- Renewable Energy

- Europe Hydrogen Electrolyzer Market

Europe Hydrogen Electrolyzer Market Size, Share, and Growth Forecast, 2025 - 2032

Europe Hydrogen Electrolyzer Market By Technology (Alkaline Electrolyzer, Proton Exchange Membrane (PEM) Electrolyzer, Others), Power Rating (Below 500 kW, Others), End-user Industry (Energy & Utilities, Others), and Country Analysis for 2025 - 2032

Europe Hydrogen Electrolyzer Market Size and Trends Analysis

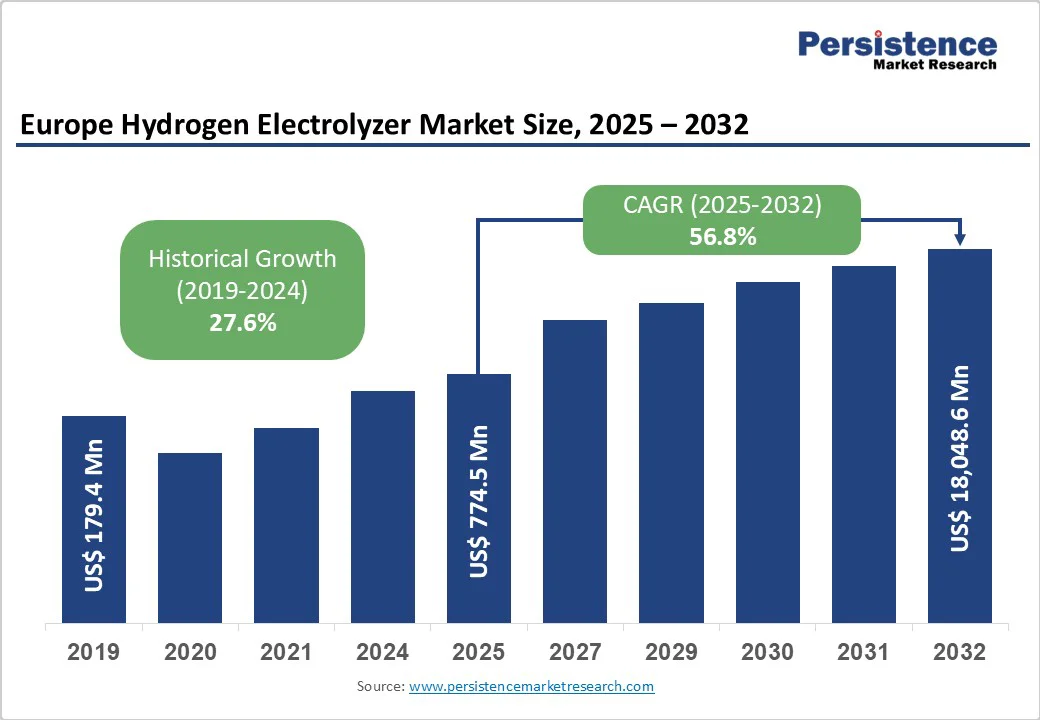

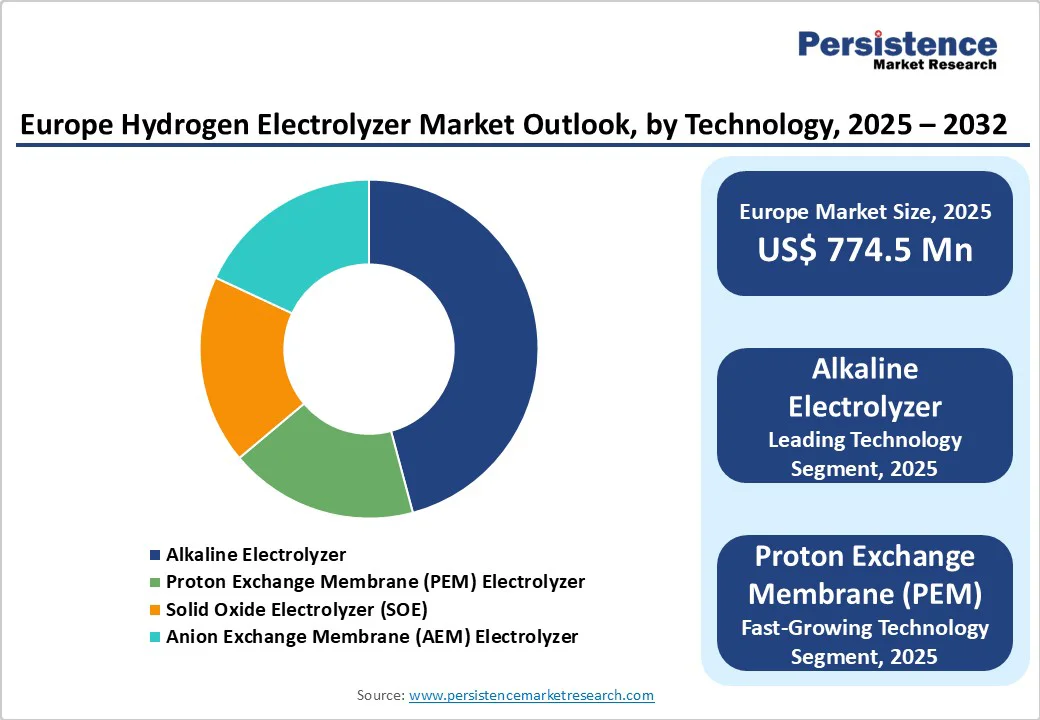

The Europe hydrogen electrolyzer market size was valued at US$774.5 Million in 2025 and is projected to reach US$18,048.6 Million by 2032, growing at a CAGR of 56.8% between 2025 and 2032, driven by aggressive