- Technology

- Mobile Data Protection Market

Mobile Data Protection Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Mobile Data Protection Market by Solution (Mobile Data Protection (MDP), Data Loss Prevention (DLP), Mobile Device Management (MDM)), Development Type (Cloud, On-Premises), Industry (Manufacturing, Defence & Aerospace, IT & Telecom, BFSI, Healthcare, Others), and Regional Analysis, 2026 - 2033

Mobile Data Protection Market Size and Trend Analysis

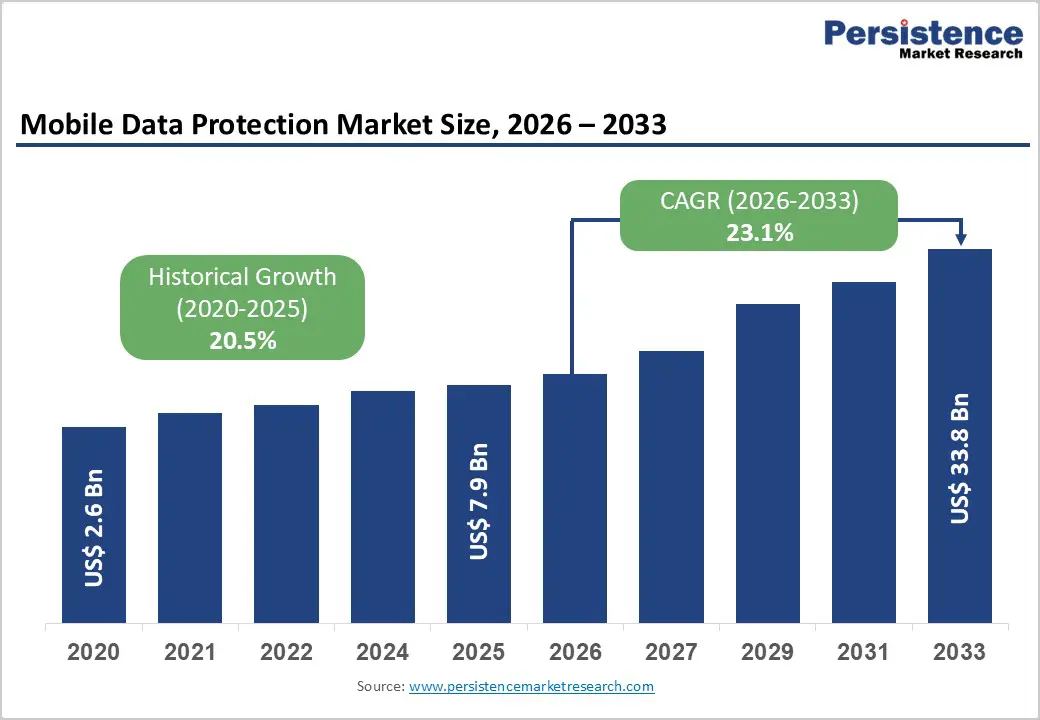

The global mobile data protection market size is expected to be valued at US$ 7.9 billion in 2026 and projected to reach US$ 33.8 billion by 2033, growing at a CAGR of 23.1% between 2026 and 2033.

This exponential growth trajectory reflects the escalating threat landscape targeting mobile devices and the rapid acceleration of Bring Your Own Device (BYOD) adoption across enterprise environments. The market expansion is driven by the convergence of several critical factors including the explosive rise in mobile ransomware attacks with 4,701 confirmed ransomware incidents globally in 2025, representing a 34% increase year-over-year, the implementation of stringent regulatory frameworks such as GDPR and emerging data protection legislation, and the critical need for Zero Trust security architectures that verify every mobile access attempt regardless of origin.

