- Automotive Components & Materials

- Automobile Coolant Market

Automobile Coolant Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Automobile Coolant Market by Product Type (Propylene Glycol, Ethylene Glycol, Glycerine), Technology Type (Inorganic Additive Technology (IAT), Organic Acid Technology (OAT), Hybrid Organic Acid Technology (HOAT)), Application Type (Passenger Cars, Commercial Vehicles, Two Wheelers, other), and Regional Analysis for 2025 - 2032

Automobile Coolant Market Size and Trends Analysis

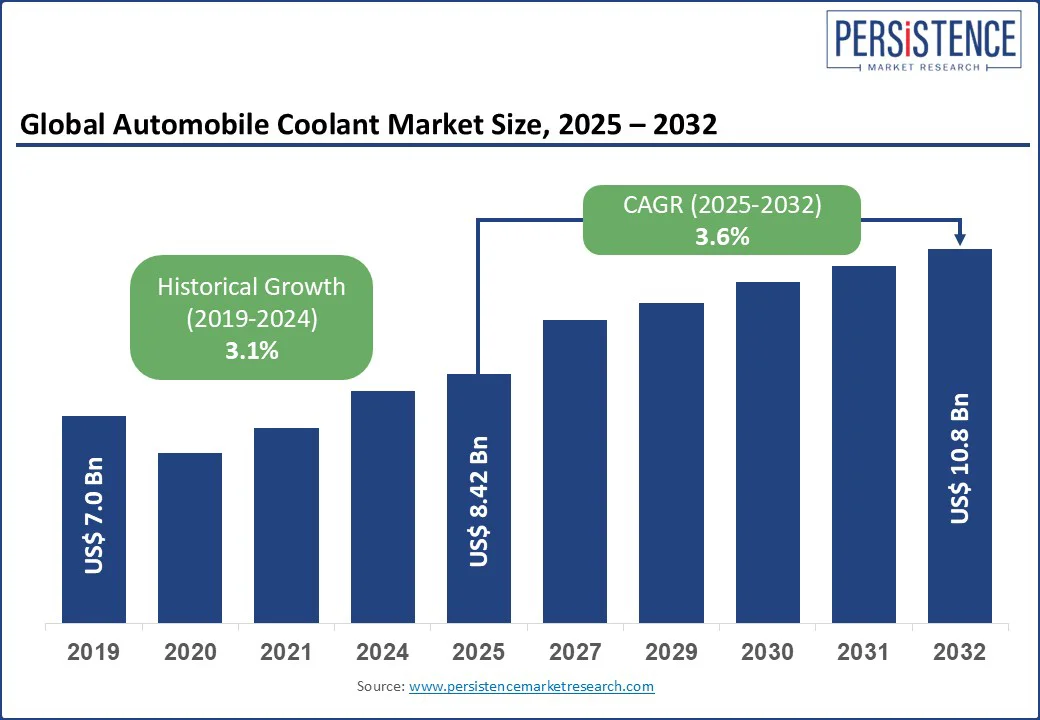

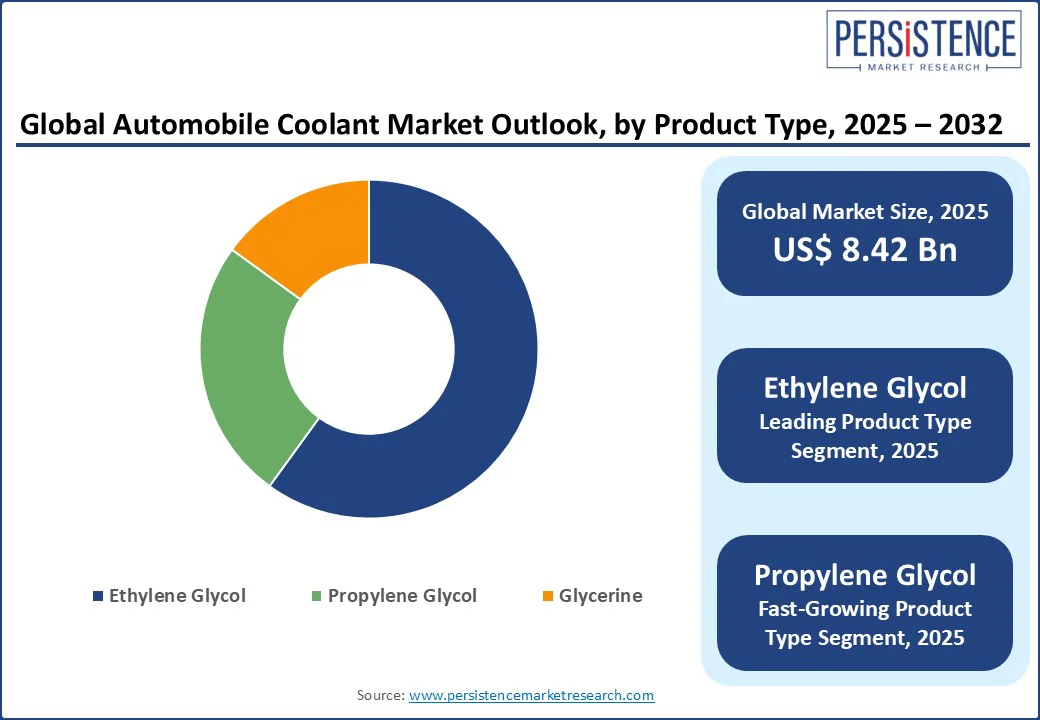

The global automobile coolant market size is likely to be valued at US$8.42 Bn in 2025 and is projected to reach US$10.8 Bn by 2032, achieving a CAGR of 3.6% during the forecast period from 2025 to 2032.

