- Bulk Chemicals

- Hydrogenated Vegetable Oil Market

Hydrogenated Vegetable Oil Market Size, Share, and Growth Forecast, 2025 - 2032

Hydrogenated Vegetable Oil Market By Grade (Unfractionated, Fractionated), Source (Soybean Oil, Palm Oil, Sunflower Oil, Cottonseed Oil, Rapeseed/Canola Oil), End-user (Food and Beverage, Personal Care and Cosmetics), and Regional Analysis for 2025 - 2032

Hydrogenated Vegetable Oil Market Size and Trends Analysis

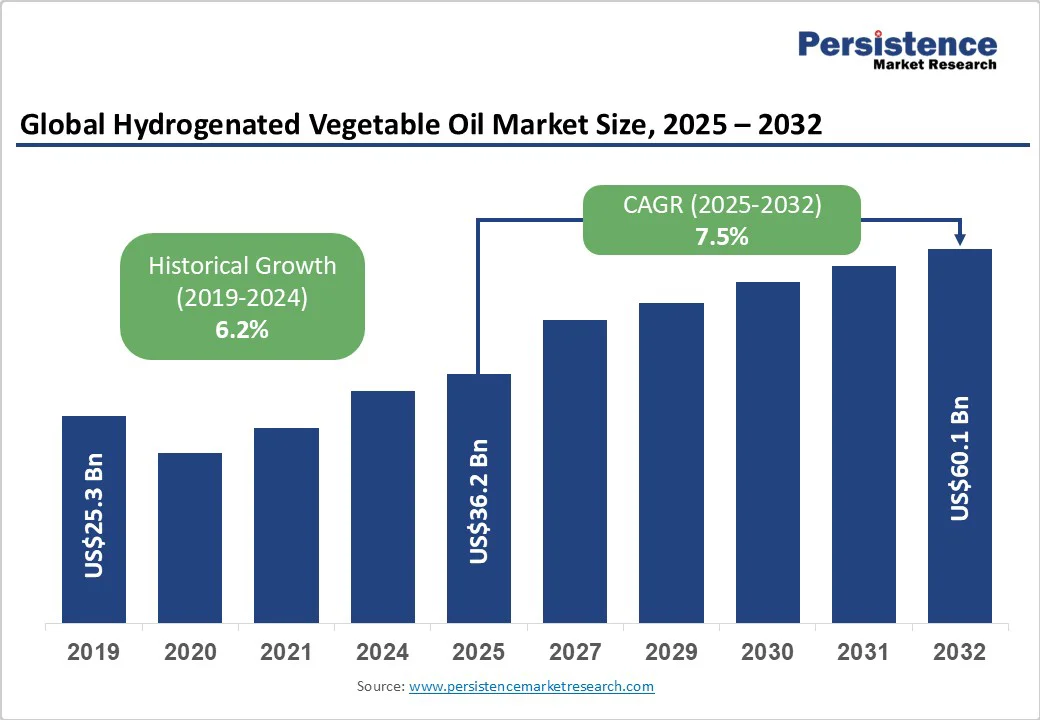

The global hydrogenated vegetable oil market size is expected to be valued at US$36.2 billion in 2025. It is projected to reach US$60.1 billion by 2032, growing at a CAGR of 7.5% from 2025 to 2032, driven by high demand in food processing, personal care, and renewable fuels. Increasing awareness of sustainable and plant-based ingredients is driving further demand in the cosmetics industry.

