- Healthcare Services

- North America Smart Home Health Market

North America Smart Home Health Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

North America Smart Home Health Market by Product (Medical Device Alert Systems, Smart Glucose Monitoring System, Smart Cardiac Monitoring System, Smart Inhalers, Others), Technology (Wireless, Wired), Application (Fall Prevention and Detection, Health Status Monitoring), and Regional Analysis from 2026 to 2033

North America Smart Home Health Market Share and Trends Analysis

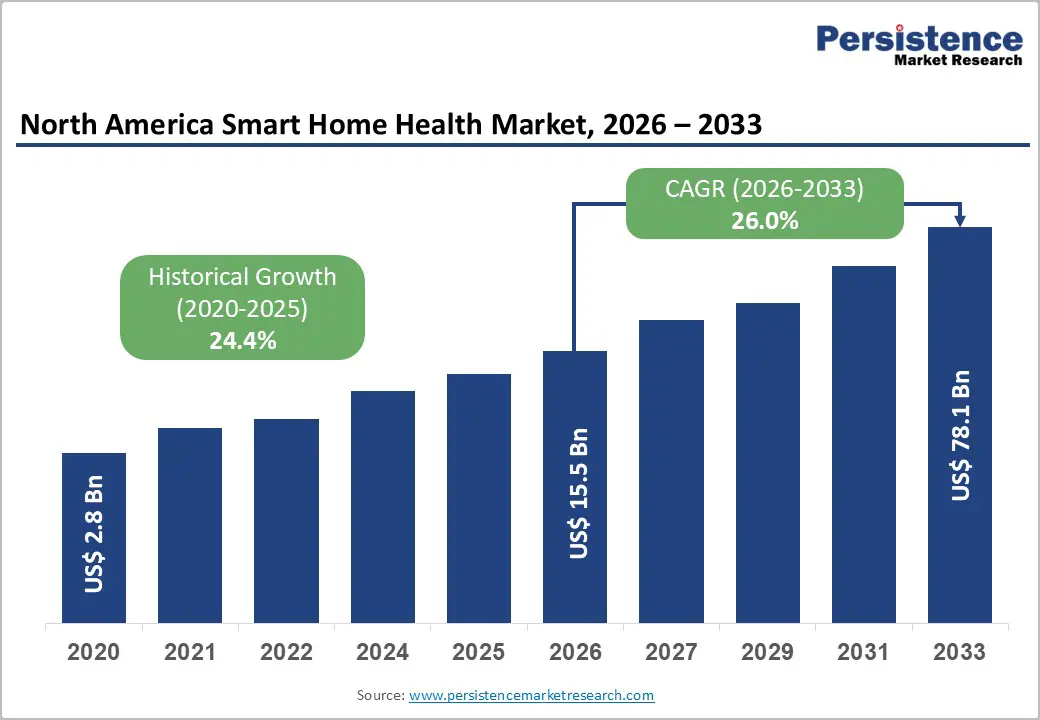

The North America smart home health market is estimated to reach US$ 15.5 billion in 2026 and US$78.1 billion by 2033, and is expected to record a CAGR of 26.0% during the forecast period from 2026 to 2033.

The North American smart home health market is growing steadily, driven by rising adoption of remote patient monitoring, connected medical devices, and digital healthcare platforms. Strong healthcare infrastructure, favorable reimbursement, and advanced IoT integration support regional leadership, while increasing chronic disease burden and aging populations continue to accelerate demand for home-based care solutions.

Key Industry Highlights:

