- Industrial Machinery

- Dry Vacuum Pumps Market

Dry Vacuum Pumps Market Size, Share, and Growth Forecast for 2025 - 2032

Dry Vacuum Pumps Market By Product Type (Dry Screw Vacuum Pump, Dry Scroll Vacuum Pump, Others), Cooling Capacity (Low Capacity (Up to 100 m³/h), Others), and Regional Analysis for 2025 - 2032

Dry Vacuum Pumps Market Size and Trends Analysis

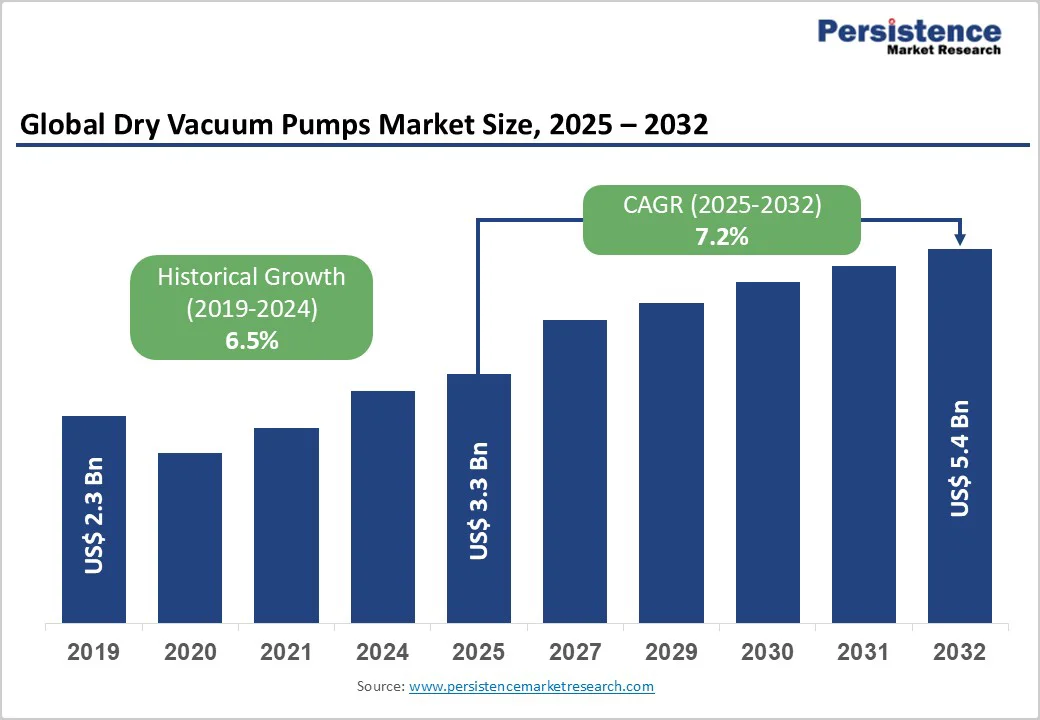

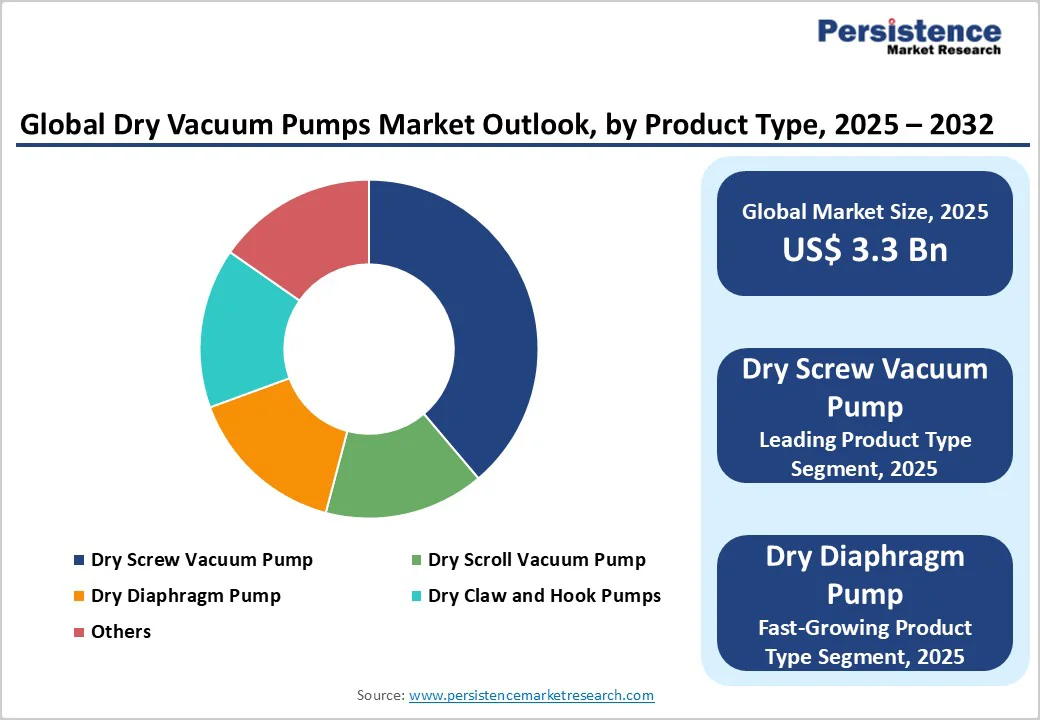

The global dry vacuum pumps market size is likely to be valued at US$3.3 Billion in 2025 and is expected to reach US$5.4 Billion by 2032, growing at a CAGR of 7.2% during the forecast period from 2025 to 2032, driven by the rising demand from semiconductor manufacturing, pharmaceutical production, and clean energy applications, alongside technological advancements enhancing efficiency and contamination control.

Key Industry Highlights:

- Regional Leaders: Asia Pacific dominates the dry vacuum pumps market with over 70% of global advanced semiconductor manufacturing capacity.

- Leading Product Type: Dry screw vacuum pumps command the largest market share at approximately 35% of the total dry pump market value, driven by superior pumping speeds and deep vacuum capabilities.

- Fastest Growing Capacity: Medium-capacity dry pumps (100-500 m³/h) represent the fastest-growing capacity segment, expanding at 7.5% CAGR due to their optimization for mid-size semiconductor facilities.

- Market Driver: The semiconductor industry is the most significant demand driver for dry vacuum pumps globally, accounting for approximately 32% of the market in 2024.

