- Smart Packaging

- Retail Glass Packaging Market

Retail Glass Packaging Market Size, Share, and Growth Forecast, 2025 - 2032

Retail Glass Packaging Market by Product Type (Bottles, Jars, Miscellaneous), Material Type (Standard Glass, Light-weighted Glass, Recycled Glass (Cullet-Based), Speciality Glass), Application (Food & Beverage, Personal Care & Cosmetics, Pharmaceutical, Miscellaneous), and Regional Analysis for 2025 - 2032

Retail Glass Packaging Market Size and Trends Analysis

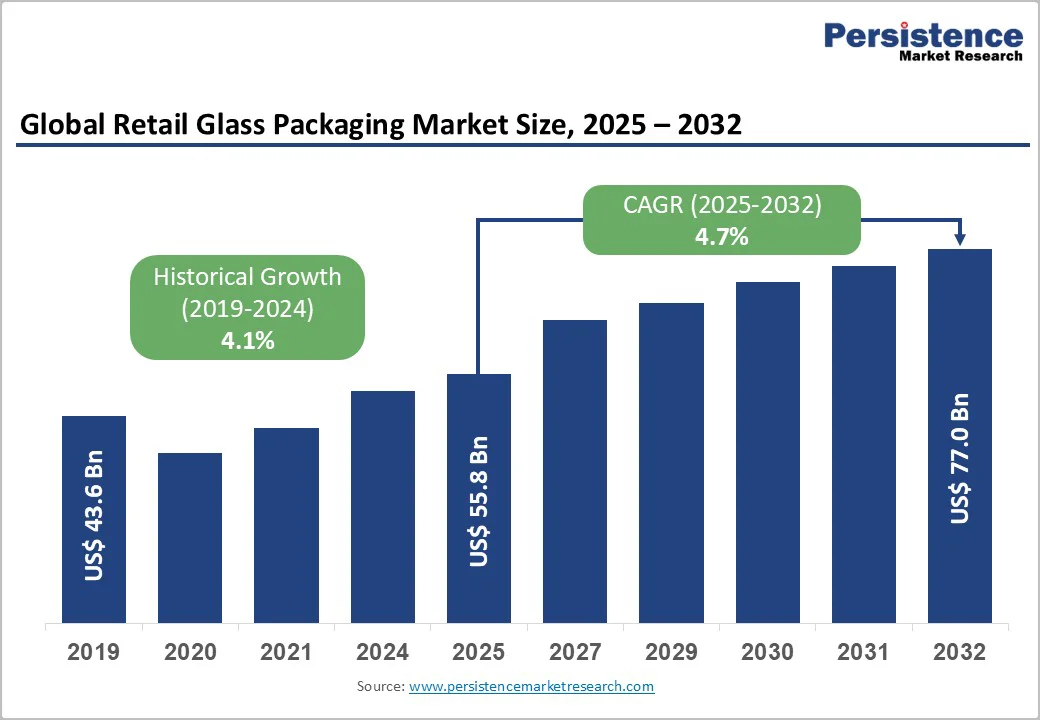

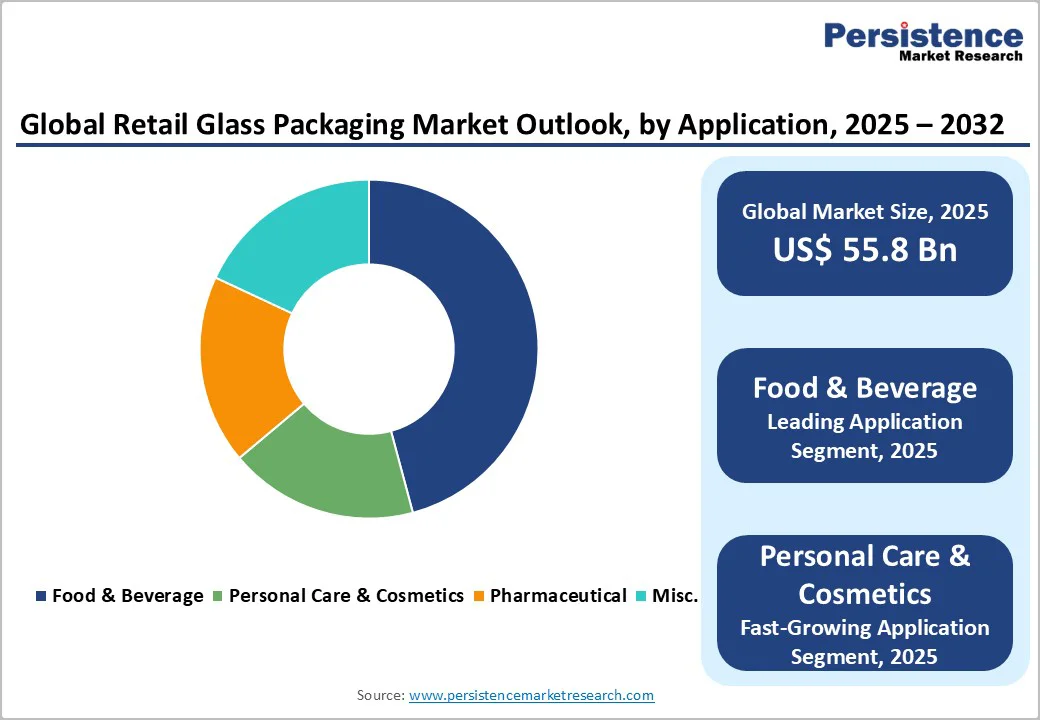

The global retail glass packaging market size is valued at US$55.8 billion in 2025 and is projected to reach US$77.0 billion, growing at a CAGR of 4.7% between 2025 and 2032.

Market expansion is fundamentally driven by rising regulatory pressures to eliminate single-use plastic packaging, intensifying consumer demand for sustainable packaging solutions, and pharmaceutical sector consolidation around injectable delivery systems requiring premium glass containment.

Additionally, premiumization trends across beverage, cosmetics, and food sectors position glass as an aspirational packaging material that enhances brand positioning while meeting stringent environmental compliance frameworks.

Key Industry Highlights:

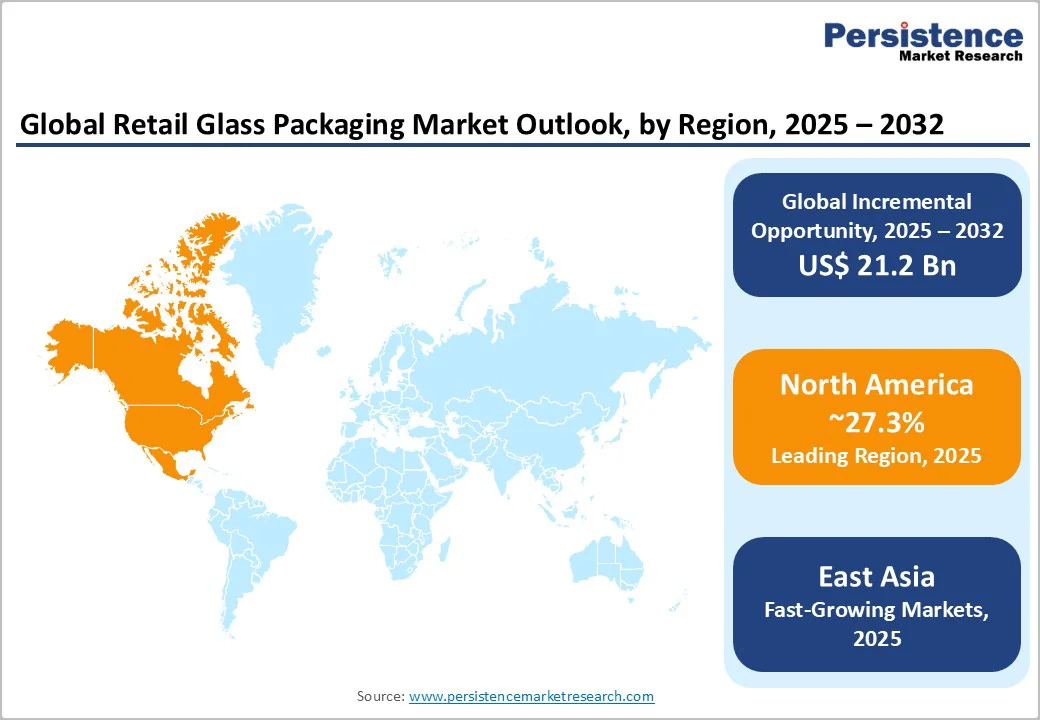

- Regional Dominance: East Asia leads the global retail glass packaging market with ~23.4% share in 2025, driven by China’s large beverage, spirits, and food processing industries, while North America (27.3%) and Europe (19.4%) maintain strong positions supported by established recycling infrastructure and stringent regulatory frameworks.

- Leading Product Type: Bottles dominate with 77.8% market share in 2025 due to their extensive use in beverages, food, and pharmaceuticals, whereas jars emerge as the fastest-growing segment, fueled by premium personal care, cosmetics, and specialty food applications.

- Dominant End-user: Food & Beverage applications hold the largest revenue share at 74.5% in 2025, while Personal Care & Cosmetics represent the fastest-growing category, driven by consumer preference for sustainable, chemically inert, and premium packaging solutions.

- Regulatory Push: Regulatory mandates, including the EU’s single-use plastics Directive and India’s Extended Producer Responsibility (EPR) rules, are accelerating glass adoption, reshaping packaging strategies for global beverage and food brands.

- Recycling Investments: Advanced recycling infrastructure in Europe achieves ~80.8% glass collection rates, while India’s ongoing initiatives and CSIR-backed programs are fostering collection, sorting, and cullet supply, creating market opportunities in emerging regions.

- Premiumization Trend: Rising consumer awareness and willingness to pay price premiums (15-25%) for sustainable and aesthetically distinctive packaging are driving adoption in high-value beverages, cosmetics, and artisanal foods.

| Key Insights | Details |

|---|---|

| Retail Glass Packaging Market Size (2025E) | US$ 55.8 Bn |

| Market Value Forecast (2032F) | US$ 77.0 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.1% |

Market Dynamics

Drivers - Regulatory Mandates for Single-Use Plastic Elimination

Regulatory frameworks across developed and emerging economies are systematically restricting single-use plastic packaging, establishing a structural tailwind for the retail glass packaging market.

The European Union's Single-Use Plastics Directive mandates the reduction of identified single-use items, while India has implemented comprehensive bans on multiple plastic formats with Extended Producer Responsibility rules for glass, paper, and metal packaging set for implementation in April 2026.

The United States exhibits fragmented but accelerating state-level restrictions on plastic packaging in food service and retail contexts. According to government waste management data, the EU achieved a 75.6% glass recycling rate by 2021, with a 2030 target of 75% minimum recycling, creating regulatory incentives for manufacturers to transition from plastic to glass.

These legislative transitions create immediate compliance pressures on packaged-goods companies and contract manufacturers to shift toward glass containers, directly boosting demand within the Retail Glass Packaging Market, with pharmaceutical, food and beverage, and personal care segments leading adoption acceleration.

Infrastructure investments across regions, including advanced glass sorting and recycling facilities, strengthen market fundamentals by reducing recycled glass sourcing costs and improving manufacturing economics.

Consumer Preference for Sustainable and Inert Packaging Materials

Demographic and psychographic shifts toward environmental consciousness and health-protective consumption patterns substantially amplify demand for glass as a premium packaging material.

Glass exhibits inherent properties of infinite recyclability without quality degradation, inert chemical composition preventing product contamination, and complete recyclability through established infrastructure.

Consumer research demonstrates premium-segment willingness to pay 15-25% price premiums for sustainable packaging alternatives in personal care, spirits, and specialty foods. The Retail Glass Packaging Market benefits from this behavioral shift, particularly in developed economies where environmental awareness correlates with purchasing intent.

India's personal care segment exhibits accelerating adoption of traditional and natural products in glass containers, driven by consumer preference for chemical-free solutions and alignment with Ayurvedic wellness traditions.