Key Industry Highlights

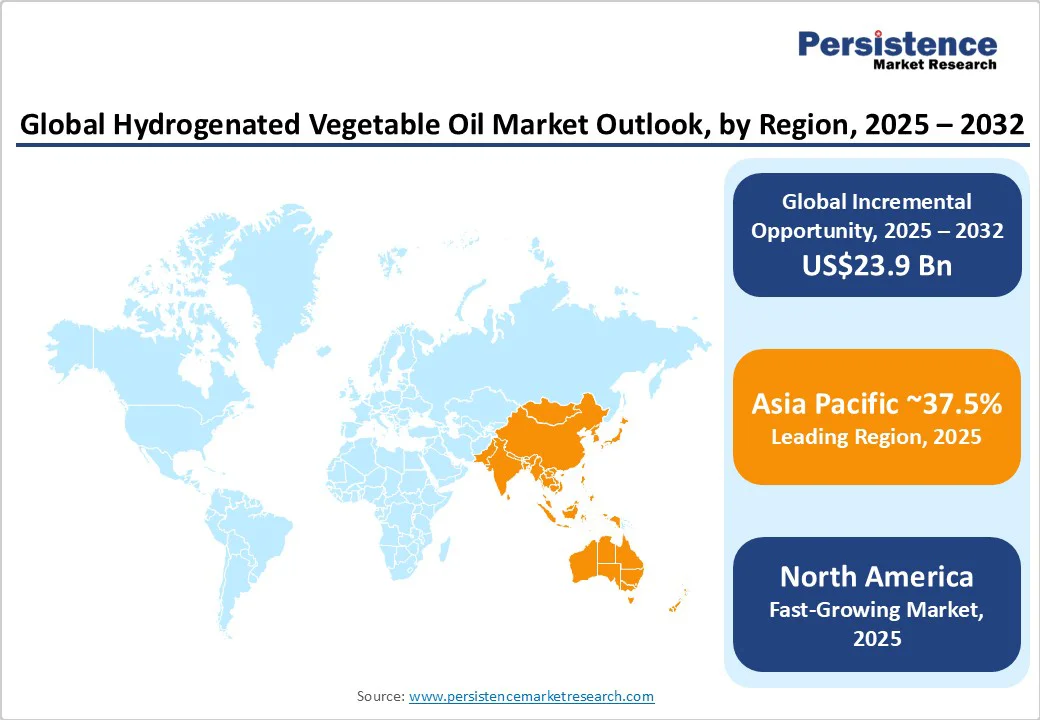

- Leading Region: Asia Pacific, with about 37.5% share in 2025, due to rising demand from food processors and abundant feedstock availability.

- Fastest-growing Region: North America, owing to investments in renewable fuels and regulatory support for sustainable HVO applications.

- Sustainability Initiative: Škoda Auto switched to using high-quality HVO fuel for the initial fill in newly manufactured diesel vehicles and for refueling its logistics fleet.

- Leading Grade: Unfractionated HVO holds nearly 46.8% share in 2025, due to its high oxidative stability and versatile semi-solid consistency.

- Dominant Source: Soybean oil, approximately 38.2% of the hydrogenated vegetable oil market share in 2025, backed by its balanced fatty acid profile.

- Key End-user: The food and beverage sector accounted for 54.7% of total sales in 2025, as HVO improves texture and mouthfeel.

| Key Insights | Details |

|---|---|

|

Hydrogenated Vegetable Oil Market Size (2025E) |

US$36.2 Bn |

|

Market Value Forecast (2032F) |

US$60.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Extended Shelf Life and Stability in Processed Food

One of the key growth drivers of hydrogenated vegetable Oil (HVO) is its resistance to oxidation and spoilage, which drastically improves the shelf life of processed food. This property ensures that products, such as packaged snacks, baked goods, and ready-to-eat meals, remain fresh over extended periods without compromising flavor or quality.

Companies are increasingly utilizing HVO to reduce waste and enhance supply chain efficiency, particularly in regions with extensive food distribution networks. For example, leading food processors in India and China are adopting hydrogenated oils in packaged bakery and snack products to maintain consistent quality during transportation and storage, while also meeting surging consumer demand for convenience food items that retain freshness for longer periods.

Improving Texture and Sensory Appeal in Food Products

Another important factor driving the adoption of HVO is its ability to improve the texture and mouthfeel of various food products. Hydrogenated oils provide the semi-solid consistency required in margarine, spreads, baked goods, and snack foods, delivering a smooth, creamy texture that consumers expect.

This characteristic also enables manufacturers to achieve uniform product quality, especially in large-scale industrial production. Europe-based bakery brands, for instance, continue to use HVO to maintain the ideal flakiness in pastries and the crispiness in cookies, ensuring that end products meet consumer expectations for taste and texture, while supporting product formulation development.

Barrier Analysis - Health Concerns Related to Trans Fats

A major restraint for HVO is the presence of trans fats in partially hydrogenated oils, which have been linked to adverse cardiovascular effects. Trans fats can raise LDL cholesterol and lower HDL cholesterol, contributing to an increased risk of coronary heart disease and stroke. These health concerns have prompted strict regulations in the U.S. and Europe, where governments are enforcing limits on trans-fat content in food products.

For instance, the U.S. Food and Drug Administration (FDA) banned artificial trans fats in processed foods in 2018, compelling several manufacturers to reformulate recipes or seek alternative oils. Such regulatory pressures limit the expansion of HVO in traditional food applications, as consumers prefer healthy alternatives with minimal cardiovascular risk.

