- Beverages

- Oat Milk Market

Oat Milk Market Size, Share, and Growth Forecast 2026 - 2033

Oat Milk Market by Product Type (Plain Oat Milk, Flavored Oat Milk), by Nature (Organic, Conventional), by Sales Channel (Supermarkets / Hypermarkets, Convenience Stores, Specialty Stores, Online Retail, Others), and by Regional Analysis, 2026-2033

Oat Milk Market Size and Trend Analysis

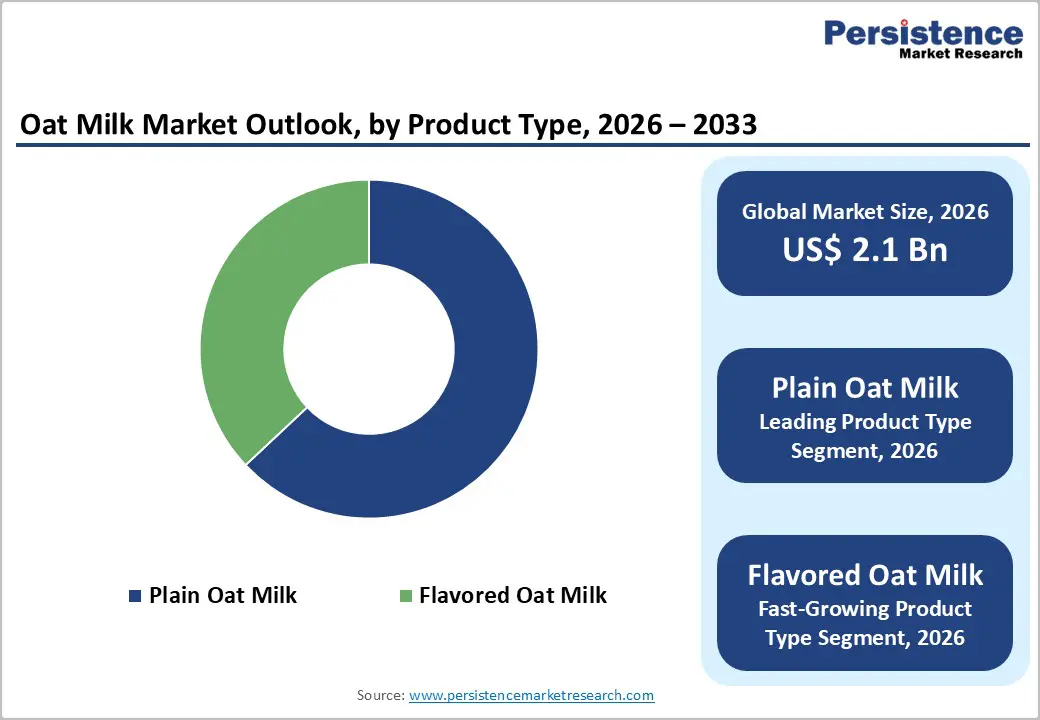

The global Oat Milk Market size is expected to be valued at US$ 2.1 billion in 2026 and projected to reach US$ 4.9 billion by 2033, growing at a CAGR of 12.9% between 2026 and 2033.

The exponential growth of the market is primarily driven by the rising global prevalence of lactose intolerance and a profound shift toward sustainable, plant-based diets among health-conscious consumers. This transition is supported by the dairy industry's environmental footprint, which has led individuals to seek low-impact alternatives that do not compromise on texture or functionality. Additionally, the rapid integration of oat-based beverages into the global café culture and strategic partnerships between manufacturers and multinational coffee chains have significantly enhanced product accessibility and consumer familiarity, further accelerating adoption across diverse demographics.