European market research indicates 68% of consumers factor sustainability into packaging choices, with glass preferred for its infinite recyclability and absence of microplastic shedding. This consumer-driven demand supports market expansion, with the fastest growth occurring in premium personal care and beverage segments where packaging aesthetics and sustainability messaging influence purchasing decisions.

Digital retail channels amplify this trend, as e-commerce platforms highlight sustainability credentials, enabling smaller artisanal brands to differentiate through glass packaging.

Restraint - High Energy Consumption and Manufacturing Cost Structure

Glass production operates at thermal scales of 1400-1600°C, rendering the manufacturing process substantially more energy-intensive than alternative packaging materials, including plastic and aluminum.

Raw material costs for silica sand, soda ash, limestone, and cullet (recycled glass) remain elevated, with soda ash pricing directly tied to natural gas volatility and energy market fluctuations. Energy consumption in glass manufacturing accounts for approximately 12-15% of total production costs, compared to 3-5% for plastic molding.

The retail glass packaging market experiences margin compression during periods of energy price volatility, with energy cost pressures reducing manufacturer profitability despite demand growth.

Glass manufacturing also generates higher per-unit production costs for lightweight designs, offsetting sustainability benefits with economic penalties that disproportionately impact price-sensitive food and beverage segments. Supply chain disruptions and raw material procurement challenges further elevate costs, restricting market penetration in price-competitive categories where plastic alternatives maintain cost advantages of 30-40% per unit.

Opportunity - Premium Product Positioning and Brand Differentiation in Emerging Markets

Emerging economies across the Asia Pacific, particularly India and Southeast Asia, exhibit a rapid expansion of middle-income groups and rising per-capita consumer spending correlated with demand for premium, visually distinctive packaging.

The Indian packaging sector, valued at over US$86 billion in 2024 and growing at 22-25% annually, creates substantial white space for glass packaging innovation in premium beverage, spirits, and cosmetics categories. India's regulatory environment supporting 100% FDI through automatic routes has attracted US$1.74 billion in packaging sector investments (2000 - 2024), with glass packaging representing high-growth segments within this investment flow.

Circular Economy Adoption and Extended Producer Responsibility Frameworks

Government-mandated Extended Producer Responsibility (EPR) regulations, particularly India's draft EPR Rules 2024 with an implementation date of April 1, 2026, create structured incentive frameworks for glass packaging adoption and recycling infrastructure development.

These regulatory frameworks mandate that producers achieve defined recycling targets, reducing virgin material reliance and establishing a competitive advantage for manufacturers utilising recycled glass cullet.

The retail glass packaging market benefits from EPR compliance, driving demand for collection systems, sorting infrastructure, and quality-assured recycled glass, creating adjacent services markets.

Germany and France have deployed advanced recycling infrastructure achieving 80.8% glass recycling rates, creating model frameworks for adoption in emerging markets. Investment in recycling infrastructure including automated sorting, optical detection systems, and furnace-grade cullet processing enhances glass supply chain economics and reduces environmental footprint by 25-30% compared to virgin glass production.

The European Union's Circular Economy Action Plan mandates minimum recycled content requirements, potentially reaching 30-40% by 2030, creating market-defined demand for recycled glass infrastructure expansion. Within the Retail Glass Packaging Market, stakeholders establishing recycled content supply chains and demonstrating verifiable sustainability metrics gain competitive positioning with multinational brands adopting science-based sustainability targets.

Category-wise Analysis

Product Type Insights

Bottles represent the dominant product segment within the retail glass packaging market, commanding 77.8% share in 2025. This leadership reflects historical category dominance across beverage, spirits, and food categories, where glass bottles provide superior product presentation, preservation characteristics, and brand communication value.

Glass bottles provide inherent product differentiation through shape, colour, and embossing capabilities, enabling brands to create distinctive shelf presence and premium positioning. The beverage industry remains the largest application category for bottles, leveraging glass's thermal stability, inertness, and infinite recyclability to preserve product quality and communicate sustainability.

