- Smart Packaging

- Blister Packs Pharmaceutical Packaging Market

Blister Packs Pharmaceutical Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Blister Packs Pharmaceutical Packaging Market by Material Composition (Plastic-Based Films, Multi-Layer Laminates, Others), Drug Form (Solid Oral Dosage Forms, Transdermal Patches, Others), Functionality, Distribution Channel, and Regional Analysis for 2026 - 2033

Blister Packs Pharmaceutical Packaging Market Size and Trends Analysis

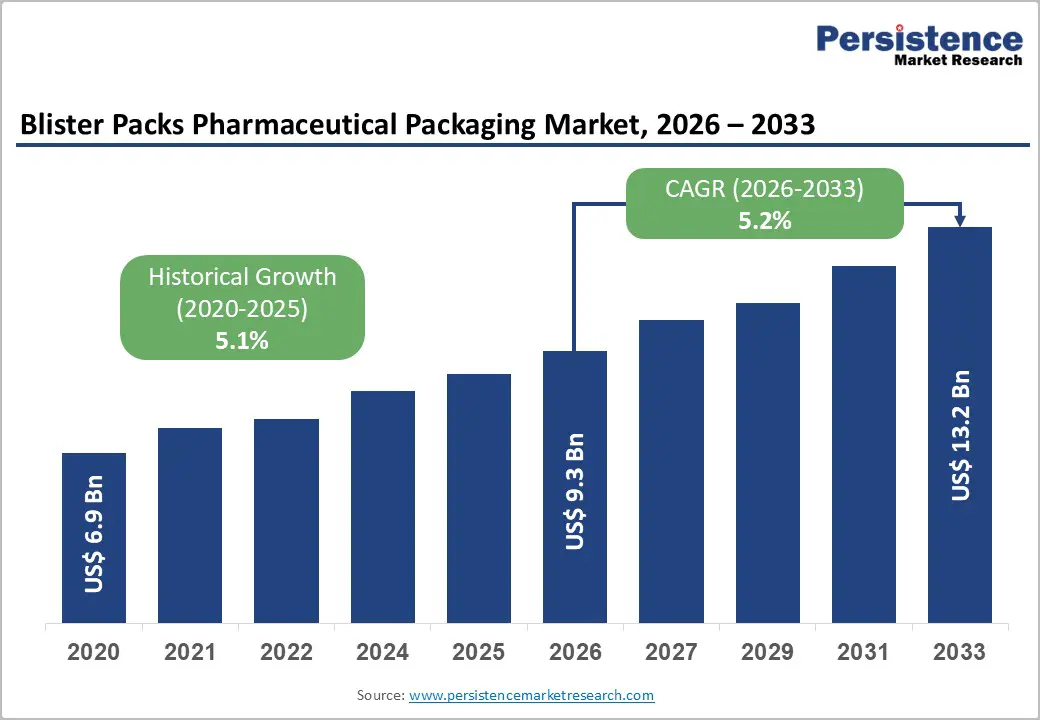

The global blister packs pharmaceutical packaging market size is likely to be valued at US$9.3 billion in 2026 and is expected to reach US$13.2 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033, driven by rising oral solid dosage production, stricter regulatory requirements for patient safety, and expanding adoption of child-resistant and environmentally sustainable blister formats.

Ongoing investments by pharmaceutical manufacturers and contract packagers in advanced blister technologies, including serialization and high-barrier materials, continue to elevate the value contribution of primary packaging. Regulatory compliance and patient-safety performance are expected to remain the primary purchasing criteria throughout the forecast period.

