- Smart Packaging

- Bag-in-Box Packaging Market

Bag-in-Box Packaging Market Size, Share, and Growth Forecast, 2025 - 2032

Bag-in-Box Packaging Market by Capacity (Small (up to 5 L), Medium (5–20 L), Large (20–100 L), and Industrial/Bulk (>100 L)), Tap (With Tap/Dispenser (spout, lever, ball valve, etc.) and Without Tap/Bulk Bag.), Industry (Food & Beverages, Pharmaceuticals & Healthcare, Chemical & Industrial, and Others), and Regional Analysis for 2025 - 2032

Bag-in-Box Packaging Market Size and Trends Analysis

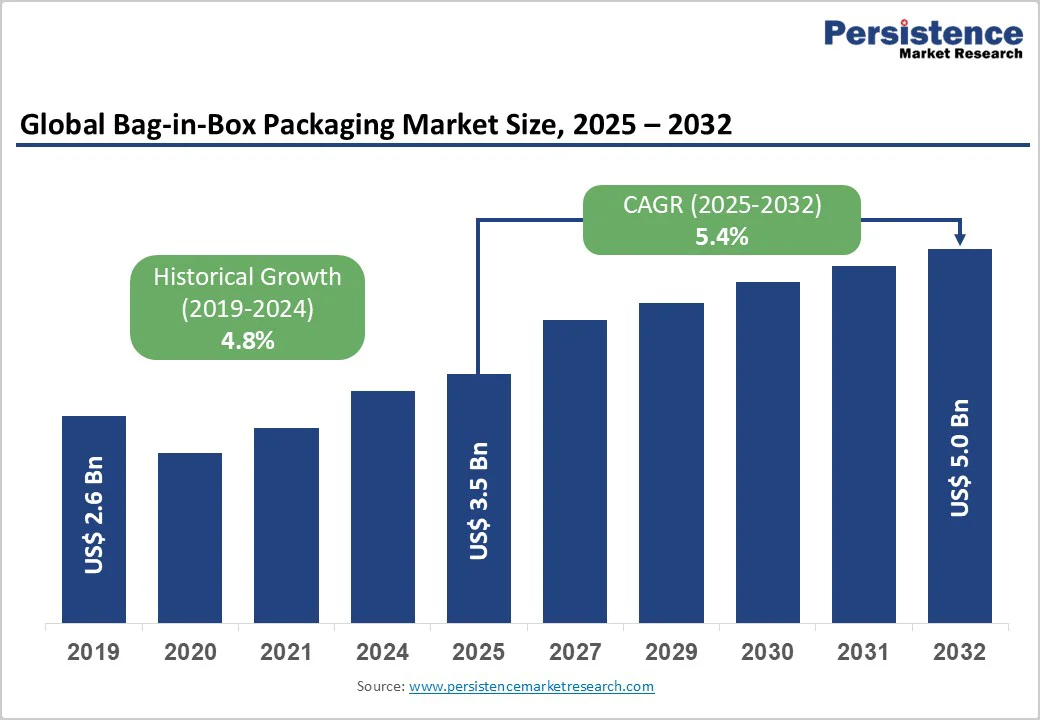

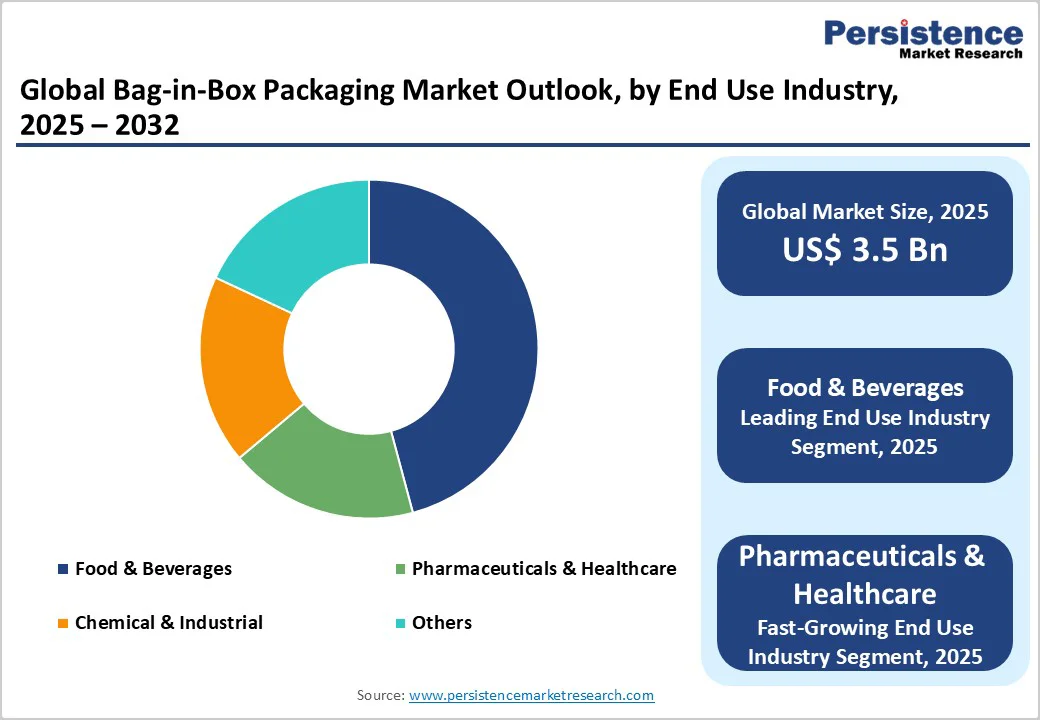

The global bag-in-box packaging market size is valued at US$ 3.5 billion in 2025 and is projected to reach US$ 5.0 billion by 2032, growing at a CAGR of 5.4% during the forecast