Food packaging applications-including oils, sauces, condiments, and preserved goods-further anchor bottles as the dominant category through established consumer expectations and regulatory approvals. Pharmaceutical bottle applications, though smaller by volume, command premium pricing structures due to Type I borosilicate requirements and stringent regulatory compliance specifications.

Jars represent the fastest-growing product segment within the Retail Glass Packaging Market, driven by accelerating demand from personal care, cosmetics, and speciality food categories emphasising premium positioning and sustainability.

Application Industry Insights

Food and beverage applications are dominant, commanding 74.5% share in 2025, reflecting established regulatory approvals, consumer familiarity, and superior performance characteristics in preservation, presentation, and sustainability. Beverage applications encompassing spirits, beer, non-alcoholic beverages, and specialty drinks represent the largest sub-segment, leveraging glass's thermal stability, product visibility, and premium brand positioning capabilities.

Glass preserves beverage flavor profiles, prevents oxidation through inert container composition, and communicates quality through distinctive packaging design. Food applications including oils, sauces, condiments, jams, and preserved goods utilise glass for superior preservation, regulatory compliance, and product quality assurance.

Regional Insights and Trends

East Asia Retail Glass Packaging Market Trends

East Asia commands the largest regional share within the retail glass packaging market, representing approximately 23.4% of global market valuation and emerging as the fastest-growing geographic segment.

China's beverage and alcohol sectors anchor glass packaging demand through massive domestic consumption and export-oriented manufacturing. Spirits production, including baijiu and premium grain alcohol, relies substantially on glass packaging for product preservation and brand positioning.

Beer manufacturing represents another substantial demand category, with Chinese breweries expanding premium segment positioning through glass bottle differentiation. Non-alcoholic beverage segments, including tea-based drinks, traditional medicine beverages, and specialty drinks, amplify category demand.

The food processing sector, encompassing oils, sauces, and preserved goods, utilizes glass extensively for regulatory compliance and product quality assurance across both domestic consumption and export markets.

Regulatory developments in East Asia amplify glass packaging positioning. China's comprehensive waste management initiatives and plastic restriction policies, announced at provincial levels, create compliance pressures on packaged-goods manufacturers to transition toward glass containers.

India's draft Extended Producer Responsibility Rules 2024 establish targets for glass packaging collection and recycling, creating structured incentive frameworks for manufacturer adoption.

Europe Retail Glass Packaging Market Trends

Europe represents approximately 19.4% of the Retail Glass Packaging Market, positioned as the third-largest geographic region with pronounced sustainability leadership and stringent regulatory frameworks supporting glass adoption.

Western Europe dominates regional demand, anchored by Germany, France, and Italy, representing the largest absolute markets with a combined market valuation exceeding US$18 billion. Germany produced 7.86 million tonnes of container glass in 2024, valued at approximately US$13.6 billion, supporting beverage, food processing, and pharmaceutical packaging applications.

German industry strength reflects technological leadership in glass manufacturing, advanced recycling infrastructure achieving 80.8% collection rates, and regulatory compliance frameworks enforcing glass packaging adoption through plastic restriction policies.

France's wine and Cognac bottle production represents a globally significant market segment, with premium spirits glass packaging commanding price premiums reflecting brand positioning and sustainability communication. Italy's food processing sector, encompassing olive oil, wine, and speciality foods, leverages glass extensively for product quality assurance and regulatory compliance.

Regulatory environment represents the most significant European market driver. The European Union's Packaging Waste Directive established minimum recycling targets of 60% for glass packaging by 2030, incentivising manufacturer investment in recycling infrastructure and recycled content product development.

The single-use plastics directive prohibits identified plastic items, including bags and containers, structurally transferring demand toward glass alternatives across food service and retail applications. Extended Producer Responsibility schemes throughout EU member states impose collection and recycling obligations on manufacturers, creating a competitive advantage for companies establishing closed-loop glass systems.

North America Market Trends

North America represents approximately 27.3% share, positioning the region as the second-largest geographic segment after the Asia Pacific. The Midwest region holds the largest market share within the U.S., leveraging well-established food processing infrastructure, agricultural supply chains, and manufacturing capacity supporting beverage and food packaging demand.