Metabolic and Insulin-related Health Risks

Another key challenge for the market is the potential contribution of HVO to metabolic disorders. Research indicates that high consumption of hydrogenated oils may be associated with insulin resistance, obesity, and metabolic syndrome, conditions that increase susceptibility to type 2 diabetes. A 2023 study published in Nutrients highlighted that diets high in trans fats correlate with impaired glucose metabolism and elevated inflammatory markers.

This rising awareness has led health-conscious consumers to shift toward non-hydrogenated or naturally saturated oils such as olive and avocado oil, thereby creating market pressure on traditional HVO producers. A few companies are hence investing in alternative formulations and interesterified oils to maintain market relevance while addressing public health concerns.

Opportunity Analysis - Developments in Deodorization Techniques

One promising growth opportunity for HVO lies in developing novel deodorization methods. Traditional hydrogenated oils often retain slight odors that can affect flavor in food applications, limiting their use in premium products. Modern techniques, such as low-temperature vacuum deodorization and steam stripping, enable manufacturers to produce odor-neutral HVO without compromising its stability or nutritional profile.

Companies such as Cargill and Bunge have invested in these technologies to serve the high-end bakery and confectionery segments in Europe and the Asia-Pacific, where consumer demand for neutral-tasting oils is rising. This development not only enhances product quality but also opens up new opportunities in ready-to-eat meals, plant-based spreads, and snack foods.

Hydrogenated Vegetable Oil as a Renewable Fuel Source

Another significant opportunity for HVO is its application in producing renewable, low-emission fuels. Hydrogenated vegetable oils can be hydrotreated to produce hydrotreated vegetable oils for use in biodiesel and sustainable aviation fuels, providing a clean alternative to fossil fuels. Europe-based companies such as Neste and Galp Energia are actively expanding HVO-based biofuel production to meet the EU’s Renewable Energy Directive targets and rising corporate sustainability commitments.

For instance, Neste’s renewable diesel plants in the Netherlands and Singapore utilize HVO derived from waste oils and fats, reducing carbon emissions by up to 90% compared to conventional diesel. Expanding HVO into the biofuel sector not only supports global decarbonization efforts but also provides a high-value avenue for waste valorization and circular economy initiatives.

Category-wise Analysis

Grade Insights

The unfractionated segment is expected to dominate with a share of approximately 46.8% in 2025, as it retains the full spectrum of fatty acids, providing excellent stability and versatility for multiple applications. Its uniform semi-solid consistency makes it ideal for bakery products, margarines, and confectionery, where texture and spreadability are essential. Unfractionated HVO also has a high melting point and superior oxidative stability, which help extend the shelf life of processed food.

Fractionated HVO is seeing steady growth as it allows producers to separate oils into liquid and solid fractions, enabling personalized applications. The liquid fraction is increasingly used in salad dressings, spreads, and margarine formulations that require soft textures. In contrast, the solid fraction is valuable in confectionery and bakery fats needing high melting points.

Source Insights

Soybean oil is anticipated to hold a share of nearly 38.2% in 2025, owing to its widespread availability, balanced fatty acid profile, and relatively low cost. It contains high levels of polyunsaturated fats that can be effectively hydrogenated to achieve the desired semi-solid consistency for margarines, bakery fats, and processed snacks. The U.S., Brazil, and Argentina are leading soybean producers, providing a reliable and extensible supply chain for HVO manufacturers.

Sunflower oil is considered a key source due to its light flavor, low saturated fat content, and high oxidative stability. Its mild taste allows HVO produced from sunflower oil to be used in bakery products, confectionery, and snack foods without altering flavor profiles. Eastern European countries, particularly Ukraine and Russia, dominate sunflower cultivation, ensuring a steady supply for regional HVO production.

End-user Insights

The food and beverages segment is expected to account for about 54.7% of the market in 2025, owing to the versatility of HVO in improving the texture, shelf life, and stability of processed food. HVO is essential in baked goods, margarine, confectionery, and snacks, providing a semi-solid consistency and oxidative stability that help ensure products maintain quality during storage and transport. In emerging markets such as India and Southeast Asia, the surge in packaged and ready-to-eat foods has boosted demand for HVO.

HVO is extensively used in personal care and cosmetics due to its emollient properties, stability, and ability to improve texture. It serves as a structuring agent in products such as lip balms, creams, lotions, and hair care items, providing smooth application and long-lasting moisture. Cosmetic brands, including L’Oréal and Beiersdorf, are incorporating HVO into formulations to improve product consistency while using plant-based ingredients that cater to sustainable and vegan trends.

