- Smart Packaging

- Europe Molded Pulp Packaging Market

Europe Molded Pulp Packaging Market Size, Share, and Growth Forecast, 2025 - 2032

Europe Molded Pulp Packaging Market By Source Material, Molded Type, Product Type, End-user, and Country Analysis for 2025 - 2032

Europe Molded Pulp Packaging Market Share and Trends Analysis

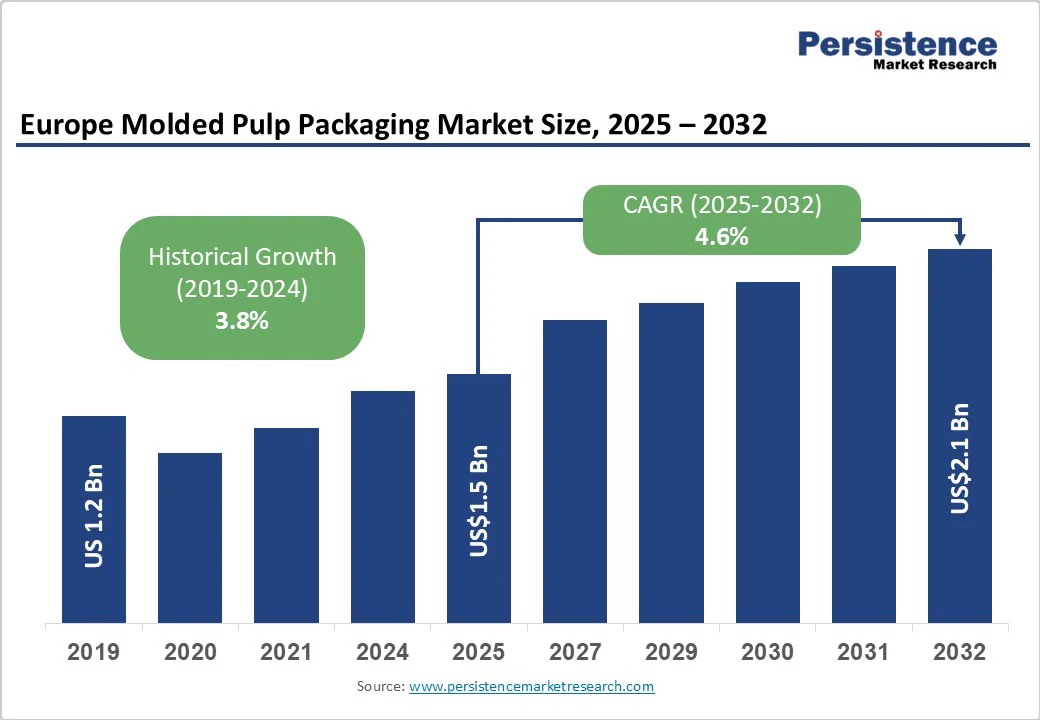

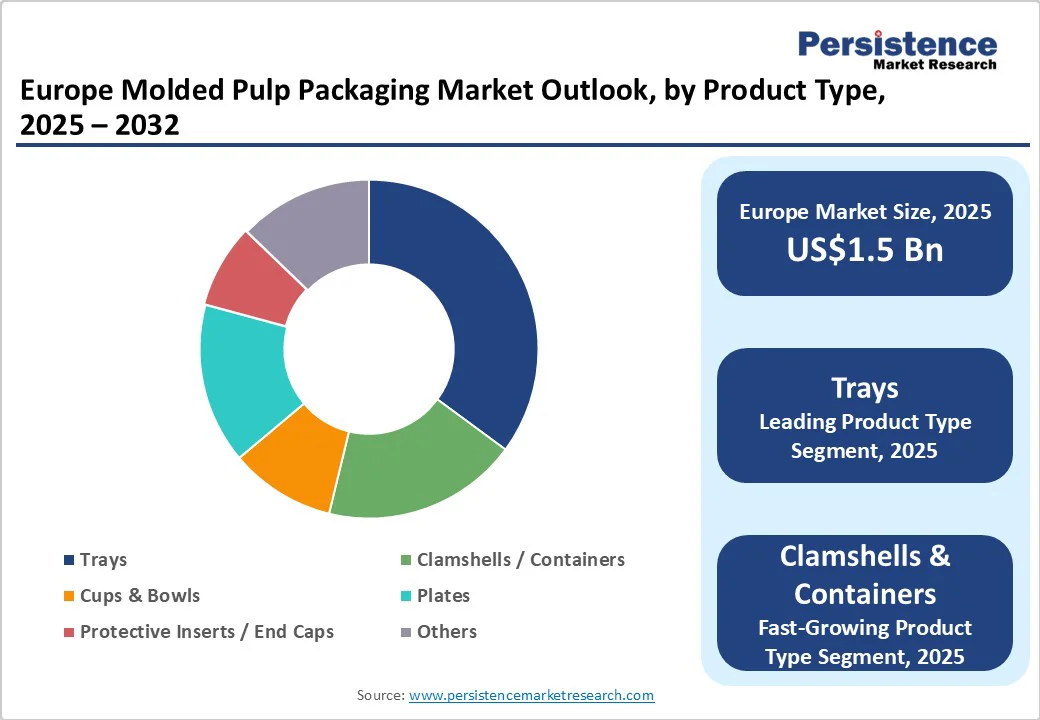

Europe molded pulp packaging market size is expected to be valued at US$1.5 Bn in 2025 and is projected to reach US$2.1 Bn, growing at a CAGR of 4.6% during the forecast period from 2025 to 2032, driven by environmental regulations, circular economy policies, and rising consumer preference for sustainable alternatives to plastics.

Key Industry Highlights:

- Dominant Product Type: By product type, trays are expected to hold a market share of around 35.1% in 2025, driven by their essential role in egg packaging and food handling.

- Leading End-user: The food and beverage segment is anticipated to hold around 43.4% of the market share in 2025, driven by its indispensable role in safeguarding eggs, fresh produce, beverages, and ready-to-serve meals across Europe.