decarbonization mandates, substantial government funding through IPCEI programs, and the scaling of renewable energy integration across industrial sectors.

Europe accounts for approximately 33% of the global alkaline electrolyzer market, driving the development of clean hydrogen infrastructure. Meanwhile, Africa’s market is growing rapidly, with electrolyzer capacity increasing from 214 MW in 2022 to 385 MW by 2024. Yet, 2025’s 10.6 GW manufacturing capacity exceeds demand, driving exports and rapid project deployment.

Key Industry?Highlights:

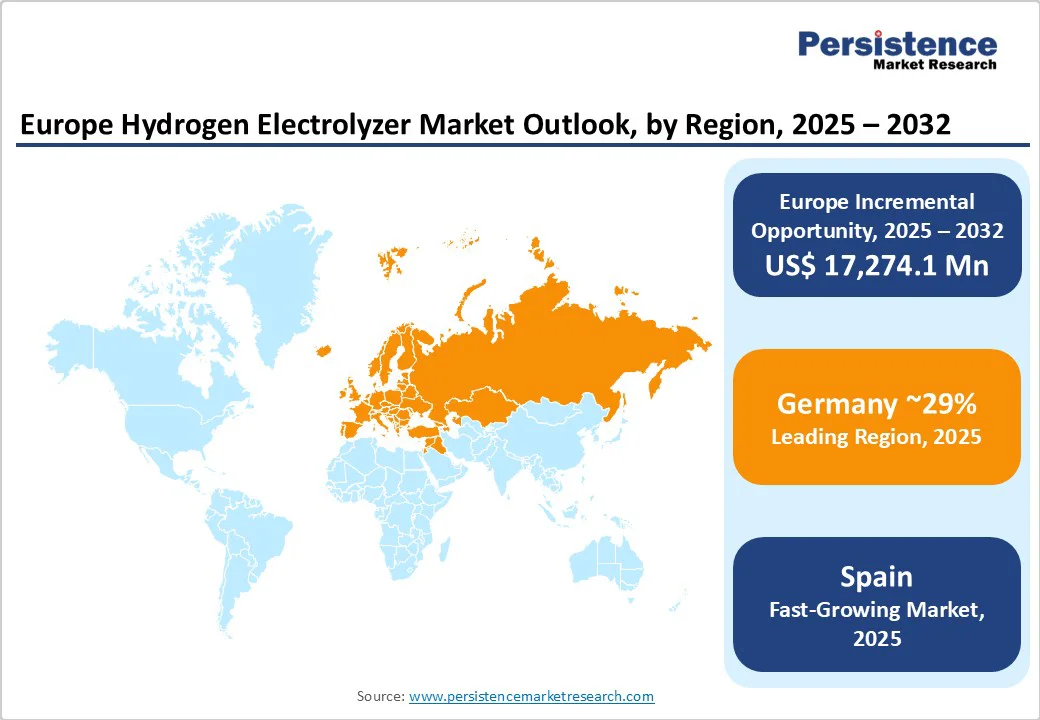

- Leading Country: Germany holds a 27.6% share of Europe’s electrolyzer market, leading the region with strong policy support and advanced industrial infrastructure.

