- Animal Health

- Animal Wound Care Market

Animal Wound Care Market Size, Trends, hare, Growth, and Regional Forecast, 2025 to 2033

Animal Wound Care Market by Product (Surgical Wound Care, Traditional Wound Care, Advanced Wound Care), by Animal Type (Companion Animal, Livestock Animal), by End User (Veterinary Hospitals, Veterinary Clinics, Home Care), by Regional Analysis, from 2026 to 2033

Animal Wound Care Market Share and Trends Analysis

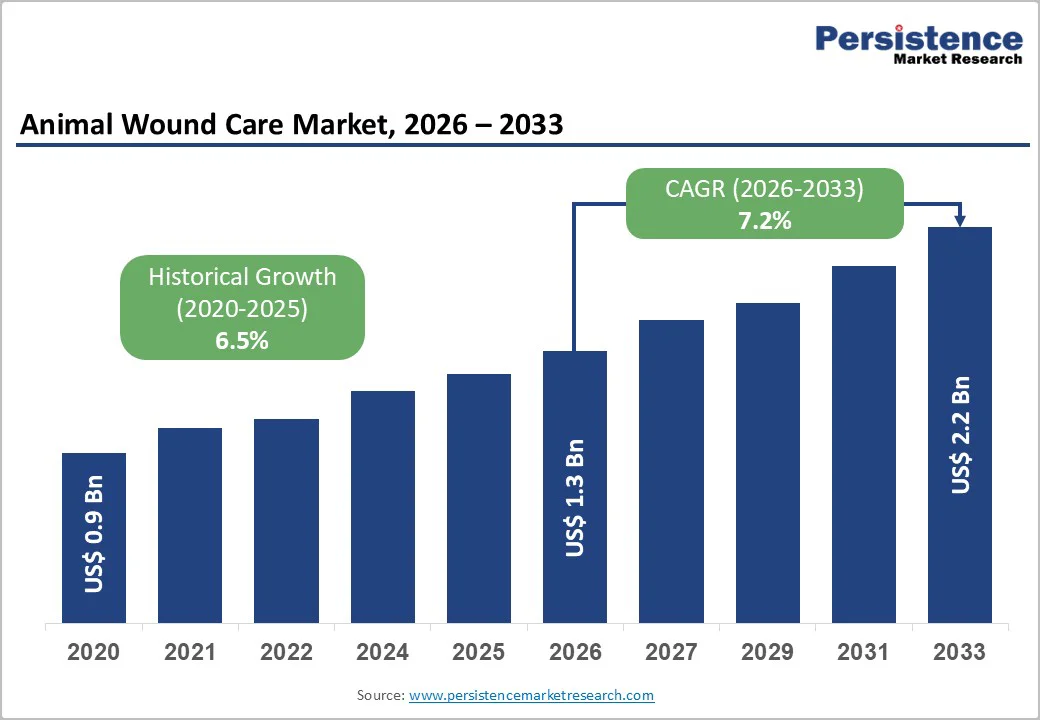

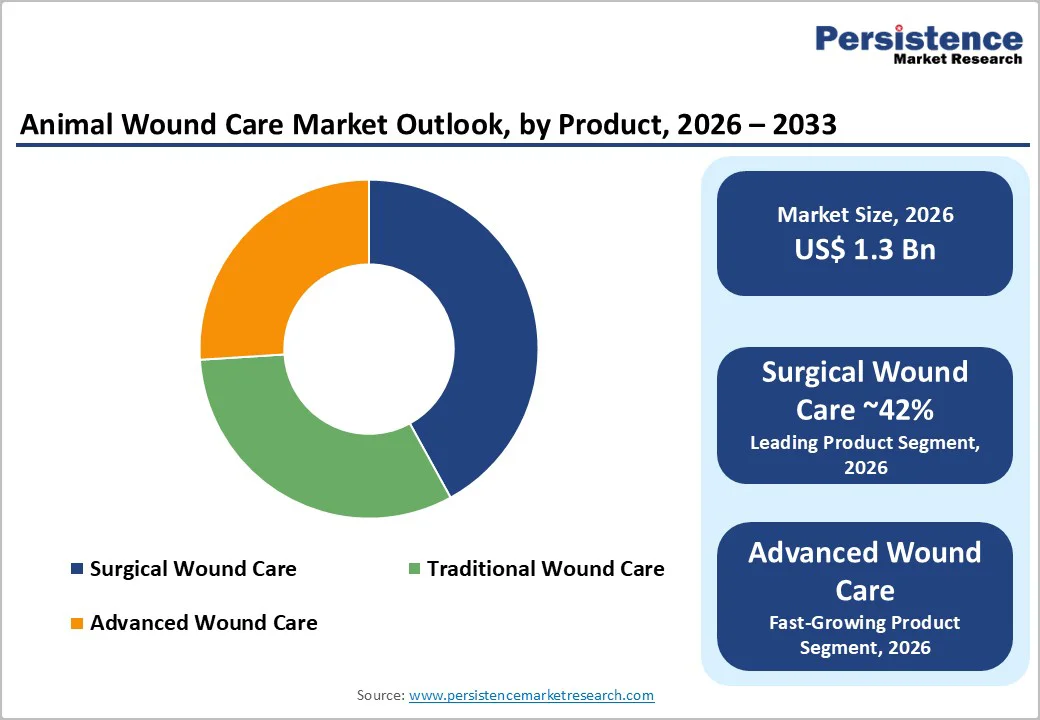

The global animal wound care market size is estimated to grow from US$ 1.3 billion in 2026 and projected to reach US$ 2.2 billion by 2033.

The market is projected to record a CAGR of 7.2% during the forecast period from 2026 to 2033. The global market is witnessing strong growth driven by a surge in pet ownership, increasing veterinary healthcare expenditure, and wider availability of advanced wound management solutions for both companion and livestock animals.

Animal surgeries have risen significantly with improved access to veterinary services, while greater awareness of animal welfare has encouraged timely treatment of injuries and post-operative care. Factors such as animal accidents, bites, and chronic wounds are also boosting the need for reliable dressings, bandages, tissue adhesives, and surgical wound care products.

