- Metals & Minerals

- Foundry Market

Foundry Market Size, Share, and Growth Forecast, 2025 - 2032

Foundry Market by Metal Type (Ferrous, Non-Ferrous), Casting Process (Sand Casting, Die Casting, Investment Casting, Others), End-user Industry (Automotive, Aerospace & Defense, Construction & Infrastructure, Industrial Machinery, Electronics, Others), and Regional Analysis for 2025 - 2032

Foundry Market Share and Trends Analysis

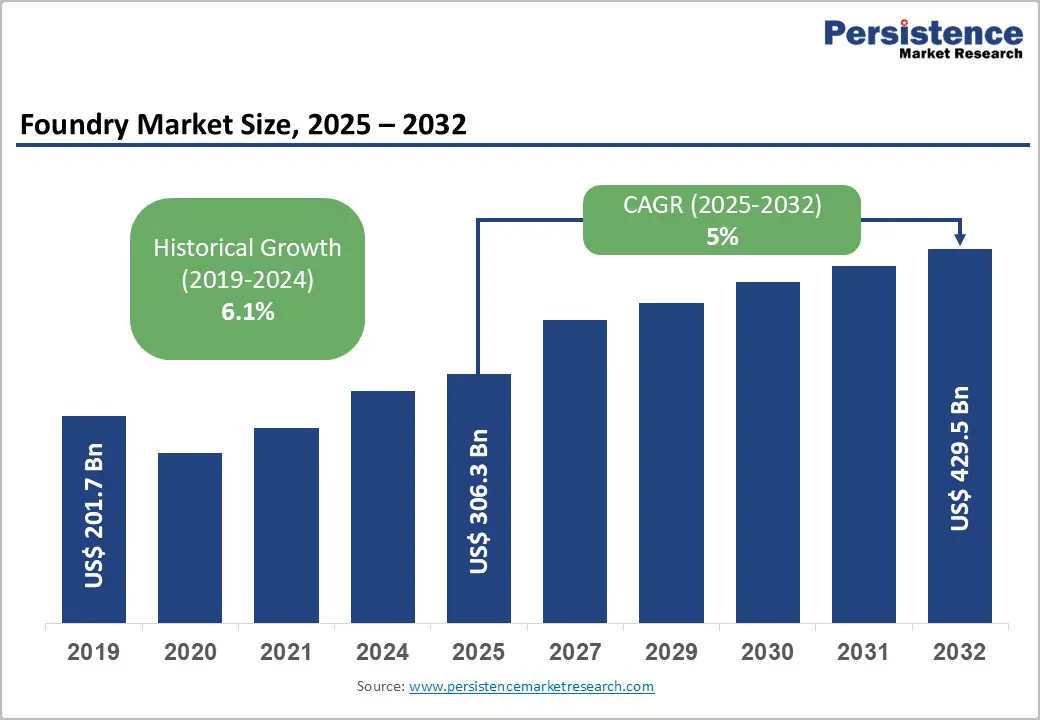

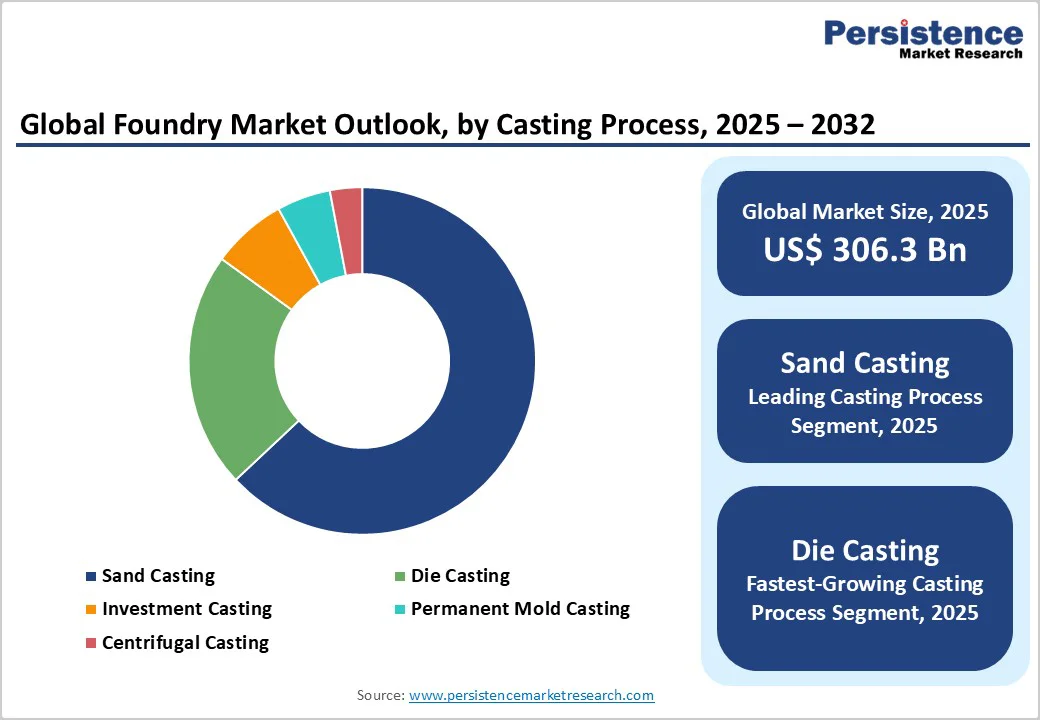

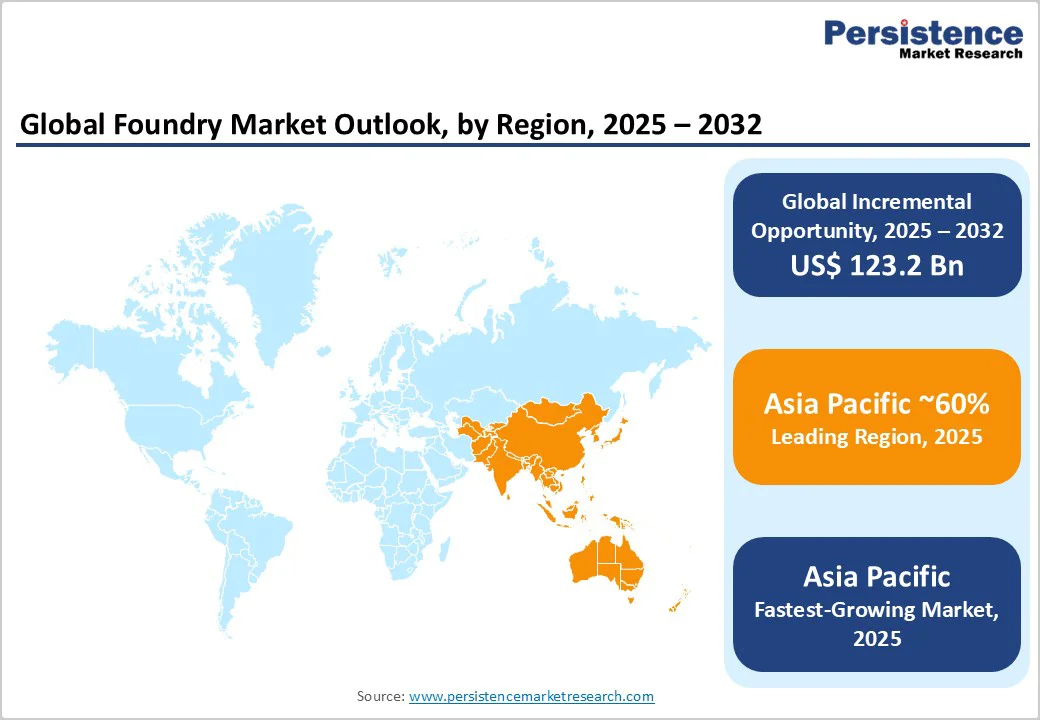

The global foundry market is expected to reach US$306.3 billion in 2025. It is estimated to reach US$429.5 billion by 2032, growing at a CAGR of 5% during the forecast period 2025 − 2032, driven by an accelerating demand for lightweight metal castings in automotive electrification, rapid adoption of Industry 4.0 digitalization technologies across manufacturing facilities, and substantial government-backed investments in semiconductor fabrication.

Rising infrastructure in emerging economies and the automotive shift to EVs, demanding specialized aluminum die-cast components, are driving market growth. Momentum is strongest in advanced process nodes for AI applications, while traditional foundries modernize with robotics and IoT-enabled quality control.

Key Industry Highlights

- Regional Dominance: Asia Pacific dominates with 60% market share and is projected to grow at a 7% CAGR as China, India, and ASEAN nations expand manufacturing capacity to serve domestic and export markets.

- Leading Metal Type: Ferrous castings command around 59% market share in 2025, fueled by EV lightweighting requirements.

- Dominant Casting Processes: Sand casting maintains about 63.2% of the revenue share, while aluminum die-casting is likely to be the fastest-growing segment, driven by automotive structural applications and the adoption of gigacasting technology.

