- Non-food Packaging

- Oxo-Biodegradable Plastic Packaging Market

Oxo-Biodegradable Plastic Packaging Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Oxo-Biodegradable Plastic Packaging Market by Material Type (Polyethylene (PE), Polypropylene (PP), Polystyrene (PS), Polyvinyl Chloride (PVC), Polyethylene Terephthalate (PET)), Packaging Type (Bags & Sacks, Films & Wraps, Pouches, Containers), End-user, Regional Analysis, 2025 - 2032

Oxo-Biodegradable Plastic Packaging Size and Trend Analysis

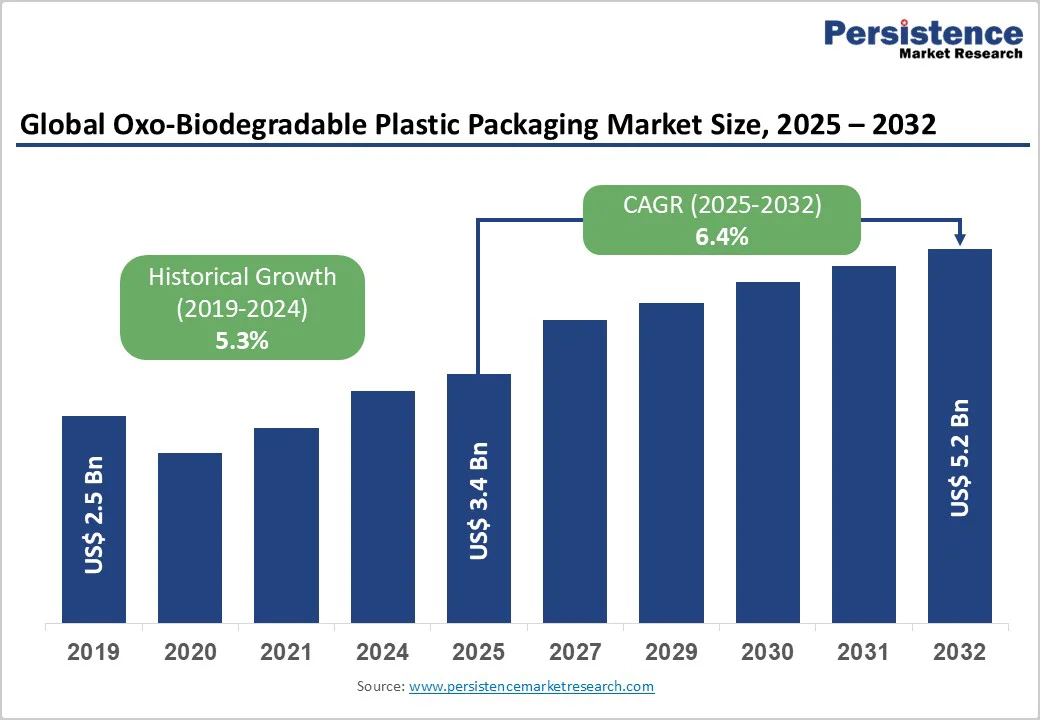

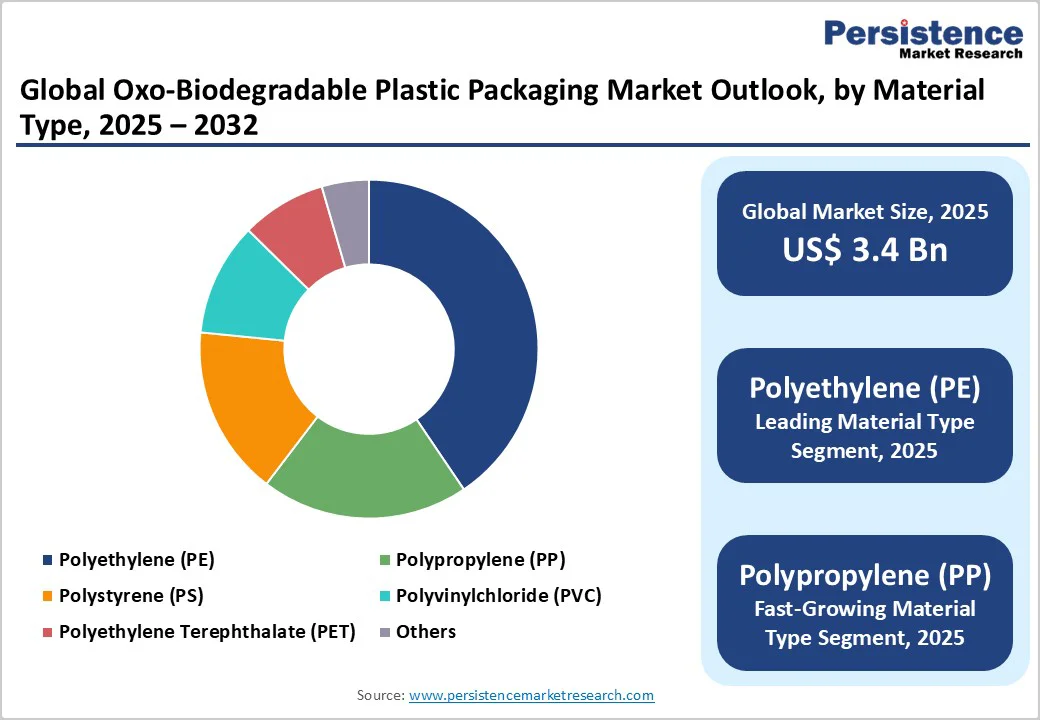

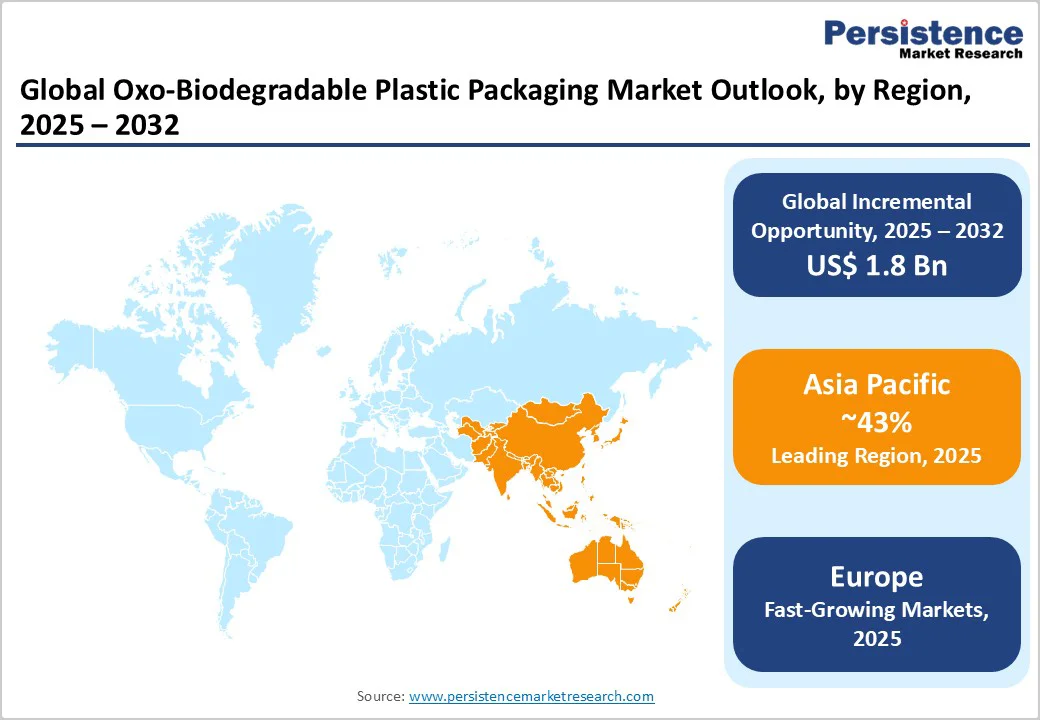

The global oxo-biodegradable plastic packaging market size is valued at US$ 3.4 billion in 2025 and is projected to reach US$ 5.2 billion, growing at a CAGR of 6.4% between 2025 and 2032. The market's robust expansion is driven by the rise in environmental regulations and consumer demand for sustainable packaging solutions across developed and emerging economies.

Key Industry Highlights:

- Leading Region – Asia Pacific holds 43% of the global market, driven by China and India’s regulatory mandates, cost-efficient production, and rapid adoption across retail and FMCG sectors.

- Fastest Growing Region – Europe is expected to achieve a 7.1% CAGR, fueled by EU sustainability laws, circular economy targets, and strong demand for recyclable and biodegradable materials.

- Dominant Segment – Bags & Sacks lead with 42% share, supported by global single-use plastic bans and scalable oxo-biodegradable film manufacturing systems.

- Fastest Growing Segment – Films & wraps expand rapidly due to growing applications in food, industrial, and lamination packaging, emphasizing material efficiency and environmental compliance.