Key Industry Highlights

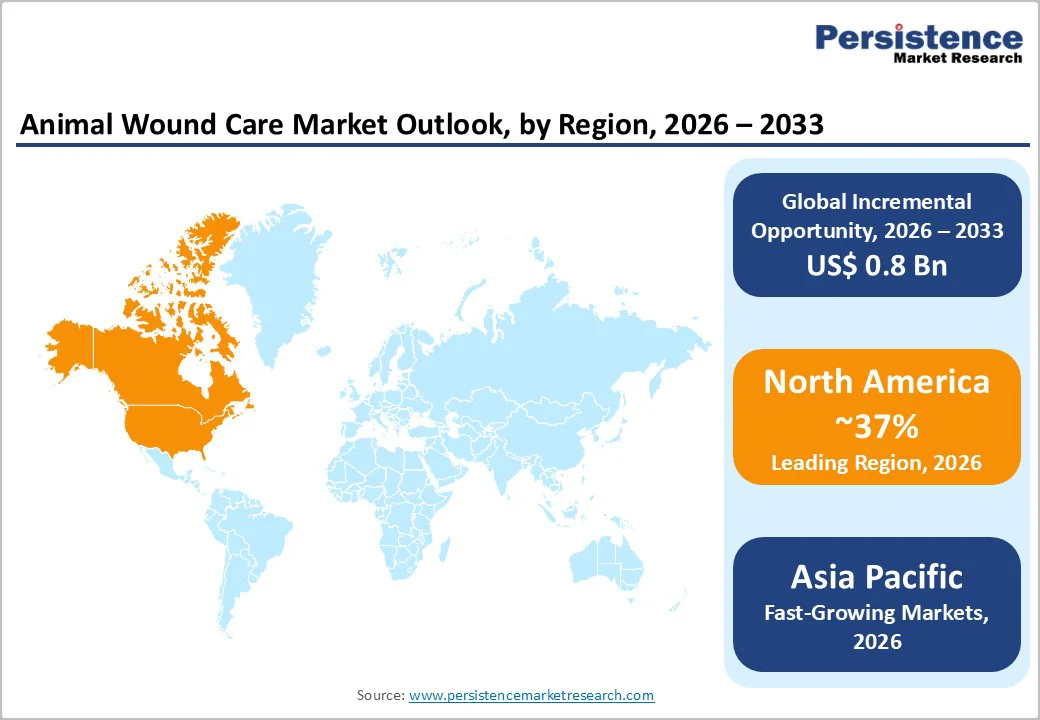

- Leading Region: North America holds the largest market share in 2025 for animal wound care, backed by robust veterinary infrastructure, high pet ownership rates, and strong regulatory oversight.

- Fastest Growing Region: Asia Pacific emerges fastest in growth, driven by rising pet ownership, increasing awareness of animal health, and expanding veterinary services.

- Dominant Segment: Surgical wound care products are the leading segment in 2025, accounting for more than 42% market share due to their critical role in veterinary surgeries.

- Fastest Growing Opportunity: The home care segment exhibits the highest growth, fuelled by demand for convenient and effective wound care solutions for pets.

| Key Insights | Details |

|---|---|

| Animal Wound Care Market Size (2026E) | US$ 1.3 Bn |

| Market Value Forecast (2033F) | US$ 2.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.2% |

| Historical Market Growth (CAGR 2020 to 2024) | 6.5% |

Market Dynamics

Driver - Rising Pet Ownership and Humanization of Pets

The surge in pet ownership across many regions, coupled with the growing humanization of pets, has significantly reshaped consumer expectations around animal healthcare. Today, pet owners view their animals as family members and are more proactive about seeking quality medical care rather than relying on basic first-aid or home remedies.

This emotional connection has fueled higher spending on preventive and post-surgical treatments, leading to a spike in demand for advanced wound care solutions. According to the American Pet Products Association (APPA), more than 70% of U.S. households now own a pet, and annual expenditure on pet healthcare has increased sharply over the past decade.

Similar trends are being observed in Europe and urban areas across Asia Pacific, where veterinary hospitals and pet clinics are reporting increased caseloads of wound treatments, surgeries, and post-operative care. The availability of specialized products such as moisture-retentive dressings, tissue adhesives, sutures, and antimicrobial sprays has further encouraged pet owners to opt for professional care rather than temporary fixes.

As awareness of proper wound management expands through social media, veterinary education campaigns, and pet insurance adoption, demand for high-quality wound care products is expected to continue its upward trajectory.

Restraints - High Cost of Advanced Wound Care Products

Despite strong demand trends, the high pricing of advanced wound care products remains a major obstacle to widespread market penetration. Solutions such as hydrogels, hydrocolloids, foam dressings, and bioactive formulations deliver superior healing outcomes, yet their premium cost places them out of reach for many pet owners.

This limitation is particularly evident in developing regions where disposable income is lower and veterinary care is often paid out-of-pocket. Livestock farmers face an additional challenge, as treating multiple animals with high-cost products becomes economically impractical, prompting them to rely on inexpensive topical agents or basic bandages.

Even in developed countries, lack of reimbursement systems for veterinary care means not all pet owners can afford advanced treatments recommended by veterinarians. Clinics in cost-sensitive markets often hesitate to stock premium wound care if demand is unpredictable, which further slows adoption.

While manufacturers have begun offering smaller pack sizes and economy variants, price sensitivity continues to restrict market expansion. Unless costs are reduced through innovation, large-scale production, or subsidies, many consumers will continue to choose affordable alternatives rather than specialized wound healing products, limiting the market’s overall growth potential.

Opportunity - Technological Advancements in Wound Care

Technological innovation is emerging as one of the most promising growth avenues for the animal wound care market. Veterinary medicine is increasingly adopting solutions once reserved for human healthcare, including bioactive dressings, nanofiber scaffolds, antimicrobial peptide formulations, and controlled-release wound healing systems.