Key Industry Highlights:

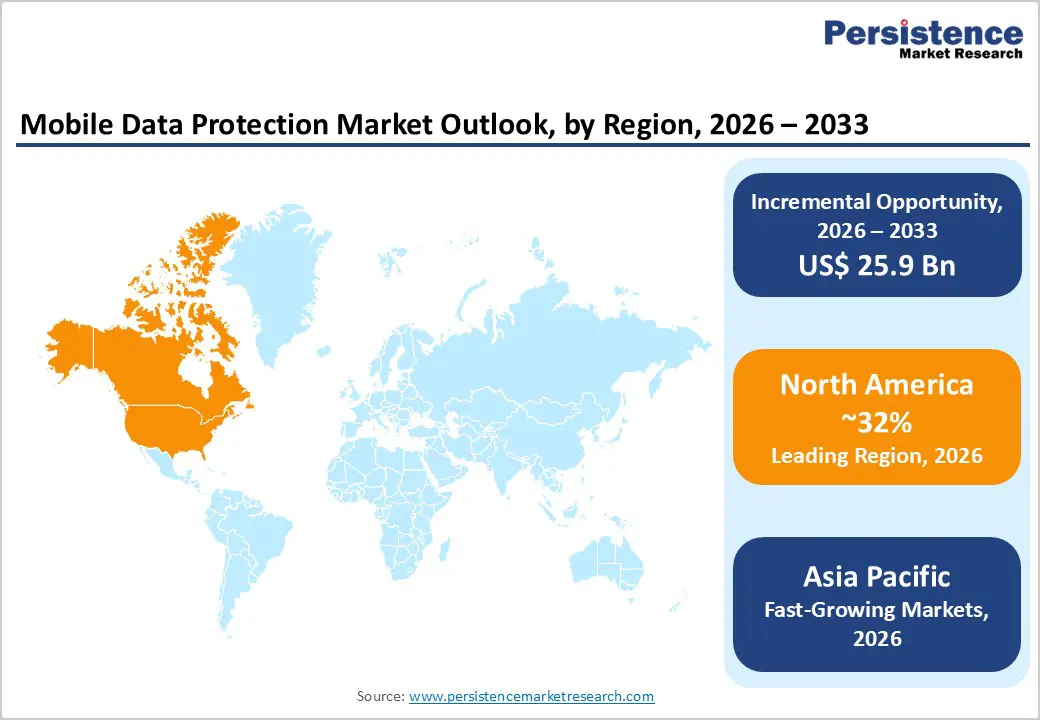

- Leading Region: North America leads with a 32% share in 2025, supported by mature enterprise security ecosystems, strict compliance requirements, and strong investment from major security vendors.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a 26.5% CAGR through 2033, driven by rapid digitalization, rising mobile payments, and accelerating BYOD adoption.

- Dominant Segment: Mobile Device Management (MDM) dominates the market, with about a 42% share in 2025, as enterprises prioritize centralized control of personal and corporate devices.

- Fastest Growing Segment: Cloud-based Mobile Data Protection is the fastest-growing model with a 25.8% CAGR due to demand for centralized policy management, real-time threat intelligence, and reduced infrastructure costs.

