- Nutraceuticals & Functional Foods

- Health Food Ingredient Market

Health Food Ingredient Market Size, Share, and Growth Forecast, 2026 - 2033

Health Food Ingredient Market by Source (Plant, Animal, Microbial), Form (Dry, Liquid), Product Type (Protein, Vitamin, Mineral, Biotics), Application (Food & Beverage, Pharmaceutical, Diet Supplement, Feeds), and Regional Analysis 2026 - 2033

Health Food Ingredient Market Share and Trends Analysis

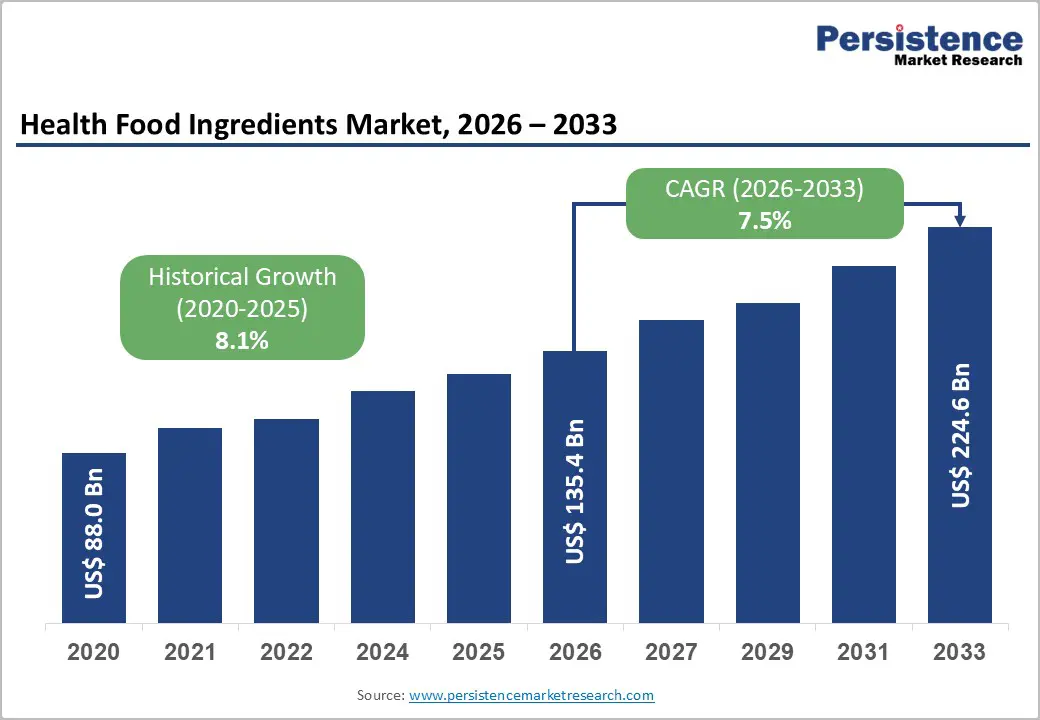

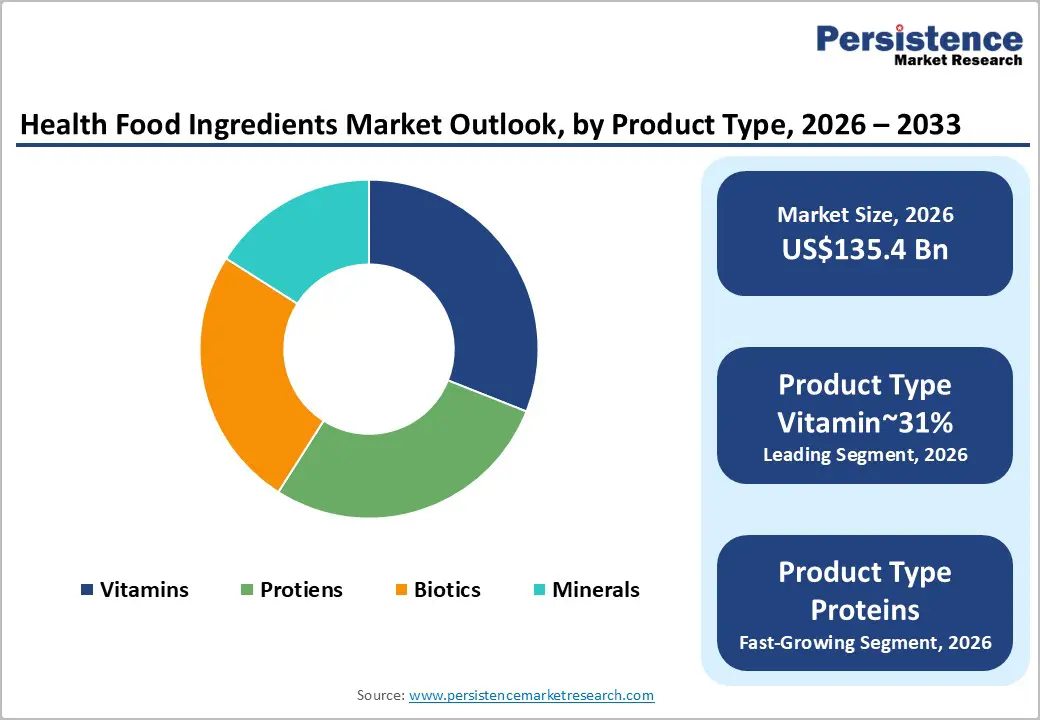

The global health food ingredient market size is likely to be valued at US$135.4 billion in 2026 and is expected to reach US$224.6 billion by 2033, growing at a CAGR of 7.5% during the forecast period from 2026 to 2033, driven by the structural shift in consumer behavior toward preventive healthcare and nutritionally optimized diets worldwide.

Advances in precision fermentation and biotechnology are enabling manufacturers to develop high-efficacy bioactive compounds with enhanced bioavailability, aligning with the demands of the clean-label movement. The pharmaceutical and animal feed segments are witnessing particularly rapid adoption, with probiotics in animal feed expected to grow amid regulatory initiatives to phase out antibiotic growth promoters.

Key Industry Highlights:

