 2026 - 2033

Pharmaceutical Secondary Packaging Market Size and Trends Analysis

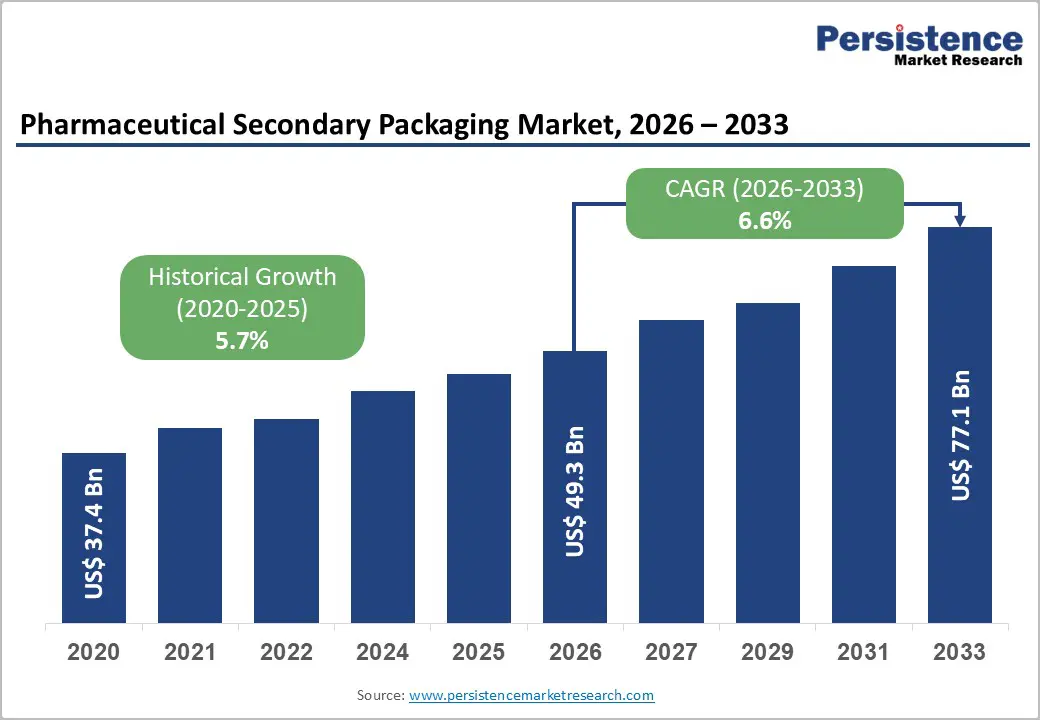

The global pharmaceutical secondary packaging market size is likely to be valued at US$49.3 billion in 2026 and is expected to reach US$77.1 billion by 2033, growing at a CAGR of 6.6% between 2026 and 2033, driven by increasing demand for sustainable packaging solutions and patient-centric formats, which are enhancing value per unit across key markets. Although challenges such as raw material price volatility and rising regulatory compliance costs persist, the market outlook remains positive, supported by ongoing pharmaceutical innovation and rising global healthcare expenditure.

Pharmaceutical secondary packaging encompasses cartons, blister cards, inserts, labels, corrugated shippers, and other protective outer packaging used to secure and provide information about primary drug containers. Over time, its function has expanded beyond basic containment to become a vital component of regulatory compliance and supply chain management, incorporating features such as serialization, tamper-evidence mechanisms, and cold-chain monitoring capabilities.

Key Industry Highlights:

