- Smart Packaging

- Protective Packaging Market

Protective Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Protective Packaging Market by Product Type (Flexible, Foam, Others), Material (Paper & Paperboard, Plastic Foams, Others), Function, End-user, and Regional Analysis for 2026 - 2033

Protective Packaging Market Size and Trends Analysis

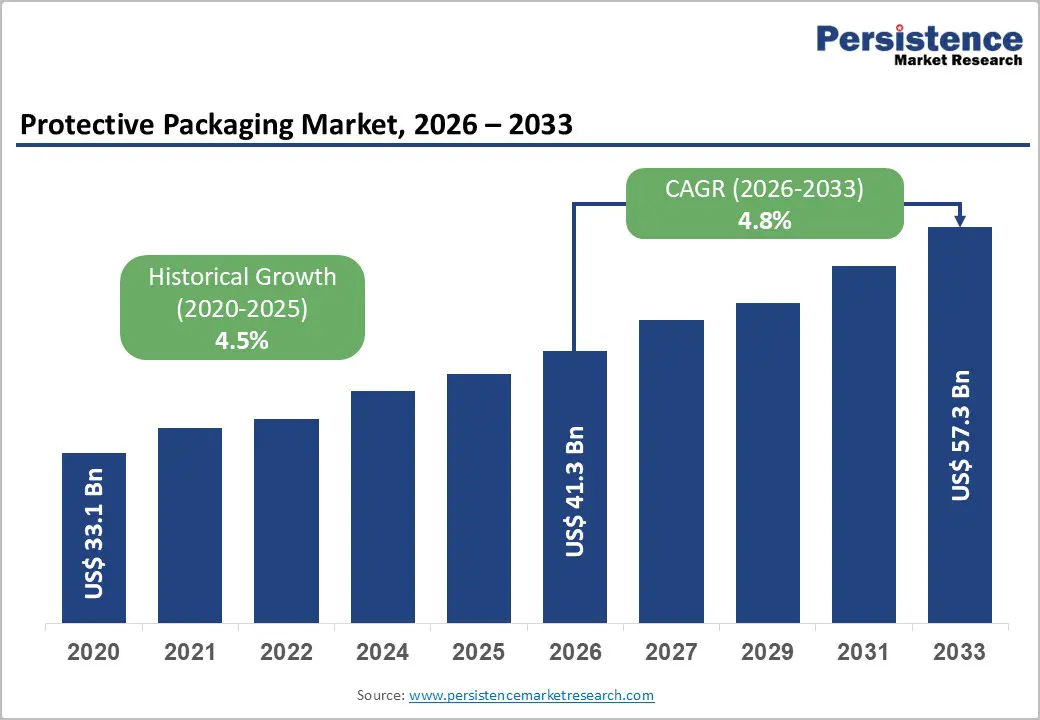

The global protective packaging market size is likely to be valued at US$41.3 billion in 2026 and is expected to reach US$57.3 billion by 2033, growing at a CAGR of 4.8% between 2026 and 2033, driven by the sustained expansion of e-commerce, increasing regulatory scrutiny on packaging waste, and the transition toward recyclable and lightweight materials. Rising parcel volumes and extended supply chains are increasing the risk of product damage, reinforcing the need for efficient protective solutions. Sustainability mandates are accelerating the adoption of paper-based and automation-compatible packaging formats across industries.

Key Industry Highlights:

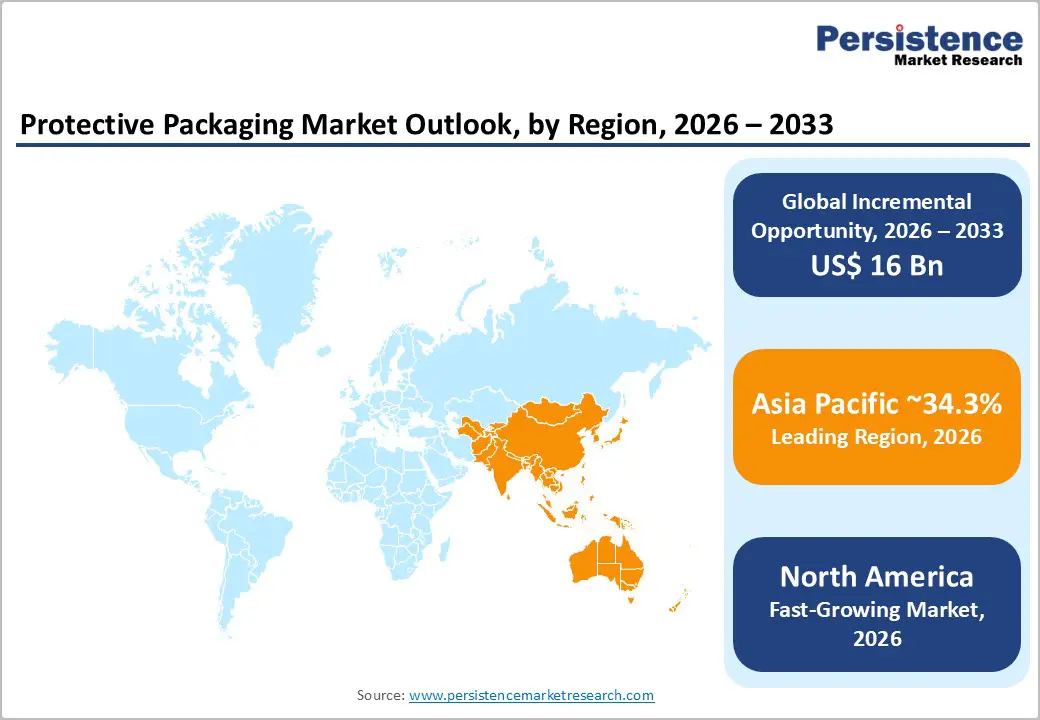

- Leading Region: Asia Pacific is the leading region, accounting for approximately 34.3% of the market share, driven by strong manufacturing activity and expanding e-commerce ecosystems.

- Fastest-growing Region: North America is the fastest-growing region, supported by high e-commerce penetration, advanced logistics infrastructure, and increasing adoption of automated packaging systems.

- Investment Plans: Market participants are actively investing in automation technologies, paper-based sustainable packaging, and integrated packaging systems, with a strong focus on reducing material usage and improving operational efficiency.

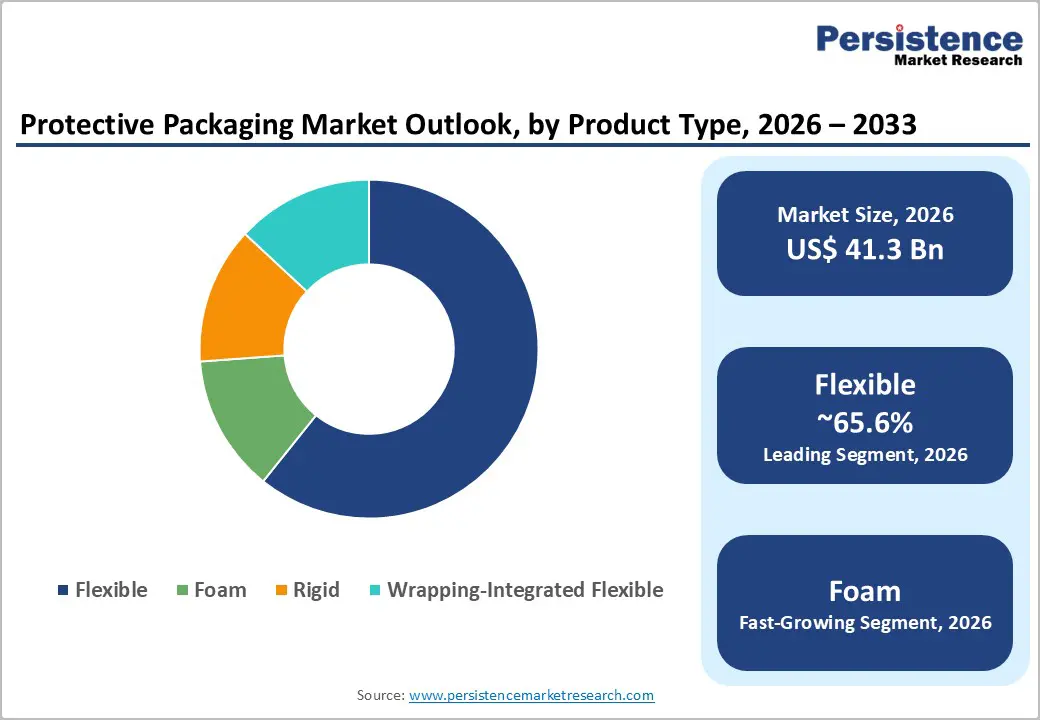

- Dominant Product Type: Flexible packaging dominates, holding an estimated 65.6% share, due to its lightweight nature, versatility, and suitability for high-volume e-commerce operations.

