- Specialty & Fine Chemicals

- Glass Fiber Reinforced Plastic (GFRP) Composite Materials Market

Glass Fiber Reinforced Plastic (GFRP) Composite Materials Market Size, Share, and Growth Forecast, 2025 - 2032

Glass Fiber Reinforced Plastic (GFRP) Composite Materials Market by Product Type (S-Glass, C-Glass, E-Glass, Others), Resin Type (Polyester, Vinyl Ester, Epoxy, Polyurethane, Thermoplastic, Others), Manufacturing Process (Compression Molding, Injection Molding, Others), and Regional Analysis for 2025 - 2032

Glass Fiber Reinforced Plastic (GFRP) Composite Materials Market Share and Trends Analysis

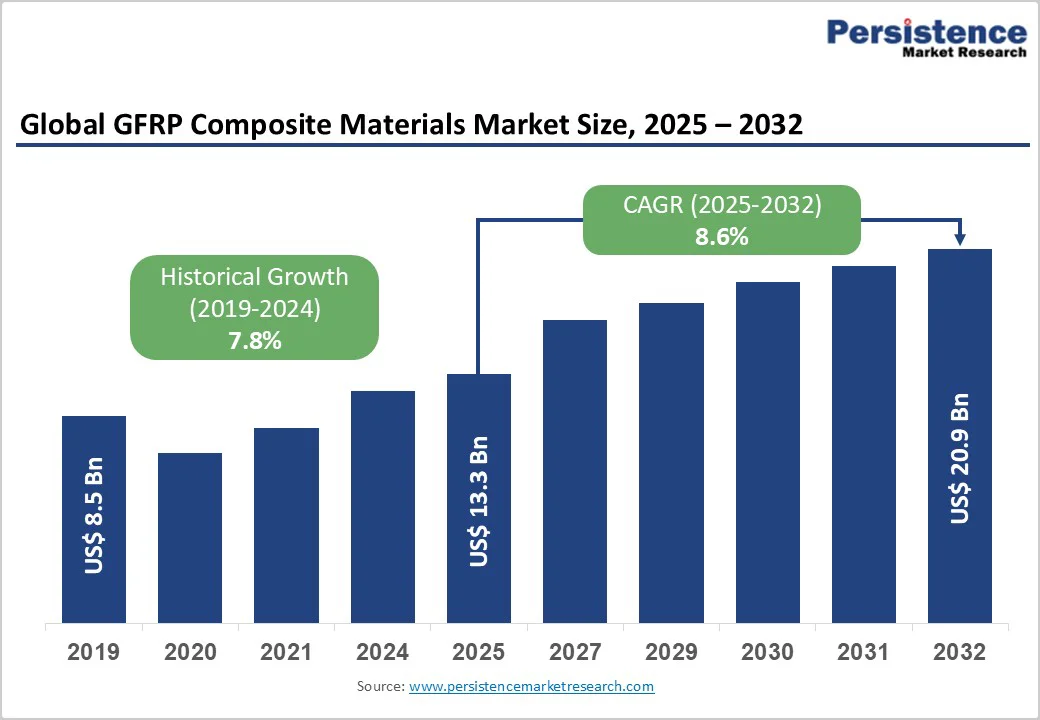

The global glass fiber reinforced plastic (GFRP) composite materials market size is likely to be valued at US$ 13.3 billion in 2025, and is projected to reach US$ 20.9 billion by 2032, growing at a CAGR of 8.6% during the forecast period 2025 - 2032.

Market expansion is driven by the escalating demand for lightweight materials in automotive and aerospace sectors, rapid growth in renewable energy applications particularly wind turbine manufacturing, and expanding construction and infrastructure projects requiring durable composites.

Regulatory emphasis on fuel efficiency and emissions reduction, technological advancements in manufacturing processes, and increasing adoption of bio-based and sustainable GFRP materials further boosts market growth.