Regional Insights

Asia Pacific Hydrogenated Vegetable Oil Market Trends

Asia Pacific is poised to account for nearly 37.5% of the share in 2025, spurred by urbanization, industrialization, and increased demand for processed food. China is considered a key contributor due to its expanding food processing industry. The availability of feedstocks such as palm and soybean oils further supports the production of HVO in the country.

The food and beverage industry is the dominant end-user segment for HVO in the Asia Pacific, utilizing it in products such as baked goods, margarine, and confectionery to improve texture, shelf life, and stability. Additionally, the region is seeing a surge in interest in HVO for non-food applications, including cosmetics and biofuels, as consumers and industries seek more sustainable and renewable alternatives.

North America Hydrogenated Vegetable Oil Market Trends

In North America, HVO is integral to various industries, including food production, cosmetics, and biofuels. The U.S. has specifically seen significant investment in HVO production facilities. For instance, Diamond Green Diesel in Louisiana has expanded its renewable diesel production capacity to over 275 million gallons annually, meeting the high demand for renewable fuels in the transportation and industrial sectors. Similarly, Neste's renewable diesel plant in California contributes to the region's sustainable fuel supply.

The market faces challenges due to policy uncertainties and trade tensions. In March 2025, Reuters reported that biofuel companies in the U.S. and Canada were reducing production amid unclear policies on green fuel subsidies and concerns over a potential trade war. This uncertainty has disrupted the biofuel industry's growth, affecting the demand for vegetable oils. New U.S. tariffs have made imported feedstocks more expensive, and uncertainty over biofuel subsidy programs is further hindering the market.

Europe Hydrogenated Vegetable Oil Market Trends

Europe’s market is experiencing steady growth, boosted by stringent environmental policies and increasing demand for sustainable fuels. The European Union's Renewable Energy Directive (RED II) mandates high biofuel blending ratios, propelling the adoption of HVO in transportation and aviation sectors. For example, Toyota has enabled its Land Cruiser and Hilux models in Western Europe to use HVO100 diesel fuel, derived from renewable sources such as waste cooking oil, complying with EU standards.

The automotive fuel segment is a key contributor to the European market, with substantial investments in production facilities. Galp Energia, in collaboration with Japan's Mitsui, is constructing an HVO plant at its Sines refinery in Portugal, aiming to produce 270,000 metric tons per year of renewable biodiesel and sustainable aviation fuel by 2026. This facility will utilize green hydrogen generated from wind and solar energy, showcasing Europe's commitment to low-carbon solutions.

Competitive Landscape

The global hydrogenated vegetable oil market consists of leading companies such as Archer Daniels Midland Co., Bunge Ltd., Cargill Inc., and Wilmar International Ltd., among others. They are focusing on product innovation and capacity expansion to meet the increasing demand for hydrogenated vegetable oils in various applications. A few other players are exploring new business models to adapt to market changes.

Key Industry Developments

- In October 2025, Eni launched a new hydrotreated vegetable oil/sustainable aviation fuel project in Sannazzaro de’ Burgondi, Italy. It has started the authorization process and has applied to an environmental impact assessment.

- In April 2025, Repsol and Bunge announced a major milestone in the development of renewable fuels in Europe: the incorporation of novel intermediate crops into the production of renewable fuels. Camelina and safflower will be processed into low-carbon-intensity oils and used as feedstocks to produce hydrotreated vegetable oil.

Companies Covered in Hydrogenated Vegetable Oil Market

- Archer Daniels Midland Company

- Croda International Ltd.

- BASF SE

- AAK AB

- Louis Dreyfus Company (LDC)

- Bunge Limited

- Amandus Kahl GmbH & Co. KG

- Clariant International Ltd.

- Wilmar International Limited

- The Innovation Company

- Kahl World

- Evident Ingredients GmbH

Frequently Asked Questions

The hydrogenated vegetable oil market is projected to reach US$36.2 Billion in 2025.

The rising demand for long shelf life in processed food and the adoption of biofuels are the key market drivers.

The hydrogenated vegetable oil market is poised to witness a CAGR of 7.5% from 2025 to 2032.

The emergence of novel deodorization methods and the expansion into aviation fuels are the key market opportunities.

Archer Daniels Midland Company, Croda International Ltd., and BASF SE are a few key market players.