- Leading Material: Paper & paperboard leads, accounting for over 44.8% share, driven by increasing regulatory pressure and growing demand for recyclable and eco-friendly packaging solutions.

| Key Insights | Details |

|---|---|

| Protective Packaging Market Size (2026E) | US$41.3 Bn |

| Market Value Forecast (2033F) | US$57.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Factors - Driver, Restraint, and Opportunity Analysis

Driver Analysis - Rapid Expansion of E-Commerce and Omnichannel Logistics

The continued growth of e-commerce has significantly increased the demand for protective packaging solutions. With global digital commerce volumes expanding steadily, a higher proportion of goods is now shipped individually rather than in bulk. This shift exposes products to multiple handling points, increasing the likelihood of damage due to shock, vibration, and compression. Protective packaging plays a critical role in mitigating these risks through cushioning, wrapping, and void-fill solutions. The business impact is substantial: companies are prioritizing packaging that ensures product integrity while maintaining cost efficiency, particularly in last-mile delivery. As omnichannel retail becomes standard, demand for adaptable and lightweight protective formats continues to rise.

Increasing Regulatory Pressure for Sustainable Packaging

Governments and regulatory bodies are introducing stricter packaging regulations to reduce environmental impact. Policies focused on recyclability, material reduction, and waste management are compelling manufacturers to redesign packaging systems. Compliance requirements are particularly stringent in sectors such as food and healthcare, where packaging must meet both environmental and safety standards. These regulations are accelerating the shift toward paper-based materials, recycled content, and biodegradable solutions. From a market perspective, this is driving innovation in material science and increasing demand for certified, compliant packaging solutions. Companies that align with regulatory expectations are gaining a competitive advantage in both developed and emerging markets.

Growth of Global Manufacturing and Supply Chain Complexity

Global manufacturing networks are becoming increasingly distributed, with products often crossing multiple regions before reaching end consumers. This complexity increases the need for durable and reliable protective packaging to maintain product quality throughout transit. Industries such as electronics, automotive, and pharmaceuticals rely heavily on protective packaging to safeguard high-value and sensitive goods. As supply chains extend geographically, packaging is no longer viewed as a secondary function but as a critical component of quality assurance. This trend is supporting demand for high-performance materials, including foam and engineered flexible packaging, particularly in B2B logistics environments.

Restraint Analysis - High Compliance Costs and Regulatory Complexity

While sustainability regulations are driving innovation, they also introduce significant cost and operational challenges. Companies must adapt to evolving standards related to recyclability, labeling, and material usage, often across multiple jurisdictions. This increases design complexity, testing requirements, and certification expenses. The need to comply with different regional regulations can slow product development and increase time-to-market. Smaller manufacturers are particularly affected due to limited resources for regulatory compliance. These factors collectively create barriers to entry and may limit the pace of innovation for certain market participants.

Material Performance Limitations and Cost Trade-Offs

Despite the growing preference for sustainable materials, not all protective packaging applications can transition away from traditional materials such as plastics and foams. Products that are fragile, heavy, or sensitive to environmental conditions require high-performance packaging solutions that may not be easily replicated with eco-friendly alternatives. This creates a trade-off between sustainability and functionality. In many cases, the cost of product damage outweighs the benefits of using lower-cost or environmentally friendly materials. As a result, manufacturers must carefully balance performance, cost, and environmental impact, which can constrain widespread adoption of certain materials.

Opportunity Analysis - Expansion of Paper-Based and Recyclable Packaging Solutions

Paper and paperboard materials are gaining traction as sustainable alternatives to plastic-based packaging. With increasing regulatory and consumer pressure to reduce plastic waste, companies are investing in paper-based protective formats such as molded fiber, paper wraps, and corrugated cushioning. These materials offer recyclability and biodegradability while maintaining adequate protection for a wide range of products. The opportunity lies in further improving the strength, durability, and moisture resistance of paper-based solutions. Companies that can deliver high-performance, sustainable packaging at scale are well-positioned to capture market share.

Integration of Automation and Smart Packaging Systems

The adoption of automation in packaging operations is transforming the protective packaging market. Automated systems enable faster packaging processes, reduce labor costs, and improve consistency in packaging quality. Technologies such as right-sizing equipment, automated bagging systems, and AI-driven packaging optimization are gaining traction. These solutions not only enhance operational efficiency but also reduce material usage and shipping costs. The shift toward integrated packaging systems presents a significant growth opportunity for suppliers that offer both materials and equipment as part of a comprehensive solution.