Key Industry Highlights

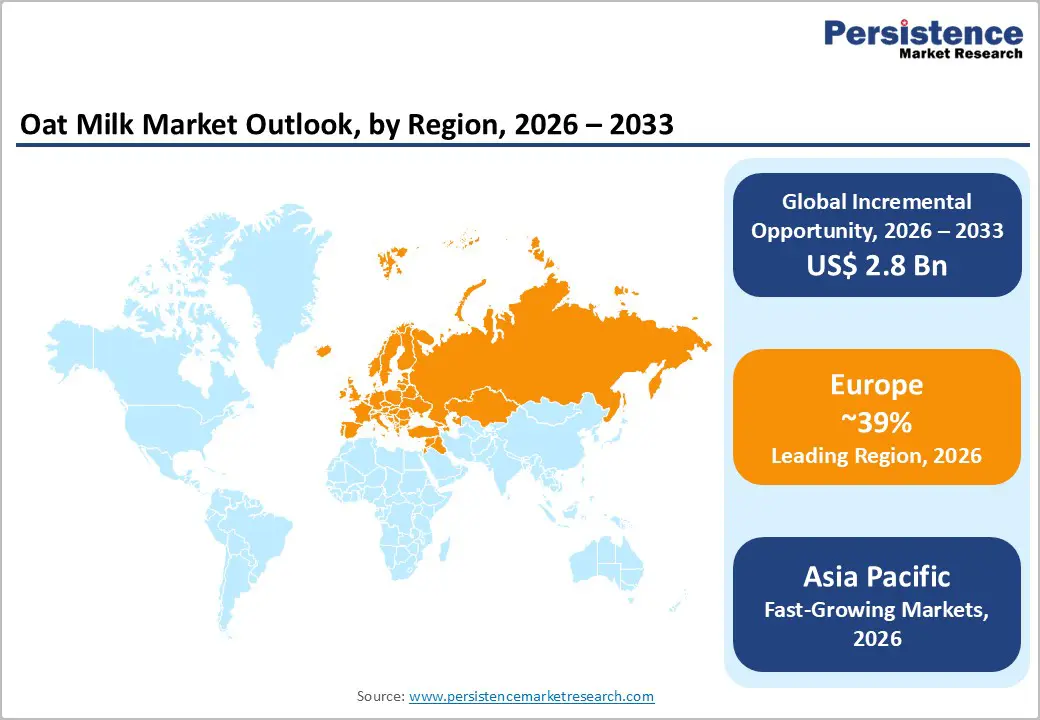

- Leading Region: Europe, commanding around 39% market share in 2025, supported by strong sustainability policies, high clean-label awareness, and deep integration of oat milk into daily diets and coffee culture.

- Fastest-Growing Region: Asia Pacific, fueled by high lactose intolerance prevalence, rapid expansion of specialty coffee chains, rising disposable incomes, and strong adoption in China, India, Japan, and Southeast Asia.

- Dominant Product Type Segment: Plain / Unsweetened Oat Milk, leading with approximately 63% share due to versatility, lower sugar content, and preference among health-conscious and culinary users.

- Fastest-Growing Product Segment: Flavored and Barista-Grade Oat Milk, driven by RTD consumption, café-style beverages, and demand for indulgent yet dairy-free options.

- Market Drivers: Rising lactose intolerance, preventive health awareness, heart wellness positioning, and environmental sustainability advantages over conventional dairy.

- Opportunities: Expansion into barista-grade foodservice, clean-label fortification, functional nutrition positioning, and subscription-led online retail models.

- Key Developments: In December 2025, a Swedish oat milk brand launched caramel-flavored Barista Iced Macchiato and Barista Iced Flat White across 400+ Tesco stores in the UK, In May 2025, New Zealand’s Boring Oat Milk entered over 1,000 Woolworths stores in Australia, marking its largest retail expansion to date.

| Key Insights | Details |

|---|---|

| Global Oat Milk Market Size (2026E) | US$2.1 Bn |

| Market Value Forecast (2033F) | US$4.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 12.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 11.7% |

