- Industrial Machinery

- Material Handling Cart Market

Material Handling Cart Market Size, Share, and Growth Forecast, 2026 - 2033

Material Handling Cart Market by Product Type (Cranes & Lifting Equipment, Industrial Trucks, Others), Application (Automotive, Food & Beverages, Chemical, Semiconductor & Electronics, Aviation), and Regional Analysis for 2026 - 2033

Material Handling Cart Market Size and Trends Analysis

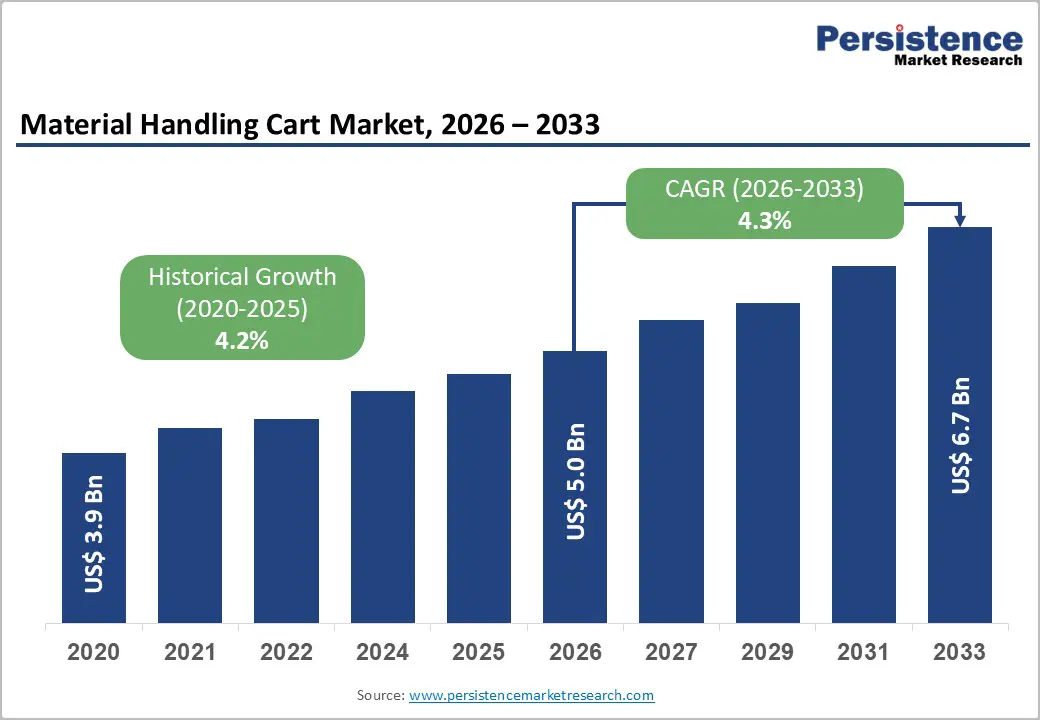

The global material handling cart market size is likely to be valued at US$5.0 billion in 2026 and is expected to reach US$6.7 billion by 2033, growing at a CAGR of 4.3% during the forecast period from 2026 to 2033, driven by rising warehouse automation, e-commerce growth, industrial expansion, labor cost pressures, and the demand for operational efficiency and supply chain optimization.

The market is witnessing increased adoption of smart and connected carts integrated with IoT and data analytics, enabling real-time inventory tracking and workflow optimization. Growing emphasis on workplace safety and ergonomic handling solutions is encouraging companies to replace manual carts with safer, more efficient alternatives. Customized and lightweight cart designs are gaining traction to meet diverse industry requirements, from automotive and food & beverage to semiconductor and aviation sectors.