Key Industry Highlights

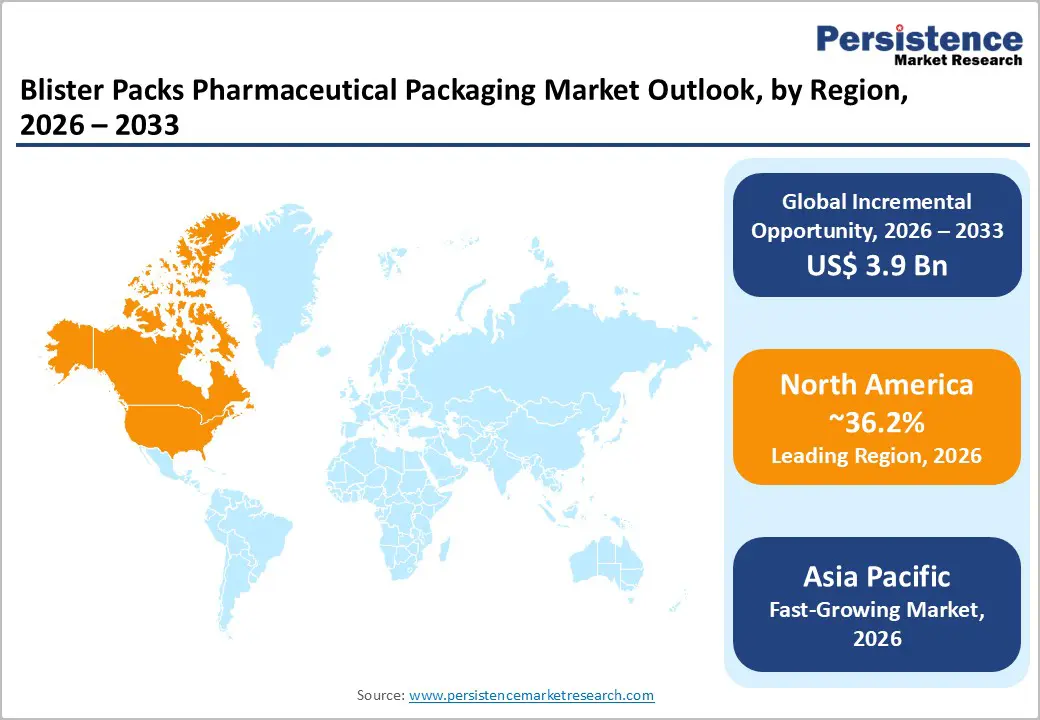

- Leading Region: North America is projected to account for approximately 36.2% of market share in 2026, supported by high pharmaceutical consumption, strong specialty drug pipelines, and advanced regulatory-compliant blister packaging infrastructure.

- Fastest-growing Region: Asia Pacific, projected to register the highest regional growth rate, driven by rapid expansion of generics manufacturing, export-oriented pharmaceutical production, and increasing investment in high-speed blistering and compliance upgrades.

- Investment Plans: Major investments are focused on automation, serialization-ready blister lines, sustainable mono-material blister systems, and digital printing technologies, with converters allocating multi-million-dollar capital expenditure to upgrade thermoforming, lamination, and traceability capabilities.