Market Dynamics

Driver – Rising Global Prevalence of Lactose Intolerance and Dairy Allergies

The primary catalyst for the surge in demand for oat milk is the increasing medical recognition of lactose intolerance, which affects approximately 65% to 70% of the global adult population according to the National Institutes of Health (NIH). Unlike soy or nut-based alternatives, oat milk is naturally free from common allergens such as nuts and soy, making it a "safe-haven" beverage for individuals with multiple dietary sensitivities. Furthermore, organizations like the World Health Organization (WHO) have highlighted the importance of dietary diversification to manage metabolic health, leading many consumers to adopt oat milk for its high content of beta-glucan, a soluble fiber known to support heart health and maintain healthy cholesterol levels. This medical and nutritional positioning has transitioned oat milk from a niche vegan product to a mainstream dietary staple.

Environmental Sustainability and Lower Carbon Footprint

Consumer behavior is increasingly influenced by "eco-anxiety" and the desire for sustainable consumption, providing a massive tailwind for the market. Research from the University of Oxford suggests that producing a glass of dairy milk results in almost three times more greenhouse gas emissions than any plant-based alternative. Specifically, oat production requires significantly less land and water compared to almond or cow's milk. For instance, growing oats uses about 80% less land than dairy farming and significantly less water than almond cultivation, which is often criticized for its impact on water-stressed regions like California. This environmental advantage resonates deeply with Millennial and Gen Z consumers, who prioritize brands that demonstrate transparent supply chains and carbon-neutral goals, thereby driving the long-term viability of the industry.

Restraints – High Retail Price Points Compared to Conventional Dairy

Despite its growing popularity, the market faces significant barriers due to its premium pricing structure. On average, a liter of oat milk can be 2.5 to 3 times more expensive than conventional cow's milk in regions such as North America and Europe. This price disparity is often attributed to the specialized enzymatic liquefaction processes required to maintain the milk's creamy texture and the high costs associated with small-batch production and cold-chain logistics. For budget-conscious households, especially in emerging economies within Asia Pacific and Latin America, this "vegan tax" remains a deterrent. According to data from various regional trade associations, price sensitivity remains the leading reason why flexitarian consumers hesitate to make a full permanent switch from animal-based dairy.

Opportunity – Expansion into the Foodservice and Barista-Grade Segment

The professional coffee segment represents a massive growth frontier for oat milk producers. Unlike many other plant milks, oat milk possesses a unique protein and carbohydrate profile that allows it to froth and steam similarly to dairy milk, making it the preferred choice for baristas. Partnerships with global entities like Starbucks, Costa Coffee, and Dunkin' have already proven successful, but there remains untapped potential in independent café networks and the Horeca (Hotel, Restaurant, and Cafe) sector in developing regions. Innovations in "Barista Blends" that are specifically formulated to resist curdling in high-acidity coffee environments are expected to drive volume sales. As more specialty coffee shops adopt oat milk as their default non-dairy option, the "halo effect" from professional use will continue to drive retail sales as consumers seek to replicate the café experience at home.

Technological Advancements in Product Fortification and Clean-Label Formulations

Significant opportunities lie in developing next-generation oat milk products that bridge the nutritional gap relative to bovine milk. While oats are naturally healthy, they often lack the protein, calcium, and Vitamin B12 levels found in dairy. Market participants who invest in advanced micro-encapsulation and fortification technologies can offer products that match the nutritional profile of dairy without compromising the "clean-label" status that consumers demand. According to the Plant Based Foods Association (PBFA), there is a rising demand for "ultra-clean" products, those with fewer than five ingredients and no added sugars or oils. Companies that can achieve the desired creamy mouthfeel using only water, oats, and sea salt, while delivering essential micronutrients, will likely capture the highest market share among health-centric demographics.