- Key Market Opportunity – Pharmaceutical & healthcare packaging offers the highest growth potential, driven by FDA-approved oxo-biodegradable formulations ensuring safety, sterility, and sustainability.

| Key Insights | Details |

|---|---|

|

Market Size (2025E) |

US$ 3.4 Bn |

|

Market Value Forecast (2032F) |

US$ 5.2 Bn |

|

Projected Growth CAGR (2025-2032) |

6.4% |

|

Historical Market Growth (2019-2024) |

5.3% |

Market Dynamics

Drivers - Rising Environmental Regulations and Policy Support Driving Market Expansion

Global environmental policies are increasingly shaping the oxo-biodegradable plastic packaging market by setting strict compliance standards for manufacturers. The European Union’s Single-Use Plastics Directive (2019/904), which became fully enforceable in 2024, and the Packaging and Packaging Waste Regulation (PPWR) of December 2024 are transforming industry practices. These regulations aim to eliminate harmful single-use plastics, enforce circularity, and achieve a 15% per capita reduction in packaging waste by 2040.

Asia Pacific and Middle Eastern countries such as Saudi Arabia, the UAE, and Pakistan have made oxo-biodegradable plastics mandatory for short-life plastic products, establishing a unified regulatory framework. This clarity encourages investment in new production facilities, ensures compliance alignment, and strengthens the overall growth momentum of oxo-biodegradable packaging on a global scale.

Growing Consumer Demand for Sustainable and Eco-Friendly Packaging

Evolving consumer preferences toward environmentally responsible products are a major catalyst for oxo-biodegradable plastic packaging demand. Surveys reveal that nearly 70% of consumers now favor bioplastics or biodegradable alternatives, often accepting higher costs for sustainable value propositions. This shift is especially prominent in Europe and North America, where green-conscious buyers influence corporate packaging decisions and brand loyalty.

Major companies in the food, beverage, and personal care sectors are increasingly integrating oxo-biodegradable materials into packaging to align with sustainability goals and enhance brand reputation. The implementation of Extended Producer Responsibility (EPR) schemes and corporate carbon-reduction commitments provides economic incentives for adoption. Together, these factors reinforce a strong, consumer-driven momentum that sustains market expansion beyond mere regulatory compliance.

Restraints - Ongoing Controversy Regarding Environmental Performance and Microplastics Formation

Despite growing commercialization, oxo-biodegradable plastics face persistent scrutiny regarding their true environmental benefits and microplastic generation potential. Research groups and environmental organizations, including the Ellen MacArthur Foundation, argue that these materials may fragment into microplastics rather than fully biodegrade under natural conditions. The United Nations Environment Programme (UNEP) maintains that “the fate of microplastic fragments remains unclear,” prompting cautious policy stances across developed regions. Consequently, several jurisdictions have restricted or banned oxo-biodegradable plastics altogether, dampening market confidence and curbing adoption in environmentally sensitive consumer and industrial segments.

Recycling Stream Contamination and Circular Economy Incompatibility

Oxo-biodegradable plastic packaging faces significant compatibility issues with established recycling systems, posing challenges in markets with advanced waste-management infrastructure. These plastics are difficult to distinguish from conventional polymers during sorting, often contaminating recycling and composting streams. Their partial degradation can impair the quality and resale value of recycled plastics, discouraging recyclers from processing mixed material batches.

Industry associations and regulatory bodies acknowledge these challenges. The Biodegradable Plastics Association and leading additive manufacturers have highlighted that oxo-biodegradable materials are incompatible with closed-loop recycling systems. Furthermore, the European Union’s Circular Economy Action Plan excludes oxo-biodegradable plastics from certified composting and recycling categories, effectively narrowing their commercial scope in regions pursuing zero-waste and circular economy objectives.

Opportunities - Accelerated Adoption in Emerging Markets with Developing Waste Management Infrastructure

Emerging economies across Asia Pacific, Latin America, and the Middle East & Africa offer significant opportunities for oxo-biodegradable plastic packaging due to underdeveloped waste collection systems and high plastic pollution levels. Countries such as Brazil, Mexico, and several African nations face growing environmental challenges from unmanaged plastic waste, making low-cost and self-degrading packaging solutions highly attractive. Symphony Environmental Technologies has leveraged this opportunity by establishing operations in over 100 countries through an extensive network of 70+ regional partners.

A notable policy shift occurred in 2024 when Brazil’s Supreme Federal Court recognized the environmental benefits of oxo-biodegradable plastics, opening one of the world’s largest plastic-consuming markets, over 7.5 million tonnes annually, to wider adoption. With only 1.28% of plastic waste currently recycled in Brazil, oxo-biodegradable solutions present a practical and scalable alternative, enabling market expansion in regions lacking sophisticated recycling infrastructure.