Key Industry Highlights

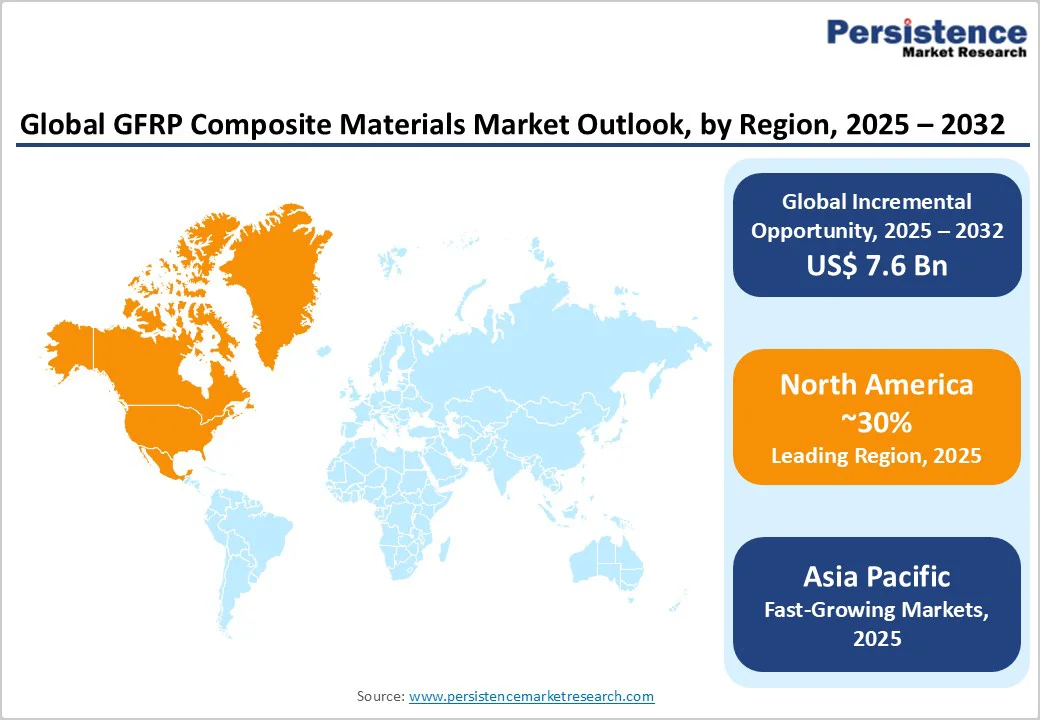

- Leading Region: North America dominates in 2025 with nearly 30% market share, driven by established aerospace and automotive manufacturing excellence and strict regulatory standards.

- Fastest-growing Regional Market: Asia Pacific is poised to register the highest CAGR of 7.2% through 2032, propelled by rapid industrialization, automotive production expansion, and construction growth.