Automotive coolants, formulated with propylene glycol (PG), ethylene glycol (EG), and glycerine, are critical for regulating engine temperatures, preventing corrosion, and ensuring optimal performance in vehicle cooling systems.

Key Industry Highlights

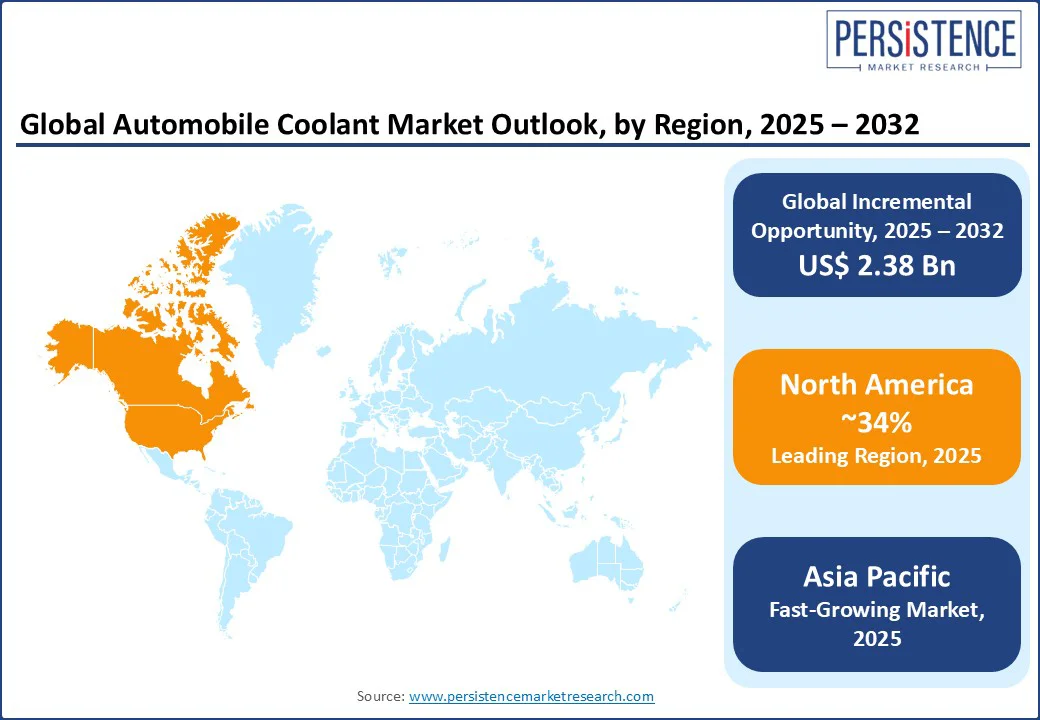

- Leading Region: North America dominates the automobile coolant market due to electric vehicle (EV) adoption, sustainability regulations, and the shift toward eco-friendly coolants such as PG and glycerine-based formulations.

- Fastest-Growing Region: Asia Pacific witnesses significant growth and the fastest growing CAGR, driven by robust vehicle production in China and India

- Major Developments: EU Green Deal and net-zero targets are accelerating demand for sustainable coolants, supported by recycling initiatives and AI integration for thermal system optimization.