Key Industry Highlights:

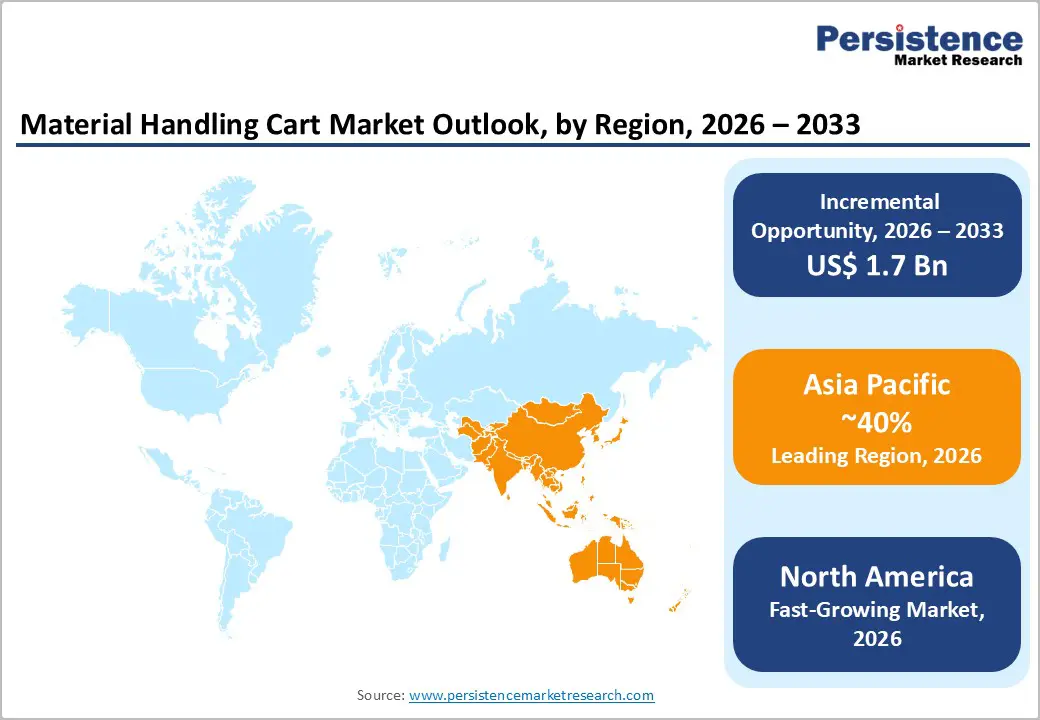

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for 40% market share in 2026, driven by industrialization, manufacturing growth, technology adoption, and rising e-commerce demand.

- Fastest-growing Region: North America is likely to be the fastest-growing region for material handling carts in 2026, supported by automation in retail and logistics, e-commerce growth, and the adoption of advanced warehouse technologies.

