- Biotechnology

- Cell Culture Media Market

Cell Culture Media Market Size, Share, and Growth Forecast, 2026 - 2033

Cell Culture Media Market by Product Type (Serum-free Media, Classical Media, Others), Media Type (Liquid Media, Semi-solid and Solid Media), Application (Biopharmaceutical Production, Drug Screening and Development, Others), and Regional Analysis for 2026 - 2033

Cell Culture Media Market Share and Trends Analysis

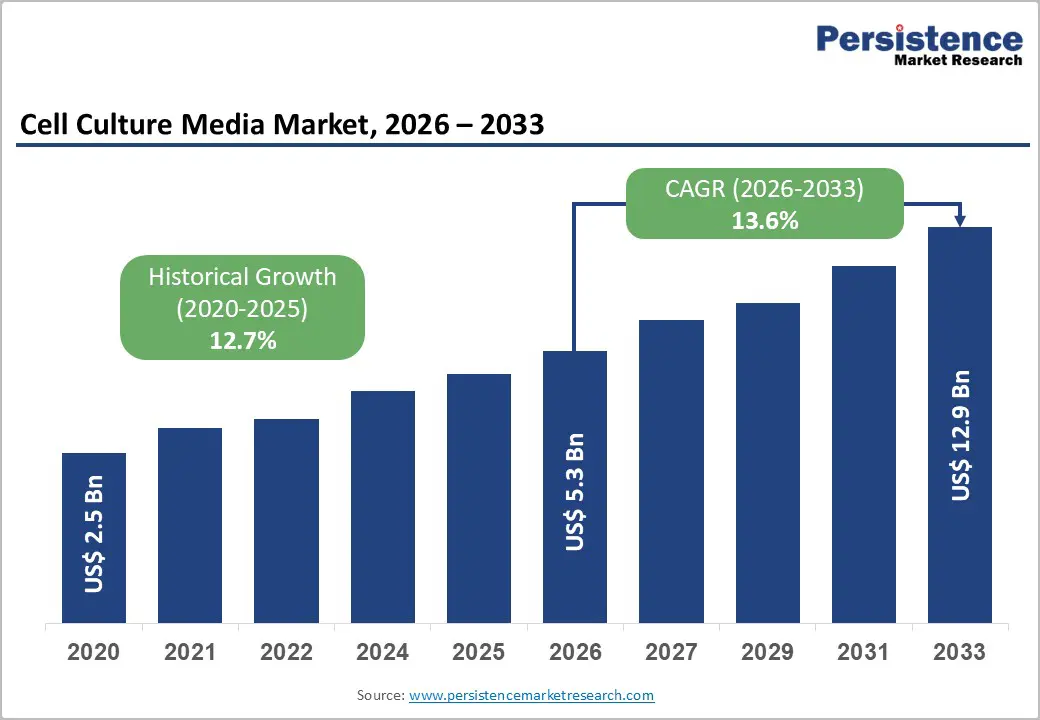

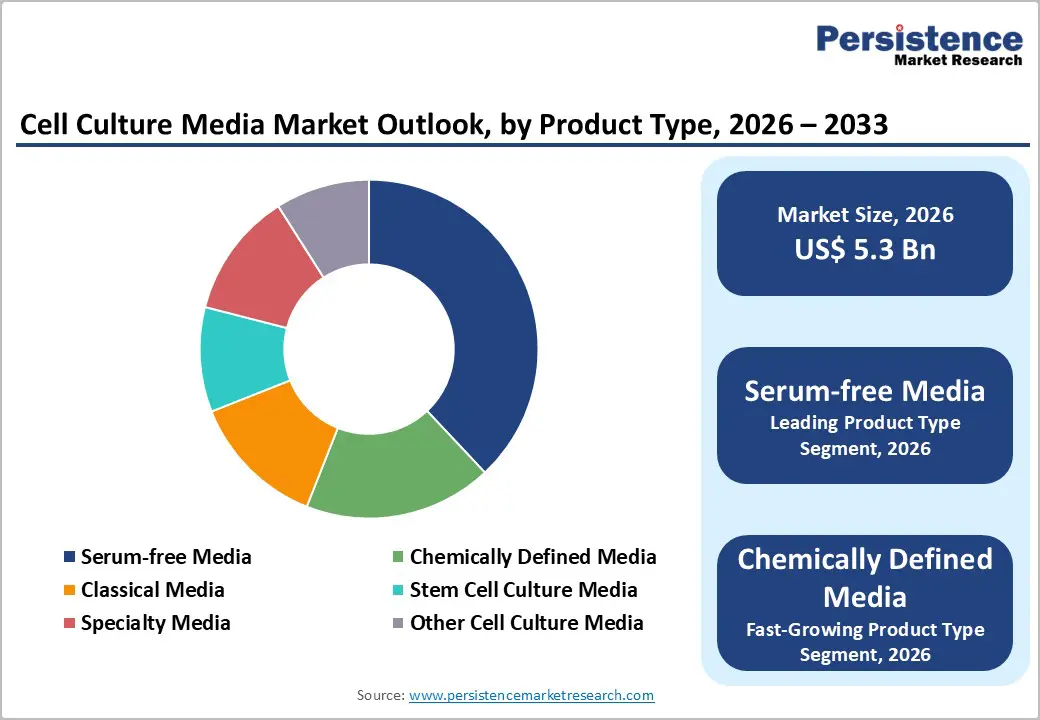

The global cell culture media market size is likely to be valued at US$5.3 billion in 2026 and is estimated to reach US$12.9 billion by 2033, growing at a CAGR of 13.6% during the forecast period 2026 - 2033, driven by expanding biologics manufacturing, rapid cell and gene therapy commercialization, and increasing adoption of serum-free production systems.

The growing prevalence of chronic diseases and rising global demand for monoclonal antibodies are accelerating large-scale cell-based bioprocessing activities. Regulatory emphasis on contamination-free manufacturing and chemically defined formulations is encouraging biopharmaceutical companies to modernize upstream production infrastructure.

Key Industry Highlights:

- Leading Product Type: Serum-free media is set to hold around 38% market share in 2026, driven by intensive regulatory transitions away from animal-derived components to maximize biological safety profiles.

- Fastest-growing Product Type: Chemically defined media is projected as the fastest-growing segment, driven by rising regulatory focus on batch consistency.

- Leading Application: Biopharmaceutical production is estimated to hold roughly 44% market share in 2026, due to expanding global commercial pipelines for monoclonal antibodies and therapeutic vaccines.

- Fastest-growing Application: Drug screening and development is forecast to record the fastest growth, driven by widespread adoption of high-throughput automated target identification workflows and complex three-dimensional cell-based toxicity modeling assays.

