- Non-food Packaging

- Tape Backing Materials Market

Tape Backing Materials Market Size, Share, and Growth Forecast, 2026 - 2033

Global Tape Backing Materials Market by Material (Polypropylene (BOPP/CPP), Specialty Films (PTFE/PI), Others), Tape Type (Masking & Painter’s, Electrical & Electronics, Others), End-use Industry, Manufacturing Process, and Regional Analysis for 2026 - 2033

Tape Backing Materials Market Size and Trends Analysis

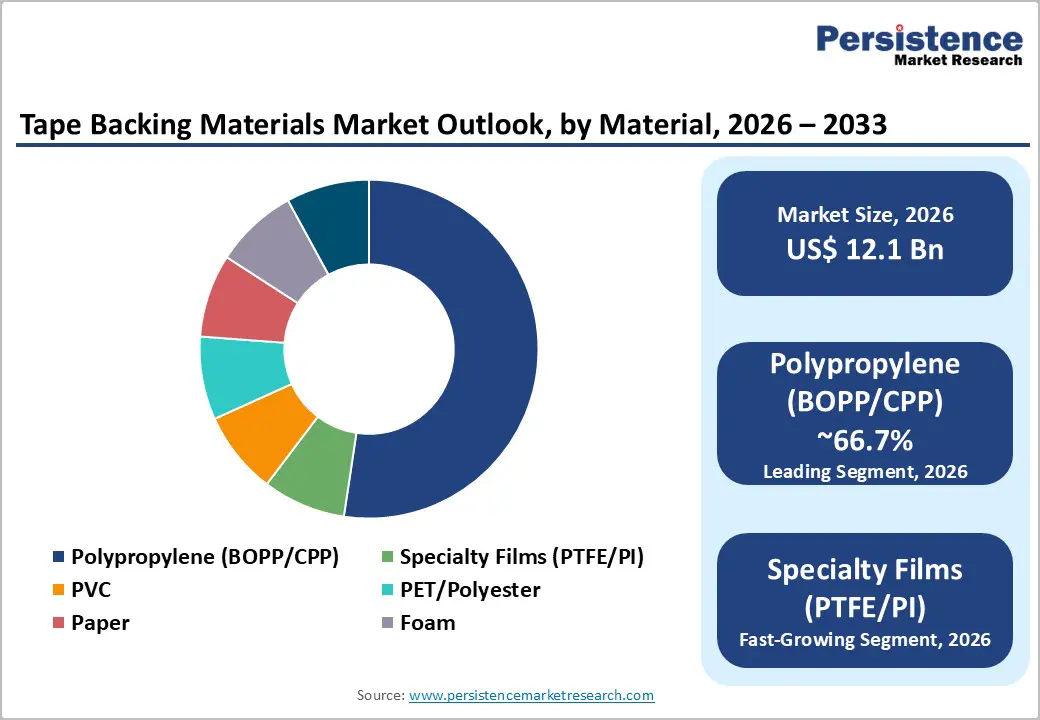

The global tape backing materials market size is likely to be valued at US$12.1 billion in 2026 and is expected to reach US$16.7 billion by 2033, growing at a CAGR of 4.7% during the forecast period from 2026 to 2033, driven by sustained expansion in e-commerce and logistics packaging, rising electronics and semiconductor manufacturing activity, and a gradual structural shift toward recyclable and fiber-based backing materials in response to sustainability requirements.

Advances in manufacturing processes, particularly biaxially oriented films (BOPP/BOPET) and multi-layer lamination technologies, are improving throughput and cost efficiency across large-scale tape production.