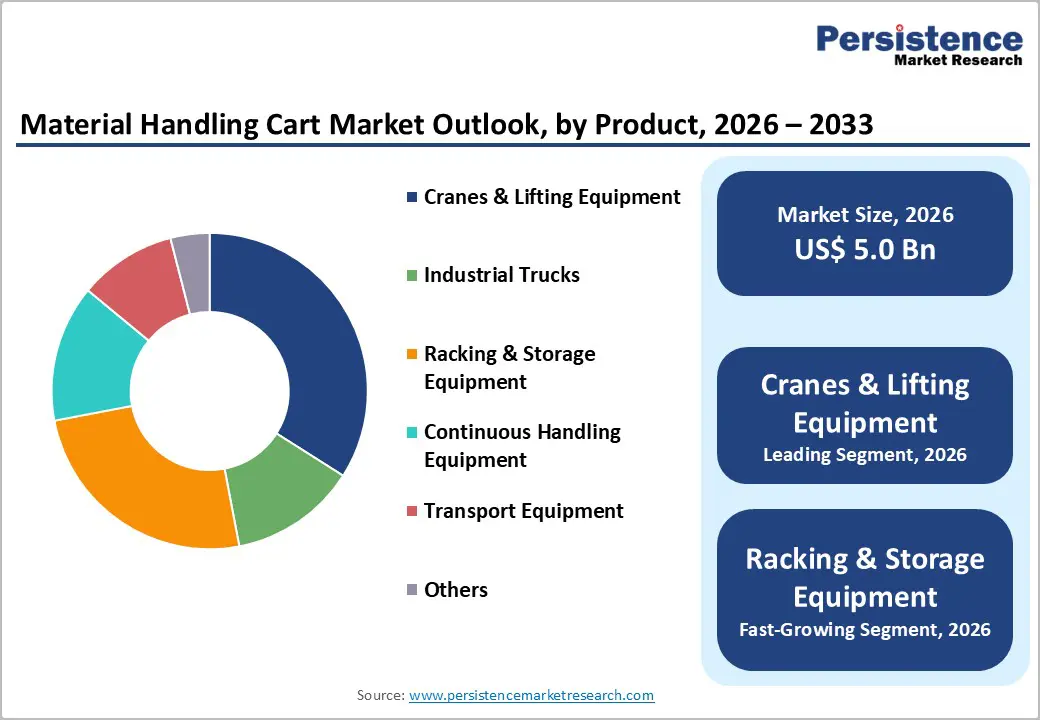

- Leading Product Type: The cranes & lifting equipment segment is projected to represent the leading product type in 2026, accounting for 35% of the revenue share, driven by heavy-duty applications in construction, manufacturing, and logistics, as well as the need for safe and efficient lifting of large loads across industries.

- Leading Application: The automotive segment is anticipated to be the leading application, accounting for over 25% of revenue in 2026, supported by assembly-line efficiency, lean manufacturing practices, and the handling of heavy components in global production hubs.

| Key Insights | Details |

|---|---|

| Material Handling Cart Market Size (2026E) | US$5.0 Bn |

| Market Value Forecast (2033F) | US$6.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

E-commerce and Logistics Expansion

The rapid growth of online retail has significantly increased order volumes, customer expectations for faster delivery, and the complexity of fulfillment operations, compelling warehouses and distribution centers to adopt more efficient internal transport solutions. Material handling carts, ranging from ergonomic push carts to advanced automated tuggers, play a vital role in supporting the high throughput required for picking, packing, sorting, and staging tasks. Unlike fixed conveyors or heavy machinery, carts offer flexibility, adaptability, and lower capital cost, making them ideal for dynamic fulfillment environments where product mixes, order sizes, and storage layouts change frequently. As e-commerce carriers and third-party logistics providers expand their footprint, they prioritize solutions that reduce cycle times, minimize manual labor strain, and integrate seamlessly with warehouse management systems.

The logistics sector’s structural evolution has amplified the importance of material handling carts as foundational components of modern supply chain operations. Traditional logistics libraries characterized by pallet jacks and forklifts are now complemented by a broader array of carts engineered for diverse functions, from transporting delicate goods to supporting high-speed sortation. E-commerce-driven demand for rapid delivery expands into tier-2 and tier-3 cities, and distribution nodes are proliferating, requiring standardized yet adaptable handling solutions that can operate across varied facility sizes. Material handling carts help bridge gaps between automated systems and manual processes, serving as flexible intermediaries that ensure smooth flow from inbound receiving to storage areas and outbound dispatch zones.

Supply Chain and Skilled Labor

Persistent shortages of key raw materials such as high-strength steel, aluminum alloys, and electronic components for smart/automated carts have created bottlenecks for manufacturers, leading to extended lead times and cost escalation. These disruptions are often exacerbated by geopolitical tensions, fluctuating trade policies, and uneven recovery rhythms across major manufacturing hubs. Congestion at major ports, intermittent factory shutdowns, and limited availability of specialized parts slow down the ability of OEMs to scale production in time to meet rising orders. Manufacturers must balance inventory risk with service-level commitments, leading to higher working capital requirements and pricing pressures.