Strong pharmaceutical industry presence in the Northeast and California regions drives pharmaceutical glass packaging demand through biologic drug manufacturing, vaccine production, and injectable therapeutic development concentrated in these geographies.

Regulatory environment dynamics significantly influence the North American market trajectory. The U.S. Environmental Protection Agency established mandatory recycling infrastructure targets, with state-level regulations progressively restricting single-use plastics in food service and retail packaging. California, New York, and Massachusetts implemented particularly stringent restrictions on plastic packaging, creating regulatory tailwinds for glass adoption.

The Clean Seas Act and state-level ocean conservation initiatives amplify pressure on packaged-goods manufacturers to transition from plastic to glass containers. The region's robust recycling infrastructure-achieving approximately 31% glass recycling rates supports glass packaging economics through cullet availability and manufacturing cost reduction.

Regional market investments underscore growth trajectory. Owens-Illinois committed over US$600 million to expand North American operations, focusing on lightweight glass technology development and manufacturing capacity expansion in key regional markets.

Competitive Landscape

The global retail glass packaging market is consolidated, dominated by major players such as Owens-Illinois Inc., Ardagh Group S.A., Verallia, Vidrala S.A., and Bormioli Rocco S.p.A., who collectively control a significant share of production capacity and cater to leading beverage and spirits brands worldwide. These companies leverage large-scale manufacturing, advanced glassmaking technologies, and premium bottle design capabilities to maintain competitive advantages.

The market’s consolidation is reinforced by strategic mergers, acquisitions, and capacity expansions aimed at meeting sustainability targets like lightweighting and recycled cullet integration. Smaller regional players compete primarily on niche applications or localized demand, but the industry remains largely oligopolistic due to high capital intensity, stringent quality standards, and strong brand relationships.

Key Industry Developments

- Oct. 22, 2025, Ardagh Glass Packaging-North America expanded its retail glass packaging portfolio with the launch of a new 100ml premium liquor bottle designed and manufactured in the U.S. The addition strengthens its presence in the spirits segment by complementing its existing 50ml stock bottle line. The development reinforces Ardagh’s position as the largest domestic supplier of glass bottles to the U.S. spirits market, supporting brand differentiation through recyclable, high-quality glass solutions.

- March 13, 2025, O-I Glass announced a multi-horizon strategic roadmap aimed at strengthening its global glass packaging business, emphasizing cost competitiveness, network optimization, and profitable category expansion. The company raised its “Fit to Win” savings target to at least $650 million by 2027 while reaffirming its 2025 and 2027 financial guidance. The strategy positions O-I to grow its presence in attractive retail glass packaging segments through segmented customer strategies and geographic expansion initiatives.

Companies Covered in Retail Glass Packaging Market

- Owens-Illinois Inc.

- Ardagh Group S.A.

- Vidrala S.A.

- Vetropack Holding Ltd

- Gerresheimer AG

- Verallia

- Nihon Yamamura Glass Co., Ltd.

- Bormioli Rocco S.p.A.

- Consol Glass (Pty) Ltd

- Piramal Glass Limited

Frequently Asked Questions

The global retail glass packaging market is projected to be valued at US$ 55.8 bn in 2025.

The Bottles segment is expected to hold around 77.8% market share by Product Type in 2025, driven by.

The retail glass packaging market is expected to witness a CAGR of 4.7% from 2025 to 2032.

Regulatory mandates reducing single-use plastics, consumer preference for sustainable and inert packaging, and the pharmaceutical sector demand for injectable drug containers are the primary drivers of the Retail Glass Packaging market growth.

Premium product positioning in emerging markets, adoption of circular economy and EPR frameworks, and technological innovations in lightweight and specialised glass applications are the key market opportunities for the Retail Glass Packaging market.

The leading global players in the Retail Glass Packaging market include Owens-Illinois Inc., Ardagh Group S.A., Vidrala S.A., Vetropack Holding Ltd, and Gerresheimer AG.