- Fastest-growing Country: Spain holds a 12% market share, showcasing rapid growth driven by abundant renewable resources and active participation in strategic IPCE.

- Dominant Technology Type: Alkaline Electrolyzer dominates the European market with 44% market share in 2025, driven by cost-effectiveness and proven scalability for large industrial applications.

- Leading Power Rating Type: The below 500 kW segment holds a 40% share in 2025, dominating Europe’s electrolyzer market by supporting distributed hydrogen production for industry, mobility, and grid services.

| Key Insights | Details |

|---|---|

|

Europe Hydrogen Electrolyzer Market Size (2025E) |

US$774.5 Mn |

|

Market Value Forecast (2032F) |

US$18,048.6 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

27.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

56.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Europe Green Deal Implementation and Regulatory Framework

Europe’s regulatory frameworks are key drivers of electrolyzer adoption, setting binding targets and financial incentives to scale hydrogen infrastructure. The Alternative Fuel Infrastructure Regulation (AFIR) requires hydrogen refueling stations every 200 km by 2030, ensuring consistent demand. Germany’s €9 billion National Hydrogen Strategy aims for 10 GW capacity by 2030, while the revised Industrial Emissions Directive eases compliance for electrolyzers producing under 50 tons/day. The EU’s Net Zero Industry Act targets 100 GW electrolyzer capacity by 2030, complemented by national goals such as France’s 4.5 GW by 2030 and 8 GW by 2035. Collectively, these policies foster investor confidence and enable industrial-scale hydrogen project deployment.

Industrial Decarbonization Requirements

Europe’s industrial sectors are under increasing pressure to decarbonize, driving strong electrolyzer demand for green hydrogen production. The steel industry alone consumes 50–80 kg of hydrogen per ton of steel, with hydrogen-based direct reduction cutting emissions from 2,000 kg to under 400 kg CO? per ton. Chemical and petrochemical industries, accounting for 44% of end-user demand in 2025, use hydrogen for ammonia, methanol, and refining, with refineries needing around 30,000 tons annually for decarbonization. The EU Emissions Trading System’s carbon pricing enhances competitiveness, with green hydrogen expected to reach parity once prices exceed €60 per ton of CO2.

Renewable Energy Integration and Grid Stability

Electrolyzer systems provide essential grid balancing services as Europe scales renewable electricity generation, converting excess capacity into storable hydrogen. Wind and solar integration necessitate flexible energy storage solutions, with electrolyzers reducing curtailment losses by 30% in 2023. The technology enables power-to-gas applications, facilitating seasonal energy storage and grid stabilization during renewable intermittency periods. Europe's electricity generation increasingly relies on variable renewable sources, creating a systematic demand for technologies capable of utilizing surplus generation.

Barrier Analysis - High Capital Investment Requirements

Electrolyzer deployment faces significant financial barriers, with PEM electrolyzer systems costing up to 40% more than alkaline alternatives, deterring smaller utilities and industrial players. Capital expenditure ranges from €1,666/kW (US$1,800/kW) for alkaline systems to €1,970/kW (US$2,130/kW) for PEM technology, creating investment hurdles for medium-scale applications. Around 60% of European enterprises cited budget constraints as barriers to expanding electrolyzer capacity in 2023, limiting market penetration among smaller operators and creating fragmented adoption patterns across industrial sectors.

Technical and Operational Challenges

Electrolyzer technology faces durability and efficiency constraints that impact commercial viability and operational performance. PEM systems require expensive materials, including platinum and iridium, increasing production costs and limiting scalability. Manufacturing capacity utilization remains low, with actual electrolyzer output reaching only 2.5 GW despite 25 GW/year global manufacturing capacity. Technical limitations in high-pressure applications and efficiency concerns have delayed large-scale electrolyzer projects by 12 months in 2023, while skilled workforce shortages affect 70% of manufacturers across European operations.

Opportunity Analysis - Large-Scale Industrial Hydrogen Hubs

Europe’s industrial clusters offer major potential for large-scale electrolyzer deployment, fostering economies of scale and integrated hydrogen value chains. These hubs aim to replace fossil-based hydrogen in refineries, chemical plants, and steel facilities, such as the Normandy industrial basin’s 200 MW electrolyzer project serving multiple industries. Spain’s hydrogen valleys, totaling 425 MW across five projects, further highlight regional ecosystem growth. By integrating hydrogen production, storage, and end use, such initiatives cut transport and infrastructure costs. IPCEI funding support covering up to 100% of project funding gaps also enhances financial viability and accelerates large-scale industrial adoption.