Key Industry Highlights

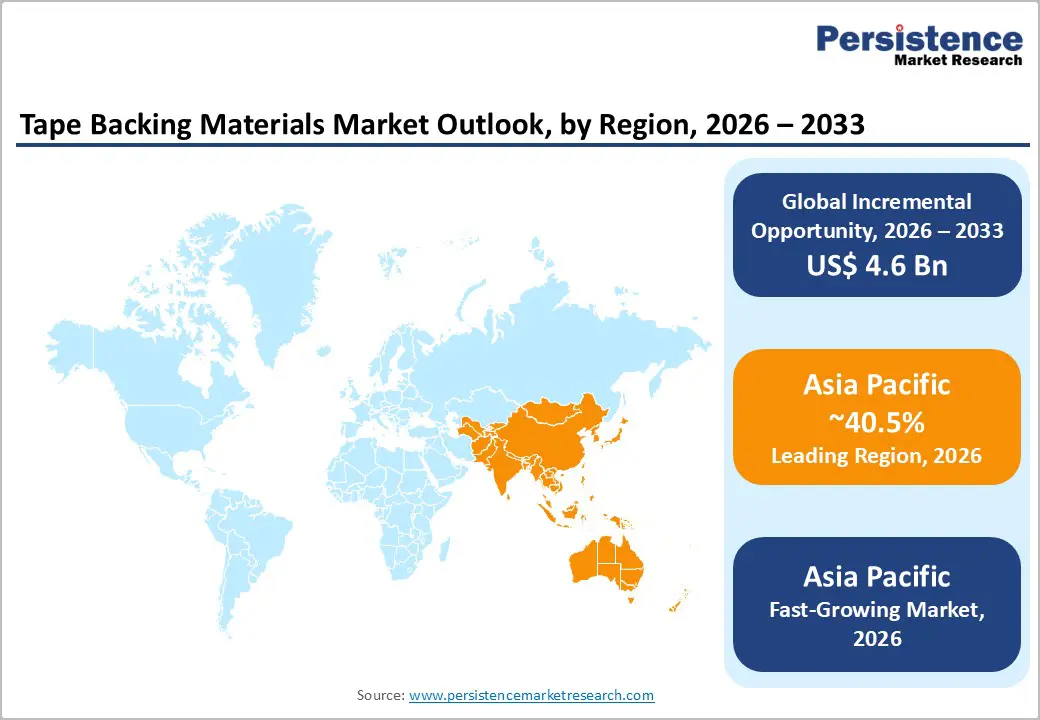

- Leading Region: Asia Pacific is projected to lead the market with approximately 40.5% share, supported by large-scale BOPP and PET film manufacturing capacity, cost-efficient production, and strong demand from packaging, electronics, and logistics applications.

- Fastest-growing Region: Asia Pacific is also likely to be the fastest-growing region, driven by expanding electronics manufacturing in China, Japan, and South Korea, rapid e-commerce growth in India and Southeast Asia, and continued investments in high-volume film extrusion and tape converting facilities.

- Investment Plans: Manufacturers are prioritizing capacity expansion in BOPP and specialty film lines, particularly in Asia Pacific and India, while North America and Europe are seeing investments in nearshoring, recycled-content materials, and specialty backing technologies to strengthen supply chain resilience and sustainability compliance.

- Dominant Material: Polypropylene (BOPP/CPP) is anticipated to dominate with approximately 66.7% revenue share, reflecting its cost efficiency, mechanical strength, and widespread use in packaging and logistics tapes.

- Leading Tape Type: The masking and painter’s tapes segment is estimated to hold the largest revenue share at approximately 31.2% in 2026, supported by consistent demand from construction, renovation, and professional painting applications.

| Key Insights | Details |

|---|---|

| Tape Backing Materials Market Size (2026E) | US$12.1 Bn |

| Market Value Forecast (2033F) | US$16.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - E-commerce and Logistics Demand (Packaging Volume Growth)

Global growth in e-commerce and parcel delivery continues to drive strong demand for packaging tapes, directly increasing consumption of tape backing materials such as BOPP and PET films. Packaging tapes remain one of the most widely used pressure-sensitive tape formats due to their role in case sealing, parcel integrity, and automated fulfillment operations. BOPP serves as the primary high-volume backing material owing to its favorable cost-to-performance ratio, tensile strength, and compatibility with high-speed converting equipment.

Although fiber-based alternatives are gaining attention, they have not materially displaced BOPP volumes in high-throughput logistics applications. Rising packaging demand strengthens upstream demand for polypropylene and polyester film producers and favors tape manufacturers with scale advantages, long-term raw material contracts, or vertically integrated film supply. Smaller converters face margin pressure due to raw material price volatility and limited purchasing leverage.

Sustainability and Regulatory Pressures (Substitution for Recyclable Backings)

Environmental regulations and customer sustainability commitments are accelerating the adoption of recyclable, fiber-based, and high-high-recycled-content tape backing materials. Retailers, logistics providers, and consumer goods companies are increasingly specifying recyclable packaging components, including tape systems. Commercialization of transparent paper backings and recycled PET carriers during 2024-2025 has expanded viable alternatives to conventional plastic backings.

These developments open new procurement opportunities with environmentally focused customers and support premium pricing for certified sustainable products. Tape producers that invest in recyclable backing development can access sustainability-driven demand and strengthen long-term customer relationships, while those that delay R&D risk losing share in procurement processes increasingly influenced by environmental criteria.

