- Beverages

- Dairy Alternative Beverages Market

Dairy Alternative Beverages Market Size, Share, and Growth Forecast, 2025 - 2032

Dairy Alternative Beverages Market by Beverage Type (Almond Milk, Soy Milk, Oat Milk, Coconut Milk, Rice Milk, Hemp Milk, Cashew Milk), Flavor (Vanilla, Chocolate, Strawberry, Hazelnut, Other Seasonal Flavors), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retail, Specialty Stores, Others), and Regional Analysis for 2025 - 2032

Dairy Alternative Beverages Market Size and Trends Analysis

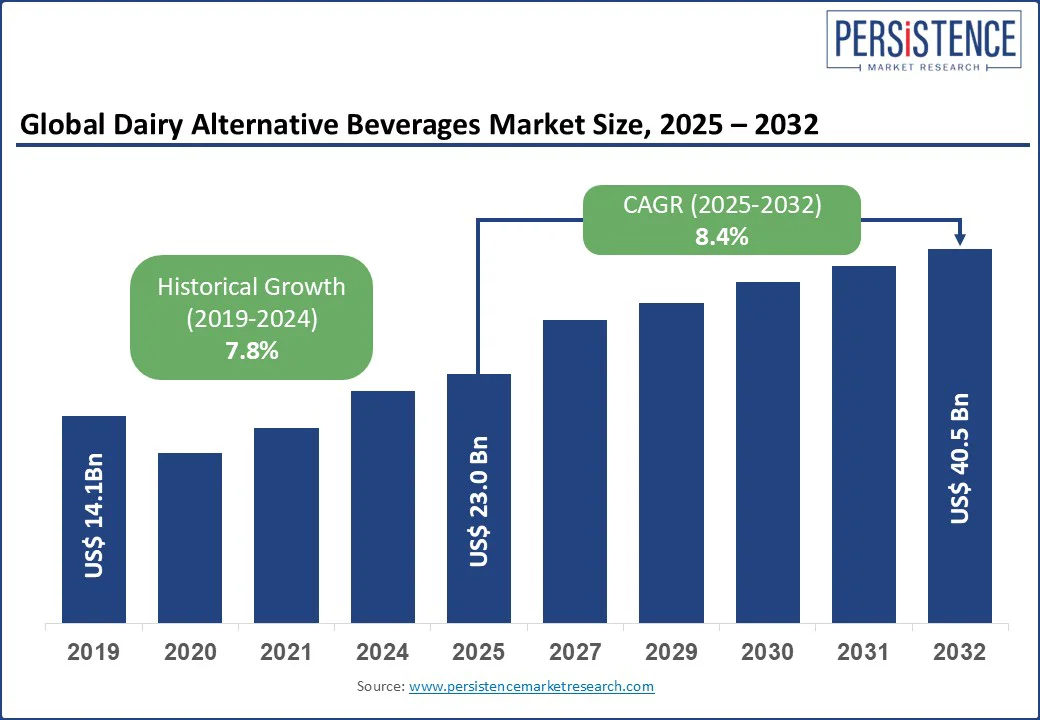

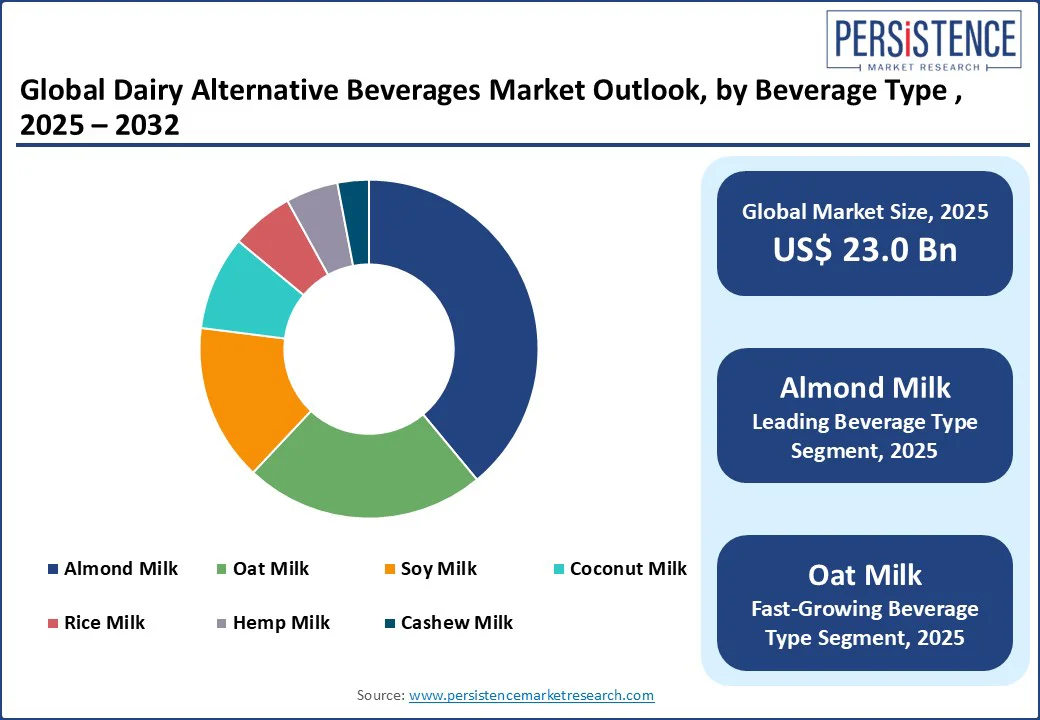

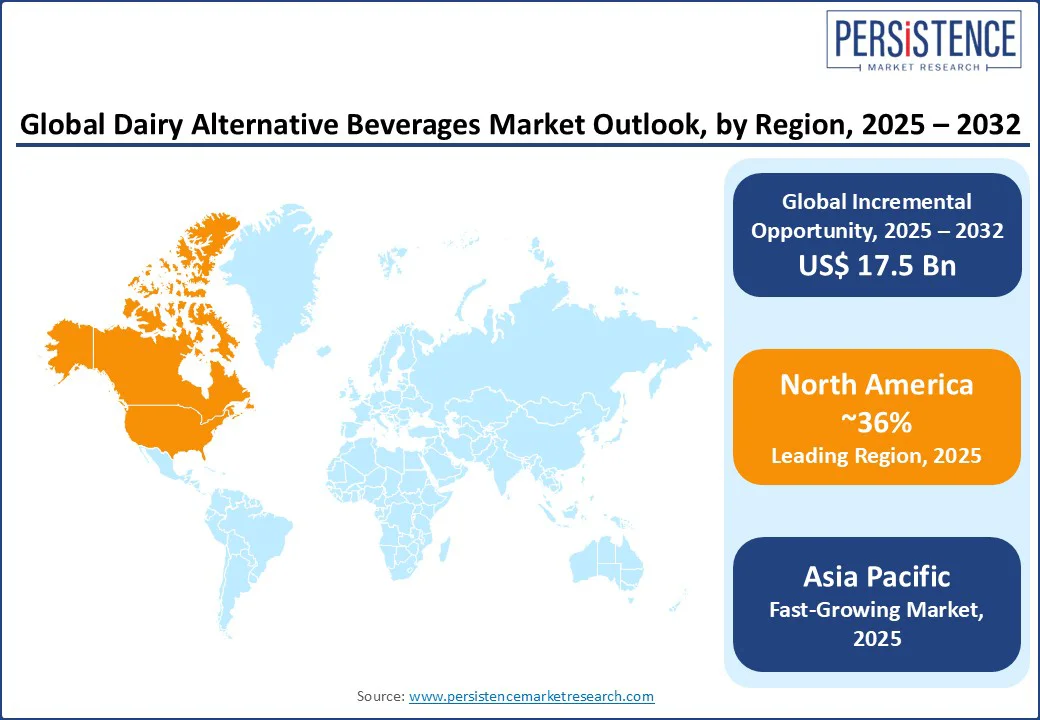

The global Dairy Alternative Beverages Market size is likely to value at US$ 23.0 Bn in 2025 and is expected to reach US$ 40.5 Bn by 2032, growing at a CAGR of 8.4% during the forecast period from 2025 to 2032.