- Driver: A major catalyst for growth in the packaging sector is the significant shift toward sustainable packaging solutions in Europe.

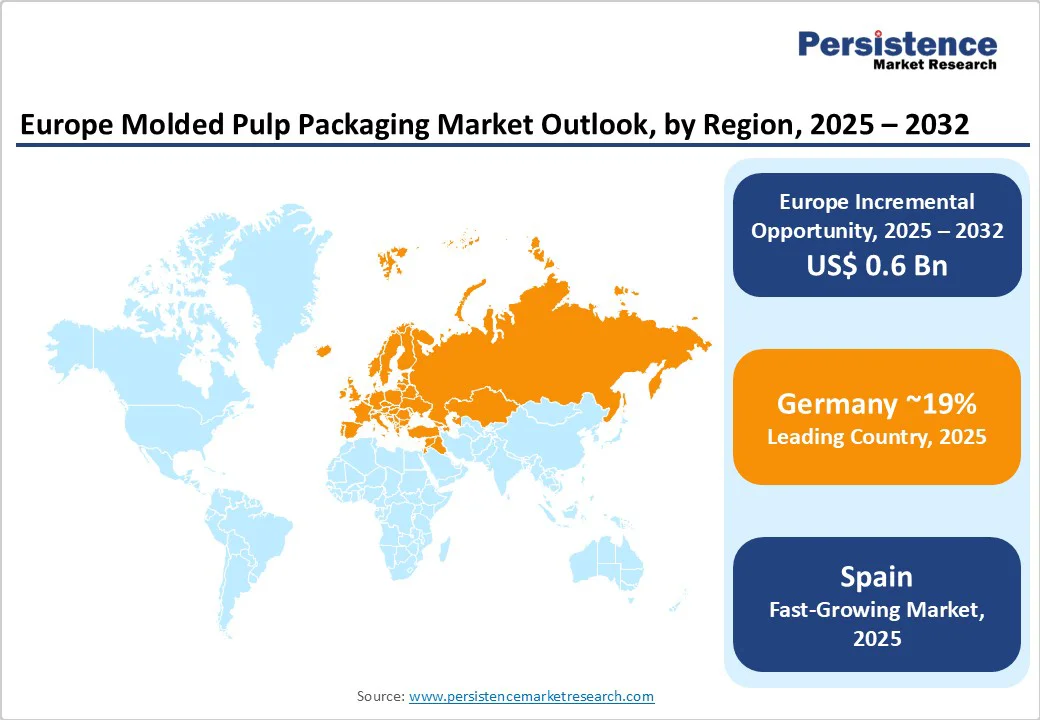

- Leading Country: Germany is anticipated to lead with approximately 19.4% market share, due to large-scale production and innovative SMF solutions.

- Opportunity: The rapid expansion of e-commerce across Europe creates a significant opportunity for the molded pulp packaging market.

| Key Insights | Details |

|---|---|

| Estimated Market Size (2025E) | US$1.5 Bn |

| Projected Market Value (2032F) | US$2.1 Bn |

| Value CAGR (2025 to 2032) | 4.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Strong Push Toward Sustainable Packaging Solutions in Europe

The strong shift toward sustainable packaging solutions in Europe stands as one of the most powerful growth drivers for the packaging sector. Governments, industries, and consumers continue to demand packaging that supports a circular economy while reducing dependence on plastics. Paper and fiber-based formats play a central role in this transition, backed by impressive recycling performance.