- Market Opportunity: Electric vehicle battery manufacturing presents the most significant emerging opportunity, with global lithium-ion production capacity targeting 9 TWh by 2030.

| Key Insights | Details |

|---|---|

| Dry Vacuum Pumps Market Size (2025E) | US$3.3 Bn |

| Projected Market Value (2032F) | US$5.4 Bn |

| Global Market Growth Rate (CAGR 2025 to 2032) | 7.2% |

| Historical Market Growth Rate (CAGR 2019 to 2024) | 6.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Semiconductor Industry Expansion and Advanced Chip Manufacturing

The semiconductor industry is the most significant driver of global demand for dry vacuum pumps, accounting for approximately 32% of the total vacuum dry pump market share in 2024.

Modern semiconductor fabrication facilities require sophisticated vacuum environments for critical processes, including lithography, deposition, etching, and ion implantation. Each 200 mm semiconductor wafer fabrication facility typically installs around 600 essential vacuum pumps, while advanced 300 mm extreme ultraviolet (EUV) fabs can install over 5,000.

The rapid expansion of chipmaking capacity for artificial intelligence accelerators and high-bandwidth memory (HBM) technologies sustains robust capital equipment spending beyond traditional semiconductor industry cycles.

Dry vacuum pumps offer superior contamination control compared to oil-sealed alternatives, making them essential for achieving the stringent cleanroom standards and process-purity requirements required for nanometer-scale semiconductor production.