Cross-Border Hydrogen Trade Infrastructure

Europe’s developing hydrogen backbone is set to boost international trade and optimize production across member states. The Europe Hydrogen Backbone plans 9,040 km of pipelines by 2032, linking production hubs with demand centers. Cross-border trade reached 18.21 kt in 2024, signaling early integration. Import infrastructure will enable access to low-cost renewable hydrogen from regions such as Latin America, capable of producing over 7 MTPA with <3? Kg CO2-eq/kg by 2030. Europe’s electrolyzer manufacturing, leading in alkaline and PEM technologies, can serve both domestic and global markets.

Category-wise Analysis

Technology Insights

Alkaline electrolyzers are expected to dominate the European market in 2025, capturing a 44% share due to their cost-effectiveness and proven scalability for large industrial applications. With lower capital expenditure at €1,666/kW (US$1,944/kW) compared to PEM alternatives, alkaline technology is ideal for megawatt-scale hydrogen production. Recent improvements in electrode materials and system design have enhanced efficiency and durability, exemplified by Thyssenkrupp Nucera’s 740 MW project for green steel production. Its ability to handle variable loads and intermittent renewable energy supports broad adoption across European industrial sectors.

Proton Exchange Membrane (PEM) electrolyzers, the fastest-growing segment in 2025, are valued for their dynamic response and flexibility in renewable energy integration. PEM systems are suited for applications requiring rapid start-up and shutdown cycles, crucial for renewable-powered operations. Key deployments include BASF’s 54 MW system producing 8,000 metric tons of green hydrogen annually and Air Liquide’s 200 MW Normand’Hy project targeting 28,000 tons. Compact and flexible, PEM technology is well-suited for distributed hydrogen production and mobility applications.

Power Rating Insights

The below 500 kW segment holds the largest share in Europe’s electrolyzer market in 2025, accounting for 40% of deployments. This category caters to distributed hydrogen production for industrial processes, mobility infrastructure, and grid balancing. Its low capital requirements and operational flexibility enable wider adoption across diverse end-users and emerging regions.

The 500 kW–2 MW segment is the fastest-growing power category, capturing 27% of the market in 2025. Optimized for mid-scale industrial applications, it balances economic efficiency with renewable energy integration. Projects such as Cummins’ 5 MW PEM electrolyzer in Bavaria, producing 2.2 tons of green hydrogen daily, highlight its suitability for regional hydrogen supply chains and industrial decarbonization.

End-user Industry Insights

The energy & utilities sector represents the leading segment with 43% market share in 2025, driven by grid balancing requirements and renewable energy integration applications. Utility companies deploy electrolyzers for power-to-gas applications, seasonal energy storage, and grid stability services during renewable intermittency periods. The sector's growth is supported by regulatory frameworks requiring renewable energy integration and carbon emission reductions across Europe's power systems.

Steel & Metal Processing emerges as the fastest-growing end-user segment in 2025, driven by industrial decarbonization mandates and green steel production initiatives. Hydrogen-based direct reduction technology can reduce steel production emissions from over 2,000 kg to below 400 kg CO? per ton, creating substantial hydrogen demand across Europe steel manufacturing. Projects such as H2 Green Steel's deployment of over 700 MW of alkaline electrolyzers for Europe's first large-scale green steel plant demonstrate the sector's transformation potential and the growth trajectory of electrolyzer demand.

Country Insights

Germany Market Trends

Germany is anticipated to hold 27.6% of Europe’s electrolyzer market in 2025, asserting leadership through robust policy frameworks and advanced industrial infrastructure. The country has installed over 5 GW of electrolyzer capacity, with plans to reach 10 GW by 2030, supported by the National Hydrogen Strategy’s €9 billion (US$10.5 billion) funding. The Federal Network Agency has approved a hydrogen core grid of 9,040 km to be completed by 2032, establishing a systematic distribution network for electrolyzer-produced hydrogen. Industrial demand from chemical, steel, and refining sectors further drives deployment, exemplified by BASF’s 54 MW PEM electrolyzer at Ludwigshafen, producing 8,000 metric tons annually.

Germany’s Hydrogen Acceleration Act designates hydrogen infrastructure as nationally important through 2045, streamlining approvals and accelerating project timelines. Combined with technological leadership in electrolyzer manufacturing, led by companies such as Siemens Energy and Thyssenkrupp Nucera, the country is well-positioned to maintain market dominance. Its integrated approach of policy support, industrial demand, and technological innovation ensures Germany remains a central hub for Europe’s hydrogen transition.