The ongoing shortage of skilled labor is needed to operate, integrate, and maintain advanced handling systems. Warehouses and logistics facilities adopt increasingly sophisticated carts equipped with IoT sensors, automation interfaces, and real-time tracking. There is a growing demand for technicians, engineers, and operators who can configure, troubleshoot, and optimize these systems. Many regions face a mismatch between labor market supply and the technical competencies required, resulting in slower technology absorption and elevated training costs. Employers must invest in comprehensive training programs, certification initiatives, and cross-functional upskilling to ensure personnel can support mixed fleets of manual, semi-automated, and fully automated carts.

Automated Guided Vehicle (AGV) and Autonomous Mobile Robot (AMR) Integration

Warehouses and distribution centers strive for higher throughput, flexibility, and accuracy. AGVs and AMRs offer autonomous navigation, collision avoidance, and adaptive routing, significantly enhancing material movement efficiency. Integrating carts with AGV/AMR systems enables organizations to automate repetitive transport tasks such as moving inventory between workstations, consolidation points, and staging areas, reducing reliance on manual labor and minimizing operational bottlenecks. This convergence is particularly impactful in e-commerce, retail logistics, automotive assembly, and high-volume manufacturing hubs, where rapid order fulfillment and lean material flow are strategic priorities.

Organizations are increasingly seeking scalable automation that can adapt to peak demand fluctuations, SKU proliferation, and multi-channel fulfillment strategies, making automated guided vehicle and autonomous mobile robot-assisted carts an attractive alternative to fixed conveyor systems or standalone manual carts. These autonomous systems can be quickly redeployed across different zones, supporting both short- and long-haul movement within complex facilities, thereby increasing operational flexibility and lowering the total cost of ownership. Vendors in the material handling equipment market are responding by developing modular platforms that allow existing cart fleets to be retrofitted with autonomous modules, or by offering turnkey solutions with integrated navigation and fleet management.

Category-wise Analysis

Product Type Insights

The cranes & lifting equipment segment is expected to lead the material handling cart market, accounting for approximately 35% of revenue in 2026, driven by heavy-duty applications across construction, manufacturing, and logistics sectors. These systems are essential for safely lifting and transporting large or bulky loads, making them indispensable in industries that require precise load management and high operational reliability. For example, in automotive manufacturing, overhead cranes are used to move engines and chassis components across assembly lines efficiently, reducing production bottlenecks and ensuring workplace safety. The widespread adoption of cranes and lifting equipment is also supported by their ability to handle diverse weight ranges and accommodate both fixed and mobile applications.

The racking & storage equipment segment is likely to represent the fastest-growing segment in 2026, supported by the increasing demand for warehouse optimization, high-density storage solutions, and e-commerce fulfillment efficiency. For example, Mecalux S.A. provides modular shelving and automated racking systems that allow warehouses to maximize vertical space while improving inventory accessibility and throughput. The growth is largely driven by the surge in e-commerce, which requires rapid order processing and efficient storage of diverse SKUs. These systems not only reduce floor space usage but also enhance operational workflows by enabling faster picking and sorting, minimizing human effort and errors. Retailers and logistics providers adopting high-density racking can respond more quickly to fluctuating demand while reducing storage costs.

Application Insights

The automotive segment is projected to lead the market, capturing around 24% of the revenue share in 2026, supported by assembly line efficiency, lean manufacturing practices, and the handling of heavy components in global production hubs. For example, Toyota Industries Corporation extensively uses material handling carts and cranes to transport engine blocks, chassis assemblies, and other heavy automotive components across production facilities. These solutions ensure smooth material flow, reduce labor strain, and minimize downtime, which is critical in high-volume manufacturing environments. Automotive plants often integrate carts with automated guided vehicles (AGVs) and conveyor systems to achieve just-in-time delivery of components to assembly lines, enhancing overall operational efficiency.

