- Hardware & Software IT Services

- Mobile Device Management Market

Mobile Device Management Market Size, Share, and Growth Forecast 2026 – 2033

Mobile Device Management Market by Component (Solution, Software), Deployment Model (Cloud, On-Premise), Enterprise Size (Large Enterprises, Small & Medium Enterprises), Industry Vertical (IT & Telecom, Healthcare, BFSI, Retail, Manufacturing, Government, Others), Regional Analysis, 2026–2033

Mobile Device Management Market Size and Trend Analysis

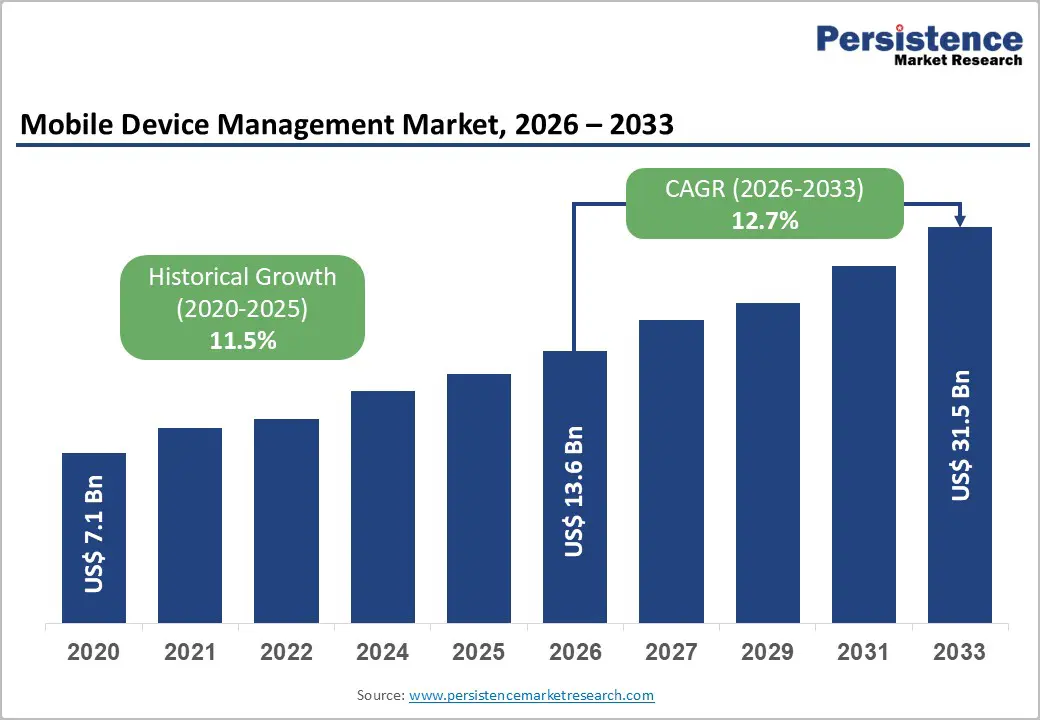

The global Mobile Device Management Market size is anticipated to reach US$ 13.6 Billion in 2026 and is projected to reach US$ 31.5 Billion by 2033, growing at a CAGR of 12.7% between 2026 and 2033. Organizations globally are prioritizing cloud-based mobile device management solutions to secure distributed workforces, with 80% of enterprises now embracing bring-your-own-device (BYOD) policies generating 55% productivity gains. Rising cybersecurity mandates, compliance requirements including GDPR, HIPAA, and PCI-DSS, combined with expansion of 5G technology and IoT device proliferation, create substantial demand acceleration across enterprise segments worldwide.

Key Highlights Summary

- Solution/Software dominates at 72% market share, while Services segment accelerates at 15.6% CAGR, reflecting growing organizational preference for vendor-managed operational support.

- Healthcare vertical emerging as fastest-growing segment at 15.1% CAGR, driven by telemedicine, EHR cloud migration, and HIPAA compliance mandates.