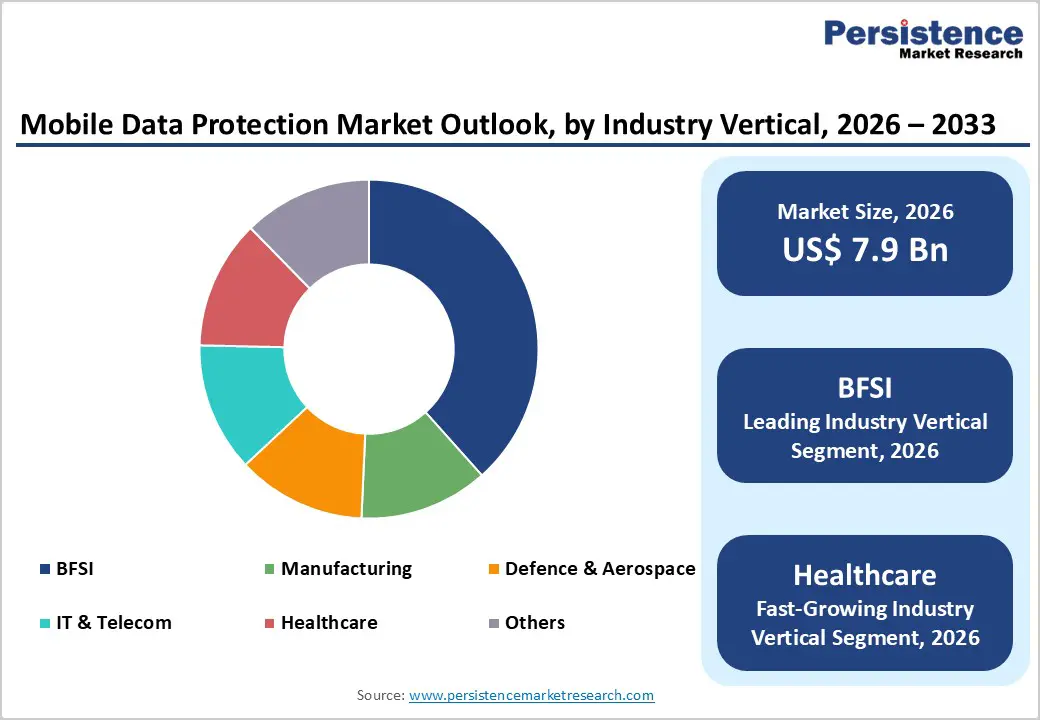

- Key Market Opportunity: Healthcare offers the strongest opportunity as growing regulatory pressure and rising data breaches increase demand for secure, workflow-integrated mobile protection solutions.

| Key Insights | Details |

|---|---|

|

Mobile Data Protection Market Size (2026E) |

US$ 7.9 billion |

|

Market Value Forecast (2033F) |

US$ 33.8 billion |

|

Projected Growth CAGR(2026-2033) |

23.1% |

|

Historical Market Growth (2020-2025) |

20.5% |

Market Dynamics

Drivers – Rising Mobile Ransomware and Advanced Malware Threats

The mobile threat landscape has reached unprecedented severity, with organizations facing increasingly sophisticated attack vectors targeting sensitive enterprise data. From January to September 2025, 4,701 confirmed ransomware incidents occurred globally, representing a 34% year-over-year increase, while mobile cyberattack attempts reached approximately 11,000 daily attacks during the same period. Notably, Android devices account for 47% of all infected mobile devices globally, with 50 times as many malware infections on Android as on iOS, underscoring the critical vulnerability of enterprise-distributed Android smartphones.

The proliferation of ransomware-as-a-service (RaaS) models has democratized attack capabilities, enabling even unsophisticated threat actors to launch devastating campaigns targeting mobile infrastructure. In response, enterprises are accelerating the deployment of Mobile Threat Defense (MTD) solutions capable of real-time threat detection, behavioral analytics, and automated response protocols. The economic impact of ransomware is becoming increasingly severe, with average recovery costs now ranging from US$ 5-6 million per incident and downtime spanning 24-27 days, compelling organizations to view comprehensive mobile data protection as a business-critical investment rather than an optional security infrastructure.

Massive Proliferation of Bring Your Own Device (BYOD) and Mobile Workforce Expansion

Enterprise adoption of BYOD policies has transformed organizational security perimeters, with 65% of devices accessing business data now being personally owned smartphones and tablets. This fundamental shift in the computing paradigm has exposed enterprises to unprecedented data-loss risks, as personally managed devices operate outside traditional corporate security controls and firewalls, creating attack surfaces that legacy security architectures cannot effectively defend.

The post-pandemic acceleration of remote work and distributed workforce models has accelerated BYOD adoption, with organizations recognizing that strict device ownership policies are incompatible with employee preferences and modern flexible work arrangements. The challenge for enterprises lies in simultaneously protecting sensitive corporate data while respecting employee privacy preferences and avoiding excessive monitoring of personal device usage. The emergence of sophisticated Zero Trust architecture frameworks capable of continuously verifying device posture and context-aware access control across personal devices represents a transformative approach that is gaining rapid enterprise adoption.

Restraints - Complexity of Implementation and Integration with Legacy Enterprise Systems

Organizations seeking to deploy comprehensive mobile data protection solutions face formidable implementation challenges, particularly when integrating advanced security architectures with sprawling legacy IT environments built on incompatible infrastructure. Many enterprises continue to operate a hybrid infrastructure that combines on-premises systems, private cloud resources, and public cloud services, creating fragmented security domains that struggle to implement unified mobile data protection policies.