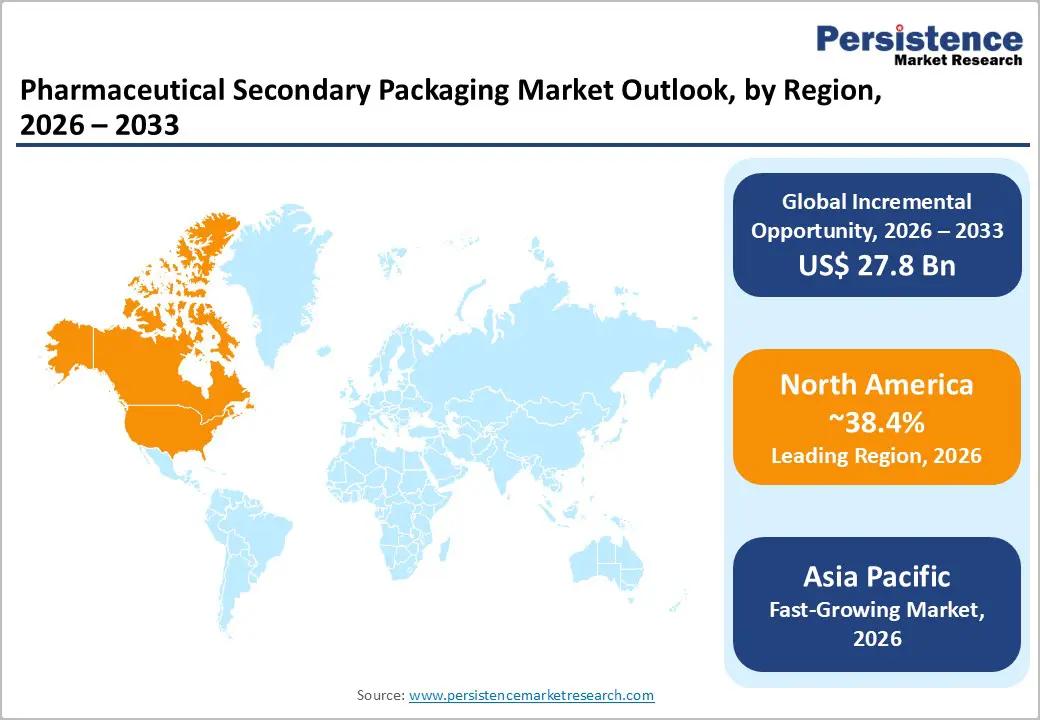

- Leading Region: North America is projected to hold 38.4% of the market share, supported by DSCSA-driven serialization compliance, strong biologics penetration, and advanced GMP-certified contract packaging infrastructure.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, driven by pharmaceutical manufacturing expansion in China and India and increasing alignment with global serialization standards, contributing a rapidly rising share of the global demand.

- Investment Plans: Capital investments are concentrated in automation, cold-chain secondary packaging, and digital serialization systems, particularly in the U.S. and Europe, where compliance mandates and biologics growth are accelerating high-value infrastructure spending.

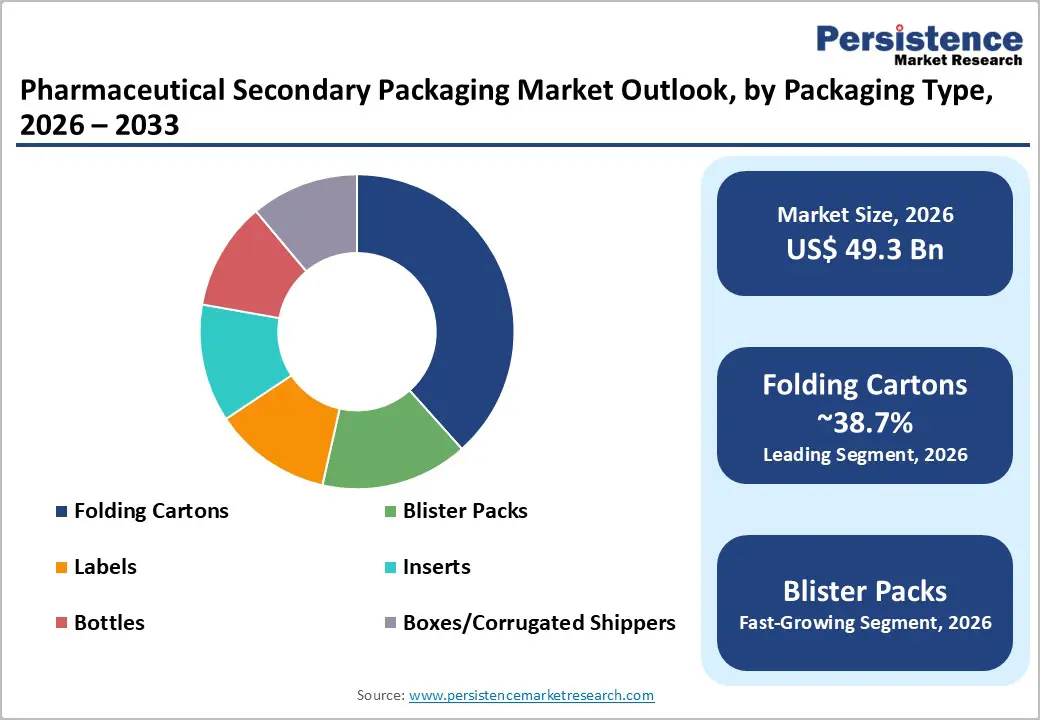

- Dominant Packaging Type: Folding cartons are anticipated to lead with an anticipated 38.7% market share, supported by cost-efficiency, scalability, regulatory labeling compatibility, and widespread use in prescription and OTC drug packaging.