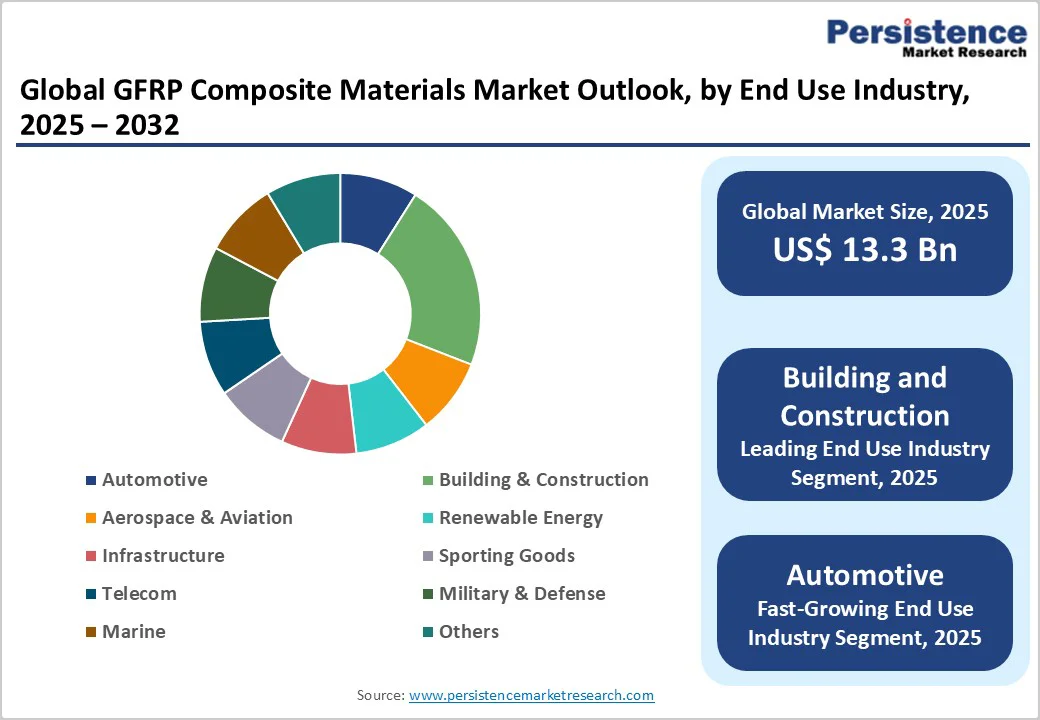

- Leading End-Use Industry: The building & construction sector dominates the GFRP composite materials market, accounting for approximately 32% of the revenue share in 2025.

- Dominant Product Type: E-glass commands largest revenue share at 54% owing to its versatility, cost-effectiveness, and proven performance across applications.

- Key Market Opportunity: Infrastructure modernization and civil engineering applications targeting corrosion-resistant pipes, bridges, and structural reinforcement supporting infrastructure resilience and lifecycle cost reduction supporting long-term growth.

| Key Insights | Details |

|---|---|

| Glass Fiber Reinforced Plastic (GFRP) Composite Materials Market Size (2025E) | US$ 13.3 Bn |

| Market Value Forecast (2032F) | US$ 20.9 Bn |

| Projected Growth CAGR (2025 - 2032) | 8.6% |

| Historical Market Growth (2019 - 2024) | 7.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Accelerating Automotive Electrification and Lightweight Material Adoption

The electrification of the automotive industry and the growing emphasis on lightweight materials are driving significant demand for glass fiber reinforced plastic composites. These materials offer substantial vehicle weight reduction while maintaining structural integrity and crash protection, which supports extended electric vehicle range and lower operating costs.

Increasingly, automotive manufacturers are replacing traditional metals and thermoplastics with GFRP composites in body panels, bumpers, interior parts, and structural reinforcements.

High-volume production methods such as compression and injection molding enable scalability and cost efficiency for automotive original equipment manufacturers (OEMs), aligning with regulatory pressures such as Euro 6 and emissions standards of the U.S. Environmental Protection Agency (EPA) that push for improved fuel efficiency through weight reduction.

In the renewable energy sector, rapid expansion of wind power capacity is fueling the demand for GFRP composites in turbine blade manufacturing. These composites provide an excellent strength-to-weight ratio, fatigue resistance, and corrosion protection, essential for the growing size and complexity of wind turbine blades used in harsh, offshore environments.

Advanced manufacturing techniques, such as pultrusion and filament winding, optimize blade production costs while ensuring durability. Renewable energy targets set by governments around the world and corporate sustainability commitments continue to promote wind capacity growth, sustaining long-term demand for GFRP composites.

High Manufacturing Costs and Raw Material Price Volatility

Glass fiber reinforced plastic composite manufacturing faces significant cost pressures due to volatile raw material prices and specialized production requirements. High-performance resins like epoxy and vinyl ester carry 25-40% price premiums over standard polyester formulations, while glass fiber feedstock costs fluctuate with crude oil and global energy prices.