The technical complexity of deploying containerization, mobile threat detection, and endpoint management across heterogeneous device ecosystems (combining iOS, Android, and legacy platforms) requires specialized expertise that many mid-sized organizations lack internally. The financial burden of a comprehensive mobile data protection infrastructure extends beyond initial software licensing to encompass ongoing professional services for customization, integration, ongoing support, and training of internal security teams, creating total cost of ownership concerns that constrain adoption among budget-conscious mid-market enterprises.

Regulatory Ambiguity and Data Sovereignty Concerns in Global Operations

Organizations operating across multiple jurisdictions face increasingly fragmented regulatory requirements governing mobile data protection, creating compliance complexity that confounds standardized security implementation. The European Union’s General Data Protection Regulation (GDPR) imposes stringent requirements for data protection, consent management, and breach notification (within 72 hours of discovery), while emerging regulations in countries like India, with the Personal Data Protection Bill and China, with data localization mandates, create conflicting requirements.

Organizations struggle to implement mobile data protection solutions that simultaneously satisfy GDPR’s transparency and consent requirements, China’s data sovereignty mandates requiring processing of sensitive information within national borders, and the HIPAA compliance requirements for healthcare organizations. The inability to deploy a unified, global mobile data protection infrastructure forces multinational enterprises to implement regionally specific security solutions with increased capital expenditure and operational complexity.

Opportunity - Healthcare Sector Transformation Through Secure Mobile Device Deployment

The healthcare industry presents a high-growth opportunity for mobile data protection solutions, driven by the critical need to safeguard sensitive patient information on mobile devices used by clinicians, care providers, and administrative staff. In the United States alone, 725+ healthcare data breaches were disclosed in 2023, exposing over 133 million patient records. Mobile devices are a primary attack vector, given their portability and connectivity to sensitive patient databases.

Healthcare organizations are increasingly deploying biometric authentication, Zero Trust access frameworks, and secure work-life partitioning through Android Enterprise Work Profiles and Apple’s proprietary container technologies to enable clinicians to access real-time patient data without compromising security. Furthermore, integrating wearable devices and health-monitoring IoT endpoints into clinical workflows requires sophisticated mobile data protection architectures capable of managing diverse device ecosystems while maintaining patient privacy.

Financial Services Sector Acceleration Through Zero Trust Banking and Advanced Threat Detection Features

The Banking, Financial Services, and Insurance (BFSI) sector faces unprecedented mobile app security challenges as financial institutions rapidly transition to mobile-first banking models. The increasing adoption of mobile wallets, payment applications, and digital trading platforms is creating an expanded attack surface for financial fraud and data theft. The sector is experiencing a rapid escalation of sophisticated threats, including session hijacking, API exploitation, malware disguised as overlay screens, and voice-based scams employing OTP call merging, targeting high-value financial transactions.

Financial institutions are urgently deploying Runtime Application Self-Protection (RASP) technologies and on-device threat detection systems to identify jailbroken devices, injected malware, and manipulated code before malicious actors can intercept OTPs or reroute funds. The Reserve Bank of India, the Securities Exchange Board of India (SEBI), and global financial regulators are tightening scrutiny on mobile application security, mandating the implementation of end-to-end mobile app security covering hardening, real-time fraud detection, secure APIs with encryption and rate limiting, and behavioral analytics identifying synthetic identities and bot fraud.

Category-wise Analysis

Solution Insights

Mobile Device Management (MDM) is the leading solution in the Solution Type category, commanding approximately 42% market share in 2025. The dominant position of MDM solutions reflects their fundamental importance in enabling enterprises to assert centralized control and visibility over the sprawling population of personally owned and corporate devices that access sensitive business data.

MDM platforms provide granular capabilities, including device enrollment and authentication, application distribution and management, policy enforcement, remote device wipe, and comprehensive asset inventory management, making them essential infrastructure for organizations implementing BYOD policies. The increasing integration of MDM with Mobile Application Management (MAM), containerization technologies, and threat detection engines is reinforcing MDM’s leadership position as enterprises recognize that effective mobile data protection requires unified device, application, and data management.

