- Inks, Coatings, Adhesives & Sealants (ICAS)

- Packaging Additives Market

Packaging Additives Market Size, Share, and Growth Forecast, 2025 - 2032

Packaging Additives Market By Additive Type (Antimicrobial Additives, Anti-fog Additives), Packaging Material (Plastic, Paper & Paperboard Packaging), Application, and Regional Analysis for 2025 - 2032

Packaging Additives Market Size and Trends Analysis

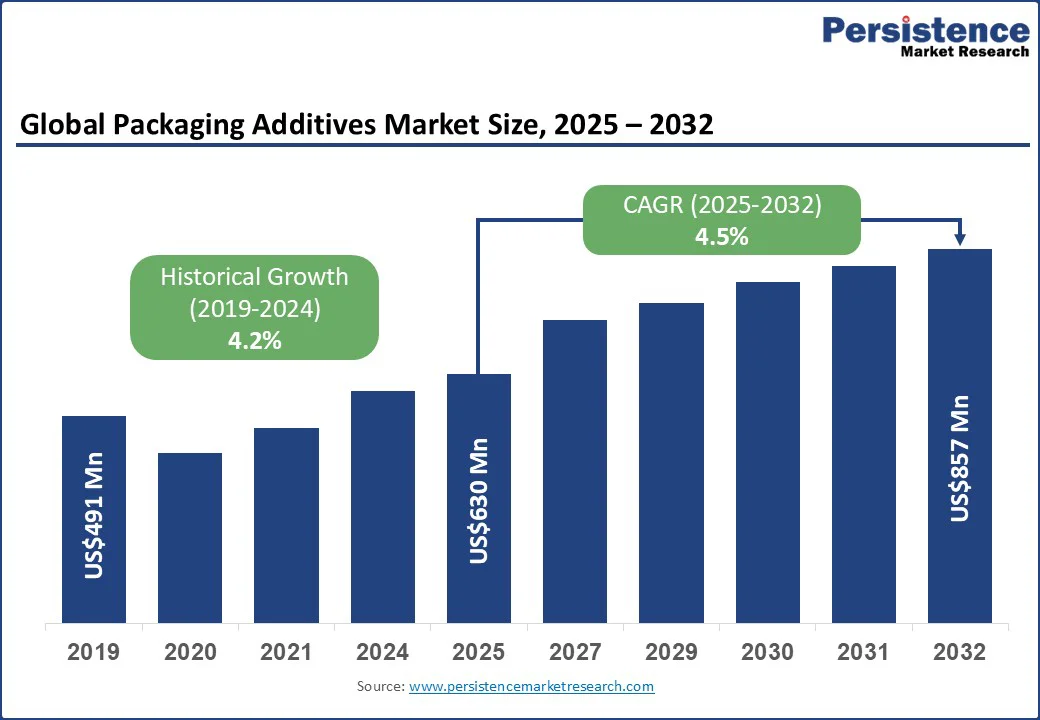

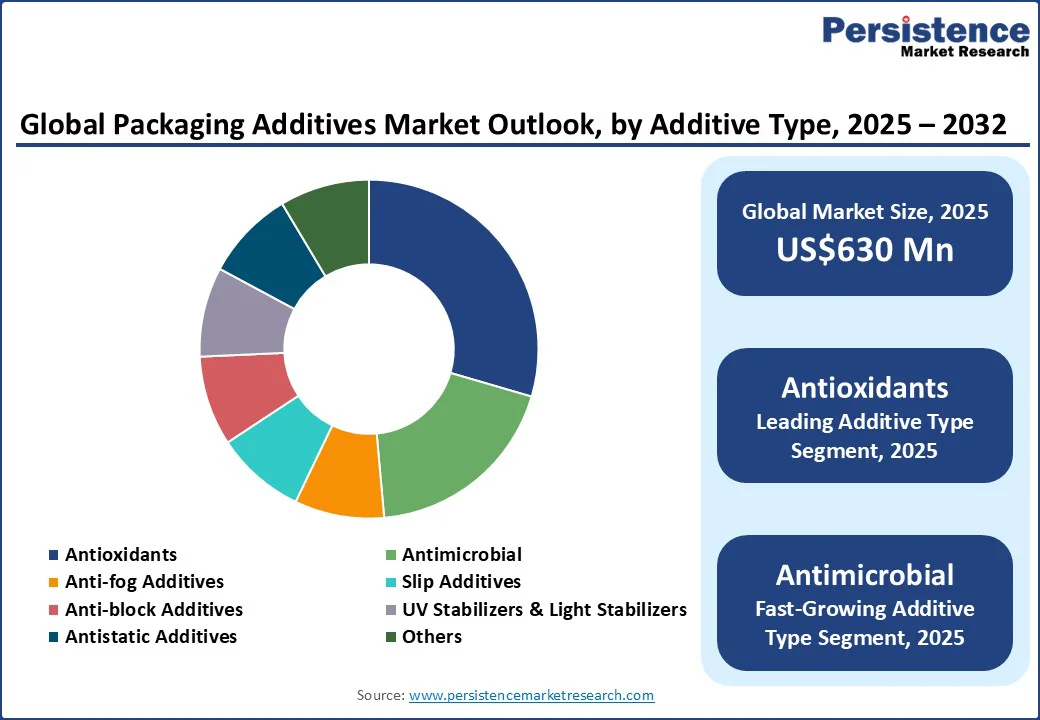

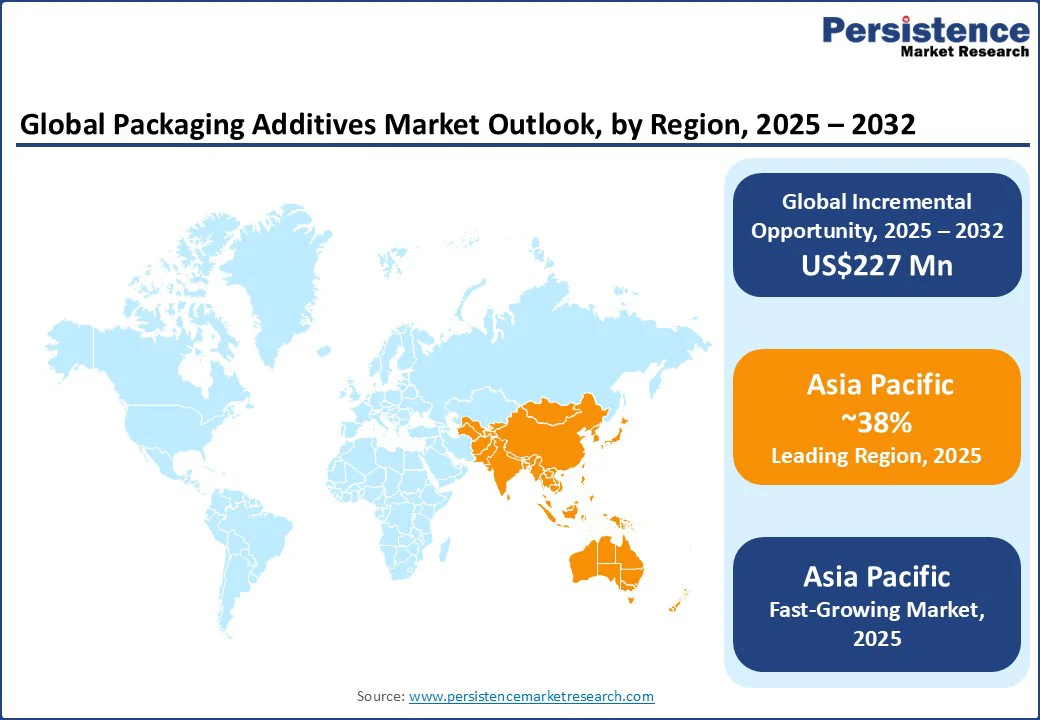

The global packaging additives market size is likely to be valued at US$630 Mn in 2025 and is expected to reach US$857 Mn by 2032, growing at a CAGR of 4.5% during the forecast period from 2025 to 2032.

Key Industry Highlights:

- Leading Region: Asia Pacific with a 38% market share in 2025, driven by rapid industrialization, strong plastics processing capacity in China, and rising demand for sustainable packaging in India.

- Fastest-growing Region: Asia Pacific projected to expand at a high CAGR, supported by government-led sustainability policies and growth in food and pharmaceutical packaging sectors.

- Dominant Additive Type: Antioxidants holding nearly 30.7% share in 2025, as they prevent oxidation, discoloration, and nutrient degradation.