Manufacturing facilities require capital-intensive equipment investments often exceeding US$ 5-10 million, limiting new entrants and regional expansions. Skilled labor shortages in developed markets further elevate operational and training costs. These raw material and labor expenses, often representing 40-50% of total production costs, constrain pricing flexibility and pose challenges in price-sensitive applications.

Environmental and regulatory compliance adds further complexity to the market. Stricter EPA and global regulations on volatile organic compound (VOC) emissions necessitate costly resin reformulations and pollution control measures. Recycling and end-of-life disposal remain problematic due to a lack of viable infrastructure and technologies, limiting circular economy integration.

Moreover, concerns about the environmental impact and durability of polymer matrices and fiberglass reinforce market hesitancy, especially among OEMs and government buyers. With regulatory uncertainty around recyclability and environmental assessments, manufacturers must innovate towards eco-friendly resins, enhanced recyclability, and sustainable production to overcome growth barriers and align with evolving market demands.

Infrastructure Modernization and Civil Engineering Applications Expansion

GFRP composites are gaining significant traction in infrastructure modernization and civil engineering due to their outstanding corrosion resistance and durability. GFRP rebars, for instance, are increasingly replacing traditional steel reinforcement in bridges, coastal structures, and other environments exposed to corrosive elements, reducing maintenance costs over the infrastructure’s lifespan.

Worldwide expansion of water treatment and desalination facilities has also augmented the demand for corrosion-resistant piping and equipment made from GFRP. Rehabilitation projects across aging transport networks and evolving building codes continue to boost GFRP use, with railway modernization further requiring lightweight, vibration-damping composites to enhance passenger comfort and energy efficiency.

Advanced manufacturing and Industry 4.0 technologies are enhancing GFRP production by improving cost efficiency and quality control. Techniques such as 3D printing and additive manufacturing enable rapid prototyping and customized composite parts, while automated compression and injection molding support scalable, high-volume production with minimal waste.

AI-driven process monitoring and digital controls optimize manufacturing parameters in real time, reducing defects and cycle times. Innovations such as self-healing composites extend product lifespans and reduce maintenance needs, supporting premium pricing strategies. These advancements attract investment from technology-focused OEMs and industrial equipment manufacturers, fueling the GFRP composite materials market growth.

Category-wise Analysis

Product Type Insights

E-glass dominates in 2025, commanding approximately 54% of the glass fiber reinforced plastic composite materials market revenue share, driven by its exceptional versatility, cost-effectiveness, and proven performance across diverse industrial applications.

E-glass provides balanced mechanical properties including excellent tensile strength while maintaining electrical insulation characteristics critical for numerous applications. The compatibility of this product with multiple resin systems including polyester, epoxy, and vinyl ester enables flexible design and manufacturing approaches, enhancing its industrial appeal.

Global E-glass production capacity significantly exceeds alternative glass types ensuring supply availability supporting cost competitiveness. On the other hand, S-glass is enlarging its market share by addressing premium aerospace and defense applications where superior tensile strength justifies premium pricing.

C-glass and ECR-glass are meeting the requirements of specialty corrosion-resistant applications in chemical processing and marine environments, supporting niche market positioning.

Resin Type Insights

Polyester resin dominates the resin type segment in the GFRP composites market, accounting for about 70% of total production. Its widespread use is driven by cost-effectiveness, ease of processing, and compatibility with high-volume manufacturing methods including open molding and hand layup.

These characteristics make polyester resin especially suitable for construction, marine, and industrial applications, where price sensitivity and scalability are crucial. The resin’s mechanical properties and corrosion resistance meet the performance needs of many cost-sensitive applications, helping to justify its broad adoption.

Moreover, polyester resin offers a flexible manufacturing process that supports regional producers and small enterprises, enabling accessibility across diverse markets. Its faster curing times facilitate lower cycle times, essential for sectors such as automotive and construction requiring rapid production.

