- Healthcare Services

- Pharmaceutical Contract Sales Outsourcing Market

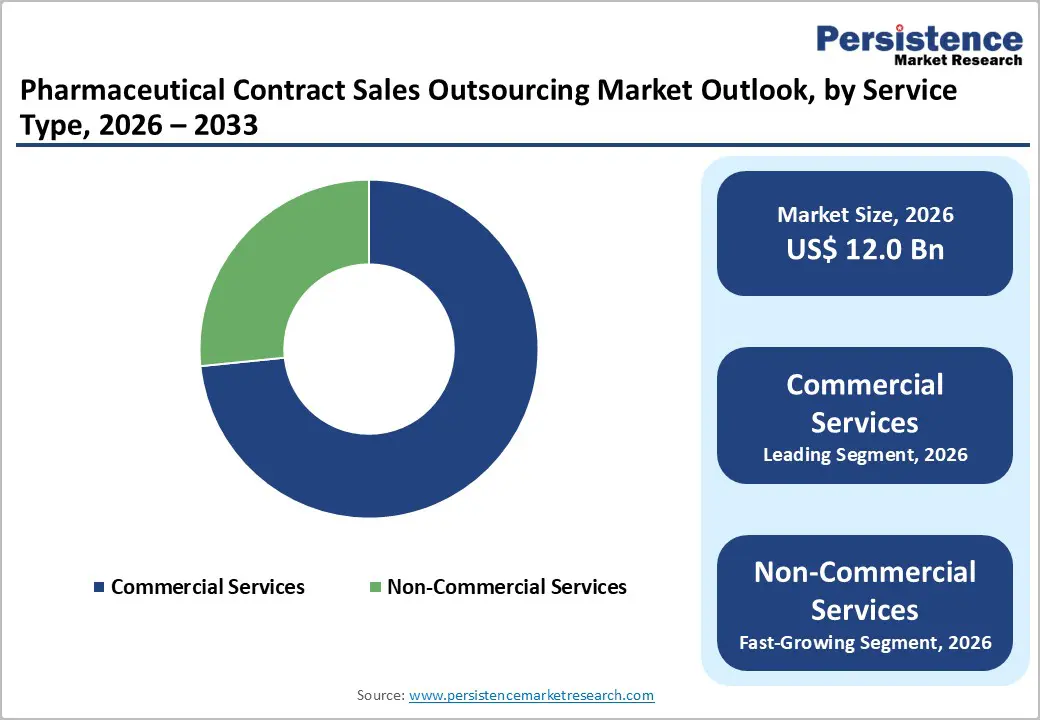

Pharmaceutical Contract Sales Outsourcing Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Pharmaceutical Contract Sales Outsourcing Market by Service Type (Commercial Services, Non-Commercial Services), Therapeutic Area (Oncology, Cardiovascular Disorder, Metabolic Disorders, Neurolog, Infectious Disease, Orthopedic Disease, Others), and Regional Analysis from 2026 to 2033

Pharmaceutical Contract Sales Outsourcing Market Share and Trends Analysis

The global pharmaceutical contract sales outsourcing market size is estimated to grow from US$ 12.0 billion in 2026 to US$ 21.3 billion by 2033, growing at a CAGR of 8.5% during the forecast period from 2026 to 2033.

The global market is witnessing a steady growth, driven by the rise in pharmaceutical outsourcing, specialty drug launches, and cost optimization strategies. Expanding commercialization pipelines and demand for flexible field sales models support market expansion. North America leads due to mature outsourcing adoption, while Asia-Pacific grows rapidly with rising pharma investments and market access expansion.

Key Industry Highlights:

- Dominant Segment: Oncology accounts for 33.4% share of the pharmaceutical contract sales organizations (CSO) market in 2025, driven by increasing specialty drug launches, complex biologics commercialization, and demand for highly trained field forces. The need for targeted physician engagement, hospital detailing, and value-based selling strategies supports sustained outsourcing in oncology portfolios.

- Dominant Region: North America leads the pharmaceutical CSO market in 2025 with 42.3% share, supported by mature outsourcing adoption, strong specialty drug pipelines, and the presence of major pharmaceutical companies. Advanced commercialization models and high promotional spending drive dominance, while Asia-Pacific remains the fastest-growing region due to expanding pharma investments and improving market access infrastructure.

- Growth Indicators: Rising pharmaceutical cost pressures, increasing specialty and biologic drug launches, growing need for flexible sales models, expansion of emerging biotech companies lacking in-house sales teams, and demand for data-driven commercial strategies are key growth drivers.