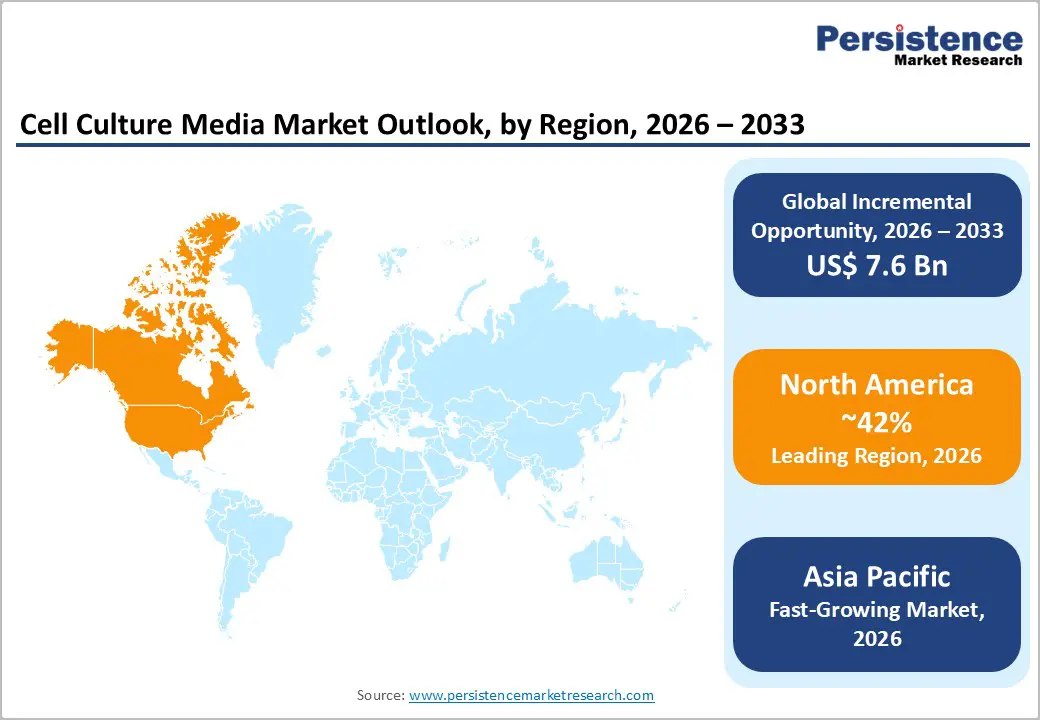

- Regional Leadership: North America is projected to capture roughly 42% of the market share by 2026, while Asia Pacific is forecast to record the fastest growth due to rapid bioprocessing capacity expansions and massive capital shifts toward contract manufacturing localization.

- Competitive Environment: The market reflects a consolidated structure, with key players such as Thermo Fisher Scientific and Merck KGaA leveraging scale, supply chain integration, and processing efficiency to maintain competitive positioning.

- Innovation Trends: Technological advancements in chemical definition, product diversification into specialty media configurations, and contamination-focused solution development are shaping long-term market evolution and investment direction.

DRO Analysis

Driver - Rising Biopharmaceutical Production Capacity

Expansion of biologics manufacturing facilities is increasing the consumption of specialized media formulations required for mammalian cell cultivation and recombinant protein production. Large-scale investments in monoclonal antibody manufacturing, biosimilars, and vaccine development are creating sustained demand for high-performance nutrient systems. Biopharmaceutical producers are prioritizing chemically defined formulations to improve batch consistency, regulatory compliance, and contamination control across commercial manufacturing operations.

The U.S. Food and Drug Administration expanded multiple 2025 guidance initiatives supporting cellular and gene therapy manufacturing flexibility and advanced biologics development, strengthening production scalability requirements for culture systems. Growing approval activity for biologics and regenerative therapies is increasing dependence on optimized media compositions capable of supporting higher cell densities, productivity, and process reproducibility within commercial bioprocessing infrastructure.

Restraint - High Production and Validation Costs

Complex formulation requirements and stringent sterility standards increase manufacturing expenses for chemically defined and specialty media products. Suppliers must maintain highly controlled raw material sourcing, endotoxin testing, and quality validation processes. Elevated operational costs reduce pricing flexibility and pressure margins, particularly among mid-sized biotechnology manufacturers operating under limited production budgets.

Batch-to-batch validation requirements and extensive documentation obligations create scalability limitations for emerging suppliers. Regulatory expectations regarding contamination control and media consistency increase investment burdens related to testing infrastructure and compliance management. Production inefficiencies linked to sensitive raw materials and cold-chain handling further constrain commercial expansion opportunities across cost-sensitive therapeutic development programs.

Opportunity - Expansion of Chemically Defined and Serum-Free Platforms

Biopharmaceutical companies are accelerating the transition toward chemically defined and serum-free formulations to improve reproducibility and reduce contamination risks. This transition is creating opportunities for manufacturers capable of developing optimized nutrient systems tailored for monoclonal antibody production, stem cell expansion, and vaccine manufacturing. Demand for animal-origin-free production environments is strengthening the commercialization potential for precision-formulated media technologies.

Regulatory agencies are increasing their focus on traceability and manufacturing consistency across biologics production workflows. Media developers investing in recombinant supplements, AI-driven nutrient optimization, and scalable bioprocess automation can strengthen supply agreements with pharmaceutical producers seeking compliant and high-efficiency upstream manufacturing solutions across commercial therapeutic pipelines.