The dairy alternative beverages industry has experienced robust growth, driven by rising consumer demand sfor plant-based diets, increasing awareness of lactose intolerance, and the growing trend toward sustainable and ethical food consumption.

The sector is driven by the demand for versatile, health-conscious, and environmentally friendly beverage options that cater to diverse dietary preferences while aligning with global sustainability objectives.

Key Industry Highlights:

- Leading Region: North America, holding a 36% dairy alternative beverages Market share in 2025, driven by high consumer awareness, advanced retail infrastructure, and a strong preference for plant-based products.

- Fastest-growing Region: Asia Pacific, fueled by rapid urbanization, increasing health consciousness, and the rising adoption of vegan and flexitarian diets.

- Major Developments Dairy Alternative Beverages Market: Europe, advancing through initiatives such as the EU’s Farm to Fork Strategy, with significant investments in sustainable food systems and plant-based innovations.

- Dominant Beverage Type: Almond Milk, commanding nearly 39% market share, reflecting its widespread popularity due to its taste, versatility, and nutritional profile.

- Leading Distribution Channel: Supermarkets/Hypermarkets, accounting for over 49% of market revenue, driven by the global surge in e-commerce and direct-to-consumer platforms.

|

Global Market Attribute |

Key Insights |

|

Dairy Alternative Beverages Market Size (2025E) |

US$ 23.0 Bn |

|

Market Value Forecast (2032F) |

US$ 40.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.8% |

Market Dynamics

Driver - Surge in Plant-Based Diets and Health Consciousness

The dairy alternative beverages market is experiencing robust growth, fueled by the exponential rise in plant-based diets and heightened health consciousness. Greater awareness of lactose intolerance, dairy allergies, and the nutritional benefits of plant-based options is driving consumers away from traditional dairy.

This shift is reinforced by the expanding vegan and flexitarian populations, particularly across North America and Europe, where demand for low-calorie, nutrient-rich beverages is surging. Supportive government initiatives, such as the EU’s Farm to Fork Strategy and the U.S. Dietary Guidelines promoting plant-based diets, further accelerate adoption.

For instance, a 2023 report by the Good Food Institute revealed that plant-based milk accounts for 15% of total milk sales in the U.S. Derived from almonds, soy, oats, and coconuts, these beverages not only provide nutritional value but also deliver a lower environmental footprint, appealing strongly to eco-conscious consumers.

Restraint - High Production Costs and Supply Chain Challenges

The dairy alternative beverages market faces notable restraints due to high production costs and ongoing supply chain disruptions. Manufacturing plant-based drinks, especially almond and cashew milk, demands substantial resources, including large volumes of water, significant energy, and raw inputs such as nuts and grains.

For instance, growing a single almond can consume between 1 and 3.2 gallons of water, creating a considerable environmental strain in drought-affected regions such as California, which supplies about 80% of the world’s almonds. Additionally, the industry’s energy-intensive operations, spanning grinding, blending, and pasteurization, are further impacted by rising energy prices, particularly in Europe amid geopolitical instability. Compounding these issues, supply chain bottlenecks, from port congestion in Asia to labor shortages in North America, drive up costs and hinder scalability, disproportionately affecting smaller producers that lack the economies of scale enjoyed by larger competitors.

Opportunity - Innovations in Product Development and Sustainability

The growing emphasis on sustainability and product innovation offers strong growth potential for the dairy alternative beverages market. Advances in processing technologies such as enzyme-based extraction, ultrafiltration, and high-pressure processing enhance taste, texture, and nutritional value, while nutritional fortification with vitamins, calcium, and plant-based proteins boosts health appeal.