Eurostat reported that in 2022, Europe achieved an 83% recycling rate for paper and cardboard, far surpassing plastics at 41%. CEPI further highlighted that 95% of containerboard fibers in Europe came from recycled paper, showcasing a highly efficient value chain built around fiber circularity. This established recycling ecosystem creates strong momentum for molded pulp packaging, particularly in food, consumer goods, and protective applications.

Industry-led initiatives such as the 4evergreen Alliance aim to push fiber-based packaging recycling rates to 90% by 2030, accelerating adoption across the continent. At the same time, the rise of non-wood fibers such as hemp, flax, straw, and textile waste expands raw material availability and enhances innovation opportunities. These developments reinforce Europe’s position as a leader in sustainable packaging solutions, ensuring molded pulp packaging remains central to the region’s long-term environmental and circular economy goals.

High Production and Raw Material Costs Hinder Market Growth

High production and raw material costs create a serious barrier for the Europe molded pulp packaging market. The sector relies heavily on fiber availability, labor input, and energy consumption, all of which vary widely across EU member states. These cost factors directly impact competitiveness in comparison to cheaper plastic packaging alternatives.

In 2024, Europe’s consumer goods industry reflected striking disparities in price levels, with Denmark recording costs 43% above the EU average while Bulgaria was 40% below. At the same time, Germany reported the highest energy price levels among 36 European countries, putting further pressure on energy-intensive operations such as molding and drying.

These variations in input costs across Europe significantly influence the affordability and scalability of sustainable packaging solutions. Higher production costs reduce margins for manufacturers, complicate pricing strategies, and limit broader adoption, particularly in high-cost economies. The combination of elevated energy prices, wage disparities, and raw material challenges makes it difficult for producers to sustain growth without passing costs to consumers.

Unless cost-efficiency innovations emerge, high production and raw material expenses will remain a structural restraint, slowing the long-term transition to fiber-based alternatives across Europe’s packaging landscape.

Expansion of E-commerce and Protective Packaging Applications

The rapid expansion of e-commerce across Europe creates a significant opportunity for the molded pulp packaging market. According to the International Trade Association, Europe ranked as the third-largest retail e-commerce market globally, generating US$631.9 Bn in revenue in 2023, with projections to reach US$902.3 Bn by 2027, at an annual growth rate of 9.31%.

With e-commerce contributing 9.3% to the U.K.’s GDP and high penetration rates in Germany, France, and the Nordic countries, the demand for sustainable and protective packaging formats continues to accelerate. Molded pulp packaging offers the cushioning, recyclability, and eco-friendly credentials that digital retail channels require for safe deliveries and consumer trust.

Protective molded pulp packaging also aligns with cross-border e-commerce, where Luxembourg (80% cross-border share) and Ireland (68.6%) lead in digital trade. This growth amplifies the need for packaging solutions that withstand transport, support brand identity, and comply with Europe’s circular economy framework.

Recent innovations in molded pulp packaging for cosmetics and beauty brands, such as modular dual-shell designs and bagasse-based materials, demonstrate how protective and premium features converge in the market. As e-commerce reshapes retail and consumer engagement, molded pulp packaging secures its role as a versatile solution, positioning the Europe molded pulp packaging market for long-term growth in both protective packaging and sustainable e-commerce applications.

Circular Economy and Closed-Loop Recycling Initiatives

Circular economy and closed-loop recycling are shaping a major trend in the Europe molded pulp packaging market. The new EU Packaging and Packaging Waste Regulation (PPWR 2025/40) enforces harmonized rules on recyclability, recycled content, and design-for-recycling, replacing the earlier directive to create a unified sustainability framework across member states.

By aiming to make all packaging recyclable in an economically viable way by 2030 and reducing dependence on virgin raw materials, this regulation positions molded pulp packaging as a preferred fiber-based alternative for foodservice, e-commerce, and industrial applications.

The pulp and paper sector supports this momentum, as paper and board consumption increased by 7.5% in 2024 while paper for recycling utilisation rose by 4.1%, driven largely by packaging grades now accounting for 63% of production (CEPI). Exports of paper and board also grew by 16.8% in North America, highlighting Europe’s global trade strength in fiber solutions.

Together with PPWR’s restrictions on single-use plastics and mandatory recycled content targets, these factors reinforce molded pulp packaging as central to Europe’s shift toward a circular, climate-neutral economy by 2050, making recycling and resource efficiency a defining trend across the packaging industry.

Category-wise Analysis

Product Type Insights

By Product type, Trays are expected to hold a market share of around 35.1% in 2025, driven by their essential role in egg packaging and food handling. The EU, with over 350 million laying hens producing nearly 6.7 million tonnes of eggs annually, relies heavily on molded pulp trays to ensure safe storage, transport, and retail display.

Governed by strict EU marketing standards under the Common Market Organisation (Regulation (EU) No 1308/2013 and related provisions), trays comply with requirements for grading, marking, and food safety while offering strong protection and ventilation.