Category-wise Analysis

Product Type Insights

The serum-free media segment is anticipated to secure around 38% of the cell culture media market share in 2026, reflecting intensive regulatory transitions away from animal-derived components to maximize biological safety profiles. For instance, Thermo Fisher Scientific expanded specialized formulation production to supply global monoclonal antibody manufacturing facilities requiring strict contamination prevention. This shift ensures superior batch reproducibility during large-scale clinical synthesis pipelines.

The chemically defined media segment is expected to be the fastest-growing segment, propelled by rising adoption of precision bioprocessing and increasing regulatory emphasis on formulation consistency. Merck KGaA introduced advanced chemically defined solutions supporting high-density mammalian cell cultivation in commercial manufacturing facilities. Reduced variability, enhanced scalability, and compatibility with automated upstream production systems are accelerating commercial deployment across therapeutic development operations.

Media Type Insights

The liquid media segment is poised to dominate with a forecast market share of over 72% in 2026, powered by immediate integration capabilities into automated sterile bioprocessing pipelines without requiring external hydration filtration infrastructure. Merck KGaA delivers ready-to-use liquid formulation configurations directly to commercial bioreactor facilities, minimizing preparation times. This operational efficiency eliminates internal facility formulation mixing validation expenses.

The semi-solid and solid media segment is estimated to be the fastest-growing segment, fueled by rising stem cell differentiation assays, colony-forming cell selection protocols, and specialized microbiological diagnostic validation requirements. Stemcell Technologies provided specific semi-solid methylcellulose matrices to support standardized hematopoietic progenitor cell quantification procedures within clinical research laboratories. This physical state maintains the necessary spatial cell orientation.

Application Insights

Biopharmaceutical production is likely to be the leading segment with a projected 44% of the cell culture media market share in 2026, due to expanding global commercial pipelines for monoclonal antibodies and therapeutic vaccines. Lonza utilized high-volume optimized growth formulations within contract manufacturing facilities to fulfill global commercial biotherapeutic delivery contracts. This industrial utilization commands dominant bulk chemical sourcing allocations.

Drug screening and development is anticipated to be the fastest-growing segment, fueled by widespread adoption of high-throughput automated target identification workflows and complex three-dimensional cell-based toxicity modeling assays. Danaher incorporated precise nutritional formulations into automated cellular assay platforms to evaluate novel small-molecule chemical libraries for oncological indications. This integration accelerates early-stage pre-clinical target validation phases.

Regional Insights

North America Cell Culture Media Market Trends

North America is expected to lead with an estimated 42% of the cell culture media market share in 2026, supported by extensive biopharmaceutical manufacturing infrastructure and massive corporate investments into advanced therapeutic pipelines. Accelerated clinical trial approvals by regional regulatory bodies drive immediate demand for high-tier chemically defined formulations.

U.S. Cell Culture Media Market Insights

The U.S. cell culture media infrastructure is expected to expand due to substantial federal funding allocations for domestic biological manufacturing resiliency initiatives. Corporate expansions by major industry participants during 2025 heightened localized production capacities for specialized serum-free formulations. Increased clinical progression of personalized gene therapies across domestic medical centers drives continuous demand for customized cell cultivation inputs.

Canada Cell Culture Media Market Insights

Canada is projected to increase cell cultivation formulation utilization due to expanding public-private partnerships focused on establishing regional vaccine manufacturing autonomy. Increased biotechnical incubation hub investments across major metropolitan zones drive early-stage laboratory consumable consumption. Strategic corporate alliances during 2025, enhanced localized distribution networks, reducing supply chain lead times for specialized academic research inputs.

Europe Cell Culture Media Market Trends

Europe maintains a substantial market presence, driven by rigorous European Medicines Agency quality standards that mandate animal-component-free manufacturing workflows. The presence of established global bioprocessing contract organizations drives continuous bulk formulation consumption. Regional focus on biosimilar development accelerates utilization of optimized growth media to achieve cost-competitive production yields.

Germany Cell Culture Media Market Insights

Germany is forecast to lead regional growth, due to intensifying corporate investments in large-scale biomanufacturing facilities and advanced cellular therapy production lines. The implementation of automated formulation preparation systems within major industrial hubs optimizes large-scale production efficiency. Localized product rollouts in 2025 provided specialized media configurations tailored for high-density suspension cultures.

