- Animal Health

- Veterinary Medicine Market

Veterinary Medicine Market Size, Share, and Growth Forecast, 2025 - 2032

Veterinary Medicine Market By Animal Type (Production Animals, Companion Animals), Product Type (Biologics, Pharmaceuticals), Route of Administration (Oral, Injectable), Distribution Channel, and Regional Analysis for 2025 - 2032

Veterinary Medicine Market Size and Trends Analysis

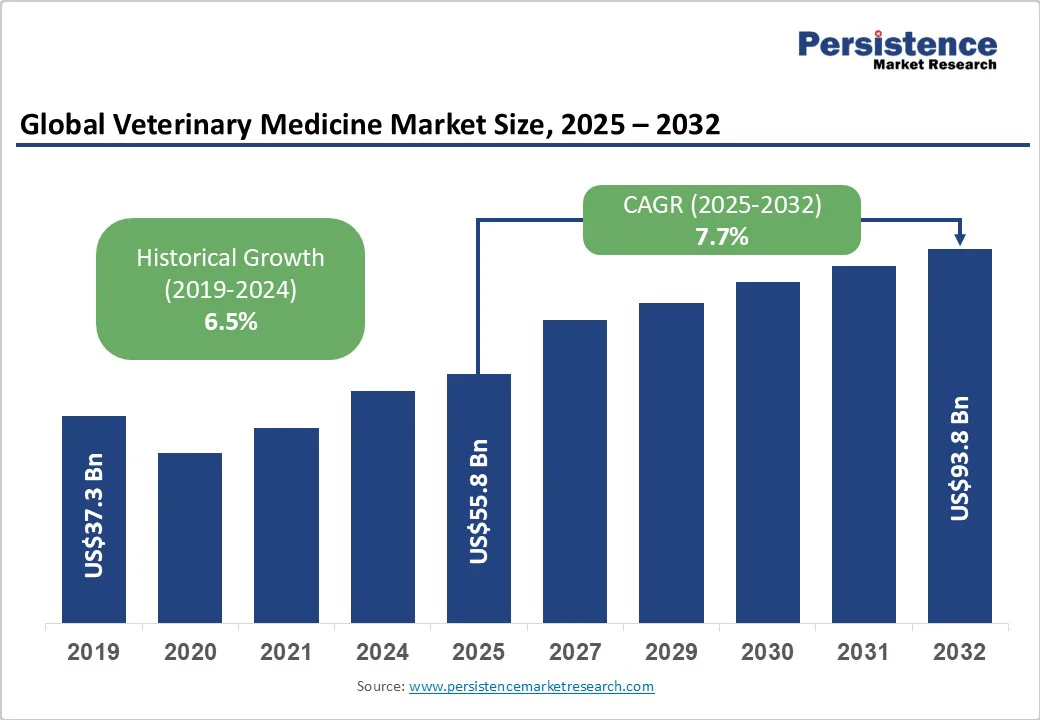

