- Medical Devices

- U.S. Automated CPR Device Market

U.S. Automated CPR Device Market Size, Share, and Growth Forecast, 2025 - 2032

U.S. Automated CPR Device Market By Product Type (Piston CPR Devices, Load-Distributing Band (LDB) Devices, Others), Power Source (Battery-driven, Electrically-driven), End-user (Hospitals, Emergency Medical Services, Others), and Regional Analysis for 2025 - 2032

U.S. Automated CPR Device Market Size and Trends Analysis

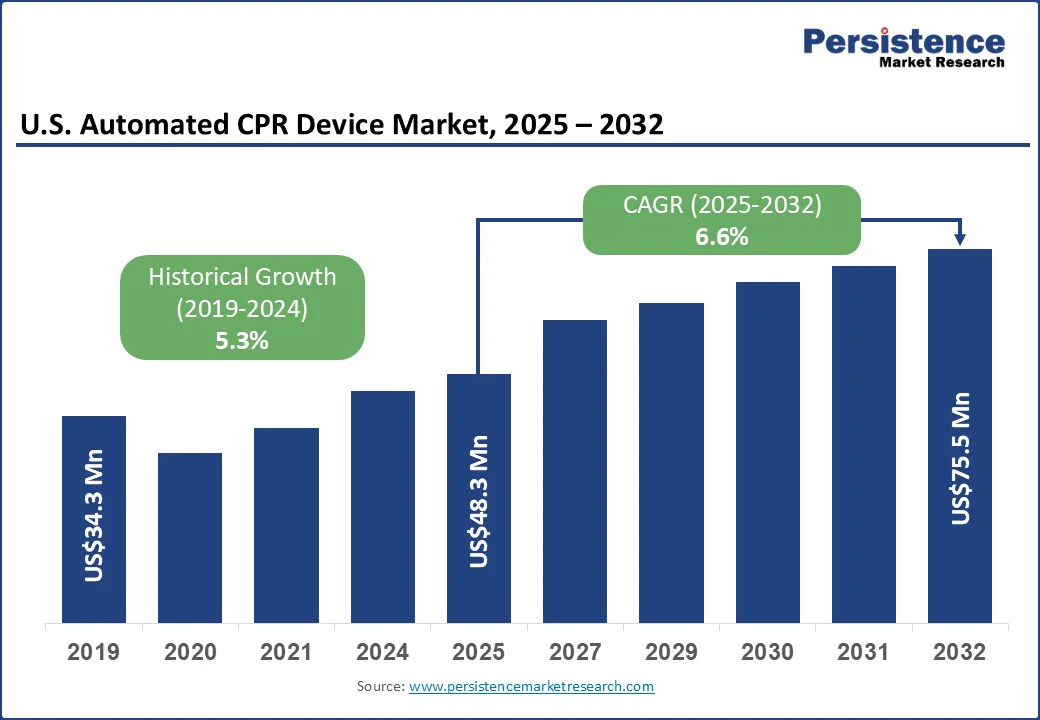

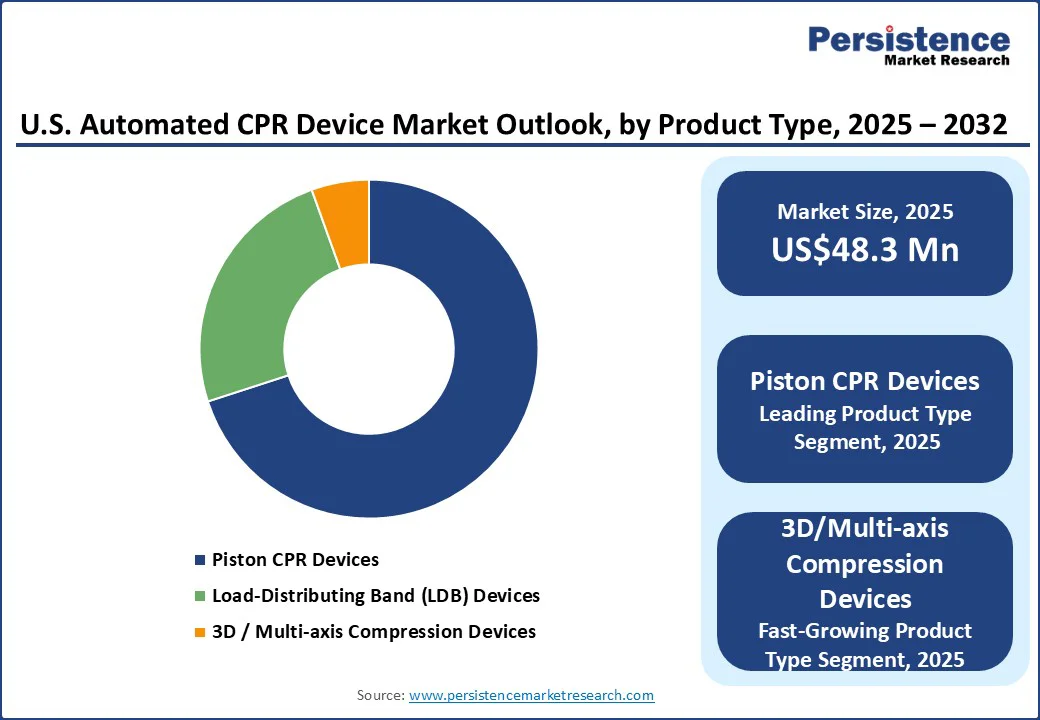

The U.S. automated CPR device market size is likely to be valued at US$48.3 Mn in 2025 and is expected to reach US$75.5 Mn by 2032, growing at a CAGR of 6.6% during the forecast period from 2025 to 2032, driven by the rising prevalence of cardiovascular diseases, increasing out-of-hospital cardiac arrests, and a growing emphasis on timely, high-quality resuscitation. The expanding geriatric population, higher incidence of comorbidities such as hypertension and heart failure, and supportive clinical research validating automated CPR devices’ effectiveness are further boosting adoption.

Key Industry Highlights

- Fastest-Growing Product Type: 3D/multi-axis and hybrid CPR devices are expanding rapidly, due to improved physiological compression, enhanced perfusion, and increasing adoption in pilot hospital programs and EMS trials.

- Power Source Leader: Battery-driven is anticipated to account for about 80.5% of the market share in 2025, driven by the high prevalence of cardiovascular emergencies, growing EMS adoption, and supportive clinical evidence demonstrating improved survival with automated chest compressions.

- Dominant End-user: Emergency Medical Services (EMS) is expected to account for 52.3% of the market share in 2025, fueled by portability, rapid deployment requirements, and widespread integration into ambulance and first-responder protocols.

- Emerging Opportunity: AI-enabled feedback systems, portable battery-driven units, and hospital-integrated solutions are gaining attention, driven by demand for real-time monitoring, workflow integration, and enhanced patient outcomes.

| Key Insights | Details |

|---|---|

|

U.S. Automated CPR Device Market Size (2025E) |

US$48.3 Mn |

|

Market Value Forecast (2032F) |