- Dominant Coolant Type: Ethylene glycol captures around 60% market share due to its superior thermal performance, cost-effectiveness, and widespread compatibility with internal combustion engines

- Leading End-User: Commercial vehicles remain the largest end-use segment, driven by their larger engines, higher thermal loads, and longer operational cycles, which demand frequent coolant replacement.

|

Global Market Attribute |

Key Insights |

|

Automobile Coolant Market Size (2025E) |

US$ 8.42 Bn |

|

Market Value Forecast (2032F) |

US$ 10.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.1% |

Market Dynamics

Driver- Electric Vehicle (EV) Market Expansion

The rapid expansion of the global EV market, valued at approximately US$400 Bn in 2024, is significantly driving demand for advanced coolants. Electric vehicles require specialized, non-conductive liquid cooling systems—accounting for about 60% of EV thermal management solutions—to ensure safe and efficient battery and motor operation. This need has prompted major players such as ExxonMobil to develop tailored coolant formulations for EVs.

According to the International Energy Agency’s Global EV Outlook 2024, EVs are expected to comprise around 40% of global vehicle sales by 2030. This surge, backed by government incentives and emissions regulations, particularly in North America and the Asia Pacific, is accelerating innovation in EV-compatible thermal management fluids.

Restraint - Environmental Concerns with Ethylene Glycol

Ethylene glycol (EG)-based coolants, while effective for thermal management, are increasingly restrained by environmental and health concerns. Globally, around two Mn tons of used coolant are generated annually, with improper disposal contributing to soil and water contamination. EG is highly toxic and poses serious risks to ecosystems if leaked or mishandled.

As a result, many regions are enforcing stricter environmental regulations and promoting sustainable practices in coolant usage. This has led to growing consumer resistance and industry-wide movement away from EG-based formulations. The trend is fueling demand for safer, eco-friendly alternatives such as propylene glycol (PG) and glycerine-based coolants, which offer lower toxicity and greater biodegradability.

Opportunity - Eco-Friendly Coolant Adoption

The transition to glycerine-based and propylene glycol (PG)-based coolants offers substantial growth opportunities, as bio-based coolants are projected to account for 15% of the global market by 2032.

These environmentally friendly formulations align with global sustainability targets and increasing consumer preference for green automotive solutions. Regions with stringent environmental regulations, such as the EU and North America, are driving this shift. Companies investing in biodegradable and low-toxicity coolants can gain a competitive edge by appealing to eco-conscious buyers and securing long-term partnerships with automakers aiming for net-zero emissions by 2050. This trend supports both regulatory compliance and innovation in sustainable thermal management.

Category-wise Insights

Product Type Insights

Ethylene glycol dominates the global automotive coolant market, accounting for over 60% of the total share, owing to its superior thermal performance, cost-effectiveness, and widespread compatibility with internal combustion engines. Its ability to provide efficient heat transfer and freeze protection makes it the preferred base fluid across passenger and commercial vehicles. Ethylene glycol coolant continues to lead in both OEM and aftermarket segments, especially in Asia Pacific and North America.

Propylene glycol emerges as the leading eco-friendly alternative. It is increasingly adopted for its non-toxic, biodegradable properties, making it ideal for applications where environmental safety is critical. Propylene glycol coolant is gaining momentum in electric vehicles and industrial fleets, supporting the shift toward sustainable automotive fluids.

Technology Type Insights

In 2025, Inorganic Additive Technology (IAT) is projected to hold approximately 62% of the global automotive coolant market. This dominance is attributed to its cost-effectiveness, broad compatibility with conventional internal combustion engines, and strong presence in high-volume vehicle platforms across regions. Inorganic coolants maintain their lead by offering proven performance and reliable corrosion protection, especially in longstanding aftermarket and OEM segments.

Organic Acid Technology (OAT) is identified by industry analysts as the leading growth driver in the coolant sector, expected to grow at a CAGR of 14% from 2024 to 2029. OAT formulations, prized for extended service life, enhanced material compatibility (especially with aluminum components), and reduced environmental impact, are increasingly adopted in modern vehicle architectures, such as electric and hybrid propulsion systems.

Application Type Insights

Commercial vehicles dominate the global automotive coolant market, holding an estimated 73% share. This dominance stems from their larger engines, higher thermal loads, and longer operational cycles, which demand frequent coolant replacement and greater fluid volumes. The surge in e-commerce and logistics operations is accelerating fleet deployment, while the rise of electric commercial vehicles fuels demand for advanced battery cooling solutions.