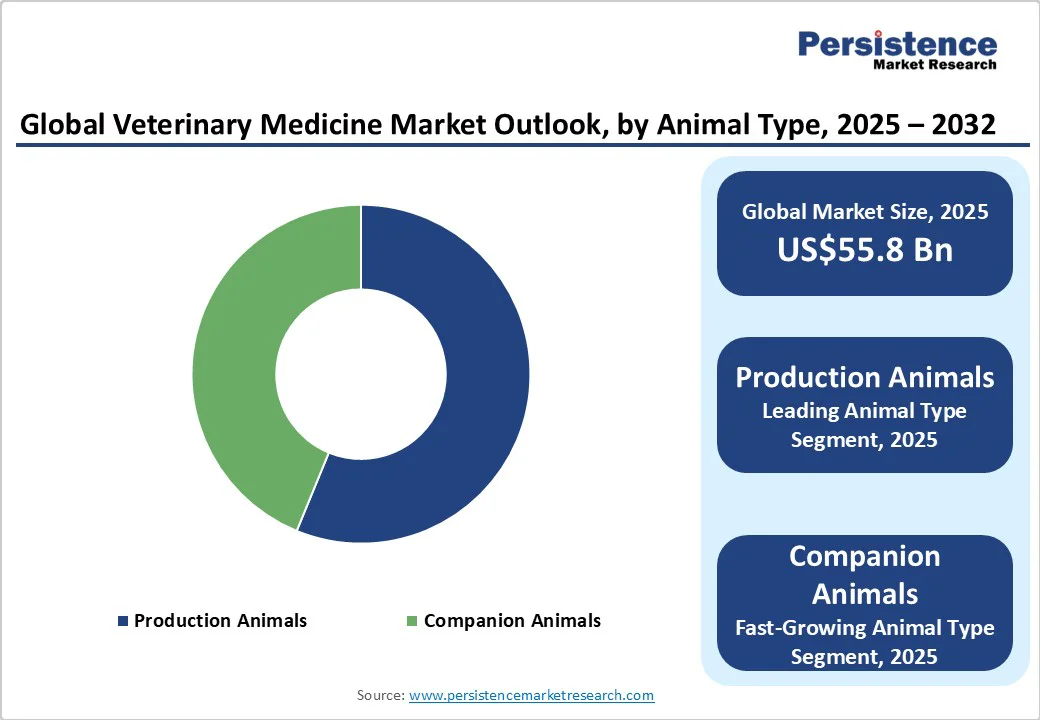

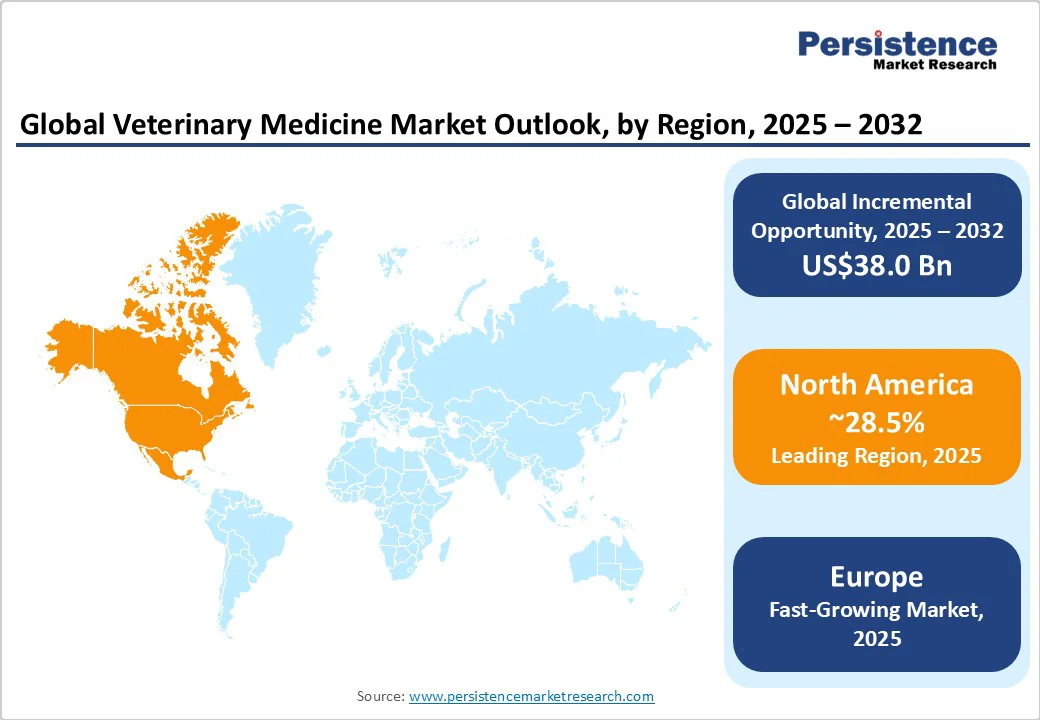

The global veterinary medicine market size is likely to be valued at US$55.8 Billion in 2025 and is estimated to reach US$93.8 Billion in 2032, growing at a CAGR of 7.7% during the forecast period 2025-2032, driven by rising pet ownership across Asia Pacific, Europe, and North America. This has raised the demand for preventive care, diagnostics, and specialized treatments.