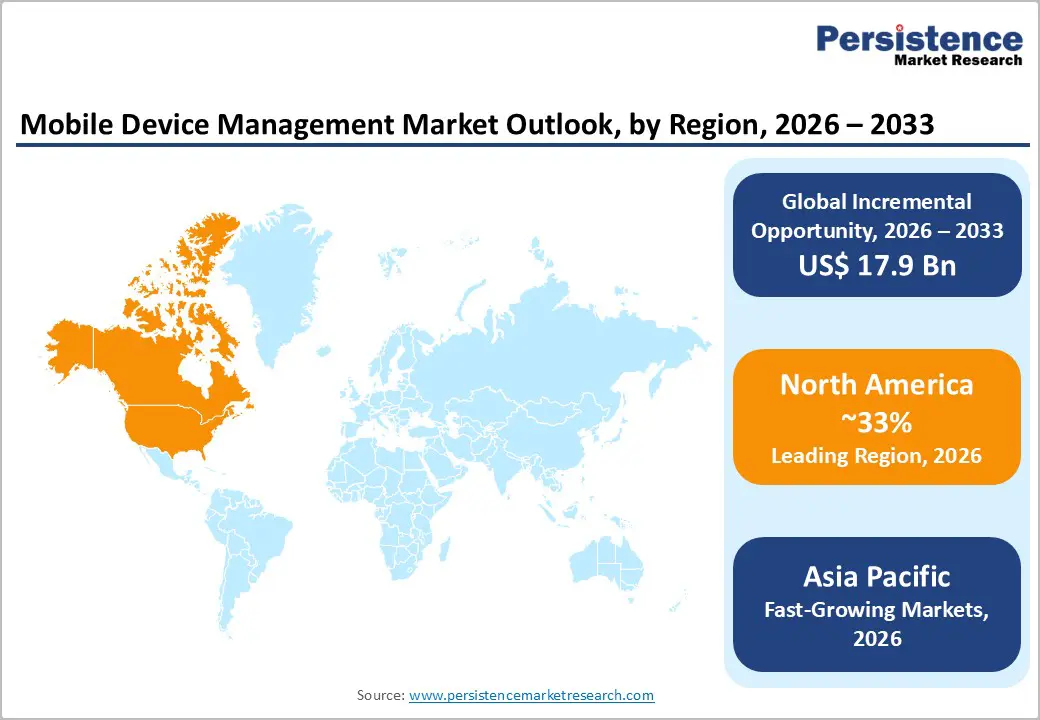

- North America maintains leadership with 33% global market share, while Asia Pacific emerges as fastest-growing region at 14.4% CAGR, driven by China, India, and ASEAN digital transformation.

- Europe holds 27% market share with steady 11.4% CAGR growth, reinforced by GDPR compliance requirements and data sovereignty mandates.

- BYOD adoption reaching 80% of organizations globally, with 55% productivity gains driving SME and mid-market adoption acceleration.

- 5G infrastructure expansion and IoT device proliferation enabling real-time MDM capabilities supporting field-intensive industries and distributed operations.