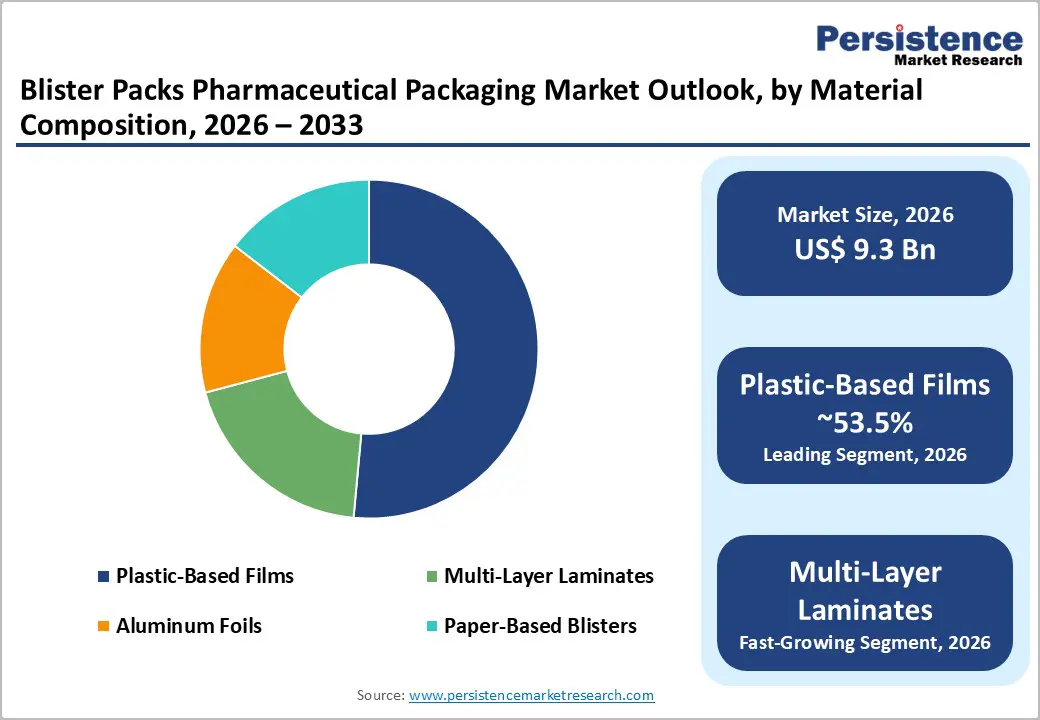

- Dominant Material Composition: Plastic-based films are anticipated to hold an estimated 53.5% market share in 2026, due to cost efficiency, widespread installed thermoforming capacity, and strong suitability for high-volume tablet and capsule packaging.

- Leading Drug Form: Solid oral dosage forms are estimated to account for approximately 71.7% of the market share, supported by large-scale production of tablets and capsules for chronic and acute therapies across retail, hospital, and export channels.

| Key Insights | Details |

|---|---|

| Blister Packs Pharmaceutical Packaging Market Size (2026E) | US$9.3 Bn |

| Market Value Forecast (2033F) | US$13.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Oral Solid-Dosage Manufacturing and Unit-Dose Adherence Requirements

The growing prevalence of chronic diseases and aging populations has significantly increased prescription volumes for oral solid dosage forms. Pharmaceutical companies are expanding tablet and capsule manufacturing capacity to meet long-term therapy demand, particularly for cardiovascular, metabolic, and central nervous system treatments. Unit-dose blister packaging supports medication adherence by enabling accurate dosing, reducing dispensing errors, and improving patient compliance through calendar-based formats. Public-health initiatives and institutional healthcare providers increasingly favor blister packs for controlled dispensing. Regulatory guidance supporting unit-dose labeling and packaging further reinforces adoption, collectively underpinning the market’s sustained mid-single-digit growth trajectory.

Regulatory Mandates for Anti-Counterfeiting, Serialization, and Patient Safety

Regulatory authorities across major pharmaceutical markets require enhanced traceability and tamper protection for medicinal products. Serialization, tamper-evident seals, and child-resistant features are increasingly mandated across primary packaging formats. Blister packs provide a practical platform for integrating these requirements through printed lidding foils, unique identifiers, and track-and-trace technologies. Pharmaceutical manufacturers and packaging suppliers are investing heavily in digital printing, inspection systems, and serialization-ready blister lines. These compliance-driven upgrades increase the per-unit value of blister packaging and favor suppliers with advanced technical and regulatory capabilities.

Barrier Analysis - Raw-Material Cost Volatility and Sustainability Transition Pressures

Fluctuations in prices for polymer resins, aluminum foil, and high-barrier laminates continue to challenge cost stability across the blister packaging supply chain. At the same time, pharmaceutical companies are accelerating the transition toward recyclable and mono-material blister formats, which often require new tooling, material qualification, and production-line modifications. These investments increase capital expenditure and unit costs for converters and contract packagers. While some cost increases can be passed through, price sensitivity among high-volume pharmaceutical customers limits margin recovery, leading to consolidation and selective capacity rationalization.

Regulatory Complexity and Barriers to Advanced Blister Functionality

Advanced blister solutions incorporating child resistance, tamper evidence, or digital connectivity require extensive engineering validation, stability testing, and regulatory documentation. These requirements extend development timelines and increase time-to-market for new packaging formats. Smaller and regional packaging providers often lack in-house regulatory expertise and quality infrastructure, limiting their ability to compete in higher-margin, feature-rich segments. As a result, innovation is concentrated among larger suppliers, while adoption in cost-sensitive markets remains slower due to compliance-related cost and time constraints.