Growth Potential in Emerging Markets and Regional Manufacturing Hubs

Emerging economies, particularly in Asia Pacific, are witnessing rapid industrialization and e-commerce expansion. Countries such as China, India, and those in Southeast Asia are becoming key manufacturing and consumption centers. This is driving demand for protective packaging across multiple sectors, including electronics, automotive, and food distribution. The increasing adoption of modern retail and logistics infrastructure further supports market growth. Companies that establish localized production and distribution networks can benefit from cost advantages and faster market penetration in these high-growth regions.

Category-wise Analysis

Product Type Insights

Flexible protective packaging is expected to remain the dominant segment, accounting for an anticipated share of approximately 65.6% in 2026. This segment includes bubble wrap, air pillows, padded mailers, stretch films, and paper-based flexible solutions. Its leadership is driven by versatility, lightweight characteristics, and efficient storage and transportation advantages. Flexible formats are extensively used across e-commerce, food & beverage, and consumer goods industries, where reducing dimensional weight is critical for cost optimization. For example, air pillow systems used by large online retailers help minimize void space while lowering shipping costs, while padded mailers are widely adopted for small electronics and apparel shipments. The segment also aligns well with automated fulfillment systems, enabling high-speed packaging operations in distribution centers.

Foam packaging is projected to be the fastest-growing product type, supported by rising demand for high-performance cushioning solutions. Materials such as polyurethane foam and expanded polystyrene (EPS) are widely used to protect fragile and high-value items, including smartphones, televisions, automotive parts, and industrial equipment. For instance, molded foam inserts are commonly used in consumer electronics packaging to secure products during long-distance transportation. As supply chains become more complex and globalized, the need for impact-resistant packaging is increasing. Foam packaging offers consistent shock absorption and vibration resistance, making it a preferred solution in industries where product damage can lead to significant financial losses and customer dissatisfaction.

Material Insights

Paper and paperboard materials are expected to lead the market, holding an anticipated share of over 44.8%. Their dominance is driven by strong sustainability credentials, including recyclability, biodegradability, and compliance with evolving environmental regulations. These materials are widely used in applications such as corrugated boxes, paper wraps, molded pulp inserts, and paper-based void fill. For example, molded fiber packaging is increasingly used as a replacement for plastic inserts in electronics and appliance packaging. Retailers and consumer brands are also adopting Kraft paper cushioning and recyclable mailers to meet sustainability targets. Continuous innovation in barrier coatings and structural strength is further enhancing the performance of paper-based materials, expanding their usability across demanding applications.

Plastic foams are anticipated to be the fastest-growing material segment due to their superior protective performance and lightweight properties. Materials such as EPS, expanded polyethylene (EPE), and polyurethane foam provide excellent cushioning, thermal insulation, and durability. These characteristics make them ideal for packaging sensitive products such as medical devices, temperature-controlled pharmaceuticals, and high-value electronics. For instance, EPS foam containers are widely used in cold chain logistics to maintain temperature stability during the transportation of vaccines and perishable goods. Despite increasing environmental concerns, the functional advantages of plastic foams continue to drive their adoption in applications where product safety and performance cannot be compromised.

Regional Insights

North America Protective Packaging Market Trends - Automation-Driven E-commerce Expansion and Sustainable Innovation

North America is the fastest-growing region in the protective packaging market, driven by a mature e-commerce ecosystem, advanced logistics infrastructure, and continuous investment in fulfillment technologies. The U.S. leads regional growth due to high online retail penetration and large-scale adoption of warehouse automation. Major retailers and logistics providers are increasingly implementing automated packaging systems, such as right-sizing equipment and high-speed bagging machines, to reduce material usage and improve throughput. For example, Amazon has expanded its use of automated packaging technologies and recyclable mailers across fulfillment centers, significantly reducing packaging waste and improving shipping efficiency. This shift is influencing suppliers to develop automation-compatible protective packaging solutions.

Regulatory frameworks in North America emphasize product safety and environmental compliance, particularly in food and healthcare applications. This is accelerating the adoption of recyclable, food-safe, and certified materials. Companies such as Sealed Air and Pregis are investing in paper-based cushioning systems and recyclable protective formats to align with sustainability targets. Innovation remains a key differentiator, with increasing focus on smart packaging, data-driven packaging optimization, and lightweight materials. Investment trends indicate strong growth in automation, integrated packaging systems, and sustainable product lines. However, cost pressures persist, as companies must balance environmental goals with operational efficiency and performance reliability.

Europe Protective Packaging Market Trends-Circular Economy Regulations Driving Material Innovation

Europe represents one of the most regulated markets for protective packaging, with strict policies focused on reducing packaging waste and promoting circular economy principles. Regulatory initiatives are accelerating the transition toward recyclable, reusable, and biodegradable packaging solutions. Countries such as Germany, the U.K., France, and Spain are key contributors to regional demand, supported by strong industrial bases and well-established retail sectors. The region’s regulatory environment is pushing companies to redesign packaging formats to meet recyclability and material reduction targets.