- Leading Packaging Material: Plastic Packaging capturing around 42.1% market share in 2025, owing to its versatility and compatibility with multiple additive functions such as UV protection, antistatic properties, and oxygen scavenging.

| Global Market Attribute | Key Insights |

|---|---|

| Packaging Additives Market Size (2025E) | US$630 Mn |

| Market Value Forecast (2032F) | US$857 Mn |

| Projected Growth (CAGR 2025 to 2032) | 4.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.2% |

Packaging additives play a vital role in enhancing the performance, safety, and shelf life of packaged goods by improving barrier properties, durability, and visual appeal. These additives, which include anti-fog agents, antimicrobial solutions, slip modifiers, and UV stabilizers, are increasingly in demand across food & beverages, pharmaceuticals, and consumer goods industries.

Market Dynamics

Driver - Advancing Packaging Performance through Nano-Tech, Bio-Based Compatibility & AI Innovation

One of the key growth drivers in the packaging additives market is the adoption of nano-silica-based thin-film oxygen barrier enhancement technologies. By integrating nano-silica particles into packaging films, manufacturers can achieve superior oxygen and moisture barrier performance while reducing overall material use through lightweighting.

This approach improves shelf stability and product freshness, and also helps companies meet sustainability mandates by lowering raw material consumption and associated carbon emissions.

Another important driver is the rising use of plant-derived compatibilizers to enhance recyclability in mixed-material packaging. Multi-layer packaging often combines incompatible polymers such as PET and PE, making recycling a challenge. Bio-based compatibilizers improve polymer bonding, reducing contamination during the recycling process and supporting the transition toward circular packaging systems.

With FMCG companies setting ambitious targets for 100% recyclable packaging, demand for these specialized additives is expected to accelerate. Growing attention on clean-label and eco-friendly packaging has also created opportunities for biodegradable antimicrobial thyme-oil packaging coatings. These plant-extract-based additives inhibit microbial growth without relying on synthetic chemicals, aligning with stricter food safety regulations and consumer preferences for natural solutions.

Restraints - Material Instability & Integration Challenges in Natural Additive Systems

The packaging additives market faces limitations linked to the thermal instability of biodegradable wax-based coating systems. Natural waxes, such as beeswax and candelilla wax, are increasingly explored as sustainable coating materials, but their relatively low melting points make them vulnerable to softening and migration when exposed to temperature variations.

This instability often reduces adhesion and abrasion resistance, while also affecting coating uniformity during large-scale application. As a result, packaging manufacturers encounter difficulties in integrating these coatings into industrial processes that require consistent performance across different supply chain environments.

Another challenge is the dispersion inconsistency of volatile essential oils in antimicrobial packaging films. Plant-based compounds, including thyme essential oil, are gaining traction for their natural antimicrobial properties, yet their integration into polymer matrices such as chitosan or pectin can be problematic.

Incomplete incorporation often leads to oil-rich clusters or surface irregularities within the film, undermining its barrier effectiveness and controlled release mechanism. These inconsistencies can also alter the sensory attributes of packaged goods, raising concerns for food and beverage companies that aim to balance product protection with consumer acceptance.

Opportunity - Smart Biodegradable Additives and Controlled-Release Technologies Driving Next-Gen Packaging

The shift toward sustainable materials is creating strong opportunities for functional biodegradable plastic additives that enhance the compostability of PLA and PHA packaging. Bio-derived plasticizers, nucleating agents, and antioxidants are being developed to improve flexibility and durability in bioplastics while ensuring compliance with compostability certifications.

This innovation allows bioplastic packaging to perform on par with traditional polymers in areas such as flexible films and food containers, giving brand owners a path to reduce reliance on conventional plastics without compromising functionality or end-of-life sustainability goals.

Another promising avenue lies in mesoporous silica-based controlled-release additives for active packaging. These advanced systems enable the gradual release of natural antioxidants and antimicrobial agents, helping extend the shelf life of perishable goods.

By embedding compounds such as curcumin or essential oils within structured carriers such as mesoporous silica or cyclodextrin complexes, manufacturers can achieve stability and timed release that traditional additives cannot provide. This opens up significant growth potential in premium food and healthcare packaging, where demand for intelligent, shelf-life-extending solutions is rapidly accelerating.

Category-wise Analysis

Additive Type Insights

Antioxidants are expected to account for the largest share of around 30.7% in 2025. Their role in preventing oxidation, discoloration, and nutrient degradation makes them indispensable in food, beverage, and pharmaceutical packaging.