period. Market expansion reflects sustained demand from food and beverage applications, emerging pharmaceutical liquid packaging adoption, and strategic sustainability positioning aligned with regulatory requirements.

Key Industry Highlights:

- Small-capacity bag-in-box containers (up to 5 litres) dominate the market, accounting for 62.5% of volume and revenue due to widespread retail wine and household beverage adoption.

- Food and beverage end-use segment leads demand with approximately 63.5% share, driven by wine, juice, dairy, and sauce packaging applications.

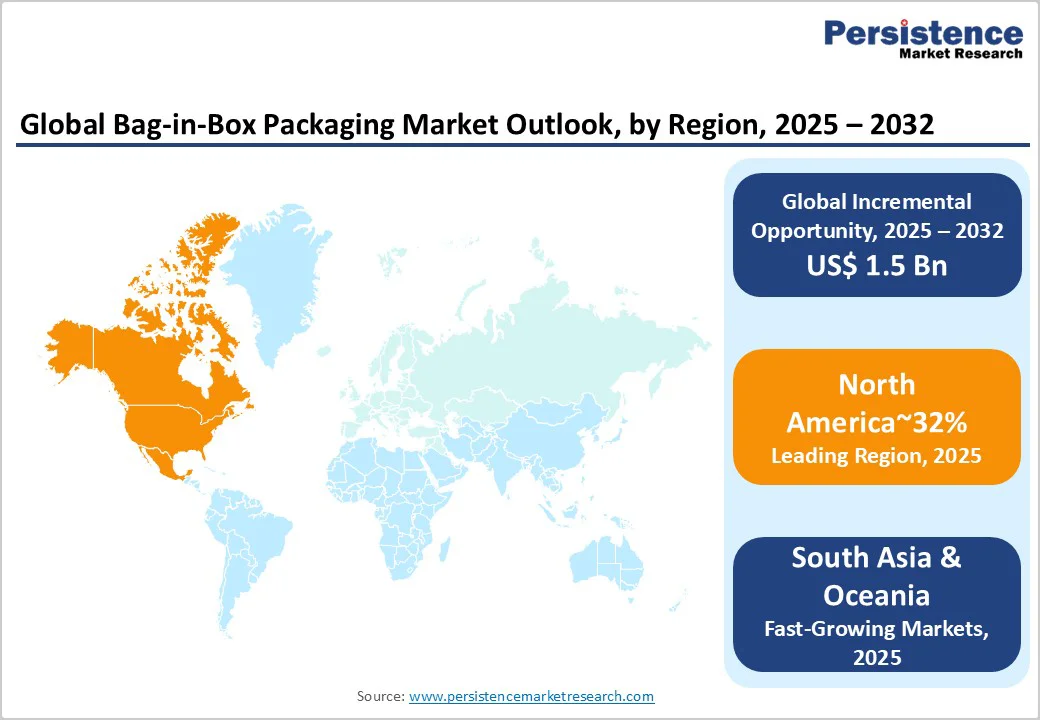

- North America holds the largest regional market share around 32%, supported by established wine consumption, beverage industry infrastructure, and e-commerce adoption.