While alternatives such as epoxy and vinyl ester provide higher performance, polyester’s balance of affordability and reliable chemical and electrical insulation properties solidifies its position as the preferred resin matrix in mass-scale GFRP composite production.

End-Use Industry Insights

The building & construction sector is the largest consumer of GFRP composite materials, accounting for about 32% of the global market share in 2025. This dominance is driven by GFRP’s exceptional strength-to-weight ratio, corrosion resistance, thermal insulation properties, and design versatility, making it highly suitable for diverse construction applications.

GFRP composites are widely used in facade panels, roofing, cladding, bridge decks, rebars, pipes, tanks, and modular structural components, offering greater durability and lower maintenance costs compared to traditional materials like steel and concrete.

The material’s ability to withstand harsh environmental conditions and reduce lifecycle costs has propelled its adoption in infrastructure projects globally. Governments and private sector investments aimed at sustainable and resilient construction further support GFRP market growth.

With ongoing advancements in composite formulations and manufacturing processes, the construction sector’s demand for GFRP composites is expected to continue expanding, reinforcing its position as a critical contributor to the market’s overall development and innovation trajectory.

Regional Insights

North America Glass Fiber Reinforced Plastic (GFRP) Composite Materials Market Trends

North America maintains significant market position through established aerospace and automotive manufacturing excellence, stringent safety and environmental regulations, and advanced technology integration.

U.S. aerospace and defense sectors drive premium GFRP composite demand for aircraft structures, defense platforms, and specialized applications justifying advanced material investments. Wind energy capacity additions in U.S. totaling 8-10 GW annually create substantial blade manufacturing demand supporting regional GFRP composite production capacity.

Vehicle production in North America exceeding 13 million units annually supports consistent composite material demand across automotive suppliers. EPA fuel efficiency standards are driving the adoption of lightweight materials, accelerating GFRP composite specification integration across platform development.

Energy efficiency building codes including IECC standards have encouraged fiberglass insulation and structural applications in construction projects. Leading manufacturers including Owens Corning have been establishing regional manufacturing strongholds, ensuring supply reliability and cost competitiveness and supporting sustained market growth.

Europe Glass Fiber Reinforced Plastic (GFRP) Composite Materials Market Trends

The Europe GFRP composite materials market exhibits mature characteristics driven by advanced regulatory frameworks and a strong focus on sustainability. Stricter automotive emissions standards such as Euro 6 are accelerating the integration of lightweight materials across European vehicle platforms, with Germany leading through its engineering innovation and automotive manufacturing prowess.

The region’s expanding wind energy sector also supports sustained demand for GFRP composites, particularly in turbine blade manufacturing to meet ambitious renewable energy capacity targets. Environmental regulations, including REACH, restrict certain resin chemistries, prompting development of low-VOC and sustainable GFRP formulations. Harmonized regulations across EU member states facilitate streamlined product development and market distribution.

Major European manufacturers such as Saint-Gobain are at the forefront of innovation, focusing on sustainable composite materials and advanced manufacturing technologies. This includes efforts to enhance recyclability, reduce emissions, and adopt circular economy principles.

The combination of regulatory pressure, green transition goals, and industry leadership ensures that Europe remains a pivotal player in the GFRP composites market, fostering continued growth marked by environmentally conscious product offerings and technological advancements.

Asia Pacific Glass Fiber Reinforced Plastic (GFRP) Composite Materials Market Trends

Asia Pacific is the fastest-growing market for GFRP composites, exhibiting a CAGR of approximately 7.2%, fueled by rapid industrialization, expanding construction activities, and growth in automotive manufacturing. China, as the world’s largest vehicle producer with annual output exceeding 27 million units, is a dominant force driving regional demand for GFRP composites.

Leading manufacturers such as Jushi Group and Chongqing Polycomp have developed extensive global production capacities, enabling cost-competitive supplies in the region.