US$75.5 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

6.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

High Adoption by EMS and Hospitals

The adoption of automated CPR devices by Emergency Medical Services (EMS) and hospitals in the U.S. has been significantly increasing due to their ability to deliver consistent, high-quality chest compressions during cardiac emergencies. A study analyzing data from 2010 to 2016 revealed that the use of mechanical CPR devices in out-of-hospital cardiac arrest cases treated by EMS professionals increased more than fourfold, from 1.9% in 2010 to 8.0% in 2016. This rise was particularly notable among older adults and in suburban areas.

The American Heart Association emphasizes that immediate CPR can triple the chance of survival, highlighting the importance of timely and effective resuscitation. Mechanical CPR devices, such as the LUCAS and AutoPulse, are designed to provide continuous compressions without fatigue, allowing EMS personnel to focus on other critical aspects of patient care. These devices have become integral in improving patient outcomes during cardiac arrests.

Limited Reimbursement Policies

Limited reimbursement policies significantly hinder the adoption of automated CPR devices in the U.S., as Medicare and Medicaid impose stringent coverage requirements, often restricting reimbursement to devices classified as "reasonable and necessary" under narrowly defined clinical conditions. For instance, Medicare's Durable Medical Equipment (DME) benefit under Social Security Act §1861(s)(6) requires that equipment meet Local Coverage Determination (LCD) criteria to be eligible for reimbursement. This means that mechanical CPR devices, which are not universally recognized as standard care, may not be reimbursed unless they meet these stringent criteria.

Additionally, Medicaid reimbursement policies vary by state, with many states paying the lesser of either the charges for services, the Medicare rate, or the maximum price allowed by the state, further complicating the reimbursement landscape for EMS providers and hospitals. These inconsistent and restrictive reimbursement policies create financial barriers, especially for smaller EMS agencies and hospitals, limiting the widespread adoption of these life-saving devices.