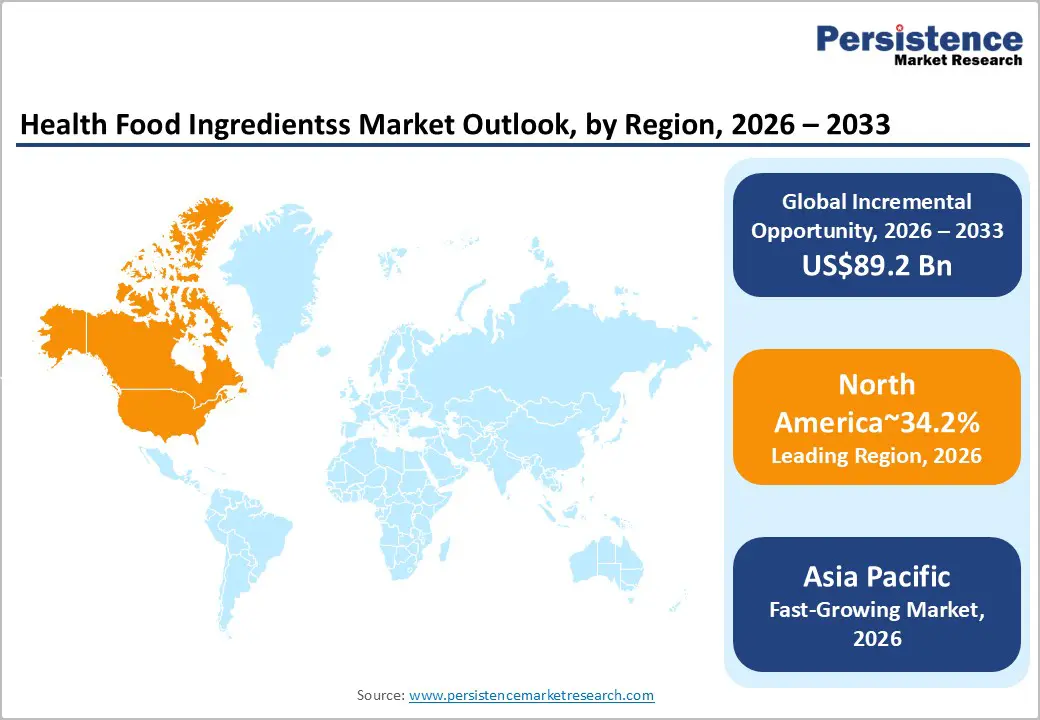

- Leading Region: North America is projected to lead the health food ingredient market, with a 34.2% share in 2026, driven by urbanization, a growing middle class, and government-backed health initiatives that boost adoption across food, supplements, and pharmaceuticals.

- Leading Source Segment: The plant-based ingredient segment is projected to remain the leading segment, capturing approximately 62% of total market share, driven by ongoing demand for sustainable, allergen-free, and environmentally efficient nutritional solutions.

- Leading Product Type Segment: Vitamins are expected to dominate the functional category in 2026, holding a 31% market share, supported by their regulatory importance, formulation flexibility, and well-established use in mass-market fortification.

- Key Industry Developments: The health food ingredient market is undergoing consolidation through strategic mergers, acquisitions, and portfolio realignments. In November 2024, OmniActive acquired ENovate Biolife to broaden its portfolio of clinically validated botanical health ingredients.

| Key Insights | Details |

|---|---|

|

Health Food Ingredient Market Size (2026E) |

US$135.4 Bn |

|

Market Value Forecast (2033F) |

US$224.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.1% |

Market Dynamics - Growth, Barrier, and Opportunity Analysis

Preventive Healthcare Paradigm and Consumer Health Consciousness

The preventive healthcare paradigm is increasingly positioning health food ingredients as structural components of mainstream nutrition rather than discretionary additives. The rising global incidence of metabolic and lifestyle-related disorders is increasing demand for functional foods aligned with disease-prevention strategies promoted by multilateral health bodies.

Consumer understanding of diet–health linkages, particularly around gut health and metabolic balance, is reshaping purchasing behaviour across food, beverage, and supplement categories, elevating bioactive ingredients into core formulation requirements.

This shift is translating into measurable economic signals across the value chain. Health-oriented formulations are sustaining pricing premiums without demand compression, indicating a durable willingness to pay for preventive benefits. Ingredient demand is further reinforced by diversification of applications, as functional fortification extends beyond supplements to mass-market food platforms.

Regulatory alignment around wellness, clean-label positioning, and nutritional efficacy is intensifying this momentum, structurally anchoring preventive nutrition as a long-term market driver rather than a cyclical trend.

High Cost of Premium Natural Ingredients

Elevated input costs remain a structural restraint across the health food ingredients market, particularly for premium natural and organic compounds. High-purity botanical and bioactive ingredients rely on labor-intensive extraction, specialized processing, and certified raw material sourcing, structurally inflating production costs relative to synthetic alternatives.This cost differential limits penetration in price-sensitive markets, where affordability continues to influence formulation decisions despite rising health awareness.

Cost pressures are further amplified by agricultural commodity price volatility, increasingly shaped by climate variability and supply-side disruptions. Margin compression persists as manufacturers absorb higher procurement expenses while facing resistance to downstream price increases.

These dynamics constrain scalability, particularly for smaller suppliers with limited hedging or vertical integration capabilities, and reinforce market unevenness where scale, sourcing resilience, and process efficiency increasingly determine competitive viability.