Opportunity Analysis - Sustainable Blister Materials and Recycle-Ready Thermoforming

Pharmaceutical manufacturers are setting measurable sustainability targets, creating strong demand for recyclable and mono-material blister solutions. Recycle-ready thermoformed blisters simplify end-of-life processing while maintaining necessary barrier performance. If even 10-20% of plastic-based blister volumes transition to validated recyclable formats over the next five years, the resulting incremental addressable value would represent a substantial revenue opportunity for material suppliers and converters. Companies offering low-permeability mono-polymer systems, supported by life-cycle assessments and regulatory validation, are positioned to secure premium pricing and long-term supply agreements with global pharmaceutical clients.

Digitally Enabled Adherence Solutions for Clinical Trials and Specialty Therapies

Blister packs integrated with digital identifiers, sensors, or data carriers enable real-time adherence monitoring and are gaining traction in clinical trials and specialty drug programs. These solutions support improved patient outcomes, data collection, and regulatory reporting. Although penetration remains limited, even single-digit adoption across blister volumes generates disproportionate revenue due to higher per-unit pricing and service-based data contracts. Strategic partnerships between packaging converters, technology providers, and pharmaceutical sponsors are accelerating pilot programs, with commercial-scale adoption expected to expand as specialty therapies and decentralized clinical trials increase.

Category-wise Analysis

Material Composition Insights

Plastic-based films are anticipated to account for approximately 53.5% of market share, maintaining their position as the dominant material category in pharmaceutical blister packaging. Thermoformed materials such as PVC, PET, and PET/PE structures are extensively used due to their cost efficiency, stable thermoforming behavior, and seamless compatibility with high-speed blistering lines. These materials enable consistent cavity depth, uniform tablet positioning, and dependable heat-sealing with aluminum lidding foils, making them ideal for mass-market tablet and capsule packaging. Plastic-based blisters are widely deployed for high-volume therapies such as analgesics, antihypertensives, antibiotics, and vitamin supplements. Hospitals, retail pharmacies, and contract packaging organizations continue to rely on these materials for both acute and chronic therapies, supported by a well-established global resin supply chain and standardized regulatory acceptance. Their balance of performance, scalability, and affordability sustains their leadership across developed and emerging pharmaceutical markets.

Multi-layer laminates are anticipated to witness accelerated adoption, emerging as the fastest-growing material category. These structures combine multiple functional layers, including polymers, aluminum foil, and coated films, to deliver superior resistance to moisture, oxygen, and light. Such barrier performance is critical for moisture-sensitive and oxygen-reactive formulations that demand extended shelf life without relying on secondary protective packaging. Multi-layer laminates are increasingly used for specialty pharmaceuticals, oncology drugs, hormone therapies, and high-potency formulations where product stability is paramount. Their ability to support high-resolution printing for serialization, tamper-evidence markings, and regulatory information enhances their value proposition. Converters investing in advanced lamination processes, cold-form technologies, and digital printing capabilities are well positioned to capture premium contracts as pharmaceutical companies prioritize product integrity and compliance-driven packaging upgrades.

Drug Form Insights

Solid oral dosage forms are anticipated to retain dominance, accounting for approximately 71.7% of market share. Tablets and capsules align naturally with blister formats due to their uniform geometry, stability, and suitability for unit-dose presentation. Blister packs provide clear dose separation, physical protection, and space for patient instructions, which supports adherence across chronic treatment regimens. This segment benefits from extensive use in therapeutic areas such as cardiovascular disease, diabetes, gastrointestinal disorders, and pain management. Blister packs are widely distributed through retail pharmacies, hospital dispensaries, and export-oriented supply chains. Most pharmaceutical manufacturing and packaging facilities remain optimized for high-speed tablet and capsule blistering, reinforcing economies of scale and sustaining the segment’s leadership position throughout the forecast period.