Integration with Advanced Monitoring Systems

Integration with Advanced Monitoring Systems presents a significant opportunity in the market. Combining automated chest compression devices with real-time monitoring systems enhances the quality and effectiveness of resuscitation efforts. For instance, ZOLL's AutoPulse Resuscitation System integrates with the X Series Advanced Monitor/Defibrillator, enabling synchronized shocks during CPR and continuous monitoring of patient parameters. This integration allows immediate adjustments to compression depth and rate based on real-time data, optimizing coronary perfusion and increasing the likelihood of survival.

Similarly, Stryker's LUCAS 3 chest compression system delivers consistent compressions with a depth of 5.3 cm and a rate of 102 per minute, aligning with current CPR guidelines. These advancements in automated CPR technology, coupled with integration into comprehensive monitoring systems, are expected to drive market growth by improving patient outcomes and operational efficiency in emergency medical services and hospital settings.

Category-wise Analysis

Product Type Insights

Piston CPR Devices are projected to lead the market with a 70.7% share in 2025, due to their proven effectiveness, reliability, and widespread adoption in EMS and hospital settings. Devices such as Stryker’s LUCAS and Defibtech’s Lifeline ARM deliver consistent chest compressions with adjustable depth and rate, maintaining coronary perfusion and reducing provider fatigue during extended resuscitations. Their ease of use and integration into EMS protocols and hospital emergency departments have further reinforced their prevalence.

Regulatory approvals from the FDA ensure safety and efficacy, making them a trusted choice among healthcare providers. With the rising prevalence of cardiovascular diseases, an aging population, and ongoing technological advancements, piston CPR devices continue to lead the market, offering superior patient outcomes and becoming the preferred solution for both pre-hospital and in-hospital cardiac emergencies.

Power Source Insights

Battery-driven devices dominate the market due to their portability, ease of use, and the ability to deliver consistent compressions in diverse emergency settings. EMS personnel and hospital staff favor battery-powered units because they do not rely on a continuous electrical supply, making them ideal for ambulances, remote locations, and during patient transport.

Modern battery technologies provide sufficient operational time for prolonged resuscitation efforts, ensuring reliability when every second counts. Additionally, battery-driven devices are lightweight and easier to deploy quickly, reducing setup time during critical cardiac emergencies. The combination of mobility, flexibility, and consistent performance makes battery-powered automated CPR devices the preferred choice, driving their leading market share in both pre-hospital and hospital environments.

Competitive Landscape

The U.S. automated CPR device market is competitive, led by players such as ZOLL Medical Corporation, Stryker, SCHILLER Americas Inc., Defibtech, and Michigan Instruments. These companies focus on device reliability, multi-axis or piston compression technology, portability, and integration with EMS and hospital protocols, while emerging players emphasize affordability, battery-driven solutions, AI-guided feedback, and ease of use to cater to pre-hospital, in-hospital, and specialty clinic settings, targeting both emergency responders and healthcare facilities.

Key Industry Developments

- In November 2024, STARS, the air ambulance service, deployed automated CPR machines on its emergency flights to enhance patient care. These devices delivered consistent, high-quality chest compressions, reducing fatigue for medical personnel and improving the chances of survival during in-flight cardiac emergencies.

- In March 2024, Stryker launched its next-generation “LIFEPAK CR2 AED” and an “Evacuation Chair” at Criticare 2024 to advance cardiac care and emergency preparedness. The LIFEPAK CR2 AED provided rapid, easy-to-use defibrillation with enhanced diagnostics, improving outcomes during sudden cardiac arrests.

Companies Covered in U.S. Automated CPR Device Market

- ZOLL Medical Corporation

- Stryker

- Michigan Instruments

- SCHILLER Americas Inc.

- Defibtech

- Weinmann Emergency

- Allied Medical LLC

- Nihon Kohden Corporation

Frequently Asked Questions

The U.S. automated CPR device market is projected to be valued at US$48.3 Mn in 2025.

Rising cardiac arrests, aging population, EMS adoption, technological advancements, and regulatory support drive market growth.

The U.S. automated CPR device market is poised to witness a CAGR of 6.6% between 2025 and 2032.

Integration with monitoring systems, portable devices, AI feedback, non-hospital deployment, and enhanced training programs offer growth opportunities.

Major players in the U.S. automated CPR device market are ZOLL Medical Corporation, Stryker, Michigan Instruments, SCHILLER Americas Inc., and Defibtech.