Personalized Nutrition and Nutrigenomics

The convergence of digital health infrastructure with nutrition science is unlocking a structurally significant opportunity in personalized nutrition. Increasing adoption of wearables, continuous biomarker monitoring, and genetic testing is shifting consumer expectations from generalized wellness to precision-aligned dietary interventions.

This evolution is repositioning nutrigenomics from a niche research domain into a commercially scalable market, with demand increasingly anchored in measurable metabolic optimization rather than lifestyle positioning alone.

Commercial upside is concentrated among ingredient suppliers capable of enabling modularity and customization at scale. Targeted probiotic strains, condition-specific micronutrient blends, and adaptable premix platforms are positioned to integrate directly with health-tech ecosystems, enabling personalized formulation delivery.

Strategic partnerships between ingredient manufacturers and digital health platforms are therefore becoming a critical route to market, reinforcing differentiation through data-driven efficacy, repeat engagement models, and higher switching costs across the personalized nutrition value chain.

Category–wise Analysis

Source Insights

The plant-based ingredient segment is expected to remain the leading contributor, accounting for approximately 62% of the total market share in 2026, supported by sustained demand for sustainable, allergen-free, and environmentally efficient nutrition solutions.

Functional equivalence to animal proteins, improving sensory performance, and broad regulatory acceptance continue to reinforce adoption across food and beverage platforms. Pea protein is expected to retain its structural leadership among plant-based proteins due to its balanced amino acid profile and formulation flexibility, whereas soy protein is projected to experience gradual share dilution as manufacturers diversify sourcing strategies to mitigate GMO-related perception risks and portfolio concentration.

Pea protein has solidified its role as a leading plant-based protein source due to its balanced amino acid profile and high digestibility. It is increasingly used in "clean label" products that avoid the top nine allergens (soy, dairy, gluten). Ripple Plant-Based Milk is a prime example of functional equivalence, utilizing a proprietary pea protein blend to provide 8g of protein per cup, matching the protein content of dairy milk.

It also offers 50% more calcium. The 2026 organic line takes this a step further by streamlining the ingredient list to just five, addressing growing consumer demands for sustainability and transparency.

The animal-based ingredients segment is projected to be the fastest-growing and is likely to remain important in applications requiring proven bioavailability and functional performance. Egg protein remains a dominant functional ingredient.

It is highly valued for its bioavailability and versatility in dietary supplements, sports drinks, and baked goods, supporting bone strength and overall growth. Whey and milk proteins are the primary beneficiaries of the protein trend in 2026.

Whey protein is currently one of the fastest-growing segments due to its rapid absorption, making it a gold standard for post-workout recovery and muscle tissue repair. Dairy proteins such as casein and whey are also vital for "healthy aging" products aimed at preventing sarcopenia in older adults.

Animal-sourced lipids, particularly EPA and DHA from fish oil, are critical for cardiometabolic health and cognitive function. Bioactive peptides derived from the hydrolysis of animal products are increasingly used for their antihypertensive, antioxidant, and immunomodulatory properties.

Product Type Insights

Vitamins are projected to be the leading functional category with a 31% market share in 2026, anchored by their regulatory relevance, formulation versatility, and entrenched role in mass-market fortification. Their dominance is structurally reinforced by mandatory inclusion across staple foods and sustained demand from beauty-from-within and preventive nutrition applications.

Product development is increasingly focused on liposomal delivery systems for vitamins C and D to preserve bioavailability during thermal processing, alongside hybrid topical-to-oral concepts that integrate vitamin E and B-complex vitamins into coordinated ingestible and cosmetic routines.

Industrial momentum is shifting toward precision fortification platforms that dynamically calibrate vitamin premixes at scale, supported by microbial fermentation routes for B-vitamins to satisfy natural-label requirements. From a market trend perspective, vitamins are transitioning from episodic immune use toward permanent integration into everyday staples such as flour, rice, and plant-based beverages, particularly within public health-driven emerging economies.