- Europe commands the second-largest market share of around 27%, bolstered by mature wine regions, foodservice sophistication, and regulatory sustainability mandates.

- East Asia is a rapidly expanding market with a 22% share in 2025, driven by rising middle-class consumption, beverage industry growth, and pharmaceutical packaging adoption.

- Tap-equipped bag-in-box systems dominate with 66% market share, reflecting consumer preference for convenience, controlled dispensing, and product protection.

| Key Insights | Details |

|---|---|

| Bag-in-Box Packaging Market Size (2025E) | US$ 3.5 Bn |

| Market Value Forecast (2032F) | US$ 5.0 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.8% |

Market Dynamics

Drivers-Sustainability Alignment and Regulatory Packaging Requirements Implementation

Environmental regulatory frameworks are fundamentally reshaping packaging specifications across beverage, food service, and pharmaceutical sectors, creating direct compliance incentives for Bag-in-Box Packaging Market adoption.

The European Union's Packaging and Packaging Waste Regulation PPWR mandates that all packaging be recyclable or reusable by January 1, 2030, with specific minimum recycled content requirements implemented progressively: 50% for glass, 70% for paper/cardboard, and 25-30% for plastic packaging beginning in 2030.

Germany's revised Packaging Act VerpackG establishes complementary requirements mandating 65% packaging waste recycling by 2025, increasing to 70% by 2030, with specific quotas for plastics 50% by 2025, 55% by 2030; glass 70% by 2025, 75% by 2030, and paper/cardboard 75% by 2025, 85% by 2030.

India's regulatory framework similarly mandates minimum recycled plastic content in new packaging as part of the Central Pollution Control Board's compliance monitoring requirements, creating regional compliance obligations affecting global beverage manufacturers operating in Indian markets.

Cost-Effectiveness and Supply Chain Optimisation Throughout Distribution Networks

Economic advantages inherent to bag-in-box packaging architecture create financial incentives supporting market expansion across cost-sensitive beverage and food service segments. The lightweight material composition of flexible bags, typically LDPE/EVOH/LDPE laminate structures, reduces transportation weight by approximately 60-70% compared to equivalent glass packaging systems, directly lowering logistics costs per unit shipped.

Beverage packaging research validates that bag-in-box systems enable higher product density per shipment; a single pallet of bag-in-box wine shipments accommodates approximately 25-30% greater volume compared to glass bottle equivalent shipments, reducing per-unit transportation expenditure and associated carbon emissions.

Food service operations prioritise bag-in-box adoption for operational efficiency advantages: compact storage footprint reduces facility space requirements compared to bulk barrel or drum systems, while integrated tap/dispenser systems enable precise portion control and reduce product waste through improved dispensing accuracy.

The United States flexible packaging industry generated US$ 41.5 billion in sales in 2022, with the Bag-in-Box Packaging Market representing approximately 8-10% of flexible packaging applications; this substantial base reflects established cost competitiveness versus rigid container alternatives across high-volume distribution channels.

Commercial kitchen operations and quick-service restaurants report 15-25% cost reduction in packaging-related expenditures, i.e., materials, storage, disposal, when transitioning from bulk barrels to standardised bag-in-box configurations.

Supply chain optimisation extends beyond transportation cost reduction; collapsible bag design enables reverse logistics efficiency for reusable outer carton systems, reducing empty container return shipping requirements and supporting circular packaging models.

Restraint - Packaging Standardisation Limitations and Customisation Cost Barriers

Bag-in-box packaging requires significant customisation investment to optimise performance for specific product formulations, barrier requirements, and dispensing specifications, creating financial barriers restricting adoption among smaller beverage manufacturers and emerging brand producers.

Custom bag films require polymer selection balancing oxygen transmission rate (OTR), moisture vapour transmission rate (MVTR), and chemical compatibility specifications calibrated for specific product chemistry; dairy applications require distinct barrier properties compared to juice, wine, or chemical formulations.