Technological Advancements in Pro-Oxidant Additives and Performance Enhancement

Continuous advancements in additive technology and polymer science are unlocking new growth avenues for oxo-biodegradable plastic packaging. Research from the Lambton Manufacturing Innovation Centre (Canada) in 2024 validated that optimized pro-oxidant masterbatch formulations can achieve controlled biodegradation without microplastic residue, reinforcing scientific confidence in the technology. This progress strengthens the industry’s credibility and regulatory acceptance in developed markets.

New additive systems, including bio-based pro-oxidants derived from epoxidized vegetable oils and cellulose nanocrystals, are enhancing flexibility, strength, and biodegradability in plastic formulations. The introduction of ASTM D6954-24 provides a standardized framework for testing degradation performance under diverse conditions. Leading players like Add-X Biotech and BiologiQ are pioneering plant-based additive blends for high-performance packaging and healthcare applications, driving adoption in premium segments and creating lucrative opportunities through value-added product diversification.

Category-wise Analysis

Material Type Insights

Polyethylene (PE) dominates the oxo-biodegradable plastic packaging market, accounting for around 38% market share. Its high flexibility, chemical resistance, and compatibility with existing plastic manufacturing lines make it ideal for bags, sacks, and films. Minimal process modifications and low additive requirements (about 2% by weight) allow easy conversion to oxo-biodegradable formats without significant cost increases, reinforcing PE’s market leadership across global applications.

Polypropylene (PP) represents the fastest-growing material segment, gaining traction in pharmaceutical, healthcare, and industrial packaging, where barrier strength and sterilization compatibility are crucial. Technological advancements in bio-based PP and improved pro-oxidant formulations are expanding its appeal, positioning PP as a preferred sustainable alternative in applications demanding higher durability and performance efficiency.

Packaging Type Insights

Bags & Sacks command the largest share of approximately 42% in the oxo-biodegradable plastic packaging market. Their wide use across retail, grocery, e-commerce, and waste management stems from strong regulatory mandates banning conventional plastics. These products offer immediate scalability and cost-effectiveness since oxo-biodegradable materials can be integrated into existing film production systems without major investment, supporting rapid compliance and adoption globally.

Films & Wraps emerge as the fastest-growing packaging category, driven by expanding use in food packaging, lamination, and industrial wrapping applications. Their light weight, flexibility, and strong performance attributes enhance suitability across high-demand sectors, particularly as consumer brands and manufacturers prioritize environmentally responsible packaging alternatives with versatile performance characteristics.

End-user Analysis

The Food & Beverages industry leads the oxo-biodegradable packaging market with around 36% market share, driven by strong regulatory restrictions on single-use plastics and consumer preference for sustainable packaging. Major global food and beverage companies have adopted biodegradable alternatives to align with sustainability goals and reduce carbon footprints, reinforcing this segment’s consistent dominance worldwide.

The pharmaceutical & healthcare segment represents the fastest-growing End-user category, supported by stricter regulatory standards from the FDA and EMA. Rising adoption of ASTM D6954-compliant materials ensures environmental compliance while maintaining biocompatibility and contamination control. This trend, combined with expanding applications in medical packaging and sterile product protection, is expected to accelerate growth in the coming years.

Regional Insights

North America Oxo-Biodegradable Plastics Trends

North America leads the global oxo-biodegradable plastic packaging market, accounting for around 36.8% of total revenue in 2024. The United States drives regional dominance through advanced regulatory frameworks, including the EPA’s single-use plastic policies and USDA BioPreferred certifications promoting bio-based materials. California’s SB 54 and state-wide EPR initiatives accelerate adoption across consumer goods and retail packaging, pushing demand for biodegradable alternatives. Major North American converters are integrating oxo-biodegradable technology into flexible and rigid formats to align with sustainability mandates and brand compliance requirements.

Rapid uptake is also seen across healthcare and pharmaceutical applications, supported by FDA traceability regulations under the Drug Supply Chain Security Act. The region’s innovation ecosystem, combined with policy-driven incentives and industrial collaboration, consolidates its leadership in sustainable packaging transformation.

Europe Oxo-Biodegradable Plastics Trends

Europe represents a highly structured and regulatory-driven market, expanding at a CAGR of 7.1% during 2024–2032. The implementation of the EU’s Packaging and Packaging Waste Regulation (PPWR) and national mandates such as Germany’s VerpackG and France’s AGEC Law are driving material innovation toward recyclable and biodegradable solutions. Germany remains a major contributor due to stringent circular economy targets and established producer responsibility systems.