Rapid Urbanization and Rising Cooling Demand in Emerging Economies

Emerging economies across the Asia Pacific, Latin America, and Africa are experiencing unprecedented urbanization rates and expanding middle-class populations requiring residential cooling infrastructure. According to United Nations projections, approximately 68% of the global population will reside in urban areas by 2050, compared to 55% in 2018.

In China, urban population growth coupled with rising disposable incomes has driven residential air conditioning penetration from 45% of households in 2015 to over 72% by 2024. India's burgeoning middle class, projected to grow to 250 million by 2030, is driving explosive demand for residential cooling systems, with air conditioning ownership expected to grow at 15-20% annually.

The expansion of commercial refrigeration infrastructure in supermarkets, cold storage facilities, and pharmaceutical warehouses is concurrently accelerating compressor demand. The Asia Pacific cold chain logistics market is projected to expand at a high CAGR through 2032, driven by e-commerce growth in food delivery and pharmaceutical distribution, which require reliable, temperature-controlled infrastructure.

Compressor manufacturers are ramping up capacity in high-growth regions to capitalize on sustained demand growth.

Barrier Analysis - High Capital Investment and Technological Complexity

Dry vacuum pumps represent a significant capital expenditure for manufacturers, with initial equipment costs sometimes representing over 5% of total fabrication facility equipment investments in semiconductor manufacturing.

The technological complexity required for installation, operation, and troubleshooting necessitates specialized engineering knowledge and workforce training, creating adoption barriers for smaller manufacturers and emerging industrial facilities.

Maintenance protocols demand precise technical expertise, and pump sizing errors can result in suboptimal performance or failure to maintain required vacuum levels, particularly in demanding applications involving condensable vapors or corrosive process gases.

Competition from Established Oil-Sealed Pump Technology

Oil-sealed vacuum pumps maintain a substantial market presence and competitive advantages in specific applications where dry-pump technology faces limitations, such as handling high moisture levels or particulate contamination.

These conventional systems benefit from decades of established market presence, customer familiarity, and lower initial acquisition costs compared to advanced dry pump systems. Industries with less stringent contamination requirements continue to prefer oil-sealed alternatives due to their lower purchase price, extended service intervals, and proven operational reliability in less demanding applications.

Opportunity Analysis - Electric Vehicle Battery Manufacturing and Energy Storage Applications

The global battery production market presents exceptional growth opportunities for dry vacuum pump manufacturers, with battery plants projected to represent the fastest-expanding application segment. Battery cell manufacturing processes, including anode coating, cathode preparation, electrolyte filling, and vacuum-drying operations, all require oil-free pumps to prevent solvent inclusions that degrade lithium-ion cell performance and longevity.

Global lithium-ion battery production capacity expansion toward 9 terawatt-hours (TWh) by 2030 creates substantial demand for dedicated vacuum systems. Vacuum impregnation processes for electric motor winding insulation enhancement also generate significant demand, particularly as automotive manufacturers invest heavily in electric vehicle drivetrain development and next-generation battery technologies.

Industry 4.0 Integration and IoT-Enabled Smart Vacuum Systems

The integration of Internet of Things (IoT) technologies and artificial intelligence with vacuum pump systems represents a significant market opportunity for equipment manufacturers and technology providers.

Smart vacuum pumps equipped with real-time monitoring sensors, predictive analytics algorithms, and remote operational control capabilities enable manufacturers to optimize energy consumption, predict equipment failures before occurrence, and minimize production downtime. IoT-connected systems can reduce energy consumption by up to 20% through intelligent speed control and variable speed drive optimization.

Digital integration with Industry 4.0 manufacturing frameworks allows seamless data exchange across production systems, enabling coordinated optimization of vacuum conditions with upstream deposition or etching processes, particularly valuable for semiconductor and pharmaceutical manufacturing, where process precision directly impacts product quality.

Category-wise Analysis

Product Type Insights

Dry screw vacuum pumps represent the dominant product segment within the dry vacuum pumps market, commanding approximately 35% market share based on 2024 industry data.