Fitment and tap design selection requires compatibility validation with specific dispensing flow rates, temperature stability across ambient storage conditions, and hygienic design meeting food safety compliance requirements.

Small producers and regional beverage manufacturers with annual volumes under 5 million units face unit cost premiums of 25-40% compared to large-scale manufacturers achieving economies of scale through dedicated production lines.

Alternative packaging systems (glass, PET bottles, Tetra Pak) offer standardised catalogue configurations enabling immediate deployment without significant engineering investment, creating a competitive disadvantage for bag-in-box adoption among cost-constrained producers.

Custom fitment development requires minimum order commitments frequently exceeding 100,000-250,000 units, restricting adoption for limited-edition products, specialty beverages, or regional brands operating below these production thresholds.

Opportunities - Pharmaceutical and Healthcare Liquid Packaging Expansion Driven by Aseptic Technology and Speciality Formulations

Pharmaceutical and healthcare liquid packaging represents an emerging growth segment for the bag-in-box packaging market as speciality pharmaceutical manufacturers and contract manufacturing organisations expand adoption of flexible packaging for oral solutions, injectable precursors, diagnostic reagents, and intermediate bulk container (IBC) applications. Aseptic bag-in-box filling technology, exemplified by Rapak Intasept® double-membrane systems with heat-sealed closure capabilities before and after filling, enables sterile pharmaceutical product packaging without chemical sterilising agents, supporting regulatory compliance for FDA and EMA guidelines.

Pharmaceutical liquid formulations increasingly utilise bag-in-box for bulk transportation of drug substances between manufacturing sites, contract manufacturing organisations, and clinical trial distributions.

Liquibox's Intasept® aseptic technology with single-use durable bags incorporating superior oxygen and moisture barrier properties and drop protection capabilities demonstrates pharmaceutical-grade performance standards supporting contamination prevention during extended shipping and storage.

E-Commerce and Direct-to-Consumer Beverage Distribution Channel Expansion

Rapid expansion of e-commerce channels in the food and beverage sector, particularly post-2020 direct-to-consumer (D2C) models for wine, craft beverages, and speciality drinks, is driving significant growth opportunities. Consumers increasingly purchase beverages online with home delivery, creating demand for packaging that is lightweight, breakage-resistant, and compact for efficient storage and shipping. Bag-in-box formats meet these requirements effectively, offering reduced shipping costs, tamper-proof designs, and integrated dispensing systems that maintain product integrity during multi-day transit.

Quick-commerce and dark-store operations in emerging markets, particularly India and Southeast Asia, are increasingly adopting bag-in-box packaging for back-of-house storage, supporting rapid fulfilment and on-demand delivery models. The 5–10 litre capacity segment is witnessing strong adoption due to its optimised bulk format for warehouse storage and logistics efficiency. Subscription beverage services and craft D2C brands are also prioritising bag-in-box formats for cost optimization while maintaining product quality.

Global e-commerce trends further support this opportunity. In India, the e-commerce industry is projected to grow from US$ 125 billion in 2024 to US$ 345 billion by 2030, fueled by 270 million online shoppers and rapid digital adoption in tier II and III cities. Quick commerce in India is expanding at a 70–80% CAGR, and subscription e-commerce is emerging as a high-growth segment. In the U.S., e-commerce accounted for 18.4% of retail sales in 2024, with total online retail sales projected to reach US$1.72 trillion by 2027. In the EU, the share of enterprises conducting e-sales increased from 17.2% in 2013 to 23.8% in 2023, with e-commerce turnover steadily rising, particularly among large enterprises.

These trends highlight that bag-in-box packaging aligns perfectly with the operational and logistical needs of e-commerce and D2C beverage distribution, making it a preferred solution for suppliers seeking to optimise costs, ensure product safety, and meet growing consumer demand for home-delivered beverages.

Category-wise Analysis

Capacity Insights

Small-capacity bag-in-box containers (up to 5 litres) dominate the Bag-in-Box Packaging Market, accounting for 62.5% of market volume and revenue, driven by widespread adoption across retail wine distribution, household beverage consumption, and foodservice quick-service restaurant applications.

The small-capacity segment benefits from established distribution relationships with retail supermarket chains, wine speciality retailers, and direct-to-consumer delivery services, which prioritise standardised sizing, enabling inventory management consistency. Manufacturing efficiency and packaging cost optimisation favour small-capacity production, with thermoforming and injection moulding processes achieving the highest throughput efficiency at smaller volumes, enabling competitive pricing.