Electronics and Semiconductor Demand (Technical Backing Requirements)

Electronics and semiconductor manufacturing is a structurally high-growth end-use segment for tape backing materials. Miniaturization, automation, and higher thermal and electrical performance requirements have increased demand for thin PET films, polyimide, PTFE, and other specialty backings capable of withstanding high temperatures and precision assembly environments. Tape usage per device continues to rise across bonding, insulation, masking, and protective applications. Producers with expertise in specialty films, precision coating, and thin-film handling benefit from higher margins and long-term OEM supply agreements. However, these segments require higher capital investment, strict quality control, and extended qualification cycles, raising entry barriers for new participants.

Barrier Analysis - Raw Material Price Volatility (Polymer Feedstocks)

Tape backing material costs remain highly sensitive to fluctuations in polypropylene and polyester resin prices. Quarter-to-quarter raw material cost swings in the mid-teen percentage range have historically occurred during polymer supply disruptions or energy price spikes. While long-term supply contracts provide partial protection, they do not fully eliminate exposure, particularly for smaller or regionally focused manufacturers. This volatility limits pricing flexibility in commoditized packaging tape segments and increases margin pressure during periods of rising feedstock costs. Companies without scale, vertical integration, or diversified product portfolios are most vulnerable.

Recycling Infrastructure and End-of-Life Limitations

Despite advances in recyclable backing materials, recycling infrastructure remains uneven across regions. Even paper-backed or recyclable tape products depend on downstream acceptance, sorting, and processing systems to achieve circularity. In markets with limited recycling capabilities, adoption of sustainable tape backings may be delayed. As a result, conversion timelines vary significantly by geography and can extend three to seven years, depending on public policy, waste management systems, and customer readiness. This constraint reduces short-term addressable volume for recyclable backings and slows market-wide transition.

Opportunity Analysis - Sustainable and Lightweight Backing Innovations

Recyclable paper, renewable-fiber, and downgauged film backings present a meaningful replacement opportunity for traditional plastic carriers in light- to medium-duty applications. Functional coatings and reinforced fiber structures enable performance parity while supporting material reduction and sustainability goals. Manufacturers that co-develop solutions with brand owners and e-commerce platforms can accelerate adoption through pilot programs, qualification testing, and long-term supply agreements tied to environmental targets.

High-Performance and Specialty Backings for Advanced Applications

Demand for specialty backings with properties such as thermal resistance, electrical insulation, EMI shielding, and chemical durability is expanding alongside electronics, electric vehicles, and advanced manufacturing. Multi-layer constructions allow customization for specific OEM requirements without excessive system complexity. Producers with advanced coating, lamination, and slitting capabilities can secure long-term supply relationships in EV battery assembly, semiconductor packaging, and high-temperature industrial uses, benefiting from higher value-per-unit and deeper customer integration.

Operational Differentiation through Integration and Services

Vertical integration across film production, adhesive formulation, and tape converting improves margin control, quality consistency, and supply reliability. Localization of backing material production strengthens resilience and supports regulatory and customer requirements. Offering value-added services such as recycling programs, take-back initiatives, private-label manufacturing, and digital printing further differentiates suppliers and embeds them more deeply into customer operations, particularly in retail, logistics, and industrial distribution channels.

Category-wise Analysis

Material Insights

Polypropylene-based films are anticipated to represent the dominant material segment, accounting for approximately 66.7% of the revenue share. Their leadership is primarily driven by cost efficiency, favorable strength-to-weight characteristics, and excellent compatibility with high-speed tape converting and automated packaging systems. BOPP, in particular, has become the industry standard backing material for carton sealing and packaging tapes used across logistics, warehousing, and e-commerce operations.

The material’s consistent tensile strength, moisture resistance, and printability make it suitable for large-scale, high-throughput applications where performance reliability and low unit cost are critical procurement criteria. Manufacturers with upstream integration into polypropylene resin production or in-house film extrusion benefit from economies of scale, tighter cost control, and supply chain stability, strengthening their competitive position in price-sensitive packaging tape segments. As global parcel volumes continue to rise, polypropylene-based backings are expected to retain structural dominance despite growing sustainability discussions.

Specialty films, including polytetrafluoroethylene (PTFE) and polyimide, are likely to be the fastest-growing material segment within the tape backing materials market. Growth is driven by increasing demand from electronics, aerospace, automotive electronics, and high-temperature industrial applications, where conventional polymer films do not meet performance requirements. These materials provide exceptional thermal resistance, electrical insulation, dimensional stability, and chemical inertness, enabling reliable performance in extreme operating environments.