Transdermal patches are anticipated to experience rapid uptake, making them the fastest-growing drug form within blister packaging. Growth is driven by rising adoption of transdermal delivery systems for pain management, hormonal therapies, smoking cessation, and neurological treatments. These products require specialized blister cavities, precise sealing, and high-barrier protection to preserve adhesive performance and ensure controlled drug release.

Blister packaging plays a critical role in protecting patches from moisture ingress, deformation, and contamination during storage and transport. As wearable, non-invasive drug delivery systems gain acceptance among patients and healthcare providers, pharmaceutical companies are increasingly investing in tailored blister solutions for transdermal formats. This trend is generating above-average revenue growth for packaging suppliers capable of meeting specialized design and barrier requirements.

Regional Insights

North America Blister Packs Pharmaceutical Packaging Market Trends - FDA-Driven Unit-Dose Adoption and Serialization-Ready Premium Blisters

North America is projected to lead the market, accounting for approximately 36.2% of the market share. High per-capita pharmaceutical consumption, a strong specialty and biologics pipeline, and advanced healthcare infrastructure sustain consistent demand for validated blister packaging solutions. The U.S. market is characterized by large-scale adoption of unit-dose packaging for both retail and institutional distribution, particularly for chronic therapies, oncology drugs, and controlled substances. Regulatory oversight from the U.S. Food and Drug Administration (FDA) strongly influences packaging design and material selection. Requirements related to container-closure integrity, child resistance, tamper evidence, and stability testing drive pharmaceutical companies toward high-quality blister formats rather than loose or bulk packaging. Compliance with the Drug Supply Chain Security Act (DSCSA) has further accelerated investments in serialization-ready blister packs, high-resolution printing, and track-and-trace integration. Packaging suppliers serving North America increasingly differentiate through validated materials, data integrity, and audit readiness.

From an industry standpoint, the region benefits from a dense ecosystem of contract packaging organizations (CPOs) and advanced converters. Companies such as WestRock, Berry Global, Amcor, and Tekni-Plex maintain significant blister packaging operations supporting both branded and generic pharmaceutical manufacturers. Ongoing investments in automation, robotics, and inspection systems enable high throughput while meeting stringent quality standards. Sustainability initiatives, such as PVC reduction, recyclable lidding foils, and downgauged materials, are gaining traction, particularly among multinational pharmaceutical brands with public ESG commitments. Together, regulatory rigor, capital investment, and innovation capacity reinforce North America’s leadership and premium product mix positioning.

Europe Blister Packs Pharmaceutical Packaging Market Trends - EMA Harmonization, Anti-Counterfeiting, and Sustainable Blister Innovation

Europe represents a substantial share of global blister packaging demand, supported by a strong pharmaceutical manufacturing base, export-oriented production, and regulatory harmonization across member states. Germany and the U.K. serve as key hubs for advanced pharmaceutical packaging, clinical-trial blistering, and high-barrier material innovation, while France and Spain contribute significant volumes through generics manufacturing and public hospital procurement programs.

A defining market driver across Europe is regulatory alignment under the European Medicines Agency (EMA) and the Falsified Medicines Directive (FMD). Mandatory serialization, tamper-evident features, and safety labeling have elevated baseline blister packaging standards across the region. As a result, pharmaceutical companies increasingly favor blister formats that integrate overt and covert anti-counterfeiting elements, high-quality print registration, and secure sealing performance. These requirements have driven steady demand for aluminum-based and multi-layer laminate blisters, particularly for prescription medicines distributed across multiple EU markets.

European packaging leaders such as Constantia Flexibles, Klöckner Pentaplast, Essentra, and Amcor play a central role in advancing sustainable blister technologies, including PVC-free structures, recyclable mono-material concepts, and paper-based blister alternatives. Investment trends reflect a balance between compliance upgrades and sustainability-driven innovation. Consolidation among mid-sized converters is improving regional coverage and technical depth, enabling suppliers to support pharmaceutical clients across development, commercial launch, and lifecycle management. These factors position Europe as a technically sophisticated and regulation-driven blister packaging market.