| Key Insights | Details |

|---|---|

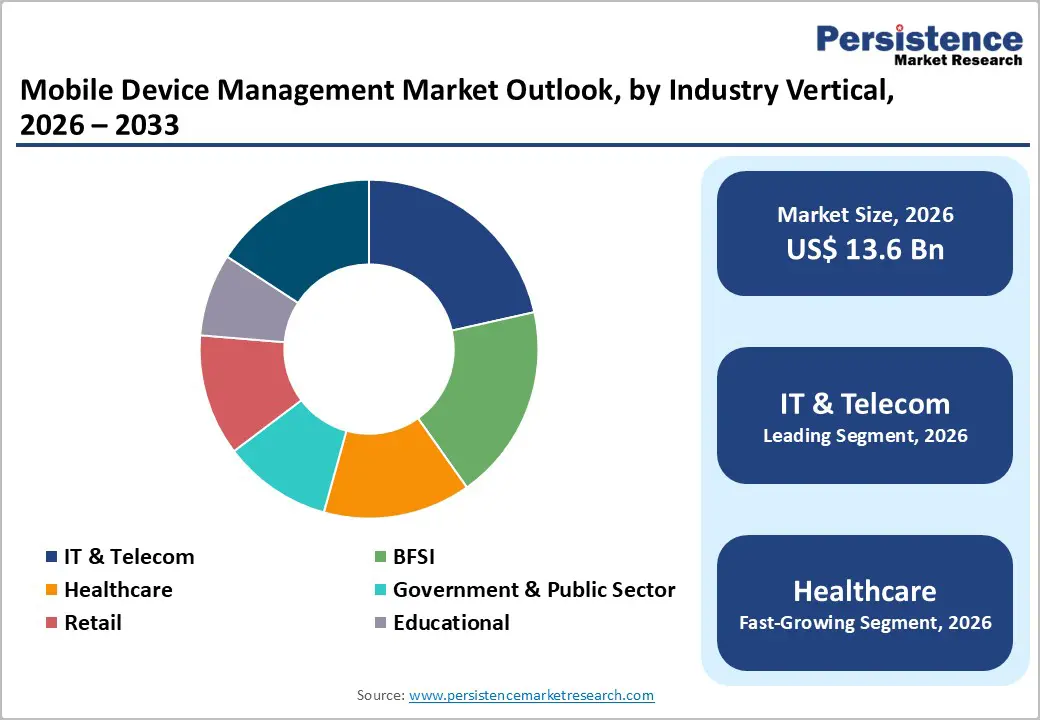

| Mobile Device Management Market Size (2026E) | US$ 13.6 billion |

| Market Value Forecast (2033F) | US$ 31.5 billion |

| Projected Growth CAGR (2026-2033) | 12.7% |

| Historical Market Growth (2020-2025) | 11.5% |

Market Dynamics Analysis

Market Growth Drivers

Accelerating Adoption of Cloud-Based Mobile Device Management and BYOD Policy Expansion

Organizations are rapidly transitioning from legacy on-premise MDM systems to cloud-based platforms, driven by cost efficiency, scalability, and remote workforce support capabilities. Cloud deployment captured 64% market share in 2026, with enterprises realizing 30%+ infrastructure cost savings versus traditional architecture. The widespread adoption of BYOD policies affecting 80% of organizations as of 2025 creates structured demand for centralized device management solutions that secure personal devices accessing corporate data. Companies save approximately USD 1,300 per employee annually through BYOD implementation while maintaining security compliance. Samsung exemplifies vendor innovation by introducing simplified cloud-based MDM solutions specifically designed for small business adoption, reducing implementation complexity and licensing barriers. The convergence of cost pressures, workforce flexibility expectations, and cloud infrastructure maturation drives aggressive migration toward cloud-based MDM platforms across enterprise segments.

Stringent Regulatory Compliance Requirements and Cybersecurity Mandates Driving Adoption

Regulatory frameworks including GDPR, HIPAA, PCI-DSS, and emerging zero-trust security mandates are creating mandatory demand for centralized, auditable device management infrastructure. Organizations managing sensitive data recognize that 60% of corporate data now resides in cloud environments on BYOD devices, necessitating sophisticated governance and encryption capabilities. Cyber-insurance providers are increasingly mandating MDM adoption as a prerequisite for coverage eligibility, extending adoption beyond traditionally security-focused sectors into mid-market organizations. Enterprises are allocating 25% of IT budgets toward mobile security solutions by 2028, reflecting heightened board-level focus on endpoint protection and compliance verification. This regulatory-driven demand trajectory ensures sustained investment in MDM solutions across BFSI, healthcare, government, and regulated manufacturing sectors through the forecast period.

Market Restraints

Security Risks Associated with Personal Device Management and Data Breach Concerns

Personal devices accessing corporate networks introduce elevated security risks compared to managed enterprise hardware, causing organizational caution around BYOD expansion. Malware, unauthorized access, and device compromise remain persistent threats despite advanced MDM technologies. Full-device management can create user friction and privacy concerns, especially when control extends into personal contexts, limiting adoption among privacy-conscious employees. These security and privacy tensions constrain MDM uptake in sensitive geographies and organizations where employee concerns outweigh perceived productivity gains, challenging broader implementation despite enterprise benefits.

Integration Complexity with Legacy Systems and Organizational Change Management Challenges

Transitioning from established on-premise MDM infrastructure to cloud-based alternatives presents substantial technical integration, data migration, and organizational change management requirements. Legacy system dependencies, custom integrations, and enterprise-specific workflow automations complicate migration decisions, extending evaluation and implementation timelines while increasing project risk. Organizations face skill gaps in cloud infrastructure management, identity and access governance, and advanced MDM configuration, requiring costly professional services and consulting engagement. These implementation barriers particularly impact mid-market organizations with constrained IT budgets and limited cloud-native expertise, slowing adoption velocity in growth-focused customer segments.

Market Opportunities

Small and Medium Enterprise Market Expansion Driven by Affordable SaaS Solutions and Government Support

Small and mid-market enterprises represent the fastest-growing customer segment at 16.6% CAGR, driven by increasingly affordable cloud-based SaaS MDM offerings, simplified implementation methodologies, and government digitalization support programs. SMEs traditionally lacked resources for sophisticated device management infrastructure, but modern cloud-based solutions eliminate expensive on-premise infrastructure requirements while providing enterprise-grade security capabilities. Regulatory support programs targeting small business digital transformation, combined with competitive pricing pressure from MDM vendors seeking market expansion, are driving accelerating SME adoption. This segment represents a substantial addressable market opportunity as mid-market organizations recognize MDM value propositions supporting hybrid workforce management and compliance obligations.