Although specialty films account for a smaller share of total volume, they command significantly higher average selling prices, supporting strong value growth. Entry barriers in this segment remain high due to complex manufacturing processes, stringent quality standards, and extended OEM qualification cycles. As a result, established suppliers with advanced material science capabilities and long-standing customer relationships enjoy durable competitive advantages. Continued investment in semiconductor fabrication, electric vehicles, and advanced manufacturing is expected to sustain above-market growth for specialty film-based tape backings.

Tape Type Insights

Masking and painter’s tapes are estimated to represent the largest tape type segment, accounting for approximately 31.2% of the revenue share in 2026. Demand is supported by steady activity across residential and commercial construction, renovation, automotive refinishing, and professional painting applications. These tapes are valued for their ability to provide clean removal, controlled adhesion, surface protection, and compatibility with a wide range of substrates, including painted walls, metals, glass, and plastics. Customer purchasing decisions in this segment are influenced by performance consistency and ease of use rather than price alone, contributing to strong brand loyalty and repeat demand.

Tape manufacturers compete by optimizing backing materials such as crepe paper, thin polymer films, and reinforced substrates to balance adhesion strength with residue-free removal. The segment benefits from stable replacement demand and remains relatively resilient to economic cycles compared with discretionary industrial tape categories.

Electrical and electronics tapes are likely to be the fastest-growing tape type segment, supported by structural growth in semiconductor manufacturing, consumer electronics, renewable energy systems, and electrified transportation. These applications require tape solutions that deliver precise insulation performance, thermal endurance, flame resistance, and dimensional stability, placing higher technical demands on backing materials and adhesive systems.

Growth is further reinforced by ongoing device miniaturization, increased tape usage per electronic component, and rising automation in electronics assembly processes. Manufacturers serving this segment benefit from higher margins but must invest in advanced process control, cleanroom manufacturing environments, and rigorous quality assurance systems. As electronics production continues to expand globally, particularly in Asia Pacific, electrical and electronics tapes are expected to remain a key growth engine for the overall tape backing materials market.

Regional Insights

North America Tape Backing Materials Market Trends - Nearshoring, Specialty Tapes, and Sustainability-Driven Innovation

North America represents a high-value and innovation-driven market for tape backing materials, supported by strong demand from electronics, medical devices, industrial manufacturing, and packaging applications. The U.S. accounts for the majority of regional consumption due to high per-capita tape usage, advanced automation in packaging and manufacturing, and a well-established converting ecosystem. Packaging tapes remain the largest volume contributor, while medical, electrical, and specialty industrial tapes deliver a disproportionate share of value. A defining regional trend is nearshoring and supply chain resilience, which has accelerated investments in domestic film extrusion, coating, and tape converting capacity.

Leading manufacturers such as 3M and Avery Dennison have continued to expand U.S.-based production lines for specialty films, medical-grade backings, and pressure-sensitive tape systems to reduce dependency on overseas supply and improve responsiveness to customers. These investments strengthen demand for high-quality PET, polyimide, and specialty polymer backings.

Sustainability requirements are reshaping procurement criteria across North America. Large retailers and logistics operators increasingly specify recycled content, recyclability, and fiber-based alternatives in packaging components, influencing tape design and backing material selection. In response, manufacturers have introduced paper-based and recycled-polyester-backed tape products targeted at e-commerce and consumer packaging applications. This shift supports gradual diversification away from conventional BOPP in select use cases, although polypropylene remains dominant in high-volume logistics operations.

Innovation ecosystems centered on advanced manufacturing, medical technology, and electronics assembly continue to support premium tape backing demand. As a result, North America maintains above-average pricing, strong margins in specialty segments, and stable long-term growth prospects, despite being a relatively mature market in volume terms.

Europe Tape Backing Materials Market Trends - Regulation-Led Sustainability and High-Performance Industrial Demand

Europe is characterized by strong demand for engineered and application-specific tape backing materials, supported by industrial production, automotive manufacturing, construction renovation activity, and healthcare applications. Germany leads regional demand due to its extensive automotive, electrical engineering, and industrial equipment sectors, where performance-driven tape solutions are integral to assembly, insulation, and surface protection processes.

The U.K. and France contribute steady volumes through building renovation, professional painting, and consumer-facing tape applications. The region’s operating environment is shaped by stringent environmental regulations and harmonized sustainability policies, which are accelerating the adoption of recyclable, low-emission, and fiber-based backing materials. Circular economy objectives influence both material selection and product design, encouraging tape manufacturers to reduce polymer content, increase recycled material usage, and improve end-of-life compatibility. European producers such as Tesa SE have expanded their portfolios of paper-backed, solvent-free, and recycled-content tape solutions to align with evolving regulatory and customer expectations.