- Opportunity: Opportunities include expansion of hybrid and digital detailing models, penetration into emerging markets, partnerships with mid-sized and virtual biotech firms, integration of real-world data analytics in sales strategies, and specialized contract teams for rare diseases and precision medicine portfolios.

| Key Insights | Details |

|---|---|

| Global Pharmaceutical Contract Sales Outsourcing Market Size (2026E) | US$ 12.0 Bn |

| Market Value Forecast (2033F) | US$ 21.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.3% |

Market Dynamics

Driver: Rising Outsourcing of Pharmaceutical Commercial Operations

A major structural shift in the pharmaceutical industry is the increasing outsourcing of commercial operations, including salesforce deployment, physician engagement, and patient support programs. According to the U.S. Bureau of Labor Statistics (BLS), pharmaceutical and medicine manufacturing employed over 330,000 workers in 2023, while employment in professional and business services where outsourced commercial providers are categorized, exceeded 22 million, reflecting the broader shift toward contracted service models. Additionally, the U.S. Food and Drug Administration (FDA) approved 55 novel drugs in 2023, sustaining a high volume of product launches that require rapid commercialization. Outsourcing enables pharmaceutical companies to scale field teams quickly without expanding fixed payroll infrastructure.

This trend is further supported by cost pressures and evolving healthcare delivery models. Data from the U.S. Centers for Medicare & Medicaid Services (CMS) show that national health expenditures reached USD 4.5 trillion in 2022, growing 4.1% year-over-year, intensifying scrutiny on pharmaceutical spending and promotional efficiency. Maintaining large in-house salesforces involves fixed salaries, compliance training, travel, and administrative costs. By contrast, CSO models convert fixed costs into variable contractual expenses, allowing firms to align sales resources with product lifecycle stages. Moreover, increasing specialization in oncology, rare diseases, and biologics requires highly trained representatives, which outsourced providers can deploy more flexibly across geographies.

Restraints: Regulatory and Compliance Complexities Across Regions

One of the most persistent restraints on the Pharmaceutical CSO Market is the regulatory complexity involved in cross-border commercial activities. Outsourced sales teams must comply with multiple regulatory frameworks, including GDPR in Europe, HIPAA in the U.S., and local promotional codes which significantly increases governance costs. This has been documented as a material burden for CSOs, forcing them to allocate extensive resources to compliance training and legal oversight rather than direct sales execution.

For example, industry compliance bodies such as the Prescription Medicines Code of Practice Authority (PMCPA) in the U.K. recorded 264 complaints about potential promotional code breaches in 2024, illustrating the level of scrutiny applied to pharmaceutical sales practices. These regulatory demands slow the deployment of outsourced teams and require continuous investment in governance infrastructure. Inconsistent regulatory requirements across regions can also delay market entry and complicate messaging for CSO field forces. As a result, many pharmaceutical companies find that compliance concerns erode some of the anticipated cost and agility benefits of outsourcing.

Opportunity: Growth of Hybrid and Digital Sales Engagement Models

The proliferation of hybrid and digital sales engagement models represents a significant opportunity for the CSO market. Traditional in-person detailing is being augmented or partially replaced by technology-enabled interactions, including virtual engagement, CRM analytics, and data-driven targeting systems that extend reach beyond conventional field forces. CSO providers are increasingly adopting these tools, enabling sponsors to optimize engagement while controlling costs.

Statistical trends support this shift: industry data suggests 61% of pharmaceutical companies have integrated digital technologies into their sales processes in the past five years, reflecting the migration toward omnichannel engagement strategies that blend digital and face-to-face interactions. This trend accelerates the relevance of hybrid sales models in a post-COVID environment, where healthcare professionals increasingly prefer remote or mixed engagement formats. Enhanced digital tools improve metrics like targeting precision, messaging personalization, and performance reporting, creating measurable ROI improvements.

CSOs that build robust hybrid capabilities stand to capture larger portions of the overall market by offering flexible, tech-driven commercial solutions that align with evolving prescriber preferences and pharmaceutical commercialization strategies.

Category-wise Analysis

By Service Type, Commercial Services Dominate the Pharmaceutical Contract Sales Outsourcing Market

Commercial Services occupies 73.4% share of the global market in 2025, because they encompass core revenue-generating functions such as salesforce deployment, physician detailing, market access support, and promotional activities. In the United States alone, prescription drug sales exceeded $600 billion in 2023, according to online studies by leading companies, underscoring the scale of commercial activity that needs effective execution. The FDA approved 55 novel drugs in 2023, many of which, particularly oncology and rare disease treatments, require specialized sales engagement for adoption by healthcare professionals. Outsourcing commercial services allows pharmaceutical firms to scale sales forces with experienced teams, avoid long recruitment cycles, and manage regulatory compliance. Government data show that healthcare providers increasingly engage with product specialists; for example, the American Medical Association reports that physician detailing influences prescribing behavior for approximately 40-60% of new products, which drives demand for professional commercial services.

By Therapeutic Area, High cancer incidence and complex oncology drugs drive specialized outsourced sales engagement demand

Oncology dominates because cancer therapies represent one of the largest and fastest-growing segments of the pharmaceutical pipeline, requiring intensive commercialization. The U.S. National Cancer Institute estimates that over 1.9 million new cancer cases were diagnosed in 2023, and oncology drug spending reached ~$200 billion annually in major markets, reflecting high treatment demand. Oncology drugs often involve complex mechanisms, narrow indications, and specialized administration pathways, making tailored sales engagement critical for uptake. The FDA’s Center for Drug Evaluation and Research noted that a significant share of novel drug approvals in recent years are oncology or hematology agents. These treatments require skilled field teams to educate physicians on clinical data and real-world use, increasing outsourcing to CSOs with oncology expertise. As a result, oncology accounts for the largest share of CSO therapeutic engagement.