Category-wise Analysis

Product Type Analysis

The Plain Oat Milk segment currently dominates the market, accounting for a 63% share in 2025. This leadership is sustained by the product's extreme versatility across various culinary applications, including cooking, baking, and as a base for cereal and coffee. Consumers favor plain variants because they typically contain fewer additives and allow for better control over sugar intake. According to Persistence Market Research, health-conscious shoppers prioritize "unsweetened" and "original" labels to avoid hidden calories. Conversely, the Flavored Oat Milk segment is identified as the fastest-growing category. This growth is fueled by the rising demand for on-the-go, ready-to-drink (RTD) beverages. Innovations in flavors such as chocolate, vanilla, and seasonal variants like pumpkin spice are attracting younger consumers and children, positioning oat milk as a treat-based nutritional beverage.

Sales Channel Analysis

Supermarkets / Hypermarkets remain the leading sales channel, capturing a share of approximately 55% in 2025. These large-scale retail outlets provide consumers with a "one-stop-shop" experience, offering a diverse array of brands, sizes, and price points. The ability to compare products physically and take advantage of bulk discounts makes this channel indispensable for weekly household grocery shopping. However, the Online Retail segment is the fastest-growing sales channel. The surge in e-commerce is attributed to the convenience of doorstep delivery and the rising popularity of subscription models for heavy, shelf-stable items like multi-pack milk cartons. Platforms like Amazon and specialized health-food e-tailers allow niche brands to reach consumers directly, bypassing the high "slotting fees" of traditional retail, while providing existing brands with a platform to offer exclusive deals and auto-replenishment services.

Region-wise Insights

North America Oat Milk Market Trends and Insights

North America holds a significant position in the global landscape, characterized by a highly mature innovation ecosystem and high consumer awareness. The United States serves as the regional engine, where the adoption of plant-based diets has transitioned from a trend to a permanent lifestyle for millions. According to the Good Food Institute (GFI), oat milk has rapidly overtaken soy milk to become the second-most popular plant milk in the U.S., trailing only almond milk. The regulatory framework provided by the U.S. Food and Drug Administration (FDA) regarding labeling has generally remained favorable, allowing brands to use familiar terminology while emphasizing nutritional benefits.

Innovation in the U.S. and Canada is focused on "functionalization," with companies like Califia Farms and SunOpta Inc. launching products enriched with probiotics, adaptogens, or extra protein. The region's competitive landscape is also seeing a rise in private-label offerings from major retailers such as Whole Foods Market and Kroger, which are making oat milk more affordable. Furthermore, the strong presence of coffee culture in cities like Seattle and New York ensures that the barista-grade segment remains a massive driver of volume, as consumers increasingly view oat milk as a premium upgrade to their daily latte.

Europe Oat Milk Market Trends and Insights

Europe is the leading regional market, commanding a 39% share in 2025. This dominance is rooted in the region's long-standing history with dairy alternatives and a strong regulatory focus on sustainability. Countries like Sweden, the birthplace of Oatly Group AB, and Germany are at the forefront of consumption. The European Commission's "Farm to Fork" strategy, part of the European Green Deal, encourages a shift toward plant-based diets to meet climate goals, providing a supportive policy environment for the industry. France and Spain are also seeing rapid growth as traditional dairy companies like Danone and Lactalis Group pivot their portfolios to include plant-based brands like Alpro.

A key trend in Europe is the strict adherence to "clean-label" standards and the high penetration of organic certified products. Regulatory harmonization across the EU ensures that products meet rigorous safety and purity standards, fostering high consumer trust. Furthermore, the region is witnessing a surge in "local sourcing" initiatives, where brands emphasize the use of European oats to reduce "food miles" and support local farmers. The integration of oat milk into traditional European breakfast cultures and its use in vegan-friendly baking and desserts are also contributing to the steady market expansion across the continent.