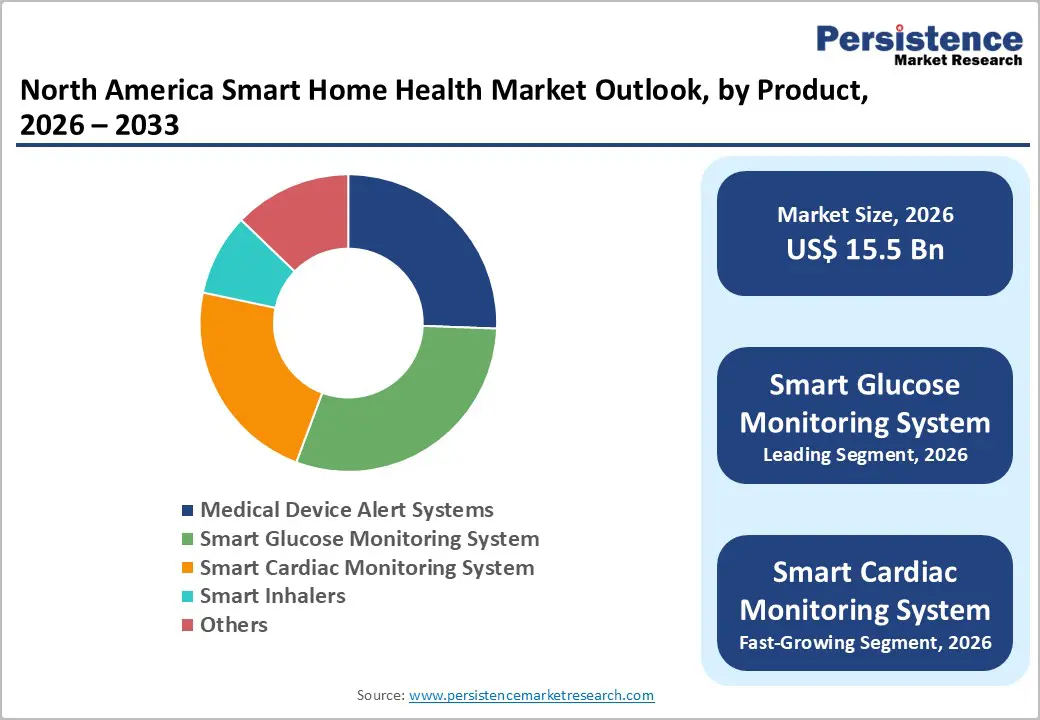

- Dominant Segment: Smart Glucose Monitoring Systems are a leading product segment in the North American smart home health market, with a 30.1% share in 2025, driven by the high prevalence of diabetes and strong adoption of continuous glucose monitoring (CGM) technologies. These systems enable real-time, remote tracking of blood glucose levels, seamless data sharing with clinicians, improved glycemic control, and strong reimbursement support, accelerating home-based diabetes management.

- Market Drivers: Key drivers include the rising prevalence of chronic diseases, aging population, growing preference for home-based care, expansion of telehealth services, advancements in IoT and AI-enabled health devices, and supportive reimbursement policies for remote patient monitoring.

- Market Opportunity: Significant opportunities exist in AI-powered monitoring platforms, integration of smart home health systems with telehealth, expansion of wireless technologies, data-driven personalized care, and increased adoption of smart home health solutions among older adults and chronic care populations.

| Key Insights | Details |

|---|---|

| North America Smart Home Health Market Size (2026E) | US$ 15.5 Bn |

| Market Value Forecast (2033F) | US$ 78.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 26.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 24.4% |

Market Dynamics

Driver: AI-Driven Personalized Healthcare & Predictive Analytics

AI-driven personalized healthcare and predictive analytics are significant growth drivers for the North American smart home health market, as they enable care tailored to individual patient needs and anticipate health events before they occur. AI-powered predictive analytics analyzes vast real-time and historical clinical data from electronic health records (EHRs), wearables, and other sources to identify patterns that predict disease progression, readmission risk, and treatment responses. As of 2024, about 71% of U.S. hospitals reported using predictive AI integrated with EHR systems, up from 66% in 2023, indicating rapid adoption in clinical settings to improve decision-making and care coordination.

These capabilities support personalized interventions and continuous remote monitoring. For example, AI-supported models can reduce ICU admissions, shorten hospital stays, and optimize staffing through accurate patient flow predictions. Predictive analytics has also been shown to help hospitals lower readmission rates by identifying high-risk patients early and enabling proactive outreach.

Restraints: High Upfront Costs for Advanced Systems

One key restraint for the North America smart home health market is the high upfront cost of deploying advanced technologies, which can impede adoption, especially among smaller providers and resource-limited care settings. Advanced smart home health systems, which integrate sensors, IoT connectivity, cloud infrastructure, and AI analytic,s require substantial initial investment in hardware, software platforms, and secure networking. These costs are compounded by ongoing expenses for device maintenance, software updates, technical support, and staff training, often straining constrained budgets. According to market analysis on IoT in healthcare, high implementation and integration costs remain significant barriers, despite the potential long-term benefits.

Moreover, reimbursement models for remote monitoring and next-generation connected devices continue to evolve, and many smart health technologies are not fully reimbursed under traditional fee-for-service structures. This creates uncertainty for healthcare organizations considering large upfront expenditures without guaranteed financial return. Even when projected long-term cost savings exist, the immediate capital outlay to acquire and integrate systems with existing EHRs and clinical workflows can deter adoption, particularly for smaller clinics, rural hospitals, and home care agencies. The financial burden associated with cutting-edge smart health infrastructure thus slows broad deployment across diverse provider segments.

Opportunity: Wearables & IoT Ecosystem Expansion

Expansion of wearables and the IoT ecosystem presents a major opportunity for the North American smart home health market by enabling continuous, real-time health monitoring outside traditional clinical settings. Wearable devices, such as smartwatches, fitness trackers, and medical sensors, capture biometric data including heart rate, glucose levels, activity patterns, and sleep quality. In 2022, over 100 million wearable devices (including smartwatches and medical sensors) were sold, and forecasts suggest sustained growth in wearable deployments as healthcare integration advances.

This growth directly fuels smart home health capabilities: IoT-enabled wearables enable remote patient monitoring, chronic disease management, and early detection of clinical deterioration, reducing hospital readmissions and easing the burden on acute care systems. Connectivity between wearables and clinical IT systems allows care teams to receive continuous data streams, improving patient engagement and enabling proactive interventions. The expansion of IoT also supports the broader healthcare ecosystem, with cellular and LPWAN IoT connections projected to exceed 4 billion globally by 2024, underscoring the scale of connectivity infrastructure available to support next-generation health devices.