Regional Insights

North America Pharmaceutical Contract Sales Outsourcing Market Trends

North America holds the largest share of the market, with 42.3% of global market revenue, because it remains the world’s largest pharmaceutical market with an advanced commercialization infrastructure. According to the U.S. Centers for Medicare & Medicaid Services (CMS), national prescription drug spending in the U.S. exceeded $370 billion in 2023, reflecting substantial demand for drug promotion and sales engagement. The region also hosts the headquarters of many global pharmaceutical firms, leading to intensive outsourcing of field forces to specialist CSOs. The U.S. Food and Drug Administration (FDA) reported 55 novel drug approvals in 2023, many requiring targeted physician engagement, further boosting CSO demand. Additionally, healthcare providers in the U.S. and Canada are among the most accessible for structured sales interactions, which increases the utility of outsourced commercial services. High regulatory standards and advanced market access practices reinforce reliance on professional CSOs for compliance-aligned promotion.

Europe Pharmaceutical Contract Sales Outsourcing Market Trends

Europe is strategically important due to its large elderly population and high chronic disease prevalence, which drive sustained demand for pharmaceuticals. Eurostat reports that over 20% of the EU population was aged 65 or older in 2023, elevating demand for treatments requiring ongoing commercial support. The European Medicines Agency (EMA) approved numerous novel therapeutic agents in recent years, many requiring localized sales strategies to address diverse healthcare systems across EU member states. Countries such as Germany, France, and the UK have substantial healthcare expenditures, with OECD data indicating that pharmaceutical spending accounts for about 16% of total health expenditure in major European markets. This diversity of regulatory frameworks and multilingual regions increases demand for outsourced CSOs with localized expertise in physician engagement and market access.

Asia-Pacific Pharmaceutical Contract Sales Outsourcing Market Trends

Asia Pacific’s rapid growth is driven by expanding pharmaceutical consumption and rising healthcare investments. The World Health Organization’s Global Health Expenditure Database shows that countries like China and India increased health spending by over 7% annually between 2018-2022, signaling expanding access to medicines. China has become the second-largest global pharmaceutical market, with prescription drug sales exceeding $170 billion in 2023, according to national health statistics, creating demand for commercial support. Additionally, regulatory reforms in markets like India, South Korea, and Japan have accelerated approvals of innovative therapies, necessitating outsourced sales expertise. A growing middle class and increased insurance coverage expand treatment uptake, while local biotech growth fuels the need for scalable CSO solutions. Lower operational costs and expanding logistics infrastructure further attract global CSOs into the region.

Competitive Landscape

The pharmaceutical contract sales organizations (CSO) market is moderately consolidated, led by global players such as IQVIA, Syneos Health, Inizio Engage, and Amplity Health, alongside regional specialists. Competition centers on therapeutic expertise, geographic reach, digital capabilities, and flexible deployment models. Strategic partnerships, oncology-focused teams, and hybrid engagement solutions drive differentiation and long-term contracts.

Key Industry Developments:

- In September 2025, Pharmaceutical contract sales organizations redefined field deployment strategies by integrating AI-enabled technologies into their commercial operations. Companies implemented artificial intelligence-driven analytics to optimize territory alignment, physician targeting, and call planning, improving field force productivity and engagement efficiency. AI tools were used to analyze prescription trends, patient demographics, and real-world data, enabling more precise deployment of sales representatives across high-potential regions and therapeutic segments.

- In January 2025, Syneos Health signed an agreement with ACTIVATO to strengthen clinical trial operations in Japan. The collaboration aimed to enhance local study execution by combining Syneos Health’s global clinical development capabilities with ACTIVATO’s regional expertise, site network, and regulatory knowledge within the Japanese market.

Companies Covered in Pharmaceutical Contract Sales Outsourcing Market

- IQVIA, Inc.

- Syneos Health

- Ashfield Medcomms.

- Axxelus

- EPS Corp.

- QFR Solutions

- MaBico

- Mednext Pharma Pvt. Ltd.

- Peak Pharma Solutions Inc.

- Promoveo Health

- Zuellig Pharma Corporation

- Inizio Engage

- Amplity, Inc.

- GTS Solution

- DistriPhil

- CMIC HOLDINGS Co., LTD.

- Mercalis

- Mednext Pharmaceuticals Pvt. Ltd.

- Outsourced

- Others

Frequently Asked Questions

The global pharmaceutical contract sales outsourcing market is projected to be valued at US$ 12.0 Bn in 2026.

Rising pharmaceutical outsourcing, specialty drug launches, cost optimization, and flexible commercial deployment demand.

The global pharmaceutical contract sales outsourcing market is poised to witness a CAGR of 8.5% between 2026 and 2033.

Expansion into emerging markets, digital engagement models, oncology specialization, and biotech partnerships.

IQVIA, Inc, Syneos Health, Ashfield Medcomms, Axxelus, EPS Corp., QFR Solutions.