U.K. Cell Culture Media Market Insights

The U.K. is expected to experience a steady consumption increase, driven by expanding life science research clusters and genomic medicine clinical initiatives. Regulatory framework adaptations post-2025 streamline clinical translation pathways, accelerating cell therapy scaling protocols. Corporate research partnerships with elite academic institutions maintain high baseline demands for specialty stem cell media.

Asia Pacific Cell Culture Media Market Trends

Asia Pacific is forecast to be the fastest-growing market for cell culture media, stimulated by rapid bioprocessing capacity expansions and massive capital shifts toward contract manufacturing localization. Supportive government industrial policies and lower operational cost profiles attract significant international biomanufacturing investments. Rising regional chronic disease diagnostic requirements drive high-volume classical media utilization across healthcare networks.

China Cell Culture Media Market Insights

China is anticipated to contribute massive growth volume, due to large-scale national biomanufacturing infrastructure investments and escalating domestic biosimilar production pipelines. Local chemical synthesis companies expanded production capabilities in 2025, increasing regional availability of cost-effective formulations. Strategic regulatory reforms accelerate domestic clinical trial approvals, driving immediate formulation consumption scaling.

Japan Cell Culture Media Market Insights

Japan is likely to see specialized expansion, driven by pioneering clinical advancements in induced pluripotent stem cell research and regenerative medicine paradigms. Favorable regulatory fast-track pathways for regenerative therapeutics incentivize immediate industrial-scale cell cultivation and formulation procurement. Collaborations between domestic electronics conglomerates and biotechnology entities optimize automated cell expansion machinery utilizing specialized formulations.

Competitive Landscape

The global cell culture media market is consolidated, with a small number of multinational life sciences corporations controlling the vast majority of industrial supply chains. Thermo Fisher Scientific, Merck KGaA, Danaher Corporation, Sartorius AG, and Lonza Group leverage extensive global distribution networks, substantial research budgets, and integrated bioprocessing product suites to maintain dominant market shares.

These leading entities utilize economies of scale to manufacture highly consistent bulk formulations, establishing high entry barriers for new market entrants. Smaller specialized providers maintain viable operations by focusing exclusively on niche applications, including specific stem cell lineages or customized local formulation capabilities. Strategic client retention relies on locking formulations into regulatory-approved therapeutic manufacturing protocols.

Key Industry Developments:

- In May 2026, FUJIFILM Biosciences and NextCell Pharma launched a commercial platform integrating RUO stromal cells with PRIME-XV cell culture media, reinforcing standardized solutions for regenerative medicine and cell therapy development.

- In March 2026, Lonza Group AG announced expansion initiatives for advanced bioprocessing and cell culture manufacturing capabilities, reinforcing scalable biologics production efficiency.

- In March 2025, PHCbi launched the LiCellGrow™ cell expansion system with automated culture condition control technology, reinforcing scalable and high-efficiency cell cultivation processes for advanced therapy manufacturing.

Companies Covered in Cell Culture Media Market

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Danaher Corporation

- Sartorius AG

- Lonza Group AG

- FUJIFILM Irvine Scientific, Inc.

- Corning Incorporated

- Stemcell Technologies Inc.

- PromoCell GmbH

- HiMedia Laboratories Pvt. Ltd.

- PAN-Biotech GmbH

- Caisson Laboratories, Inc.

Frequently Asked Questions

The cell culture media market is projected to reach US$5.3 billion in 2026.

Rising biologics production, expanding cell and gene therapy development, and increasing adoption of serum-free bioprocessing systems are driving growth in the cell culture media market.

The cell culture media market is poised to witness a CAGR of 13.6% from 2026 to 2033.

Expansion of chemically defined media, increasing regenerative medicine investments, and growing demand for scalable cell therapy manufacturing platforms are creating key opportunities in the cell culture media market.

Some of the key market players include Thermo Fisher Scientific, Merck KGaA, Danaher Corporation, Sartorius AG, and Lonza Group.