Europe also demonstrates strong demand for laminated and reinforced backing materials, particularly in automotive wiring, electric vehicle assembly, and industrial masking applications. The ongoing transition toward electrified transportation supports increased use of PET and specialty polymer backings that offer thermal stability and dimensional consistency. Investment in R&D remains a key competitive factor, as customers prioritize compliance, reliability, and performance over price alone. Overall, Europe’s tape backing materials market emphasizes quality, sustainability, and regulatory compliance, resulting in slower volume growth than Asia Pacific but higher value density and innovation intensity.

Asia Pacific Tape Backing Materials Market Trends - Manufacturing Scale, Electronics Leadership, and Rapid Volume Growth

Asia Pacific is projected to lead the market with approximately 40.5% share in 2026 and remains the fastest-growing region, driven by its central role in global manufacturing and packaging supply chains. China dominates high-volume production of BOPP and PET films, supported by large-scale polymer capacity, cost-efficient manufacturing, and extensive tape converting infrastructure.

These capabilities underpin the region’s leadership in packaging and logistics tape applications. Japan plays a distinct role as a technology leader in specialty and high-performance backing materials, particularly for electronics, automotive electronics, and semiconductor manufacturing. Companies such as Nitto Denko have advanced thin-film, high-temperature, and precision backing technologies that support premium tape applications requiring exacting performance standards. These products command higher margins and reinforce Asia Pacific’s leadership in electronics-focused tape solutions.

India is emerging as a key growth market due to rapid expansion in e-commerce, infrastructure development, and domestic manufacturing. Investments in new BOPP film lines and tape converting facilities are increasing local availability of packaging-grade backing materials while reducing reliance on imports. This expansion supports rising demand from logistics, construction, and consumer goods sectors.

Across Southeast Asia, competitive labor costs and expanding industrial bases are attracting new converting capacity, further strengthening the region’s supply position. Combined with sustained growth in electronics production and global export activity, Asia Pacific is expected to remain the primary volume growth engine and manufacturing backbone of the global tape backing materials market over the forecast period.

Competitive Landscape

The global tape backing materials market is moderately concentrated. Large multinational manufacturers lead high-value applications, while commodity packaging backings are supplied by numerous regional producers. Specialty film segments exhibit a higher concentration due to technical barriers and qualification requirements.

Key developments include new product launches in professional masking tapes, capital investments in polyester and adhesive capacity, expansion of recycled-content tape portfolios, and commercialization of paper-based transparent backings. These actions reflect industry-wide focus on performance innovation, sustainability, and supply chain localization.

Dominant strategies include product innovation, sustainability differentiation, vertical integration, and regional capacity expansion. Certification capability, OEM qualification expertise, and full-chain sustainability offerings are increasingly important competitive differentiators.

Key Industry Developments

- In June 2025, Tesa SE announced the expansion of its recycled PET and paper-based tape backing portfolio, supporting increased adoption of sustainable packaging and masking tape solutions across Europe and North America.

- In December 2024, Ahlstrom introduced MasterTape Cristal, a paper-based transparent backing material designed to reduce plastic waste while delivering performance comparable to conventional plastic tapes, reinforcing sustainability in packaging and industrial tape applications.

Companies Covered in Tape Backing Materials Market

- 3M

- tesa SE

- Nitto Denko Corporation

- Avery Dennison

- Intertape Polymer Group

- Lintec Corporation

- Shurtape Technologies

- Lohmann GmbH & Co. KG

- Scapa

- Berry Global

- Henkel

- Bostik

- Saint-Gobain Performance Plastics

- PPM Industries

- Advance Tapes International

- Nichiban Co., Ltd.

- Teraoka Seisakusho Co., Ltd.

- Yongle Tape Co., Ltd.

Frequently Asked Questions

The global tape backing materials market is estimated to be valued at US$12.1 billion in 2026.

By 2033, the tape backing materials market is expected to reach US$16.7 billion.

Key trends include rising demand from e-commerce and logistics packaging, growing use of specialty films for electronics and high-temperature applications, increased focus on recyclable and recycled-content backing materials, and capacity expansion in Asia Pacific supported by cost-efficient manufacturing.

By material, polypropylene-based backings (BOPP/CPP) lead the market with approximately 66.7% share, driven by their cost efficiency and widespread use in packaging and logistics tapes.

The tape backing materials market is projected to grow at a CAGR of 4.7% between 2026 and 2033.

Major players include 3M, Tesa SE, Nitto Denko Corporation, Avery Dennison, and Intertape Polymer Group, all of which have broad offerings across packaging, masking, industrial, and specialty tape applications.