For instance, Alpro’s use of high-pressure processing has extended shelf life without compromising nutritional quality. Sustainable packaging innovations, including recyclable cartons, biodegradable bottles, and compostable caps, resonate with eco-conscious consumers; for example, Tetra Pak’s fully recyclable plant-based beverage cartons, launched in 2024, are gaining traction among leading brands. E-commerce channels enable customization through limited-edition flavors and seasonal blends, driving engagement and brand loyalty, such as Oatly’s barista-grade seasonal oat milk series for specialty coffee. Supportive regulations and dietary guidelines encourage plant-based adoption, particularly in emerging markets where rising urbanization and awareness of lactose intolerance expand the consumer base. Additionally, climate-conscious behavior and lifecycle assessments highlighting lower carbon and water footprints strengthen the competitive positioning of plant-based beverages as premium, sustainable, and health-forward choices.

Category-wise Analysis

Beverage Type Insights

Almond Milk dominates the dairy alternative beverages market, expected to account for approximately 39% of the industry share in 2025. Its dominance stems from its creamy texture, mild flavor, and widespread use in beverages, smoothies, and culinary applications. Almond milk’s high nutritional value, including low calories and high vitamin E content, makes it a popular choice among health-conscious consumers. Its compatibility with various flavors, such as vanilla and chocolate, enhances its applicability across markets.

The Oat Milk segment is the fastest-growing from 2025 to 2032, driven by increasing consumer preference for sustainable and allergen-free options. Oat milk’s low environmental impact, requiring significantly less water than almond milk, and its creamy texture make it ideal for coffee shops and home use. The rise of barista-grade oat milk and its growing presence in mainstream retail channels, particularly in North America and Europe, is accelerating its adoption, especially among younger demographics.

Flavor Type Insights

Vanilla holds the largest dairy alternative beverages market share, accounting for 2025. Its popularity is driven by its versatile flavor profile, which complements a wide range of beverages and culinary applications. Vanilla-flavored dairy alternatives are widely used in coffee, smoothies, and baking, making them a staple in both retail and foodservice sectors. The flavor’s smooth and familiar taste appeals to a broad consumer base, particularly in North America and Europe.

Strawberry is the fastest-growing flavor segment, fueled by its appeal to younger consumers and its use in seasonal and limited-edition products. The vibrant color and sweet-tart profile of strawberry-flavored dairy alternatives make them popular in ready-to-drink beverages and children’s products. The growing demand for innovative and indulgent flavors, particularly in e-commerce and specialty retail, is driving the rapid adoption of strawberry-flavored dairy alternatives.

Distribution Channel Insights

Supermarkets/hypermarkets dominate the dairy alternative beverages market with a 49% share, driven by their extensive product variety, strong brand presence, and convenient one-stop shopping experience, attracting a broad consumer base seeking diverse, accessible, and trusted plant-based beverage options.

Specialty Stores are the fastest-growing distribution channel, driven by the increasing demand for premium and niche plant-based beverages. These stores cater to health-conscious and vegan consumers, offering specialized products such as organic, non-GMO, and artisanal dairy alternatives. The rise of boutique health food stores and cafes, particularly in urban areas, is fueling the adoption of specialty retail as a key distribution channel.

Regional Insights

North America Dairy Alternative Beverages Market Trends

North America is the leading region in the global dairy alternative beverages market, with approximately 36 % of the total market revenue, with the United States and Canada at the forefront. North America is a key region in the global dairy alternative beverages market, led by the United States and Canada. High consumer awareness of plant-based diets, advanced retail infrastructure, and the presence of major players such as Blue Diamond Growers, Danone North America, Califia Farms, and Oatly drive growth.

Environmental concerns, lactose intolerance prevalence, and regulatory support, such as USDA promotion of plant-based diets, further boost demand. Rising vegan and flexitarian populations, alongside preferences for organic, clean-label, and fortified beverages, shape purchasing trends. In the U.S., supermarkets dominate distribution, while online channels are growing rapidly, fueled by convenience and product versatility.