These next-generation products promote faster tissue repair, reduce infection risk, and minimize dressing-change frequency, benefits highly valued by veterinarians and pet owners alike. Controlled-release formulations, for example, steadily deliver therapeutic agents, improving compliance and reducing stress for animals requiring long-term care.

The integration of natural biomaterials, probiotics for wound healing, and smart dressings that monitor moisture levels are also gaining attention. Companies investing in R&D and applying clinical evidence to their product portfolios are positioned to stand out in an increasingly competitive field.

Demand for such innovations is further supported by the rise of pet insurance, specialty veterinary hospitals, and rehabilitation centers, which prioritize advanced care for trauma and post-surgical recovery. As awareness spreads and prices gradually decrease over time, technologically enhanced wound care solutions are expected to play a transformative role in shaping the future of veterinary treatment.

Category-wise Analysis

By Product Type Insights

Surgical wound care products accounted for nearly 42% of the total market share in 2025, making it the leading segment within the animal wound care industry. This category comprises sutures, staples, tissue adhesives, wound closure strips and related post-operative care materials, all of which play a vital role in ensuring proper healing after surgical procedures.

The steady rise in veterinary surgeries, including spaying and neutering, orthopedic repair, tumor removal, fracture fixation, and soft tissue procedures continues to drive demand for these products. As veterinary professionals increasingly prioritize faster healing, reduced infection rates and improved recovery outcomes, surgical wound solutions have become the primary choice due to their reliability and proven effectiveness.

The expansion of veterinary specialty hospitals and the adoption of minimally invasive procedures are also increasing the use of medical-grade closure devices and adhesives. With a growing emphasis on structured post-surgical care protocols, the dominance of the surgical wound segment is expected to remain strong across both companion and livestock animal healthcare settings.

By Animal Type Insights

Companion animals held about 65% of global animal wound care consumption in 2025, making them the largest end-user group in the market. The sharp growth in pet adoption, expanding pet insurance coverage, and greater willingness among owners to invest in high-quality treatment contribute significantly to this dominance.

Dogs and cats account for the majority of veterinary wound care cases, with a high incidence of accidental injuries, bite wounds, post-operative wounds and chronic dermatological issues requiring professional management. As pets are increasingly viewed as family members, owners are more inclined to pursue advanced care options such as antimicrobial dressings, bioactive products and premium bandaging systems.

Livestock animals represent the fastest-growing segment, fueled by rising awareness of animal welfare in the farming sector and economic losses associated with untreated wounds among cattle, sheep and horses. Growth opportunities are especially strong in regions with expanding commercial livestock operations, where infection control and faster wound recovery directly impact productivity and animal health outcomes.

Region-wise Insights

North America Animal Wound Care Market Trends

North America remains the largest market for animal wound care products, holding an estimated 37% share in 2025. The U.S. leads the regional market due to high pet ownership, well-developed veterinary infrastructure, and a stringent regulatory environment that ensures quality standards for wound care products.

Veterinarians and pet owners increasingly prefer advanced solutions such as bioactive dressings, hydrocolloids, and barrier gels, which offer faster healing and reduce infection risk.

The growing humanization of pets has prompted owners to invest more in animal healthcare, further supporting market expansion. In addition, rising healthcare expenditures and the trend of specialized veterinary clinics and animal hospitals have strengthened demand for premium wound care products.

Home care solutions are also gaining popularity as pet owners look for convenient, effective ways to manage wounds outside clinical settings. Online procurement platforms, telemedicine consultations, and direct-to-consumer delivery models are facilitating access to these products.

This combination of advanced veterinary services, consumer awareness, and digital availability continues to create new growth opportunities, reinforcing North America’s position as a dominant and innovation-driven market for animal wound care products.