Amino acids are poised to be the fastest-growing functional category, driven by the rise of active lifestyles and the need to improve protein quality in plant-based nutrition. Innovation is shifting from traditional powders to clear EAA (Essential Amino Acid) recovery waters and targeted amino acid sachets designed to address limiting amino acid profiles in legume-based diets, with a focus on leucine-centric formulations.

Industrial advancements are centered on enzymatic hydrolysis technologies to produce rapidly absorbed bioactive peptides, as well as upcycled extraction methods that source amino acids from food-processing byproducts, enhancing both cost efficiency and sustainability.

One example is MuscleBlaze BCAA Gold, an Indian brand marketed as a high-leucine formulation to support faster muscle protein synthesis and recovery, often used as an intra-workout drink. Beyond supplements, Indian nutrition promotes "Complete Protein Combos" such as Dal + Rice (combining lysine from dal and methionine from rice) or Khichdi, which naturally balance the amino acid profile for those following vegetarian diets.

Regional Insights

North America Health Food Ingredient Market Trends

North America is expected to lead, accounting for an estimated 34.2% market share in 2026, with the U.S. serving as the primary engine of growth. The region’s expansion is underpinned by a sophisticated innovation ecosystem, where venture capital and private equity flow into alternative proteins, functional ingredient startups, and AI-driven formulation platforms reinforce technological leadership.

Regulatory evolution, including the FDA’s 2025 revision of the “healthy” definition, is projected to accelerate product reformulation toward higher nutrient density, creating structural demand for fortified snacks, beverages, and convenience-oriented functional foods. The region’s market consolidation enables major suppliers to leverage scale, R&D capacity, and integrated supply chains to sustain competitive advantage while mitigating entry barriers for smaller players.

Consumer behavior in North America is heavily oriented toward functional convenience, personalized nutrition, and preventative wellness, which is expected to support ongoing adoption across food, beverage, and dietary supplement channels.

Investment in digital traceability, clean-label verification, and clinical substantiation further reinforces the region’s market credibility. Combined with mature distribution infrastructure and high-income consumer segments, these factors position North America to maintain structural market dominance, sustain pricing premiums, and continue leading innovation in bioactive, plant-based, and fortified health ingredient applications.

Europe Health Food Ingredients Market Trends

Europe is expected to remain the second-largest regional market, with Germany, the U.K., and France leading in revenue contribution and innovation adoption. The market is structurally shaped by regulatory harmonization under the EFSA, which enforces some of the world’s strictest health claim and novel food standards, reinforcing scientific substantiation as a market prerequisite.

Germany is projected to maintain leadership within Europe, with health and wellness foods expanding at a high CAGR, supported by strong consumer preference for organic and clean-label products, environmental consciousness, and premium positioning. EU sustainability frameworks, including the Deforestation Regulation and Green Deal initiatives, are structurally reinforcing the adoption of upcycled, plant-based, and circular-economy-aligned ingredients across food, beverage, and animal feed applications.

Regulatory stringency and sustainability mandates are expected to continue driving structural demand for transparent and traceable supply chains, favoring suppliers with demonstrable ESG compliance and innovation in meat and dairy alternatives. Growth opportunities are projected to concentrate in premium, sustainability-differentiated botanical extracts, functional ingredients targeting aging populations, and microbiome-supportive products.

Regional consolidation, evidenced by €3.87 billion (US$$4.6 billion) in 2025 M&A activity, is reinforcing competitive positioning, creating an innovation-driven, high-compliance environment that underpins long-term strategic stability across the European health food ingredient landscape.

Asia Pacific Health Food Ingredient Market Trends

Asia Pacific is projected to remain the fastest-growing regional market, with China, Japan, and India serving as the primary growth engines. China’s “Healthy China 2030” policy is expected to accelerate fortified staple food production and functional food adoption, while rapid urbanization and rising disposable incomes are driving premium ingredient demand.

India’s market expansion is structurally supported by preventive healthcare awareness and the integration of Ayurvedic ingredient knowledge with modern nutritional science, enabling broader consumption of functional and botanical products.