Innovation in flavors, protein enrichment, and barista-friendly blends attracts wider consumers. Canada mirrors these trends, emphasizing locally sourced and sustainably packaged options. With double-digit growth projections, the sector is set to expand through product innovation, e-commerce investment, and strategic acquisitions, reinforcing North America’s strong global position.

Europe Dairy Alternative Beverages Market Trends

Europe holds a significant share in the global dairy alternative beverages market, driven by strong sustainability initiatives, advanced manufacturing capabilities, and growing e-commerce adoption. Leading countries include Germany, the UK, and Sweden. Germany benefits from its leadership in plant-based innovation, with companies such as Alpro investing in sustainable production methods. The UK’s market is bolstered by the rapid growth of veganism and initiatives promoting alternatives to dairy, such as the Vegan Society’s campaigns. Sweden’s market is supported by significant investments in oat milk production, led by brands such as Oatly.

The EU’s stringent regulations, such as the Farm to Fork Strategy, drive the adoption of eco-friendly dairy alternatives, though compliance with complex labeling and environmental laws poses challenges. Europe’s dairy alternative beverages market is projected to grow steadily from 2025 to 2032, supported by consumer demand for sustainable and health-conscious products.

Asia Pacific Dairy Alternative Beverages Market Trends

Asia Pacific is the fastest-growing region in the global dairy alternative beverages market. This regional growth is primarily driven by high consumer demand in countries such as China, India, and Japan. Rapid urbanization, rising health consciousness, and the growing adoption of vegan and flexitarian diets are key factors boosting demand. China leads the industry, benefiting from a well-developed retail ecosystem and increasing demand for soy and almond milk in urban centers. India’s market is driven by a high prevalence of lactose intolerance and growing awareness of plant-based nutrition.

The rapid expansion of e-commerce across the region has further accelerated the need for accessible and affordable dairy alternatives, particularly for last-mile delivery. Rising middle-class populations and increasing disposable incomes are fueling greater consumption of packaged beverages, boosting market demand. Government initiatives promoting sustainable food systems, such as China’s Green Food Strategy, have reinforced the adoption of plant-based beverages, aligning with broader environmental objectives.

Competitive Landscape

The global dairy alternative beverages market is characterized by strong competition, regional strengths, and a mix of global and local manufacturers. In developed regions such as North America and Europe, large firms such as Blue Diamond Growers, WhiteWave Foods, and Oatly dominate through scale, advanced technology, and established partnerships with retailers and e-commerce platforms.

In the Asia Pacific, rapid urbanization and growing health consciousness are attracting investments from both local and international players. Companies are focusing on sustainability, product innovation, and flavor diversification to gain a competitive edge. Digital marketing and direct-to-consumer models have emerged as key differentiators, enabling personalized offerings and faster market penetration. Strategic alliances and R&D initiatives are further intensifying the competitive landscape.

Key Developments

- In December 2024, Oatly announced the closure of its Singapore plant, citing its shift toward an asset-light supply chain strategy. The company plans to consolidate Asia-Pacific supply through existing European facilities

- In December 2023, Almond producer Blue Diamond Growers is launching a new plant-based milk product for health-conscious consumers.

Companies Covered in Dairy Alternative Beverages Market

- Archer Daniels Midland

- Blue Diamond Growers

- SunOpta

- WhiteWave Foods Company

- Panos Brands

- Others

Frequently Asked Questions

The Dairy Alternative Beverages market is projected to reach US$ 23.0 Bn in 2025.

The surge in plant-based diets and government-backed sustainability initiatives is our key driver.

The Dairy Alternative Beverages market is poised to witness a CAGR of 8.4% from 2025 to 2032.

Innovations in product development and sustainable packaging are key opportunities.

Blue Diamond Growers, WhiteWave Foods, Oatly, Archer Daniels Midland, and Hain Celestial Group are key players.