Medium-capacity bag-in-box containers (5-20 litres) represent the fastest-growing market segment, driven by foodservice sector expansion, quick-commerce dark store adoption, and emerging pharmaceutical liquid packaging applications.

Foodservice operators increasingly standardise on 10-liter bag-in-box systems for beverages, cooking oils, sauces, and liquid seasonings, supporting bulk dispensing efficiency and waste reduction through improved portion control. Quick-commerce operations in Asia-Pacific markets increasingly utilise 5-10 litre configurations for back-of-house beverage and juice concentrate storage, enabling rapid fulfilment of on-demand delivery orders while optimising warehouse space utilisation.

Tap Insights

Bag-in-box packages with integrated tap/dispenser systems command a dominant market share of around 66% in 2025, reflecting consumer and commercial preference for convenience, controlled dispensing, and product protection.

Integrated tap technology enables precise portion control, reducing product waste, addresses food safety concerns through minimised oxygen exposure, and provides user-friendly operational simplicity, supporting widespread adoption across retail and foodservice environments. Tap design innovation drives competitive differentiation; premium tap systems incorporate drip-catch mechanisms, flow regulation features, and hygiene designs supporting food safety compliance.

Bulk bag-in-box systems without integrated tap mechanisms represent the fastest-growing segment, reflecting expansion in food manufacturing, chemical distribution, and pharmaceutical intermediate bulk container applications.

Non-tap configurations emphasise cost optimization and manufacturing efficiency; simplified design eliminates tap component manufacturing, assembly, and quality control requirements, reducing unit costs by 15-25% compared to tap-equipped alternatives.

Industrial and pharmaceutical bulk applications frequently eliminate tap integration; IBC implementations and chemical distribution rely on external connection systems enabling direct integration with processing equipment or transfer protocols.

Industry Insights

The food and beverage segment dominates the bag-in-box packaging market demand, reflecting a share of around 63.5%, with established adoption across wine distribution, juice production, dairy products, cooking oil and sauce packaging, and beverage concentrate supply systems.

Wine represents the largest sub-segment; North American annual bag-in-box wine consumption exceeds 200 million units, with European consumption surpassing 150 million units annually, reflecting mature market penetration within wine distribution channels.

Juice and juice concentrate applications similarly demonstrate substantial market volume; beverage manufacturers utilise bag-in-box for fountain drink concentrates, post-mix solutions, and ready-to-drink juice products delivered to foodservice operations and retail customers. Dairy liquid products, including milk, cream, and non-dairy milk alternatives, utilise bag-in-box for institutional foodservice distribution, supporting portion control and operational efficiency in cafeteria and institutional food service environments.

Regional Insights and Trends

North America Bag-in-Box Packaging Market Trends

North America maintains the largest regional market share of around 32% globally, supported by established wine consumption patterns, dominant beverage industry infrastructure, and food service sector sophistication.

The United States flexible packaging industry generated US$ 41.5 billion in sales in 2022, with bag-in-box representing approximately 8-10% of flexible packaging applications; a substantial base reflects established cost competitiveness versus rigid container alternatives across high-volume distribution channels.

The North American beverage market serves major branded manufacturers (PepsiCo, Kellogg Company, Tyson Foods) deploying bag-in-box systems across diverse applications from juice concentrates to cooking oils and sauces.

Wine-on-tap expansion in restaurants, bars, and hospitality venues accelerates bag-in-box adoption; premium beverage positioning through wine-on-tap service delivery supports market growth as operators recognize competitive advantages, including reduced waste, improved cost economics, and enhanced freshness guarantee.

E-commerce channel expansion in North America drives bag-in-box adoption; lightweight, compact design reduces dimensional weight shipping costs while durability addresses logistics damage concerns inherent to glass packaging.

East Asia Bag-in-Box Packaging Market Trends

East Asia represents a rapidly expanding regional market for the Bag-in-Box Packaging Market, capturing an estimated 22% market share in 2025, driven by beverage industry expansion, wine consumption growth among emerging middle-class consumers, and pharmaceutical manufacturing development.

China and Japan emerged as leading adoption markets during 2023–2025, with Chinese wine producers such as Changyu Pioneer Wine and Great Wall Wine, along with beverage manufacturers, increasingly deploying bag-in-box systems for domestic consumption and regional distribution.