These pumps deliver superior performance in demanding industrial applications requiring high pumping speeds and deep vacuum levels essential for semiconductor fabrication, chemical processing, and metallurgical operations. Dry screw technology operates through intermeshing helical rotors that compress gases without requiring sealing fluids, delivering exceptional reliability and energy efficiency compared to alternative technologies.

Their robust design handles corrosive and hazardous gases common in chemical and semiconductor industries, while providing maintenance-intensive intervals estimated at approximately one year between preventive service activities. The technology's maturity, proven track record across multiple industries, and ability to achieve vacuum levels down to 0.01 mbar justify market leadership positioning.

Capacity Insights

Medium capacity pumps (100-500 m³/h) dominate the market with approximately 42% market share, reflecting widespread application across mid-size semiconductor fabrication facilities, pharmaceutical manufacturing operations, and chemical processing plants. This capacity range offers an optimal balance between operational flexibility, energy consumption, and cost-effectiveness for the majority of industrial applications.

Medium-capacity systems accommodate diverse process requirements without excessive oversizing that increases capital expenditure and energy operating costs. They serve as primary backing pumps for turbomolecular and cryo-pump systems in ultra-high vacuum applications, while functioning as sole vacuum sources for rough-to-medium vacuum industrial processes.

The prevalence of 300 mm wafer fabrication facilities utilizing hundreds of medium-capacity pumps across etching, deposition, and environmental chambers drives sustained demand growth in this segment.

Regional Insights

North America Dry Vacuum Pumps Market Trends

North America maintains a substantial market share, driven by pharmaceutical innovation, advanced semiconductor research facilities, and aerospace industry requirements for space simulation and vacuum coating applications. The region hosts major pharmaceutical and biotechnology research centers conducting extensive freeze-drying operations for vaccine development and biopharmaceutical manufacturing.

Regulatory frameworks, including NFPA 99 Health Care Facilities Code compliance requirements, mandate integration of advanced vacuum systems in hospital environments and pharmaceutical sterilization facilities, supporting steady equipment demand.

The aerospace and space exploration sectors represent high-value niche markets, with dry vacuum pump systems essential for spacecraft component testing, vacuum welding operations, and liquid rocket engine performance validation. The U.S. government initiatives supporting commercial space exploration and satellite manufacturing directly increase capital equipment investments for vacuum technology infrastructure.

Leading equipment manufacturers, including Agilent Technologies and Gardner Denver Inc., maintain significant research and development operations in North America, driving innovation in scroll pump technology and contamination management solutions specifically designed for laboratory instrumentation and analytical equipment applications.

Europe Dry Vacuum Pumps Market Trends

Europe represents a mature market with substantial demand from chemical processing, pharmaceutical manufacturing, and precision instrumentation sectors. The region prioritizes environmental sustainability and energy efficiency in compliance with European Union industrial emission directives, driving the adoption of advanced dry pump systems offering reduced carbon footprint and lower power consumption.

Germany, as the industrial heartland of Europe, hosts sophisticated chemical and pharmaceutical manufacturing facilities alongside advanced research institutions, generating consistent demand for precision vacuum equipment.

European manufacturers emphasize quality engineering and product reliability, supporting premium product positioning for brands including Pfeiffer Vacuum GmbH and Busch Group operating from German manufacturing bases.

The region's strict environmental regulations governing air quality, refrigerant management, and industrial emissions standards necessitate investment in clean, sustainable vacuum technologies. Emerging opportunities in freeze-drying and pharmaceutical isolator systems for biopharmaceutical development create expanding demand across pharmaceutical innovation hubs in France, Spain, and the U.K.

Asia Pacific Dry Vacuum Pumps Market Trends

Asia Pacific dominates the market, housing over 70% of advanced semiconductor chip manufacturing capacity concentrated in China, Taiwan, South Korea, and Japan.