- Leading Application: Prescription drugs dominate with an anticipated 45.6% market share, driven by stringent labeling regulations, serialization mandates, and sustained demand for chronic disease therapies.

| Key Insights | Details |

|---|---|

| Pharmaceutical Secondary Packaging Market Size (2026E) | US$49.3 Bn |

| Market Value Forecast (2033F) | US$77.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Traceability and Serialization Mandates

Global regulatory agencies have implemented stringent track-and-trace requirements to combat counterfeit drugs and enhance supply chain transparency. In the U.S., the Drug Supply Chain Security Act mandates product-level serialization and electronic traceability. The European Falsified Medicines Directive also requires unique identifiers and tamper-evident features on prescription medicine packaging. These regulations have significantly increased capital expenditure in secondary packaging lines. Manufacturers must incorporate 2D data matrix codes, aggregation systems, vision inspection equipment, and compliance software. Serialization-related investments contribute incremental recurring revenue through equipment upgrades, validation services, and data management solutions. Secondary packaging lines now serve as the primary platform for compliance integration, increasing the strategic importance of carton and labeling systems.

Expansion of Biologics and Specialty Pharmaceuticals

Biologics, biosimilars, vaccines, and advanced therapies are growing at a faster pace than traditional small-molecule drugs. These therapies often require temperature-sensitive handling, specialized labeling, and protective outer packaging for vials, prefilled syringes, and auto-injectors. Secondary packaging solutions must provide validated insulation, cushioning, and tamper evidence while maintaining regulatory labeling integrity. Higher average selling prices (ASPs) for biologics support increased packaging expenditure per unit. Cold-chain compatible cartons, insulated shippers, and kitted packaging solutions command premium pricing and accelerate growth in high-value therapeutic categories.

Sustainability and Material Innovation

Pharmaceutical companies are incorporating environmental performance metrics into procurement decisions. Regulatory pressure and corporate ESG targets are accelerating the adoption of recyclable paperboard, mono-material blister solutions, and reduced-laminate designs. Extended Producer Responsibility policies in Europe and sustainability regulations in North America and Asia Pacific are reshaping packaging material selection. Converters investing in recycled fiber capacity, lightweighting initiatives, and mono-polymer structures gain a competitive advantage. Sustainable secondary packaging formats increasingly influence tender awards and long-term supply contracts.

Barrier Analysis - Raw Material Price Volatility and Supply Constraints

Secondary packaging profitability remains sensitive to fluctuations in paperboard, polymer resins, aluminum foil, and corrugated materials. A sustained 15-25% increase in input costs can compress converter gross margins by approximately 3-6 percentage points if pricing adjustments lag. Supply chain disruptions may also delay pharmaceutical product launches, requiring requalification of alternative materials. Inventory buffers increase working capital requirements, particularly for high-volume carton producers.

Regulatory Complexity and Extended Qualification Timelines

Although compliance mandates stimulate demand, they also increase operational complexity. Packaging validation requires stability testing, transport validation, serialization verification, and regulatory documentation. For specialty drug launches, secondary packaging qualification may extend commercialization timelines by 6-12 weeks and increase launch budgets by 0.5-1.5%. Smaller manufacturers face disproportionate compliance burdens, limiting participation in highly regulated markets.

Opportunity Analysis - Growth in Contract Packaging and Outsourcing

Pharmaceutical companies increasingly outsource secondary packaging to specialized contract packagers to reduce capital expenditure and accelerate time-to-market. Outsourcing partners provide serialization capabilities, cold-chain validation, labeling services, and regulatory compliance expertise. Investment in modular, high-speed packaging lines and digital serialization platforms enhances scalability. Regional expansion in Asia Pacific and nearshoring strategies in North America present strong growth prospects. Service-based contracts linked to operational efficiency metrics can generate recurring revenue streams.

Premium, Patient-Centric and Sustainable Designs

Secondary packaging formats that enhance adherence, accessibility, and sustainability offer pricing differentiation. Calendar blisters, easy-open cartons for elderly patients, and recyclable mono-material solutions address unmet user needs. The development of certified low-carbon paperboard cartons and recyclable blister alternatives supports procurement requirements tied to ESG objectives. Companies integrating digital health features such as QR codes for patient education further increase packaging value beyond containment.