For North America, where digital health adoption is high and infrastructure is advanced, this growth translates into stronger integration of wearable data into care plans and telehealth workflows. As interoperability improves and data analytics mature, wearables and IoT devices will become foundational to preventive care, personalized health insights, and population health strategies, representing a compelling market opportunity.

Category-wise Analysis

By Product Insights

Smart Glucose Monitoring System 30.1% share of the global market in 2025, because they address a critical chronic disease affecting over 40 million Americans (≈12 % of the population), making diabetes one of the most common long-term conditions requiring daily management. Continuous glucose monitors (CGMs) provide real-time glucose readings without frequent fingersticks, helping users and clinicians adjust insulin and lifestyle interventions more effectively than traditional monitoring. Their prevalence is increasing utilization among insured populations has been steadily rising, particularly in Medicare and Medicaid beneficiaries, reflecting broader clinical acceptance and reimbursement support. CGMs’ combination of effectiveness in diabetes self-management, continuous data, and integration with smartphones and health platforms drives their dominant market position within smart home health product portfolios.

By Technology Insights

Wireless technology dominates the smart home health market because it enables continuous, real-time data transmission, which is essential for remote monitoring and chronic disease management without physical tethering. Wireless protocols, such as Bluetooth and Wi-Fi, allow smart health devices, including glucose monitors and cardiac wearables, to send vital health data directly to smartphones, cloud platforms, or clinician dashboards, facilitating timely intervention and reducing the need for in-person visits. Continuous wireless connectivity supports modern telehealth models and aligns with long-standing digital infrastructure trends in healthcare. The broader wireless health ecosystem is rapidly expanding, with the global wireless health market projected to grow significantly over the next decade as connectivity drives adoption of remote patient monitoring. This seamless data flow and user convenience make wireless the foundational technology in smart home health solutions.

Regional Insights

U.S. Smart Home Health Market Trends

The U.S. leads the North American smart home health market due to its advanced healthcare infrastructure, high technology adoption, and broad chronic disease burden. The U.S. accounts for the largest regional share. High prevalence of chronic conditions, e.g., over 37 million Americans diagnosed with diabetes drives demand for smart home health solutions like connected glucose monitors and wearables. Telehealth and remote patient monitoring uptake is also high: many U.S. hospitals expanded telehealth use during and after the COVID-19 pandemic, thereby increasing smart device integration into care delivery.

Canada Smart Home Health Market Trends

Canada plays a significant role in the North American smart home healthcare market, owing to its publicly funded healthcare system, government-led digital health initiatives, and the growth of virtual care adoption. The Canadian segment is projected to account for approximately 20.2% of the North American remote home monitoring market in 2025, supporting regional expansion. Canada’s growth in digital health is supported by eHealth adoption: approximately 17.7 million Canadians used digital health services in 2021, with projections reaching 21 million by 2026. Additionally, surveys show that 84% of Canadian physicians believe virtual care improves access to care, demonstrating clinician support for telehealth and remote monitoring in rural and underserved regions.

Competitive Landscape

The North America smart home health market features competitive players like Apple, Philips, Medtronic, Dexcom, Fitbit (Google), and Abbott, focusing on IoT integration, AI analytics, and remote monitoring solutions. Intense innovation, partnerships with healthcare systems, and wearable technology advancements drive differentiation and market share expansion.

Key Industry Developments:

- In January 2026, Dr Odin unveiled new app-enabled connected health monitoring devices, expanding its portfolio in digital and home-based healthcare. The company introduced smart monitoring solutions that integrate with a mobile application, allowing users and caregivers to track real-time health parameters, access historical data, and receive alerts remotely.

- In November 2024, GE HealthCare and DeepHealth, Inc., a RadNet subsidiary, announced a strategic collaboration to advance AI in imaging. The partnership aims to develop SmartTechnology™ solutions that enhance image interpretation, streamline care team collaboration, and improve operational efficiency by combining GE HealthCare’s imaging expertise, RadNet’s care delivery experience, and DeepHealth’s AI capabilities.

Companies Covered in North America Smart Home Health Market

- Koninklijke Philips N.V.

- Medtronic

- GE HealthCare

- SAMSUNG

- Apple Inc.

- Google (Alphabet Inc.)

- Microsoft

- Amazon Web Services, Inc.

- Honeywell International Inc.

- Siemens Healthineers AG

- Bosch Healthcare Solutions GmbH

- LG Electronics

- Panasonic Corporation

- Withings

- Resmed

- Others

Frequently Asked Questions

The North America smart home health market is projected to be valued at US$ 15.5 Bn in 2026.

Rising chronic diseases, aging population, telehealth expansion, IoT adoption, AI integration, and supportive reimbursement policies drive growth.

The North America smart home health market is poised to witness a CAGR of 26.0% between 2026 and 2033.

AI-enabled remote monitoring, wearable integration, preventive care expansion, telehealth interoperability, data analytics, and home-based chronic management.

Koninklijke Philips N.V., Medtronic, GE HealthCare, SAMSUNG, Apple Inc., Google (Alphabet Inc.)