Asia Pacific Oat Milk Market Trends and Insights

The Asia Pacific region is the fastest-growing market globally, driven by a combination of rising disposable incomes and a high baseline of lactose intolerance among Asian populations. China, Japan, and India are identified as high-growth pockets. In China, the "Westernization" of diets and the explosive growth of specialty coffee chains have made oat milk a status symbol among urban Millennials. Brand recognition for Oatly is particularly high in Shanghai and Beijing, where the company successfully used a "coffee-first" strategy to enter the market. India is also emerging as a major player, with local startups and global giants like Nestlé S.A. launching localized products to cater to the country's massive vegetarian demographic.

Manufacturing advantages in the region, particularly the availability of cost-effective processing facilities and a large agricultural base, are encouraging both global and local players to expand. In Southeast Asia, countries like Singapore and Thailand are becoming hubs for plant-based innovation, with government initiatives supporting the growth of "future foods." The ASEAN growth dynamics are characterized by a rapid shift from traditional soy-based drinks to modern oat-based beverages, which are perceived as having a more "premium" and "creamy" profile. As distribution networks expand into tier-2 and tier-3 cities, the regional market is poised for unprecedented volume growth.

Market Competitive Landscape

The Oat Milk Market is characterized by a "consolidated-fragmented" structure. At the top tier, a few global giants, such as Oatly Group AB, Danone, and Nestlé S.A., command significant market share through massive distribution networks and heavy marketing spend. These leaders focus on "brand-as-a-lifestyle" strategies and strategic partnerships with global foodservice chains to maintain their dominance.

However, the market is also seeing a surge in "agile startups" and niche players like Elmhurst 1925 and Califia Farms, which compete on the basis of unique processing methods (e.g., cold-milling) or specific nutritional claims. Emerging business models are increasingly focused on sustainability, with companies employing "Carbon Labeling" and adopting circular economy practices. Research and development trends are currently centered on improving the "cleanliness" of labels and expanding the application of oat milk into the dairy-free yogurt and ice cream categories.

Key Developments:

- In December 2025, the Swedish brand expanded its UK presence by introducing caramel-flavored Barista Iced Macchiato and Barista Iced Flat White, which launched in November and are now available across more than 400 Tesco stores nationwide.

- In May 2025, New Zealand-based plant milk brand Boring Oat Milk expanded into more than 1,000 Woolworths stores across Australia, marking its largest supermarket rollout to date and significantly strengthening its retail footprint in the region.

- In January 2025, MYOM, a water-activated oat drink premix brand, announced its launch in Whole Foods Market stores across London, expanding access to its convenient, low-waste milk alternative for urban consumers seeking sustainable plant-based beverages.

Companies Covered in Oat Milk Market

- SunOpta Inc,

- Nestle SA

- Danone SA

- Chobani, LLC

- Califia Farms, LLC

- Earth's Own Food Company Inc

- Elmhurst Milked Direct LLC

- Happy Planet Foods

- Mooala Brands, LLC

- Oatly AB

- PACIFIC FOODS OF OREGON, LLC

- THE BRIDGE S.R.L

- Minor Figures

- Otis Oat M!lk

- Panos Brands LLC

- Pureharvest

- Sanitarium

- The Hain Celestial Group Inc.

- Vitasoy International Holdings Limited

- Arla Foods amba

Frequently Asked Questions

The global Oat Milk Market is expected to reach a valuation of approximately US$ 2.1 billion by 2026, marking a period of robust growth as plant-based beverages become a mainstream consumer preference globally

The demand is primarily driven by the rising prevalence of lactose intolerance and the increasing consumer shift toward environmentally sustainable, plant-based diets that offer a lower carbon and water footprint compared to dairy.

Europe leads the Oat Milk market with about 39% share in 2025.

A significant opportunity lies in the Foodservice sector, particularly in professional Barista-Grade formulations that are optimized for coffee shops, as well as the development of "clean-label" and nutritionally fortified products.

Key players include Oatly Group AB, Danone, Nestlé S.A., The Hain Celestial Group, Inc., Califia Farms, Lactalis Group, Campbell Soup Company, SunOpta Inc., and others