Category-wise Analysis

Packaging Type Insights

Folding cartons are anticipated to account for 38.7% of market share in 2026, maintaining their position as the leading segment. Their cost-efficiency, scalability, and compatibility with serialization and track-and-trace technologies make them the preferred format across prescription and OTC applications. Cartons provide adequate surface area for mandatory labeling, barcodes, QR codes, patient information leaflets, and branding elements required under regulatory frameworks such as serialization mandates in the U.S. and Europe. Large-scale global converting capacity ensures a stable supply and competitive pricing. For example, solid oral dose products such as tablets and capsules are typically packed in blister packs inserted into printed folding cartons with tamper-evident seals. Pharmaceutical manufacturers rely on folding cartons to standardize production across multiple SKUs and international markets while maintaining regulatory compliance and operational efficiency.

Blister packs represent the fastest-growing packaging type segment. Demand is driven by the shift toward unit-dose dispensing, enhanced tamper evidence, and improved patient compliance through calendarized packaging formats. Growth in self-medication markets and OTC consumption in emerging economies further supports expansion. Blisters are widely used for analgesics, antihistamines, oral contraceptives, and chronic therapy medications, where dose visibility and moisture protection are critical. Technological improvements in thermoforming processes and lightweight polymer films such as PVC, PVDC, and aluminum-based cold-form foils reduce material usage while maintaining barrier performance. Integration of blisters with printed cartons for combination packaging enhances safety, supports serialization, and improves shelf presence in retail pharmacy channels.

Application Insights

Prescription drugs are anticipated to account for 45.6% of the market share in 2026, making them the leading application segment. Regulatory labeling requirements, serialization codes, and tamper-evident mandates increase packaging complexity and value per unit. Chronic disease management therapies for diabetes, cardiovascular disorders, and oncology sustain consistent volume demand. Packaging for prescription oral solids often includes serialized cartons, barcoded labels, and patient information inserts to comply with global regulations such as track-and-trace directives. Specialty therapies with smaller batch sizes also require higher customization and validation standards. These compliance-driven requirements reinforce long-term demand stability and higher margins within the prescription drug packaging segment.

The biologics segment is likely to be the fastest-growing application segment within pharmaceutical secondary packaging. Products such as monoclonal antibodies, vaccines, insulin formulations, and advanced cell and gene therapies require insulated cartons, temperature-controlled secondary packs, validated shippers, and protective inserts. Higher average selling prices (ASPs) justify premium packaging expenditures and stricter validation protocols. For instance, vaccine distribution programs require secondary packaging compatible with cold chain logistics and data-logging devices. The expansion of injectable biologics and biosimilars in both developed and emerging markets is accelerating demand for high-performance packaging formats. Investment in temperature-controlled, serialized, and validated secondary packaging systems positions converters to capture disproportionate revenue growth in this high-value segment.

Regional Insights

North America Pharmaceutical Secondary Packaging Market Trends - DSCSA-Driven Serialization and Biologics Expansion

North America is expected to lead the market, accounting for approximately 38.4% of the market share in 2026. The U.S. represents the largest national contributor due to strong pharmaceutical R&D output, rapid biologics adoption, and a highly structured regulatory framework under the Drug Supply Chain Security Act (DSCSA). Full DSCSA interoperability requirements, enforced in 2023-2024, and accelerated investment in serialization-ready cartons, aggregation systems, and track-and-trace software. Canada follows with a steady uptake of recyclable and fiber-based secondary packaging aligned with national sustainability targets.

Primary growth drivers include serialization compliance, high biologics penetration, and a mature contract packaging ecosystem. Companies such as WestRock and Amcor have expanded healthcare-focused converting and cold-chain capabilities in the region, supporting temperature-sensitive biologics and specialty drugs. PCI Pharma Services has invested in the U.S. clinical trial packaging and cold-chain infrastructure, strengthening domestic biologics handling capacity. Consolidation trends, including strategic acquisitions by Berry Global in healthcare packaging, enhance technical scale and GMP-compliant capacity. These developments reinforce high barriers to entry and favor established converters with validated facilities, automation systems, and integrated serialization software, thereby sustaining North America’s leadership position.