- Application Leadership: Automotive applications account for approximately 47% of market revenue, with industrial machinery expanding at the highest 2025 - 2032 CAGR, driven by investments in automation and renewable energy infrastructure.

- Industry Dynamics: TSMC commands 65% of the semiconductor foundry market share, while traditional metal casting is fragmented, with the top 15 players collectively holding 30% share across diverse application segments.

- Key Trend: Circular-economy integration is accelerating with aluminum recycling, creating cost advantages as original equipment manufacturers (OEMs) implement lifecycle carbon accounting requirements.

- November 2025: SK Hynix's subsidiary, SK Key Foundry, announced plans to launch its silicon carbide (SiC) power semiconductor business in the first half of 2026, targeting the growing market for compound power devices.

| Key Insights | Details |

|---|---|

| Foundry Market Size (2025E) | US$306.3 Bn |

| Market Value Forecast (2032F) | US$429.5 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Circular Economy Integration and Recycled Metal Adoption

The market growth is undergoing transformative shifts as circular economy principles become embedded into operational frameworks, fundamentally altering cost structures and environmental performance metrics. Government mandates across multiple jurisdictions are progressively requiring minimum recycled content thresholds in metal products.

For example, the European Union (EU)'s Circular Economy Action Plan establishes binding targets for the utilization of secondary raw materials in manufacturing sectors. These regulatory frameworks are pushing OEMs to increasingly evaluate suppliers based on environmental, social, & governance (ESG) performance criteria rather than solely price and quality metrics.

Modern foundries are also investing substantially in closed-loop water systems, cleaner melting technologies, and emissions control infrastructure to meet stringent environmental standards while simultaneously reducing operational costs. The inherent compatibility of metal casting processes with multiple recycling cycles, maintaining structural integrity through repeated melting and reforming, positions foundries strategically within circular value chains.

This technological advantage is becoming highly valuable as supply chain disruptions and commodity price volatility highlight the strategic importance of diversified material sourcing. Recycled-metal sourcing provides substantial cost savings while simultaneously addressing customer demands for lower-impact components.

Persistent Skilled Labor Shortages Constraining Advanced Manufacturing Adoption

The foundry industry is confronting acute skilled labor shortages that are materially constraining capacity expansion and technology adoption across developed and emerging markets. Industry associations report critical roles remaining unfilled for extended periods, directly impacting production schedules and customer commitments.

Foundries require workers proficient in operating automated machinery, managing AI-driven systems, and handling digital workflows as Industry 4.0 technologies become the norm rather than the exception. Traditional hiring filters emphasizing formal educational credentials and years of experience are eliminating capable candidates from consideration, shrinking already-limited talent pools.

The demographic challenge is even more severe, with aging workforce dynamics creating knowledge-transfer risks as experienced foundry workers retire without adequate succession-planning mechanisms. Younger workers are disproportionately opting for careers in technology and service sectors rather than in heavy industry, perceiving foundry operations as physically demanding environments with limited career progression opportunities.

This perception gap persists despite modernization efforts that have transformed many foundries into technology-intensive facilities utilizing robotics, advanced simulation software, and precision measurement systems.

EV Powertrain Component Demand Creating High-Value Aluminum Casting Niches

The global EV transition is generating substantial opportunities for specialized aluminum die-casting applications, with automotive electrification creating entirely new component categories requiring foundry capabilities.

EV architectures demand lightweight structural elements, battery enclosures, motor housings, and integrated powertrain components that optimize range performance by reducing mass while maintaining structural integrity and thermal management.

The expansion of gigacasting technology, producing large structural components including underbody sections through single-piece aluminum die-casting, exemplifies the architectural innovations reshaping vehicle manufacturing economics. This approach reduces assembly complexity, eliminates hundreds of individual stamped parts and fasteners, and accelerates production throughput while improving structural performance.

Multiple automakers are replicating this manufacturing philosophy, creating concentrated demand for large-tonnage die-casting equipment and foundries capable of producing meter-scale components with tight dimensional tolerances.

Beyond structural components, battery thermal management systems represent another high-growth segment, requiring complex aluminum castings that integrate cooling channels, mounting interfaces, and electrical isolation within a single component.

Category-wise Analysis

Metal Type Insights

Ferrous castings occupy a commanding position, accounting for an estimated 59% of the revenue share in 2025, driven by extensive applications across automotive, industrial machinery, and infrastructure sectors. Gray and ductile iron castings remain fundamental to engine blocks, transmission housings, and heavy machinery components, where efficiency, machinability, and wear resistance align with performance requirements.

The ferrous segment benefits from abundant domestic iron ore production across major manufacturing economies, established supply chain infrastructure, and mature processing technologies that enable high-volume production at competitive cost points.