Europe Animal Wound Care Market Trends

Europe represents a significant market for animal wound care, driven by high standards for animal welfare and robust healthcare regulations. Countries such as Germany, the U.K., and France dominate the regional market due to strong veterinary infrastructure and a large population of companion animals.

Regulatory oversight by the European Union ensures the safe use of advanced wound care products, encouraging veterinarians and pet owners to adopt high-quality dressings, topical therapies, and post-surgical care solutions. The increasing trend of pet ownership and willingness to spend on animal healthcare is further contributing to market growth.

European veterinary hospitals and clinics are expanding, leading to higher veterinary visits and greater consumption of wound care products.

Manufacturers in the region are investing heavily in research and development to introduce technologically advanced solutions such as bioactive dressings, controlled-release topical agents, and antimicrobial gels. These innovations are enhancing treatment outcomes, accelerating healing, and preventing infection.

The combination of supportive regulations, growing pet populations, and a focus on R&D positions Europe as a hub for advanced animal wound care, providing both domestic and export opportunities for market players.

Asia and Pacific Animal Wound Care Market Trends

The Asia Pacific region is emerging as the fastest-growing market for animal wound care products, driven by rising pet ownership, increasing awareness of animal health, and expanding veterinary infrastructure.

Countries such as China, Japan, and India are experiencing a surge in animal surgeries, including spaying, neutering, orthopedic procedures, and post-trauma care, creating higher demand for advanced wound management solutions. The region benefits from cost-effective manufacturing capabilities, allowing local companies to produce high-quality wound care products at competitive prices for both domestic consumption and export markets.

Increasing government initiatives and private investment in veterinary healthcare are contributing to the expansion of animal hospitals, clinics, and specialty care centers, which further boosts the adoption of surgical dressings, barrier gels, and antimicrobial wound care products.

Urbanization and rising disposable incomes have also led pet owners to prioritize professional medical care over home remedies, enhancing the uptake of advanced solutions. As awareness about infection prevention and faster healing grows among veterinarians and animal caregivers, the region is expected to continue its strong growth trajectory, solidifying its position as a key driver of global animal wound care market expansion in the coming years.

Competitive Landscape

The global animal wound care market is moderately consolidated, with a few key players dominating the industry. Major companies focus on mergers, geographic expansion, and product portfolio enhancements. Manufacturers invest in research for next-generation wound care products, including bioactive dressings and controlled-release formulations.

Key success factors include regulatory compliance, trust built on quality certification, and after-sales support. Innovative companies differentiate with customized offerings and integrated logistics solutions, as seen in their collaborations with veterinary institutions and government procurement agencies.

Key Industry Developments:

- In September 2025, Nupsala introduced Cuvestrequin, an innovative antibiotic-free, waterproof topical barrier gel for horses with broken or irritated skin, offering an alternative to traditional bandaging for effective wound management.

- In May 2025, KeraVet Bio launched KeraVet Gel nationwide, accompanied by a full rebranding of the company. The topical therapy aids in surgical incision care and wound management, promoting faster healing while preventing animals from licking the treated area.

Companies Covered in Animal Wound Care Market

- B. Braun Melsungen AG

- Medtronic Plc

- 3M Company

- Johnson & Johnson (Ethicon)

- Smith & Nephew Plc

- Bayer AG

- Virbac S.A.

- Ceva Sante` Animale

- de Biogénesis Bagó

- Acelity L.P. Inc.

- Neogen Corporation

- Biovet AD (Huvepharma)

- Dechra Pharmaceuticals

- Advancis Medical

- Others

Frequently Asked Questions

The global animal wound care market is projected to be valued at US$ 1.3 Bn in 2026.

The increasing pet ownership and humanization of pets are the key factors driving demand for animal wound care products.

The global market is poised to witness a CAGR of 7.2% between 2026 and 2033.

The greatest opportunity lies in advanced wound care products favored by veterinarians and pet owners for faster healing and infection prevention.

Key companies include B. Braun Melsungen AG, Medtronic Plc, 3M Company, Johnson & Johnson (Ethicon), and Smith & Nephew Plc.