As consumption of processed and ready-to-eat products expands, particularly in urban markets, antioxidants remain the most widely adopted solution to ensure product stability and safety. For example, producers of pre-packaged salads often use antioxidant-enhanced PET films to maintain freshness and extend distribution cycles without compromising visual quality.

In contrast, antimicrobial additives are emerging as the fastest-growing segment. Growing awareness of foodborne illnesses and the need for contamination control in healthcare packaging are driving investments in antimicrobial technologies.

These additives, which include natural compounds and advanced materials such as silver nanoparticles, actively suppress microbial growth on packaging surfaces. Their relevance has risen sharply in sectors such as fresh meat packaging, where antimicrobial films help extend shelf life and address consumer concerns around hygiene and product safety.

Packaging Material Insights

Plastic remains the dominant packaging material in the additives market, holding 42.1% of market share. Its widespread use is driven by versatility, lightweight properties, and cost efficiency across both rigid and flexible formats.

Plastic is the preferred substrate in applications ranging from snack wrappers to pharmaceutical blister packs, making it central to the adoption of additives that enhance clarity, durability, and barrier performance. For instance, polyethylene films treated with slip and anti-block additives allow processors to achieve faster manufacturing speeds while ensuring smooth handling during storage and transport.

At the same time, biodegradable and bio-based packaging materials represent the fastest-growing segment. Increasing regulatory pressure to reduce plastic waste, combined with consumer demand for sustainable packaging, has accelerated the adoption of solutions based on PLA, PHA, and starch blends.

Additives play a critical role here by improving flexibility, strength, and shelf-life performance without compromising compostability standards. A notable example is the use of biodegradable plasticizers and antioxidants in PLA snack bags, which deliver both eco-friendly credentials and the performance characteristics needed for mass-market adoption.

Regional Insights

Asia Pacific Packaging Additives Market Trends - Rapid Growth Anchored in Industrial Scale and Regulatory Momentum

Asia Pacific is the largest and fastest-growing regional market for packaging additives, holding the largest share of around 38% in 2025. The market is being driven by rapid urbanization, food safety concerns, and government-led sustainability initiatives.

China, with its advanced plastics processing industry, is investing heavily in both traditional and green additive solutions. Recent expansions by Clariant, including new stabilizer and antioxidant facilities in Cangzhou and Hebei, highlight the country’s role as a production hub for multifunctional packaging additives.

At the same time, nationwide policies restricting single-use plastics are driving demand for biodegradable and recyclable additive technologies. This combination of industrial capacity and regulatory push positions China as a critical growth engine for the global market.

India is also emerging as a major contributor, with its packaging industry projected to reach over US$200 Bn by 2025. Rising demand from the food, beverage, and pharmaceutical sectors is creating strong interest in additives that enhance product safety, such as UV-resistant coatings and oxygen scavengers.

Indian companies are also exploring biodegradable solutions as the government strengthens its stance on plastic waste reduction. Partnerships with global innovators, such as Polymateria’s efforts to introduce real-world biodegradable plastic technology, highlight India’s importance as both a growth market and a testing ground for next-generation additive solutions.

North America Packaging Additives Market Trends - Innovation-Driven Growth Backed by Clean-Label and Sustainable Shifts

North America is supported by its strong food, beverage, pharmaceutical, and e-commerce sectors. The region is also a hub for innovation, with companies developing advanced solutions to meet growing demand for sustainability and performance. In the U.S., consumer and regulatory pressures are pushing food manufacturers toward cleaner formulations.

Major brands such as Kraft Heinz and General Mills have started eliminating artificial dyes, which has opened opportunities for natural color stabilizers and clean-label packaging additives. At the same time, new bio-based solutions such as BASF’s Envalox R-series are gaining attention for improving the recyclability and performance of biodegradable plastics, reflecting a broader industry shift toward sustainable packaging technologies.

Canada is following a similar path but with an even stronger emphasis on environmental policy. National sustainability targets are encouraging the adoption of compostable and PFAS-free packaging solutions. Aqueous coatings and biodegradable additives are being trialed in paper and fiber packaging to meet new regulatory requirements.

This policy-driven approach has made Canada an attractive market for eco-friendly additive innovation, with packaging producers collaborating closely with government-backed initiatives to reduce plastic waste.