Spain Market Trends

Spain is expected to capture 12% of the European electrolyzer market in 2025, fueled by abundant renewable resources and strategic IPCEI initiatives. Under IPCEI Hy2Use, the country has committed €524?Million (US$613?Million) to five renewable hydrogen projects totaling 425?MW of electrolyzer capacity, targeting 55,200 tons of green hydrogen annually. Spain’s hydrogen roadmap aims for 4?GW of electrolyzer capacity by 2030, focusing on industrial decarbonization and maximizing renewable energy utilization.

Key projects include Repsol’s 100?MW electrolyzer in Cartagena, producing 15,000 tons of green hydrogen annually with a €300?Million (US$351?Million) investment. Spain’s abundant wind and solar resources enable cost-competitive hydrogen production, supporting export strategies and the development of regional hydrogen hubs across Andalusia, Asturias, and other industrial regions.

Netherlands Market Trend

The Netherlands holds 7% of the European electrolyzer market, emphasizing hydrogen import infrastructure and port-based production facilities. The government awarded RWE a €551?Million (US$645?Million) grant for a 100?MW electrolyzer at Eemshaven, powered by offshore wind, to support industrial decarbonization. A 4% renewable hydrogen mandate for industry by 2030 ensures steady demand for electrolyzer-produced hydrogen.

Strategic port development positions the Netherlands as a European hydrogen import and distribution hub, exemplified by Air Liquide’s ELYgator project in Rotterdam, producing 23,000 tons of renewable hydrogen annually. The integration of electrolyzers with offshore wind farms, such as the OranjeWind project, highlights advanced renewable energy utilization and grid-balancing capabilities.

Competitive Landscape

The Europe hydrogen electrolyzer market is largely oligopolistic, dominated by a few key players with extensive manufacturing capacity, advanced technology portfolios, and strong regional project pipelines. Leading companies, including Thyssenkrupp Nucera, Nel ASA, Siemens Energy, John Cockerill Hydrogen, Plug Power Inc., and McPhy Energy S.A., benefit from strategic partnerships and government-supported hydrogen initiatives.

These firms are scaling gigawatt-level production, optimizing alkaline, PEM, and SOEC technologies, and localizing supply chains to meet EU sustainability goals. While the market’s upper segment remains concentrated among these leaders, smaller developers and start-ups drive innovation in efficiency, modularity, and cost reduction, creating a dynamic balance between consolidation and technological diversification across Europe’s growing electrolyzer industry.

Key Industry Developments

- In May 2025, Thyssenkrupp Nucera and Fraunhofer IKTS launched an 8 MW/year SOEC pilot plant in Arnstadt, Germany, advancing high-temperature electrolysis, cutting electricity use by 20–30%, and converting industrial CO? into green synthesis gas, strengthening Europe’s hydrogen technology leadership.

- In September 2025, John Cockerill Hydrogen and IRT M2P launched two advanced electrolysis test benches in Metz, France, under the IPCEI Hy2Tech program, enhancing Europe’s hydrogen R&D capabilities and accelerating innovation for large-scale renewable hydrogen deployment.

Companies Covered in Europe Hydrogen Electrolyzer Market

- Siemens Energy

- Thyssenkrupp Nucera

- Nel Hydrogen Electrolyser AS

- ITM Power

- John Cockerill Hydrogen

- McPhy Energy

- Enapter

- Green Hydrogen Systems

- Cummins Inc.

- Plug Power Inc.

- Air Liquide

- Linde

- ENGIE

- Ballard Power Systems

- Elogen

Frequently Asked Questions

The Europe hydrogen electrolyzer market is projected to be valued at US$774.5 Mn in 2025.

Alkaline electrolyzers are expected to hold 44% market share in 2025, remaining the leading technological segment due to their proven maturity and cost-effectiveness.

The Europe hydrogen electrolyzer market is poised to witness a CAGR of 56.8% from 2025 to 2032.

The Europe hydrogen electrolyzer market growth is driven by strong regulatory support, industrial decarbonization mandates, and the need for renewable energy integration and grid stability.

Key opportunities in Europe’s hydrogen electrolyzer market include industrial hydrogen hubs, regional hydrogen valleys, and cross-border trade infrastructure with pipelines and import access to low-cost renewable hydrogen.

The top key market players in the global Europe hydrogen electrolyzer market include Thyssenkrupp Nucera, Siemens Energy, Nel ASA, John Cockerill Hydrogen, Plug Power, and ITM Power.