Industries such as automotive, electronics, and pharmaceuticals are major drivers of protective packaging demand in Europe. Companies are actively investing in sustainable materials and innovative packaging technologies to comply with evolving regulations. For instance, Smurfit Westrock has expanded its portfolio of paper-based protective solutions across Europe, supporting customers transitioning away from plastic packaging. Similarly, Storopack has introduced recycled-content air cushion systems to meet sustainability requirements. These developments are reinforcing the shift toward eco-friendly materials while maintaining performance standards. The emphasis on circular economy practices is encouraging innovation in recyclable and compostable packaging formats. Companies that can deliver compliant, high-performance solutions are gaining a competitive edge. As a result, Europe is becoming a key testing ground for next-generation sustainable packaging technologies, influencing global market trends.

Asia Pacific Protective Packaging Market Trends-Manufacturing Scale and E-commerce Fueling High-Volume Demand

Asia Pacific is the largest market for protective packaging, holding a 34.3% share, driven by strong manufacturing output, rapid urbanization, and expanding e-commerce ecosystems. The region benefits from large-scale production of electronics, automotive components, and consumer goods, which require efficient protective packaging for both domestic distribution and export. Countries such as China, India, Japan, and Southeast Asian nations are central to this growth. China leads the region in manufacturing and export activity, particularly in electronics and consumer goods, creating substantial demand for foam, flexible, and molded packaging solutions. India is emerging as a high-growth market due to increasing industrialization, government initiatives supporting manufacturing, and the rapid expansion of e-commerce platforms such as Flipkart and Amazon. These platforms are driving demand for cost-effective and sustainable protective packaging solutions tailored to high-volume shipping. Japan continues to play a critical role in high-precision packaging, particularly for advanced electronics and automotive components, where quality and reliability are paramount.

The region also benefits from cost-efficient manufacturing and strong export-oriented supply chains. Companies such as Huhtamaki have expanded operations in Asia to strengthen their presence in sustainable packaging solutions, while regional players are investing in paper-based and recyclable materials to align with global sustainability trends. Investment opportunities are focused on increasing production capacity, enhancing logistics infrastructure, and developing innovative materials. Companies that localize operations and adapt to diverse regulatory and consumer requirements are well-positioned to capitalize on the region’s dynamic growth trajectory.

Competitive Landscape

The global protective packaging market is fragmented, with a mix of global leaders and regional players. Leading companies operate across multiple product categories and end-use industries, leveraging strong distribution networks and advanced manufacturing capabilities. Competitive differentiation is based on innovation, sustainability, and the ability to provide integrated packaging solutions. Key players focus on sustainability, automation, and innovation. Strategies include expanding recyclable product lines, investing in packaging automation technologies, and offering integrated solutions that combine materials, equipment, and services. Companies are also pursuing geographic expansion to capture growth in emerging markets.

Key Industry Developments:

- In September 2025, Ranpak announced the debut of its end-to-end packaging solutions for smarter, greener logistics at IMHX 2025, integrating paper-based materials with automation technologies to improve operational efficiency and sustainability across fulfillment centers.

- In November 2025, Smurfit Westrock unveiled the world’s first dedicated clinical packaging facility, strengthening its capabilities in high-value and regulated healthcare packaging while expanding its innovation footprint in specialized protective solutions.

Companies Covered in Protective Packaging Market

- Sealed Air

- Smurfit Westrock

- International Paper

- Sonoco Products Company

- Ranpak

- Pregis

- Huhtamaki

- Storopack

- Intertape Polymer Group

- Amcor

- Dow

- DS Smith

- WestRock

- UFP Technologies

- Pregis Performance Flexibles

- EcoEnclose

Frequently Asked Questions

The global protective packaging market is estimated to be valued at US$41.3 billion in 2026.

The protective packaging market is projected to reach US$57.3 billion by 2033.

Key trends include the shift toward paper-based and recyclable materials, increasing adoption of automation and right-sizing technologies, and rising demand for lightweight yet high-performance packaging solutions driven by e-commerce growth.

The flexible packaging segment is the leading category, holding approximately 65.6% market share, due to its cost efficiency, adaptability, and widespread use in shipping and logistics.

The protective packaging market is expected to grow at a CAGR of 4.8% from 2026 to 2033.

Some of the major players include Sealed Air, Smurfit Westrock, International Paper, Sonoco Products Company, and Ranpak.