India's ongoing infrastructure development and growing building construction markets are generating new demand for GFRP composites in applications such as pipes, tanks, and structural components, supported by government localization initiatives aimed at enhancing domestic manufacturing capabilities and reducing import reliance.

The Asia Pacific market expansion is also underpinned by favorable economic policies and increased investments in manufacturing infrastructure, fostering a competitive environment with innovation and capacity growth.

Regional manufacturers also benefit from lower production costs and technology adoption, positioning Asia Pacific as a key driver of the glass fiber reinforced plastic composite materials market growth. This diversified industrial base, combined with strong demand across sectors, fuels sustained market momentum through the forecast period and beyond.

Competitive Landscape

The global glass fiber reinforced plastic composite materials market structure exhibits moderate consolidation. Leading manufacturers such as Owens Corning, Saint-Gobain, Jushi Group, and Chongqing Polycomp International Corporation collectively command approximately 35-40% market revenue share through comprehensive product portfolios, established distribution networks, and technological expertise.

Tier-two participants including Taishan Fiberglass, Asahi Fiberglass, and regional specialists have captured critical market segments through specialized solutions and regional focus.

Strategic capacity expansion and R&D investment demonstrate growth commitment. Companies emphasize R&D investment, low-VOC and sustainable material development, advanced manufacturing process automation, and customized solution creation driving competitive differentiation. Regional specialists capitalize on localized requirements and supply chain advantages supporting diverse market coverage and emerging market penetration.

Key Industry Developments

- In May 2025, Porsche developed a carbon fiber-reinforced tape designed to enhance the structural strength and reduce the weight of automotive components. This innovative material offers improved manufacturing efficiency and supports the brand’s focus on lightweight, high-performance vehicles. The tape is expected to accelerate adoption of advanced composites in automotive production.

- In April 2025, researchers at Washington State University developed a method to recycle wind turbine blade materials, which commonly use GFRP, into improved plastics, enhancing sustainability in the wind energy sector. This innovative recycling process helps address the challenge of turbine blade disposal by creating high-performance plastics with superior durability. The advancement supports circular economy principles and reduces environmental impact in renewable energy infrastructure.

- In February 2025, Owens Corning sold its glass fiber reinforcements business to India-based Praana Group for US$ 755 million as part of a strategic shift to focus more on residential and commercial building products in North America and Europe. The sale enables Owens Corning to become a more focused and capital-efficient company, while Praana Group aims to expand its footprint in glass fiber reinforcements, leveraging the global push for clean energy, carbon footprint reduction, and material substitution.

Companies Covered in Glass Fiber Reinforced Plastic (GFRP) Composite Materials Market

- Owens Corning

- Machine Retail Group

- Everest Composites

- Prolong Composites

- Sancom Composites

- Jushi Group

- Chongqing Polycomp International Corporation

- Taishan Fiberglass Inc.

- Asahi Fiberglass Co. Ltd.

- RG Fibrotech

- Saint Gobain

- Tribeni Fiber Pvt Ltd.

- AGY Holdings Corp

- Nitto Boseki Co. Ltd.

- Jiangsu Jiuding New Material Co. Ltd.

- Nippon Electric Glass Co., Ltd.

- Lanxess AG

Frequently Asked Questions

The global glass fiber reinforced plastic (GFRP) composite materials market is projected to reach US$ 13.3 billion in 2025.

Automotive lightweight requirements, renewable energy wind installations, regulatory fuel efficiency and emissions standards, infrastructure modernization requiring corrosion-resistant materials, and aerospace applications demanding high strength-to-weight ratios and safety performance are driving the market.

The market is poised to witness a CAGR of 8.6% from 2025 to 2032.

Infrastructure modernization and civil engineering applications targeting corrosion-resistant composites for bridges, pipes, and structural reinforcement present substantial long-term opportunities for market players.

Owens Corning, Saint-Gobain, and Jushi Group are some of the key players in the market.