The non-ferrous aluminum segment is expected to grow at a notable pace from 2025 to 2032, as lightweight requirements intensify across transportation and energy sectors. Electric vehicle proliferation is fundamentally changing aluminum demand patterns, with battery EVs (BEVs) requiring approximately 30-40% more aluminum than their internal combustion equivalents.

Automotive lightweighting initiatives targeting fuel efficiency improvements and emission reductions are driving structural aluminum adoption beyond powertrain applications into body panels, suspension components, and chassis structures. Simultaneously, renewable energy infrastructure development, particularly wind turbine manufacturing, is generating an enormous demand for aluminum casting to build generator housings and structural components.

Casting Process Insights

Sand casting maintains market leadership with an estimated 63.2% market share in 2025, reflecting its versatility in accommodating complex geometries, compatibility with diverse alloy compositions, and relatively low tooling costs compared to alternative methods. The segment's dominance spans ferrous and non-ferrous applications, particularly in large component production for industrial machinery, infrastructure equipment, and heavy transportation.

The scalability of sand casting positions the technology as the foundational casting method across global foundries. Technological advancements in sand reclamation systems, 3D sand printing for complex mold geometries, and automated molding lines are enhancing sand casting economics and environmental performance.

Aluminum die-casting is likely to expand the fastest between 2025 and 2032, propelled by automotive electrification, electronics miniaturization, and industrial automation trends that demand high-precision, thin-walled components with excellent surface finishes.

High-pressure die-casting technology enables tight dimensional tolerances, rapid production cycles, and near-net-shape manufacturing, minimizing secondary machining requirements and creating total cost advantages in suitable applications. The automotive industry's turn toward gigacasting is pulling in substantial investments in large-tonnage die-casting capacity, with equipment manufacturers reporting multi-year order backlogs.

End-user Insights

The automotive industry leads with an estimated 47% of the market share in 2025. Traditional internal combustion vehicle production sustains substantial iron casting volumes for engine blocks, cylinder heads, transmission cases, and brake components, while the EV transition is simultaneously expanding aluminum die-casting requirements for battery enclosures, motor housings, structural elements, and thermal management systems.

The automotive aftermarket is also generating consistent demand for replacement parts, including brake rotors, suspension components, and engine rebuilds, providing volume stability that partially offsets new-vehicle production cycles.

The industrial machinery and equipment sector is slated to post the highest CAGR through 2032, driven by manufacturing automation investments, industrial robotics deployment, and capital equipment replacement cycles across developed and emerging economies.

Construction equipment manufacturing is experiencing robust growth as global infrastructure development accelerates, requiring substantial iron and steel castings for excavator components, crane structures, and material handling systems. Agricultural machinery modernization in emerging markets is generating incremental casting demand for tractor components, harvesting equipment, and irrigation systems as mechanization adoption increases.

Regional Insights

North America Foundry Market Trends

North America accounts for an estimated 17% of the global market share in 2025, dominated by the U.S. The market here is characterized by a mature foundry infrastructure requiring substantial replacement investments as aging equipment approaches end-of-service lifecycles.

American foundries are implementing robotic pouring arms, IoT-enabled furnaces, and smart blast cabinets to address persistent labor shortages. The U.S. CHIPS and Science Act is stimulating investments in semiconductor foundries, with major fabrication facilities under construction to enhance domestic capacity for advanced node manufacturing.

In Canada, foundries mainly benefit from proximity to U.S. automotive manufacturing clusters while serving domestic markets for resource extraction, energy infrastructure, and transportation equipment.

The regional regulatory environment emphasizes environmental compliance, with foundries investing in emissions control systems, energy-efficient melting technologies, and waste heat recovery infrastructure to meet progressively stringent air quality standards.

Regional automotive OEMs are restructuring supply chains to enhance resilience following pandemic-related disruptions, creating nearshoring opportunities for foundries offering just-in-time delivery capabilities and collaborative engineering support.

Europe Foundry Market Trends

Europe secures around 21% of the foundry market share in 2025, as established manufacturing economies of the EU focus on specialized high-value casting segments. Germany dominates regional production, leveraging world-leading automotive manufacturing infrastructure and precision engineering capabilities that demand high-quality castings for premium vehicle segments, industrial machinery, and capital equipment.

The European Chips Act is directing substantial public funding toward semiconductor fabrication capacity, with Germany, France, and Italy hosting major facility investments emphasizing automotive-grade semiconductors and industrial IoT applications.

The U.K., France, and Spain boast strong foundry sectors serving regional automotive, aerospace, and energy markets. European regulatory harmonization through EU environmental directives is compelling foundries to implement cutting-edge technologies for emissions control, energy management, and circular economy material flows.