The region's semiconductor manufacturing concentration drives exceptional demand, with China's semiconductor dry screw vacuum pumps market valued at 12.24 billion yuan (US$1.68 Billion) in 2025 and expanding at 10.37% CAGR through 2026. Strategic government initiatives to expand indigenous semiconductor fabrication capacity create continuous investment in vacuum technology infrastructure and equipment.

Japan-based manufacturers, including ULVAC and Ebara Corporation, leverage extensive vacuum technology expertise to serve regional semiconductor and pharmaceutical markets, while Chinese manufacturers increasingly compete through localized supply chains and cost advantages.

South Korea and Taiwan host cutting-edge semiconductor fabrication facilities requiring thousands of specialized vacuum pumps annually. India and Southeast Asian countries demonstrate emerging market potential, with expanding electronics manufacturing and increasing biopharmaceutical production capacity driving demand growth in medium-term forecasts.

Competitive Landscape

The global dry vacuum pumps market exhibits moderate consolidation characteristics with approximately the top five manufacturers controlling 40% market share, while numerous regional and specialized competitors maintain niche market positions. Leading global companies, including Atlas Copco AB, Pfeiffer Vacuum GmbH, Ebara Corporation, and Gardner Denver Inc., compete through technological innovation, product portfolio breadth, and global service infrastructure.

Market differentiation strategies emphasize energy efficiency improvements, contamination management capabilities, and Industry 4.0 integration features enabling predictive maintenance and real-time performance monitoring.

Strategic acquisitions consolidate market positions, exemplified by Busch Vacuum Solutions' acquisition of Vac-Tech Inc. in 2023, expanding market reach in semiconductor equipment servicing. Leading companies invest substantially in research and development for next-generation dry pump technologies, magnetic bearing systems, and variable speed drive optimization.

Key Industry Developments

- In January 2025, Agilent Technologies announced the IDP-35 and IDP-45 scroll pump models, expanding laboratory and research instrumentation applications, including scanning electron microscopes, mass spectrometers, and freeze-drying equipment.

- In December 2024, Atlas Copco introduces the DZS A series next-generation dry claw vacuum pumps featuring enhanced performance, energy efficiency, and reduced operational noise through advanced German engineering and cutting-edge machining technology.

- In August 2024, CryoDry establishes a strategic partnership with Pfeiffer Vacuum for freeze-drying applications, integrating premium HiScroll and Duo rotary vane pump models offering exceptional reliability and low noise operation.

Companies Covered in Dry Vacuum Pumps Market

- Agilent Technologies

- Atlas Copco AB

- Bosch Group

- DVP Vacuum

- Ebara Corporation

- Flowserve SIHI GmbH

- Gardner Denver Inc.

- Pfeiffer Vacuum GmbH

- Shanghai EVP Vacuum Technology

- ULVAC

- Busch Vacuum Solutions

- Leybold GmbH

Frequently Asked Questions

The global dry vacuum pumps market was valued at US$3.3 Billion in 2025 and is projected to reach US$5.4 Billion by 2032, representing a compound annual growth rate of 7.2% during the forecast.

Expansion for artificial intelligence chip production, pharmaceutical sector adoption for contamination-free freeze-drying and sterilization processes, and chemical industry demand for handling corrosive materials represent the three primary demand drivers.

Dry screw vacuum pumps command the largest market segment with approximately 35% market share, driven by their superior pumping speeds, deep vacuum capabilities, and robust design for handling corrosive and hazardous gases.

The Asia Pacific region dominates with over 70% of global advanced semiconductor manufacturing capacity concentrated in China, Taiwan, South Korea, and Japan, driving approximately 60-65% of the total market demand.

Electric vehicle battery manufacturing presents the most significant emerging opportunity, with global lithium-ion production capacity targeting 9 terawatt-hours by 2030, requiring specialized dry vacuum systems.

Leading market participants include Atlas Copco AB (Sweden), Pfeiffer Vacuum GmbH (Germany), Ebara Corporation (Japan), Gardner Denver Inc. (U.S.), Agilent Technologies (U.S.), and ULVAC (Japan).