Development Type Insights

Cloud-based mobile data protection solutions command the leading position within the Development Type category, capturing approximately 58% market share in 2025 and experiencing accelerating growth as enterprises accelerate digital transformation and adopt public cloud services. Cloud-based mobile data protection offers compelling advantages, including centralized policy management, enabling rapid deployment across globally distributed device fleets; real-time threat intelligence integration from large-scale telemetry networks; automatic updates and patch distribution without requiring IT administrator intervention; and scalability that matches organizational growth without infrastructure capital expenditure.

Organizations increasingly recognize that cloud-based architectures enable AI and machine learning algorithms to process massive volumes of attack data and identify sophisticated threat patterns that are impossible to detect within on-premises infrastructure. The Uptime Institute’s 2023 Outage Analysis Report demonstrated that public cloud providers deliver up to 80% reduction in recovery time objectives (RTOs) compared to traditional on-premises disaster recovery approaches, compelling risk-conscious enterprises to migrate critical security infrastructure to cloud environments.

Industry Vertical Analysis

Banking, Financial Services, and Insurance (BFSI) emerges as the leading industry vertical, commanding approximately 38% market share in 2025, reflecting the sector’s outsized vulnerability to mobile data theft and transaction fraud, as well as regulatory mandates for security implementation. The BFSI sector prioritizes mobile data protection solutions for existential risk management, given that phishing, DDoS, ransomware, crypto-mining botnets, and malware targeting financial applications pose direct revenue and reputation threats.

Financial institutions globally are deploying sophisticated mobile app security solutions, including RASP for runtime protection, secure API architectures with encryption and rate limiting, behavioral analytics for fraud detection, and end-to-end encryption protecting customer transactions and authentication credentials. Furthermore, the emerging threat of AI-powered deepfakes targeting call centers and customer authentication workflows is compelling financial institutions to implement behavioral biometrics and voice authentication alongside traditional password-based security, driving continued expansion of mobile data protection solution adoption within the BFSI vertical.

Regional Insights

North America Mobile Data Protection Market Trends and Insights

North America maintains the strongest regional market position, commanding approximately 32% of global market share in 2025, driven by the region’s sophisticated enterprise security culture, high digital transformation maturity, and stringent regulatory requirements. The United States cybersecurity market is experiencing robust growth, with North America accounting for approximately 34% of global cybersecurity spending and demonstrating strong allocation of security budgets to mobile data protection solutions. U.S. federal government agencies are pursuing ambitious cybersecurity modernization initiatives, with the U.S. Government Accountability Office and CISA (Cybersecurity and Infrastructure Security Agency) mandating implementation of Zero Trust architectures, endpoint detection and response (EDR), and advanced threat protection across federal departments and agencies.

The North American enterprise sector is rapidly adopting cloud-based mobile data protection platforms, recognizing that distributed workforces and BYOD policies necessitate sophisticated device management and threat detection capabilities. Major financial institutions are accelerating the deployment of mobile threat defense and fraud detection solutions, particularly following high-profile breaches, including the Change Healthcare attack that exposed 100 million patient records and triggered a US$ 22 million ransom payment. Healthcare organizations across North America are implementing comprehensive mobile security frameworks, including biometric authentication, containerization, and remote wipe capabilities, to protect sensitive patient data accessed by clinicians via smartphones and tablets.

Europe Mobile Data Protection Market Trends and Insights

Europe represents the second-largest regional market, capturing approximately 28% of global market share in 2025, with market dynamics significantly shaped by stringent GDPR compliance requirements and emerging regulatory harmonization across European Union member states. The General Data Protection Regulation has established Europe as the globally most advanced data protection regime, with organizations operating in European markets required to implement privacy-by-design and privacy-by-default principles mandating that mobile data protection and security controls are embedded throughout the application development lifecycle. Regulatory enforcement has intensified substantially since GDPR implementation in 2018, with data protection authorities imposing significant fines for non-compliance, including Google’s €50 million fine imposed by France’s CNIL for failure to meet transparency requirements and obtain a legal basis for data processing.

Germany, the United Kingdom, and France lead European mobile data protection adoption, driven by sophisticated financial sectors requiring comprehensive transaction security, major manufacturing operations that necessitate protection of industrial IoT devices and supply chain data, and advanced healthcare systems that protect patient data. The European market is witnessing strong growth in containerization and mobile app management solutions, as financial services and healthcare organizations seek to separate corporate and personal data on employee devices while maintaining full security visibility. Regulatory harmonization through the ePrivacy Directive review and upcoming ePrivacy Regulation is expected to create consistent security and privacy requirements across European Union member states, likely accelerating standardization of mobile data protection implementations and reducing regional fragmentation.