Convergence of Artificial Intelligence and Zero-Trust Security Models Enhancing Threat Detection and Remediation

Advanced analytics and machine learning capabilities are increasingly integrated into MDM platforms, enabling automated anomaly detection, predictive threat identification, and intelligent policy enforcement. Cybersecurity professionals report around 70-75% adoption of AI for routine security tasks, ~68-71% usage for traffic monitoring and malware detection, and ~60-64% deployment for phishing and malware attack identification. Zero-trust security architecture adoption is accelerating across regulated industries and government organizations, requiring granular device posture assessment and continuous authentication validation capabilities that modern MDM platforms uniquely enable. This convergence of AI-driven security enhancement and zero-trust mandates creates substantial incremental opportunities for vendors offering next-generation threat detection and intelligent policy orchestration capabilities.

Segmentation Analysis

Component Analysis

Solution platforms represent the foundational MDM value proposition, accounting for 72% market share and supporting device enrollment, policy configuration, compliance management, and security enforcement across heterogeneous enterprise device ecosystems. Organizations prioritize comprehensive software platforms delivering capabilities including device provisioning, application management, content distribution, analytics, and remote security controls essential for scalable, centralized governance. Leading vendors including Microsoft Intune, VMware Workspace ONE, IBM MaaS360, and Citrix Endpoint Management compete on platform breadth, cloud architecture maturity, integration depth, and continuous security innovation.

Professional and managed services form the fastest-growing component, expanding at 15.6% CAGR, driven by deployment complexity, skills shortages, and preference for vendor-operated models. Enterprises increasingly outsource endpoint operations to optimize configurations, maintain compliance, reduce internal IT burden, and strengthen security.

Deployment Model Analysis

Cloud deployment commands 64% market share, with organizations recognizing superior scalability, accessibility from distributed locations, automatic security updates, and cost efficiency versus on-premise infrastructure. Cloud-based MDM eliminates capital expenditure for server infrastructure, provides disaster recovery resilience, and supports rapid deployment across geographically dispersed organizations. SaaS MDM platforms deliver subscription-based pricing aligned with usage volumes, enabling cost predictability and operational flexibility essential for growing enterprises managing dynamic device populations.

On-premise deployment retains 36% market share, particularly prevalent in BFSI, healthcare, and government sectors requiring maximum control over sensitive infrastructure and strict data residency compliance. Organizations in these verticals maintain on-premise systems despite cloud advantages, prioritizing physical infrastructure control and localized data management supporting regulatory attestation and compliance certification requirements.

Enterprise Size Analysis

Large Enterprises contribute 69% of MDM market revenue, driven by substantial device populations, complex regulatory compliance, and capital availability for extensive platform investments. These organizations demand sophisticated management capabilities, multi-geography deployment support, advanced integration, analytics, and security controls that enterprise-grade MDM platforms uniquely provide. Leading vendors design solutions to address scalability, operational efficiency, and centralized governance, enabling large enterprises to manage heterogeneous device ecosystems while ensuring regulatory adherence and organizational security standards.

Small and Medium Enterprises (SMEs) are the fastest-growing segment, expanding at 16.6% CAGR, as cloud-based SaaS MDM solutions reduce infrastructure requirements, simplify deployment, and offer affordable access. Government digitalization initiatives and industry programs further support SME adoption, accelerating segment growth and enabling widespread digital transformation.

Industry Vertical Analysis

IT & Telecom represents the dominant vertical with 21% market share, as organizations in this sector manage large mobile device populations, leverage technology effectively, and operate sophisticated infrastructure supporting advanced MDM capabilities. Telecom operators utilize MDM for employee device management, customer device support, secure application deployment, and network security operations. Vendors focus on delivering scalable solutions with integration, analytics, and policy enforcement features tailored to complex enterprise environments, enabling IT & Telecom companies to maintain operational efficiency, regulatory compliance, and data security across diverse device ecosystems.

Healthcare is the fastest-growing vertical, expanding at 15.1% CAGR, driven by telemedicine adoption, EHR cloud migration, HIPAA compliance, and medical IoT device management. Investments in secure mobile infrastructure enable remote provider access, patient data protection, and uninterrupted clinical workflows, accelerating MDM adoption in the sector.