Europe Pharmaceutical Secondary Packaging Market Trends - FMD Compliance and Sustainable Carton Innovation

Europe is the second-largest regional market, supported by advanced pharmaceutical manufacturing in Germany, the U.K., France, and Spain. Regulatory harmonization under the Falsified Medicines Directive (FMD) has standardized serialization and tamper-evident requirements across EU member states, increasing demand for high-precision folding cartons and aggregation solutions. Compliance with FMD since 2019 continues to shape long-term packaging investment cycles.

Germany leads in high-value biologics and parenteral packaging, supported by strong export activity and advanced converting capabilities. Gerresheimer has expanded pharmaceutical packaging production capacity in Germany to meet rising demand for injectable and biologic therapies. The United Kingdom functions as a commercial and logistics hub, with contract packaging specialists such as Wasdell Group investing in serialization and cold-chain secondary packaging services. In fiber-based solutions, Stora Enso has strengthened its renewable and recyclable cartonboard offerings to address tightening EU sustainability regulations. France and Spain contribute through manufacturing exports and regional distribution networks. Across Europe, capital expenditure increasingly targets digital printing for late-stage customization, recycled fiber production, and export-oriented thermal packaging formats, reinforcing the region’s compliance-driven and sustainability-focused growth trajectory.

Asia Pacific Pharmaceutical Secondary Packaging Market Trends - Manufacturing Scale-Up and Export-Led Growth

Asia Pacific represents the fastest-growing regional market, driven by pharmaceutical manufacturing expansion in China and India, alongside high-precision biologics production in Japan. China’s pharmaceutical industrial policy and India’s Production Linked Incentive (PLI) schemes have stimulated domestic drug manufacturing capacity, directly increasing demand for compliant secondary packaging formats. ASEAN markets, including Indonesia and Vietnam, are witnessing rising OTC and generic drug consumption supported by urbanization and expanding healthcare access.

Major regional and multinational packaging firms are scaling capacity to capture this growth. UFlex has expanded pharmaceutical packaging production lines in India to serve export-oriented drug manufacturers. Huhtamaki continues to invest in flexible and printed packaging capabilities across Southeast Asia to support healthcare clients. In Japan, Dai Nippon Printing has advanced high-barrier blister and carton solutions for precision biologics and specialty medicines. Governments across the region are aligning with global serialization standards, prompting increased investment in track-and-trace systems and GMP-certified packaging facilities. Competitive manufacturing costs, combined with expanding contract packaging partnerships with multinational pharmaceutical firms, position Asia Pacific as both a high-growth domestic market and a strategic export base to North America and Europe.

Competitive Landscape

The global pharmaceutical secondary packaging market is semi-consolidated, with global packaging leaders holding significant share in premium segments such as cold-chain and serialization-integrated solutions. Regional converters serve local pharmaceutical clients and specialized niches. Leading firms prioritize consolidation, vertical integration, digital serialization services, and sustainability innovation. Differentiation is achieved through validated cold-chain capabilities, multi-site GMP compliance, and integrated contract packaging solutions.

Key Industry Developments

- In July 2025, AptarGroup introduced a nasal spray pump made with 52% bio-based feedstock, marking a sustainability milestone in pharmaceutical packaging components.

Companies Covered in Pharmaceutical Secondary Packaging Market

- Amcor plc

- WestRock Company

- Berry Global Inc.

- Gerresheimer AG

- Stora Enso Oyj

- Sonoco Products Company

- Huhtamaki Oyj

- AptarGroup, Inc.

- CCL Industries Inc.

- Constantia Flexibles Group GmbH

- UFlex Ltd.

- DS Smith plc

- Smurfit Westrock plc

- Mondi plc

- Mayr-Melnhof Karton AG

- PCI Pharma Services

- Wasdell Group

- Schott AG

Frequently Asked Questions

The pharmaceutical secondary packaging market size is estimated to be US$48.6 billion in 2026.

The global pharmaceutical secondary packaging market is projected to reach approximately US$72.4 billion by 2033.

Key trends include widespread serialization and track-and-trace integration, expansion of cold-chain and insulated packaging for biologics, rising adoption of sustainable and recyclable fiber-based cartons, automation in contract packaging facilities, and digital printing for late-stage customization.

Folding cartons lead the market by packaging type with an anticipated 38.7% market share, while prescription drugs dominate by application with an anticipated 45.6% share in 2026.

The pharmaceutical secondary packaging market is projected to grow at a CAGR of 5.8% between 2026 and 2033.

Major players include Amcor plc, WestRock Company, Berry Global Inc., Gerresheimer AG, and Stora Enso Oyj.