Japan’s aging population is anticipated to sustain demand for ingredients addressing bone health, cognitive function, and immunity, positioning the country as a regional hub for senior-focused functional innovations. Lower production costs, raw material proximity, and manufacturing scale advantages are reinforcing Asia Pacific’s competitiveness as a global ingredient processing hub.

Regulatory evolution across the region is gradually aligning with international food safety and clean-label standards, creating structural incentives for compliance-driven suppliers. Mandatory traceability systems in China and government support for AYUSH ingredient standardization in India are enhancing market entry requirements, favoring capable regional producers.

Investment trends indicate significant foreign direct investment, localized R&D centers, and scaling of personalized nutrition and functional beverage platforms. Combined with intellectual property generated through integrating traditional wellness knowledge and modern validation, these factors are expected to sustain high-volume expansion and competitive pricing advantages across Asia Pacific.

Competitive Analysis

The global health food ingredient market is moderately fragmented, with the top ten players accounting for roughly 40–45% of the total share. Multinationals such as Cargill, ADM, and DSM-Firmenich lead the bulk protein, vitamin, and lipid segments through manufacturing scale, vertically integrated supply chains, and global distribution networks.

Competitive strategies increasingly focus on turnkey solutions that combine formulation support, regulatory guidance, and technical advisory services, rather than solely supplying raw ingredients. Commodity segments such as vitamins and minerals remain highly consolidated, benefiting from scale-driven efficiency and supply reliability.

Specialized categories, botanical extracts, strain-specific probiotics, and indigenous crop ingredients retain a fragmented structure, allowing regional suppliers to capitalize on product specialization and localized sourcing. Strategic differentiation is driven by R&D, functional ingredient innovation, and responsiveness to clean-label, high-value nutrition trends.

Mid-market players such as Glanbia, Kerry, and Lonza target niche segments via probiotics, premixes, and encapsulated delivery systems, while the market continues to see consolidation in commodities and growth in specialty bioactives.

Key Industry Developments:

- In November 2025, The Hershey Company finalized its acquisition of LesserEvil, strengthening its portfolio of organic and mindful snacking options under the “Better-For-You Snacking” segment.

- In September 2025, DSM-Firmenich unveiled new health-focused rice fortification technology to combat global "hidden hunger" on a major scale.

- In March 2025, PepsiCo entered into a definitive agreement to acquire prebiotic soda brand Poppi for US$1.95 billion to bolster its "better-for-you" portfolio.

Companies Covered in Health Food Ingredient Market

- Archer Daniels Midland Company

- DSM-Firmenich

- Kerry Group plc

- BASF SE

- Ingredion Incorporated

- Tate & Lyle plc

- Glanbia plc

- Arla Foods Ingredients

- Corbion NV

- Lonza Group Ltd. (Switzerland)

- International Flavors & Fragrances

- Chr. Hansen

- Naturex

- Asahi Group Foods

- ICL Group Ltd.

- Arla Foods Group

- Carbery Food Ingredients Limited

Frequently Asked Questions

The global health food ingredient market is projected to be valued at US$135.4 billion in 2026 and is expected to reach US$224.6 billion by 2033.

Global demand for health food ingredients is rising due to the growing focus on preventive healthcare, increased consumption of fortified and functional foods, and innovations in precision fermentation that allow the production of highly effective bioactive compounds.

The health food ingredient market is expected to grow at a CAGR of 7.5% between 2026 and 2033, reflecting sustained structural demand across food, pharmaceutical, and feed applications.

The strongest growth opportunities are emerging in Asia Pacific, supported by urbanization, expanding middle-income populations, and government-backed health and nutrition initiatives in China and India.

Key players include Archer Daniels Midland, DSM-Firmenich, Kerry Group, BASF, Ingredion, Tate & Lyle, Glanbia, Arla Foods Ingredients, Corbion, Lonza Group, IFF, Chr. Hansen, and Naturex.