Regional Market Insights

North America

North America commands 33% global market share, supported by mature cloud infrastructure, widespread BYOD adoption, advanced remote work culture, and established regulatory frameworks. The United States leads regional adoption, with enterprises across BFSI, healthcare, government, and technology sectors investing heavily in comprehensive MDM platforms. Microsoft Intune, VMware Workspace ONE, and IBM MaaS360 maintain substantial North American customer bases reflecting vendor localization, support infrastructure, and integration ecosystem maturity.

The region's mature digitalization levels, high enterprise technology spending, and sophisticated security cultures position North America as a stable, innovation-driven market where next-generation capabilities in AI-driven threat detection and zero-trust architecture are rapidly adopted. Regulatory mandates including GDPR compliance for U.S. companies serving European customers, HIPAA in healthcare, and PCI-DSS in financial services drive continuous MDM investment to maintain compliance posture.

Europe

Europe holds 27% global market share with 11.4% CAGR growth, characterized by stringent data protection regulation, emphasis on data sovereignty, and strong GDPR compliance focus. Germany, the United Kingdom, France, and Spain lead regional adoption, where organizations across regulated industries prioritize MDM infrastructure supporting regulatory compliance and data governance requirements. European enterprises increasingly migrate from on-premise infrastructure toward cloud-based solutions while maintaining stringent data residency and sovereignty controls aligned with GDPR and emerging Digital Services Act compliance obligations.

The region's strong regulatory environment, combined with mature IT infrastructure and vendor competition, supports steady market growth through 2033. Regulatory harmonization efforts across the European Union and government support for digital transformation initiatives further strengthen the regional MDM opportunity.

Asia Pacific

Asia Pacific represents the fastest-growing region at 14.4% CAGR, driven by rapid digitalization across China, India, and ASEAN economies, burgeoning e-commerce and fintech sectors, and government digital transformation initiatives. China leads adoption with the largest mobile user base globally, accelerating enterprise adoption of cloud-based MDM solutions supporting sophisticated digital business ecosystems. India's rapidly expanding IT services sector, fintech innovation, and BFSI modernization create substantial MDM demand, while Japan demonstrates advanced MDM maturity across enterprise sectors.

Manufacturing sector growth across the region, coupled with 5G infrastructure expansion and IoT device proliferation, creates incremental MDM opportunities across industrial verticals. Government digitalization programs, regulatory modernization, and cost-competitive cloud infrastructure positioning strengthen Asia Pacific as the highest-growth region through 2033.

Competitive Landscape

Strategic Developments

- November 2024: IBM MaaS360 platform released Windows Release Notes updates implementing advanced encryption, compliance automation, and zero-trust security controls targeting enterprise security requirements.

- December 2024: VMware Workspace ONE (Omnissa) announced expanded ecosystem partnerships with security vendors, identity platforms, and service delivery partners, enhancing integrated platform capabilities.

- July 2024: Azercell Business launched enterprise-focused MDM solution offering centralized device control, enhanced cybersecurity, and regulatory compliance capabilities targeting Azerbaijani and regional enterprises.

Business Strategies

Leading vendors emphasize cloud-native architecture, artificial intelligence integration for threat detection, and zero-trust security model support. Microsoft Intune differentiates through Microsoft 365 ecosystem integration and governance capabilities. VMware Workspace ONE emphasizes unified endpoint management combining devices, applications, and identity governance. IBM MaaS360 focuses on enterprise security, compliance automation, and hybrid workforce management. Citrix highlights secure application delivery and workspace continuity. Emerging competition targets SME and mid-market segments with simplified, affordable SaaS platforms reducing implementation complexity.

Frequently Asked Questions

The global MDM market is valued at US$ 13.6 Billion in 2026 and is projected to reach US$ 31.6 Billion by 2033, representing substantial growth opportunities across enterprise segments and geographies.

BYOD policy expansion affecting 80% of organizations, regulatory compliance mandates including GDPR and HIPAA, cloud infrastructure adoption delivering 30%+ cost savings, and 5G/IoT technology expansion create converging drivers accelerating MDM adoption globally.

The MDM market is expanding at 12.7% CAGR through 2033.

Healthcare digital transformation, SME market expansion, AI-driven security integration, zero-trust architecture adoption, and field workforce mobility management represent primary growth opportunity vectors.

Microsoft Intune, VMware Workspace ONE, IBM MaaS360, Citrix Endpoint Management, BlackBerry UEM, Apple Business Essentials, Samsung Knox, ManageEngine, Google Workspace, and emerging vendors including Tanium, NinjaOne, and CrowdStrike lead competitive positioning.