The food & beverages segment is likely to be the fastest-growing in 2026, driven by the need for hygienic, safe, and efficient material handling solutions in production and warehousing environments. For example, Nestlé uses stainless-steel and plastic carts, designed for easy cleaning and compliance with food safety regulations, to transport ingredients and packaged goods across processing plants. The surge in packaged foods, beverages, and ready-to-eat products, coupled with the growth of e-commerce grocery fulfillment, has accelerated demand for specialized carts that prevent contamination and streamline workflow. Cold storage facilities and beverage distribution centers increasingly rely on ergonomic and automated carts to minimize manual handling, reduce labor fatigue, and maintain quality standards.

Regional Insights

North America Material Handling Cart Market Trends

North America is likely to be the fastest-growing region in the material handling cart in 2026, driven by rapid automation adoption in logistics and warehousing, rising e-commerce fulfillment demand, significant investment in smart and connected handling solutions, and increasing focus on workplace safety, labor productivity, and supply chain resilience. Increasing e-commerce penetration and omnichannel fulfillment requirements are compelling logistics providers to integrate material handling carts with digital systems, IoT connectivity, and real-time tracking, enabling more flexible and responsive material flow across facilities. Demand for ergonomic and specialized cart designs is rising in industries such as food & beverages and healthcare, where hygiene and precision are critical.

The North American market is increasingly adopting integrated automated and smart handling systems, which enhance the capabilities of traditional carts by enabling hybrid workflows. Leading companies, such as Honeywell Intelligrated, are innovating by deploying advanced conveyors, sortation systems, and automated handling platforms in fulfillment centers to optimize order processing and reduce cycle times. This integration enables carts to work in tandem with Automated Guided Vehicles (AGVs), Autonomous Mobile Robots (AMRs), and Warehouse Management Systems (WMS), creating seamless, data-driven material movement networks that boost throughput and minimize errors. The growing use of collaborative robots (cobots) and modular automation solutions enables facilities to streamline material transfer tasks without a complete infrastructure overhaul.

Europe Material Handling Cart Market Trends

Europe is likely to be a significant market for material handling carts in 2026, driven by increasing warehouse automation adoption, robust logistics and manufacturing activity, stringent safety and sustainability regulations, and rising e-commerce fulfillment needs. The European market benefits from stringent safety regulations and environmental standards that encourage the adoption of advanced handling solutions, such and connected, energy-efficient carts that reduce emissions and improve ergonomics. Increasing e-commerce activity in major hubs such as Germany, France, and the U.K. is prompting warehouse operators to modernize internal transport systems to handle higher order volumes and faster delivery timelines.

European companies are increasingly investing in systems that support predictive maintenance and workflow optimization, making material handling carts a key component of scalable warehousing strategies. The emphasis on digital transformation and resilient supply chains highlights the market’s focus on long-term efficiency improvements and operational agility. For example, Swisslog Holding AG is a Swiss automation specialist that designs and deploys advanced logistics solutions across warehouses and distribution centers. Swisslog’s offerings include automated material-handling systems, smart conveyor integration, and data-enabled cart support technologies that enhance throughput and reduce manual labor.

Asia Pacific Material Handling Cart Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for 40% market share in 2026, driven by rapid industrialization, manufacturing expansion, and strong growth in e-commerce and logistics. E-commerce giants and third-party logistics providers are investing heavily in smart warehousing and automation technologies, integrating carts with automated systems such as conveyors, automated storage and retrieval systems, and IoT-enabled tracking to improve operational visibility and speed. The rise of digital infrastructure, supportive government policies such as India’s National Logistics Policy, and the expansion of dedicated logistics parks are further boosting the adoption of advanced intralogistics solutions.