Urban household penetration of packaged beverages in China and India demonstrates robust consumption growth; rapid urbanisation and rising middle-class populations generate incremental demand for convenient, cost-effective beverage packaging, supporting accelerated bag-in-box adoption.

Japan maintains a sophisticated food service infrastructure with premium beverage standards; Suntory and Mercian Corporation's premium wine offerings in 1.5–3 litre bag-in-box formats demonstrate strong market acceptance in hospitality venues and retail channels. South Korea leverages advanced manufacturing capabilities, enabling beverage and pharmaceutical manufacturers to utilize sophisticated packaging technologies and logistics infrastructure, supporting regional distribution network development.

Europe Bag-in-Box Packaging Market Trends

Europe commands the second-largest regional market share, around 27% within the Bag-in-Box Packaging Market, supported by mature wine industry infrastructure, established foodservice sector sophistication, and a stringent sustainability regulatory environment.

European wine-producing regions such as France, Italy, and Spain maintain leadership in bag-in-box wine adoption; established brand producers increasingly offer premium and mid-tier selections in bag-in-box formats targeting restaurant and hospitality channels, with the premium wine segment within bag-in-box exhibiting strong market acceptance.

The European Union Packaging and Packaging Waste Regulation 2025/40, effective August 2026, mandates fundamental packaging strategy transformation; minimum recycled content requirements of 50% for glass, 70% for paper/cardboard, and 25-30% for plastic beginning 2030, and packaging waste reduction targets of 5% by 2030, 10% by 2035, and 15% by 2040, create regulatory incentives favoring bag-in-box formats achieving inherent material efficiency advantages.

Competitive Landscape

The global Bag-in-Box Packaging market is moderately consolidated, characterised by the presence of several well-established global players alongside numerous regional and local manufacturers.

Leading companies such as Smurfit Kappa, DS Smith, Scholle IPN Corporation, Liqui-Box Corporation, and Amcor plc dominate the market through extensive product portfolios, technological innovation, and global distribution networks. The market is driven by demand for flexible, sustainable, and cost-effective packaging solutions across food & beverages, pharmaceuticals, and industrial applications.

Regional players are increasingly gaining traction by offering niche or customised solutions, intensifying competition. Strategic collaborations, mergers, and acquisitions are common as companies expand manufacturing capacity, enhance global reach, and strengthen service capabilities.

Key Industry Developments:

- In May 2025, SIG celebrated the 70th anniversary of the bag-in-box innovation and evolving it into a fully integrated packaging system, incorporating aseptic and chilled cartons, spouted pouches, recycle-ready films, and advanced connector fitments, enhancing efficiency, product integrity, and operational flexibility across food, beverage, and industrial applications.

- In Sept 2025, Smurfit Westrock’s launch of the Bag-in-Box Powergrip, featuring a cardboard casing, integrated handle, and vacuum bag design that reduces plastic use by up to 75%, enhances content protection, and helps companies comply with upcoming European packaging regulations while improving operational efficiency.

- In Oct 2024, SIG’s recognition by the Association of Plastic Recyclers (APR) for its Terra RecShield D bag-in-box package, making it the first solution for post-mix beverage concentrates to meet the highest recyclability criteria, featuring durable laminate and fitments that enable over 99.8% product evacuation while supporting sustainability and circular packaging goals.

Frequently Asked Questions

The global Bag-in-Box Packaging Market is projected to be valued at US$ 3.5 Bn in 2025.

The Food & Beverages segment is expected to account for approximately 63.5% of the global Bag-in-Box Packaging Market by End Use Industry in 2025.

The market is expected to witness a CAGR of 4.8% from 2025 to 2032.

The Bag-in-Box Packaging Market growth is driven by increasing regulatory and sustainability mandates requiring recyclable or reusable packaging, coupled with the cost-effectiveness, lightweight design, operational efficiency, and supply chain optimisation benefits of flexible bag systems.

Key market opportunities in the Bag-in-Box Packaging Market lie in the expanding pharmaceutical and healthcare liquid packaging segment.

The key players in the Bag-in-Box Packaging market include Smurfit Kappa, DS Smith, Scholle IPN Corporation, Liqui-Box Corporation, and Amcor plc.