Beyond agriculture, molded pulp trays are gaining adoption in fresh produce, beverages, and foodservice sectors due to their recyclability and ability to replace single-use plastics. With this combination of regulatory compliance, environmental benefits, and broad application, trays remain the cornerstone product in the European molded pulp packaging market.

End-user Insights

The food and beverage segment is anticipated to hold around 43.4% share in 2025, driven by its indispensable role in safeguarding eggs, fresh produce, beverages, and ready-to-serve meals across Europe.

The EU food and beverage services sector employs over 10.9 million people and generates more than €280 Bn (US$300 Bn) in value, underscoring the massive consumption base that demands safe, hygienic, and eco-friendly packaging solutions. Molded pulp packaging for foodservice applications aligns with strict EU marketing standards, particularly in eggs and perishable goods, while meeting sustainability goals through compostable and recyclable fiber-based materials.

With nearly 2 million enterprises operating in Europe’s food and hospitality sector, molded pulp solutions provide scalable and cost-effective options for both large FMCG brands and small-scale businesses. This dominant application strengthens the position of food and beverage packaging as the backbone of the Europe molded pulp packaging market, ensuring sustained growth during the forecast period.

Country-level Insights

Germany Molded Pulp Packaging Market Trends

Germany is projected to hold around 19.4% share in 2025, driven by its position as Europe’s hub for sustainable packaging innovation and large-scale production of molded pulp packaging. The country is home to major players such as Huhtamaki and PAPACKS®, who are pioneering advanced smooth molded fiber (SMF) and hemp-based fiber packaging solutions as alternatives to single-use plastics.

Huhtamaki’s Alf facility alone has shifted to producing up to 3.5 billion SMF products annually, replacing over 2,000 tonnes of plastic and supporting foodservice, FMCG, and retail applications with certified home and industrial compostable products.

Germany’s strong industrial base, sustainability-driven policies, and alignment with EU circular economy goals make it a cornerstone for molded pulp packaging adoption in Europe. With innovation, scale, and regulatory support, Germany continues to reinforce its leadership role in shaping the future of molded fiber packaging across the region.

Competitive Landscape

The Europe molded pulp packaging market shows strong momentum as manufacturers sharpen their focus on high-capacity expansion, premium design innovation, and circular sustainability. Leading players such as Huhtamaki, PAPACKS SALES GmbH, Otarapack, Omni-Pac Group, and James Cropper PLC are investing in advanced molded fiber technologies, luxury-grade solutions, and digital tooling to serve foodservice, healthcare, cosmetics, and premium beverages.

Companies integrate renewable fibers, compostable coatings, and precision molding to meet PPWR compliance while capturing consumer preference for eco-conscious packaging. Competitive intensity remains high, with consolidation trends shaping the landscape, driving the market toward an oligopolistic structure during the forecast period.

Key Industry Developments

- In March 2025, Huhtamaki expanded its Alf, Germany site into one of Europe’s largest molded pulp facilities, with the capacity to produce up to 3.5 billion smooth molded fiber (SMF) products annually. Targeting foodservice and FMCG sectors, the compostable SMF products can replace over 2,000 tonnes of plastic each year, using fiber from sustainably managed European forests, strengthening Huhtamaki’s leadership in sustainable packaging.

- In June 2024, Bayer partnered with PAPACKS SALES GmbH to launch fiber-based molded pulp packaging for key consumer health brands such as Aspirin, Bepanthen, and Claritin. Made from renewable fibers with plant-based biodegradable coatings, the packaging supports Bayer’s goal of 100% recyclable or reusable self-care packaging by 2030, marking a major step for molded pulp adoption in the healthcare sector.

Companies Covered in Europe Molded Pulp Packaging Market

- Flatz GmbH

- Pulp-Tec Limited

- TART Packaging Solutions GmbH

- PAPACKS SALES GmbH

- Otarapack Packaging Solutions

- Huhtamaki Oyj

- Omni-Pac Group

- MM Group

- PackTech Global Solutions

- EcoMold Pulp Packaging

- James Cropper PLC

- buhl-paperform GmbH

Frequently Asked Questions

The Europe molded pulp packaging market is projected to be valued at US$1.5 Bn in 2025.

The market is poised to witness a CAGR of 4.6% from 2025 to 2032.

The Europe molded pulp packaging market is driven by the strong push for sustainable, recyclable, and biodegradable packaging that aligns with regulatory goals and consumer demand for a circular economy.

The rapid growth of e-commerce and rising demand for protective, sustainable packaging create significant opportunities for molded pulp packaging in Europe’s retail and cross-border trade sectors.

The key market players in the Europe molded pulp packaging market include Flatz GmbH, TART Packaging Solutions GmbH, PAPACKS SALES GmbH, Otarapack Packaging Solutions, Huhtamaki Oyj, and James Cropper PLC.