Europe Packaging Additives Market Trends - Policy-Led Sustainability Fueled by Circular Economy

Europe continues to lead in sustainable packaging innovation, underpinned by ambitious circular economy policies and consumer demand for eco-friendly solutions. Germany plays a central role in developing high-performance additives that enable recyclable and mono-material packaging formats.

Global players operating in Germany are increasingly investing in bio-based adhesives and barrier coatings, which allow packaging manufacturers to meet strict EU Green Deal targets and Extended Producer Responsibility (EPR) obligations. These solutions are gaining importance as brand owners look for ways to balance product safety with recyclability.

In the U.K., the spotlight is on innovative start-ups that are reimagining packaging materials. Xampla, for example, has secured US$14 Mn in funding to expand its plant-protein-based films that mimic the strength and barrier properties of plastic while remaining biodegradable. These films are already being tested by major food service companies such as Just Eat and Huhtamaki, signaling strong commercial interest.

Polymateria’s Lyfecycle additive technology, which enables polyolefins to break down under real-world conditions, is being scaled up to address persistent plastic waste. Together, these developments show how Europe is combining regulatory leadership with entrepreneurial innovation to accelerate the adoption of sustainable packaging additives.

Competitive Landscape

The global packaging additives market is moderately consolidated, with global chemical companies and specialized additive producers competing through product innovation, sustainability initiatives, and regional expansion. Key players such as BASF SE, Clariant AG, Dow, Evonik Industries, and Songwon Industrial dominate with broad portfolios of stabilizers, antimicrobial agents, and performance enhancers.

These companies are increasingly focusing on developing bio-based and recyclable additive solutions, often collaborating with packaging converters and FMCG brands to accelerate adoption. Strategic investments in capacity expansion, such as Clariant’s new stabilizer plants in China, demonstrate how leading firms are strengthening their global supply chains to meet rising demand.

Regional and niche players are also carving out opportunities by offering specialized, application-specific additives. For example, start-ups such as Xampla and Polymateria are introducing novel biodegradable additive technologies that align with emerging sustainability mandates.

Similarly, companies in the Asia Pacific are leveraging cost-efficient production and proximity to end-user industries to expand their presence in global supply chains. Competitive dynamics are therefore shaped by scale and also by the ability to innovate in line with sustainability, food safety, and performance-driven packaging requirements, making the market a blend of established leaders and agile disruptors.

Key Industry Developments:

- In April 2025, Dow launched its INNATE TF 220 Precision Packaging Resin, a BOPE film-based solution designed to boost recyclability without sacrificing performance. This resin, augmented with 10 % post-consumer recycled (PCR) plastic, was pilot-tested in China with Liby’s “Floral Era” detergent line.

- In August 2024, Xampla partnered with Lehmann Ingredients to distribute its plant-based microencapsulation technology across the U.K. food and beverage sector, enabling nutrient fortification with greater stability and reduced need for overage.

Companies Covered in Packaging Additives Market

- BASF SE

- Dow Inc.

- Clariant AG

- Evonik Industries AG

- Ampacet Corporation

- Avient Corporation

- Milliken & Company

- PolyOne Corporation (now Avient)

- Songwon Industrial Co., Ltd.

- Kaneka Corporation

- Arkema Group

- Solvay S.A.

- Flint Group

- Henkel AG & Co. KGaA

- AkzoNobel N.V.

- ALTANA AG

- Croda International Plc

- Eastman Chemical Company

- Huber Group

- PPG Industries Inc.

Frequently Asked Questions

The packaging additives market is expected to reach US$630 Mn in 2025.

By 2032, the market is projected to grow to US$857 Mn, reflecting steady adoption across industries.

Key trends include the rise of sustainable and bio-based additives, increasing adoption of active and intelligent packaging, innovations in UV-resistant and oxygen-scavenging technologies, and a strong push for circular economy packaging solutions.

The antioxidant segment leads the market, driven by demand for longer shelf life and enhanced food safety. By material, plastic packaging dominates due to its widespread use and compatibility with functional additives.

The market is expected to grow at a CAGR of 4.5% from 2025 to 2032, supported by sustainability mandates and performance-driven packaging demand.

Some major companies with strong portfolios include BASF SE, Dow Inc., Clariant AG, Evonik Industries AG, and Avient Corporation.