Companies are increasingly deploying ergonomic, connected carts that reduce manual labor strain, improve order fulfillment efficiency, and contribute to lean material flow across facilities. This transition reflects a broader shift in Asia Pacific toward integrated, data-driven supply chains that emphasize resilience, scalability, and cost-effectiveness in competitive manufacturing and distribution landscapes. For example, Daifuku Co., Ltd., has been expanding its logistics automation footprint across the Asia Pacific by providing automated conveyor systems, sortation solutions, and integrated cart handling platforms that support high-volume e-commerce fulfillment centers. In markets such as China and India, Daifuku’s solutions are helping logistics operators manage complex material flows, reduce turnaround times, and optimize storage utilization in bustling distribution hubs.

Competitive Landscape

The global material handling cart market is moderately fragmented, driven by the presence of both large multinational manufacturers and specialized regional players that collectively shape competitive dynamics through technological innovation, product diversification, and strategic collaborations. Major industrial equipment companies with extensive material handling portfolios, such as Toyota Industries Corporation and Crown Equipment Corporation, leverage their established distribution networks and broad product ranges to maintain significant market influence, with some Tier-I leaders collectively accounting for a substantial share of regional revenues. These global entities are complemented by other experienced firms such as Beumer Group and Flexqube, which focus on niche segments and tailored solutions that address specific operational needs across diverse industries.

With key leaders including Daifuku Co., Ltd., Swisslog Holding AG, Murata Manufacturing Co., Ltd., and SSI SCHAEFER alongside the aforementioned players, the competitive landscape is shaped by diversified strategies focused on innovation, strategic partnerships, and geographic expansion. These players compete through ongoing advancements in automation technologies, integration of IoT and analytics capabilities, and the development of eco-friendly, energy-efficient solutions that resonate with modern supply chain priorities. Collaborative alliances with technology providers and system integrators enable firms to incorporate advanced navigation, predictive maintenance, and real-time tracking into their handling solutions, thereby creating stronger value propositions.

Key Industry Developments:

- In December 2025, BEUMER Group inaugurated a state-of-the-art manufacturing facility in Reliance MET City, Jhajjar (Haryana), India, marking a major strategic expansion of its global manufacturing network. The new facility represents an INR 2 billion investment and is BEUMER’s first production hub in MET City, strengthening its ability to serve global and regional demand across airports, logistics, cement, and minerals & mining sectors. The high-tech plant significantly enhances BEUMER’s production capacity, enabling faster delivery, localized manufacturing, and improved supply chain efficiency for material handling solutions.

- In March 2025, Ocado Intelligent Automation (OIA) introduced the Porter Autonomous Mobile Robot (AMR), a pallet-moving solution designed to automate key warehouse workflows, including cross-docking, bulk picking, putaway, and pallet transportation. Porter is powered by OIA’s system-directed software and Fulfillment Execution System (FES), which intelligently orchestrates individual robots or fleets to optimize routing, reduce travel time, and minimize warehouse congestion. The Porter AMR can autonomously pick, move, and place pallets directly from the floor, handling loads of up to 1,500 kg, and can transport pallets or roll cages in a single trip.

Companies Covered in Material Handling Cart Market

- BEUMER GROUP

- Daifuku Co., Ltd.

- Honeywell International, Inc.

- KION GROUP AG

- Mecalux, S.A.

- Murata Manufacturing Co., Ltd.

- SSI SCHAEFER

- Swisslog Holding AG

- TOYOTA INDUSTRIES CORPORATION

- Vanderlande Industries B.V.

Frequently Asked Questions

The global material handling cart market is projected to reach US$5.0 billion in 2026.

The material handling cart market is driven by factors such as the increasing adoption of warehouse automation, the growth of e-commerce and logistics operations, rising labor costs, and the demand for efficient, safe, and flexible material handling solutions across various industries.

The material handling cart market is expected to grow at a CAGR of 4.3% from 2026 to 2033.

Key market opportunities include the integration of automation technologies such as AGVs and AMRs, increased investments in smart warehouses, the expansion of e-commerce fulfillment centers, and growing demand from emerging industrial economies.

BEUMER GROUP, Daifuku Co., Ltd., Honeywell International, Inc., KION GROUP AG, and Mecalux, S.A.are the leading players.