Asia Pacific Mobile Data Protection Market Trends and Insights

Asia Pacific emerges as the fastest-growing region, projected to grow at 26.5% CAGR during 2026-2033, driven by explosive digital transformation in China, India, and Japan, rapid expansion of mobile payment infrastructure, and escalating government mandates for cybersecurity readiness. The Indian market is experiencing exceptional growth momentum, with UPI transactions reaching 129.3 billion transactions annually and government initiatives, including the Digital India campaign and Personal Data Protection Bill, creating regulatory drivers for comprehensive mobile data protection implementations. Indian enterprises are urgently deploying mobile device management and threat detection solutions to secure the rapidly expanding base of employees accessing corporate data on personal smartphones, as BYOD adoption accelerates alongside India’s high smartphone penetration, reaching 70% among working professionals.

China maintains the region’s largest mobile security market, driven by government mandates for data sovereignty and localization, sophisticated mobile payment and fintech ecosystems, and stringent requirements for indigenous technology adoption in sensitive sectors. Japan is advancing mobile threat defense adoption across the healthcare and financial services sectors, with a particular emphasis on biometric authentication and Zero Trust access controls, reflecting the region’s advanced security maturity. The Asia Pacific region’s emergence as a high-growth market is reinforced by the concentration of mobile device manufacturing in the area, with companies such as PAX Technology, Newland Payment Technology, and emerging Chinese vendors developing sophisticated Android smart terminals and mobile security solutions tailored to regional threat landscapes and regulatory requirements.

Competitive Landscape

The global mobile data protection market is characterized by a moderately consolidated structure, with a handful of large security platform providers holding significant influence. At the same time, numerous specialized vendors compete in niche verticals and regional segments. Leading players strengthen their position through extensive ecosystems that integrate device management, threat detection, analytics, and managed services, creating high switching costs and reinforcing customer lock-in.

The competitive landscape is further shaped by ongoing consolidation, as major technology firms expand capabilities through acquisitions and platform integration strategies. Specialized providers continue to differentiate through vertical-focused offerings and advanced threat defense capabilities. Market competition is increasingly defined by technological innovation, with zero-trust architectures, AI-driven behavioral analytics, and automated response systems becoming essential components of vendor strategies. As mobile threats evolve and enterprise environments adopt more BYOD and cloud-centric models, competitors are prioritizing R&D investment to deliver unified, adaptive security platforms that outperform legacy, rule-based protection approaches.

Key Market Developments

- April 2024: Cisco Launches HyperShield AI-Powered Security Platform - Cisco Systems Inc. unveiled HyperShield, an advanced security platform leveraging artificial intelligence to provide autonomous segmentation, threat detection, and automated response capabilities protecting applications, devices, and data across data centers and edge environments.

- April 2023: Germany-based Utimaco acquires IT security solutions provider conpal to enhance confidential data protection through advanced encryption technologies, strengthening secure computing capabilities.

Companies Covered in Mobile Data Protection Market

- Broadcom Inc.

- Sophos Ltd

- Microsoft Corporation

- McAfee LLC

- Kaspersky Lab

- Intel Corporation

- Hewlett Packard Enterprise

- Thales Group

- Dell Inc.

- Cisco Systems Inc.

- Broadcom Inc.

- IBM Corporation

- Trend Micro Incorporated

- Check Point Software Technologies Ltd

Frequently Asked Questions

The market is expected to reach US$ 7.9 billion by 2026.

Rising mobile cyberattacks, growing BYOD usage, stricter data protection laws, remote-work expansion, and advanced threat detection needs drive market adoption.

North America leads the market, while Asia Pacific is the fastest-growing region.

Healthcare and BFSI offer strong opportunities due to increasing regulatory requirements, breach risks, and rapid digital workflow expansion.

The leading market players include Microsoft Corporation, Broadcom Inc., Hewlett Packard Enterprise, IBM Corporation, Cisco Systems Inc., Trend Micro Incorporated, and Check Point Software Technologies.