Regional foundries are differentiating through engineering collaboration, offering design-for-manufacturing expertise and simulation capabilities that reduce prototype iterations and accelerate product development cycles. Sustainability performance is becoming a competitive differentiator, with OEMs increasingly requiring lifecycle carbon assessments and environmental product declarations from casting suppliers.

Asia Pacific Foundry Market Trends

Asia Pacific dominates the foundry market with an estimated 60% share in 2025 and is projected to register the highest CAGR from 2025 to 2032, powered by manufacturing scale advantages, comprehensive supply chain ecosystems, and robust domestic demand growth. China leads in output through massive production capacity serving the automotive, machinery, construction equipment, and infrastructure sectors.

China's domestic EV production surge is creating concentrated aluminum die-casting demand, with multiple automakers implementing gigacasting technologies and stimulating specialized foundry capacity investments.

Taiwan maintains semiconductor foundry supremacy on the back of technological leadership in advanced process nodes serving AI, high-performance computing, and smartphone applications. India's foundry sector is experiencing exceptional growth, driven by automotive localization policies, infrastructure development programs, and manufacturing incentives under the Make in India initiative.

The regional competitive landscape balances low-cost, high-volume production capabilities against increasingly sophisticated quality requirements and environmental standards as multinational corporations extend supply chain compliance expectations to regional suppliers.

Government support mechanisms, including subsidized financing, infrastructure development, and technology transfer programs, are sustaining regional capacity expansion despite cyclical demand fluctuations and trade policy uncertainties.

Competitive Landscape

The global foundry market is moderately fragmented. In semiconductors, TSMC leads with ~65% share, followed by Samsung, GlobalFoundries, UMC, and SMIC, reflecting high capital intensity, advanced node requirements, and strong customer moats. Traditional metal casting is more fragmented, with the top 10-15 players holding ~30% and thousands of regional foundries serving niche markets.

Competitive advantage increasingly relies on technology and services; semiconductor foundries focus on Industry 4.0, simulation, and process nodes, while casting foundries leverage material expertise, quality certifications, specialized alloys, and integrated value-added services such as machining, assembly, and testing.

Key Industry Developments

- In November 2025, GlobalFoundries acquired Singapore’s Advanced Micro Foundry, boosting its silicon photonics capabilities. The deal adds manufacturing capacity, IP, and talent, enabling faster, more efficient data transfer for AI, telecom, and quantum computing. This positions GlobalFoundries as the world’s largest pure-play silicon photonics manufacturer.

- In October 2025, China’s semiconductor sector saw major state-backed consolidation as Hua Hong Semiconductor and SMIC merged subsidiaries. The move addresses U.S. export controls and chip oversupply, aiming to strengthen national champions, streamline supply chains, support advanced node development, and manage investments, despite integration challenges and market uncertainties.

- In September 2025, India’s Kolhapur Foundries launched a decarbonisation initiative targeting 30% emission reductions. Piloted across three sites, it identified energy-saving measures capable of transforming 300+ units into India’s first green MSME cluster. The program promotes sustainability, energy efficiency, and competitiveness in the foundry sector, supporting national carbon reduction goals.

Companies Covered in Foundry Market

- Taiwan Semiconductor Manufacturing Company Limited (TSMC)

- Samsung Electronics Co., Ltd. (Samsung Foundry)

- GlobalFoundries Inc.

- United Microelectronics Corporation (UMC)

- Semiconductor Manufacturing International Corporation (SMIC)

- Bharat Forge Limited

- Nemak S.A.B. de C.V.

- Ryobi Limited

- Alcoa Corporation

- Precision Castparts Corp. (Berkshire Hathaway)

- Ahresty Corporation

- Endurance Technologies Limited

- Dynacast International

- Consolidated Precision Products Corp.

- Georg Fischer Ltd.

Frequently Asked Questions

The global foundry market is projected to reach US$306.3 Billion in 2025.

The steady transition toward EVs requiring specialized aluminum die-cast components and the development of advanced process nodes serving AI applications are driving the market.

The foundry market is poised to witness a CAGR of 5% from 2025 to 2032.

An accelerating demand for lightweight metal castings in automotive electrification, rapid adoption of Industry 4.0 digitalization technologies across manufacturing facilities, and substantial government-backed investments in semiconductor fabrication are key market opportunities.

Taiwan Semiconductor Manufacturing Company Limited (TSMC), Samsung Electronics Co., Ltd. (Samsung Foundry), and GlobalFoundries Inc. are some of the key players in the foundry market.