Manufacturers across Italy, France, and Spain are focusing on agro-waste valorization projects, transforming agricultural residues into high-performance biodegradable films and pouches. Horizon Europe–funded programs further support SMEs developing sustainable alternatives, while end-use sectors particularly food and beverage packaging continue adopting compostable and degradable materials to meet 2030 recyclability targets.

Asia Pacific Oxo-Biodegradable Plastics Trends

Asia Pacific is the fastest-growing region, accounting for nearly 43% of the global oxo-biodegradable packaging market in 2024. China dominates regional supply, representing about 46% of global biodegradable plastics production, backed by government-led initiatives supporting biopolymer capacity expansion. India’s plastic ban policies and increasing environmental awareness are accelerating oxo-biodegradable adoption across retail, FMCG, and e-commerce sectors.

Southeast Asian economies particularly Thailand, Malaysia, and Indonesia are emerging as low-cost manufacturing hubs for oxo-biodegradable additives and flexible packaging films. Strong investment inflows, favorable labor economics, and strategic raw material availability enhance regional competitiveness. Japan continues driving technology advancements in pro-oxidant formulations, reinforcing Asia Pacific’s role as the growth engine of global sustainable packaging production.

Competitive Landscape

The oxo-biodegradable plastic packaging market demonstrates a moderately consolidated competitive environment, characterized by advanced technology platforms, proprietary additive formulations, and extensive regulatory compliance frameworks. Companies compete through innovation in pro-oxidant chemistry, masterbatch development, and bio-based additive integration aimed at improving performance, degradability, and cost efficiency while maintaining compatibility with existing manufacturing infrastructure.

Strategic emphasis is placed on R&D investment, certification acquisition, and regional expansion to strengthen market presence. Achieving compliance with global standards such as ASTM D6954-24, ASTM D6400, and EN 13432 remains a key differentiator, while obtaining health and food-contact approvals enhances credibility and supports adoption across high-value sectors including food, healthcare, and industrial packaging.

Key Market Developments

- In October 2024, Symphony Environmental Technologies released peer-reviewed scientific research confirming that optimized oxo-biodegradable masterbatch formulations do not generate persistent microplastics during controlled environmental degradation, validating technical performance claims and providing an independent scientific foundation supporting regulatory approval and market expansion across emerging economy jurisdictions.

- In February 2024, ENSO Plastics LLC introduced advanced compostable bag formulations with enhanced cost efficiency and degradation performance characteristics, expanding the product portfolio to address competitive pressure from premium-positioned alternatives and capturing price-sensitive market segments in Latin American and Asian growth regions.

- In March 2024, Wells Plastics Ltd. expanded its biodegradable additive technology portfolio to include enhanced formulations for expanded application coverage across pharmaceutical, healthcare, and food service packaging formats, demonstrating commitment to technology advancement and market expansion beyond traditional bags and sacks segments.

Companies Covered in Oxo-Biodegradable Plastic Packaging Market

- Symphony Environmental Technologies PLC

- Wells Plastics Ltd.

- Add-X Biotech AB

- Willow Ridge Plastics Inc.

- Licella Holdings Ltd.

- BiologiQ Inc.

- ENSO Plastics LLC

- Symphony Polymers Pvt. Ltd.

- Oxo-Biodegradable Plastics Inc.

- Elif Plastik Ambalaj Sanayi Ve Ticaret A.S.

- EPI Environmental Technologies Inc.

- UNIBAG Maghreb

- Add Plast

- Newtrans USA Company

- Licton Industrial Corp.

Frequently Asked Questions

The global oxo-biodegradable plastic packaging market is valued at US$ 3.4 Bn in 2025 and projected to reach US$ 5.2 Bn by 2032, expanding at a 6.4% CAGR driven by rising sustainability mandates and eco-conscious consumer demand.

Market growth is driven by strict global regulations, mandatory oxo-biodegradable policies in key countries, consumer preference for sustainable packaging, and corporate sustainability commitments across major end-use industries.

Bags & Sacks dominate the market with 42% share, supported by global bans on single-use plastics, cost-effective scalability, and widespread retail and waste management applications.

Asia Pacific leads with 43% share, while Latin America records the fastest growth, propelled by Brazil’s regulatory approvals and regional sustainability initiatives.

The Pharmaceutical & Healthcare sector offers the top growth opportunity through 2032, driven by FDA and EMA compliance needs and biopharma sustainability commitments.

The market is led by Symphony Environmental Technologies, with strong competition from Wells Plastics, Add-X Biotech, BiologiQ, and ENSO Plastics, focusing on additive innovation and regional expansion.