The passenger car segment remains a vital driver of market expansion, supported by rising vehicle ownership, engine technology advancements, and a growing EV fleet. Increasing urbanization, disposable incomes, and a global focus on preventive vehicle maintenance bolster coolant usage across compact and luxury cars alike.

Regional Insights

North America Automobile Coolant Market Trends

North America emerges as the leading region in the global automotive coolant market, capturing approximately 34% of global revenue in 2025. This dominance is fueled by a mature vehicle fleet, high aftermarket demand, and the accelerating shift toward eco-friendly and electric vehicle coolants.

Automotive manufacturers across the region are increasingly adopting propylene glycol and glycerine-based coolants to meet sustainability goals and comply with stringent environmental regulations. Key industry players are investing in EV-specific thermal management solutions, particularly for battery systems. A

dditionally, the region’s diverse climate conditions, especially in colder zones, drive strong demand for advanced OAT and HOAT formulations in both passenger and commercial vehicles, further supporting the long-term growth of North America’s automotive coolant market.

Europe Automobile Coolant Market Trends

In Europe, Germany holds a significant regional share in the coolant market, driven by its robust automotive industry and EU REACH regulations, with companies such as BASF leading in OAT-based coolants for luxury vehicles and EVs, prioritizing sustainability and high-performance solutions.

The United Kingdom sees growth fueled by demand for eco-friendly, glycerine-based coolant formulations in passenger cars, spurred by increasing environmental awareness. France focuses on coolants for EVs and hybrids, with Renault and PSA Group adopting HOAT solutions to support advanced powertrains. The EU’s Green Deal and net-zero emission targets, combined with advancements in EV technology and recycling initiatives for used coolants, are expected to drive steady market growth through 2032.

Asia Pacific Automobile Coolant Market Trends

Asia Pacific is expanding with the fastest CAGR in the global automotive coolant market, and is projected to be the fastest-growing region through 2032. Rapid industrialization, a booming automotive production base, and rising electric vehicle adoption continue to drive demand for high-performance and eco-friendly coolants.

The region benefits from strong government support for green mobility and increasing consumer demand across two-wheelers, passenger cars, and commercial vehicles. Major manufacturers in Asia are prioritizing cost-effective propylene glycol-based coolants, while others invest in advanced HOAT and OAT formulations for hybrid and electric vehicles. With growing urbanization, a rising middle class, and evolving automotive technologies, the Asia Pacific is set to lead both in volume and innovation across the coolant landscape.

Competitive Landscape

The global automobile coolant market is highly competitive, driven by rising demand for EV-compatible and eco-friendly formulations. Key players such as Shell, Chevron, Exxon Mobil, and Sinclair Oil lead with advanced OAT, HOAT, and PG-based coolants tailored for electric vehicles, commercial fleets, and passenger cars.

Companies such as Blue Star Lubrication focus on heavy-duty coolants with high thermal stability, while BASF, Valvoline, Prestone, and Total Energies innovate in sustainable, long-life solutions. Strategic partnerships, R&D, and compliance with environmental regulations are central to market leadership. As EV adoption and green mobility accelerate, the need for high-performance, low-toxicity automotive coolants continues to grow globally.

Key Developments

- February 2024: Arteco launched a next-generation EV-specific coolant designed to enhance thermal stability and battery protection in electric and hybrid vehicles, marking a shift toward electrification-ready formulations.

- October 2023: UPM Biochemicals announced a partnership with HAERTOL Chemie GmbH to develop bio-based glycols for sustainable coolant solutions, accelerating the automobile coolant market shift away from fossil-derived ethylene glycol.

- August 2022: BASF introduced its Glysacorr Coolant Range optimized for electric vehicle battery thermal management, emphasizing extended service life and environmental safety.

Companies Covered in Automobile Coolant Market

- Sinclair Oil Corporation

- Blue Star Lubrication Technology

- Shell

- Lukoil Petrons

- Ashland Corporation

- Chevron

- Exxon Mobil

- Others

Frequently Asked Questions

The automobile coolant market is projected to reach US$10.8 Bn in 2032.

Electric vehicle adoption, rising vehicle production, environmental regulations, and coolant technology advancements are key drivers.

The automobile market is expected to grow at a CAGR of 3.6% from 2025 to 2032.

Eco-friendly coolants, EV-specific formulations, and emerging market growth are key opportunities.

ExxonMobil, Shell, Chevron, BASF, and Valvoline are leading players.