Asia Pacific Blister Packs Pharmaceutical Packaging Market Trends - Export-Led Manufacturing Scale and Regulatory Upgrading in Generics

Asia Pacific is the fastest-growing regional market for pharmaceutical blister packaging, driven by rapid expansion of pharmaceutical manufacturing, increasing healthcare access, and cost-competitive production capabilities. China and India lead regional demand through large-scale generics manufacturing, domestic consumption growth, and export-oriented pharmaceutical supply chains. Blister packaging remains the preferred format for tablets and capsules distributed across both regulated and semi-regulated markets.

India’s role as a global generics supplier has accelerated investments in high-speed blister lines, serialization-ready packaging, and compliance upgrades aligned with U.S. FDA and European regulatory expectations. Major Indian pharmaceutical companies, including Sun Pharma, Dr. Reddy’s, Cipla, and Aurobindo Pharma, increasingly rely on blister packaging for export markets, reinforcing demand for aluminum-based and multi-layer laminate structures. China continues to expand blister packaging capacity alongside its growing domestic pharmaceutical market, with increasing emphasis on quality consistency and regulatory alignment.

Japan represents a distinct segment within Asia Pacific, emphasizing precision packaging, patient compliance, and premium materials for branded therapies. Meanwhile, ASEAN countries such as Singapore, Malaysia, and Vietnam are emerging as regional contract packaging hubs, supported by favorable investment policies and improving regulatory frameworks. Packaging suppliers are investing in digital printing, automation, and inspection technologies to meet multinational quality requirements. Collectively, manufacturing scale, regulatory upgrading, and export-driven demand position Asia Pacific for sustained above-average growth in pharmaceutical blister packaging.

Competitive Landscape

The global blister packs pharmaceutical packaging market is moderately concentrated at the top, with large global converters and material suppliers holding significant value share. The market remains fragmented among regional contract packagers serving generics and clinical-trial demand. Consolidation and strategic partnerships are increasing scale advantages for leading players, while smaller firms compete primarily on cost and regional proximity. Leading companies emphasize innovation, capacity scale, and regulatory excellence. Key strategic themes include sustainable material development, digital integration, and expansion through mergers and partnerships to support global pharmaceutical customers.

Key Industry Developments

- In September 2025, Romaco showcased its PET mono-material recyclable blister packs at PACK EXPO in Las Vegas, promoting PVC-free solutions that reduce carbon footprint while maintaining barrier properties.

- In June 2025, Schott Pharma launched a high-barrier blister packaging solution tailored for moisture- and oxygen-sensitive drugs, improving product stability and addressing a growing need for packaging that extends shelf life, particularly for specialty therapeutics.

Companies Covered in Blister Packs Pharmaceutical Packaging Market

- Amcor plc

- Gerresheimer AG

- West Pharmaceutical Services, Inc.

- Berry Global Group, Inc.

- SCHOTT AG

- AptarGroup, Inc.

- Becton, Dickinson and Company

- CCL Industries Inc.

- Constantia Flexibles Group GmbH

- Uflex Limited

- Bilcare Limited

- Huhtamaki Oyj

- Nelipak Healthcare Packaging

- Origin Pharma Packaging

- SGD Pharma

- Tekni-Plex, Inc.

- Winpak Ltd.

- Klockner Pentaplast Group

Frequently Asked Questions

The global blister packs pharmaceutical packaging market size is valued at US$9.3 billion in 2026.

By 2033, the blister packs pharmaceutical packaging market is expected to reach approximately US$13.2 billion.

Key trends shaping the market include the shift toward high-barrier multi-layer laminates, increasing adoption of serialization-ready and tamper-evident blister packs, and rising investment in environmentally sustainable blister materials.

Plastic-based films are the leading material segment, accounting for 53.5% market share, due to their cost efficiency, compatibility with high-speed blistering equipment, and widespread use in tablet and capsule packaging for both acute and chronic therapies.

The blister packs pharmaceutical packaging market is projected to grow at a CAGR of 5.2% between 2026 and 2033.

Major players include Amcor plc, Constantia Flexibles Group, WestRock Company, Berry Global Group, Inc., and Klöckner Pentaplast.