Key Industry Highlights:

- New Launch: Virbac recently announced the launch of Vikaly in Europe. It is the world's first medicated feed for cats, combining renal kibble with a veterinary drug subject to marketing authorization.

- Leading Region: North America, with about 28.5% share in 2025, due to a well-established veterinary infrastructure and superior regulatory support.

- Fastest-growing Region: Europe, backed by increasing awareness of animal welfare and technological integration in veterinary practices.

- Leading Animal Type: Production animals hold nearly 56.2% share in 2025, with the expansion of livestock farming and a rising focus on disease prevention.

- Dominant Product Type: Pharmaceuticals, approximately 61.4% of the veterinary medicine market share in 2025, fueled by broad applicability across species.

- Key Route of Administration: Injectables are likely to record about 54.7% share in 2025, backed by the rapid onset of action and precise dosing.

| Key Insights | Details |

|---|---|

|

Veterinary Medicine Market Size (2025E) |

US$55.8 Billion |

|

Market Value Forecast (2032F) |

US$93.8 Billion |

|

Projected Growth (CAGR 2025 to 2032) |

7.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Surge in Pet Ownership Globally

The rising trend of pet ownership is a major driver. Across urban and semi-urban regions in Asia Pacific, Europe, and North America, pets are now seen as family members, prompting owners to invest in regular healthcare, preventive treatments, and specialized services. In China, for example, the number of pet dogs and cats has risen sharply in recent years, fueling demand for veterinary consultations, vaccinations, and wellness programs.

As of 2024, China was home to approximately 187 million pet dogs and cats, according to the Asia Pet Research Institute. This cultural shift has also expanded services such as dental care, physiotherapy, and nutritional counseling, creating new revenue streams for veterinary practices. Practices are now integrating telemedicine and AI-backed diagnostics to meet the expectations of owners seeking convenience and high-quality care.

Rising Popularity of Pet Insurance

The increasing adoption of pet insurance is accelerating veterinary medicine demand by making novel treatments more accessible to owners. Policies that cover diagnostics, surgeries, and ongoing medical care encourage owners to pursue comprehensive treatment plans without the barrier of high upfront costs.

In the U.K., for instance, pet insurance penetration has grown steadily, prompting veterinarians to deliver sophisticated services, including oncology and orthopedic interventions. Insurance also motivates preventive care, as routine check-ups and vaccinations are often covered, which strengthens the emphasis on early disease detection.

Barrier Analysis - Proliferation of Counterfeit Veterinary Medications

The rising prevalence of counterfeit veterinary medicines poses a threat to animal health and the integrity of veterinary care. These substandard and falsified (SF) products often contain incorrect or insufficient active ingredients or harmful substances, leading to treatment failures, adverse reactions, and the development of antimicrobial resistance.

For instance, in Telangana, India, authorities seized illegal veterinary medicines worth Rs. 90,000, including antibiotics and antifungal drugs, from unlicensed sources. Such incidents highlight the challenges in ensuring the safety and efficacy of veterinary treatments, especially in regions with limited regulatory oversight.

Short Duration of Product Exclusivity

The limited duration of product exclusivity for veterinary medicines an hinder both innovation and the availability of affordable treatments. In the U.S., new animal drug products are granted five years of marketing exclusivity under the Federal Food, Drug, and Cosmetic Act, provided they have not been previously approved.

While this period allows the original manufacturer to recoup research and development costs, it may not be sufficient to incentivize the development of new therapies, especially for minor animal species or rare diseases. Also, the early entry of generic versions post-exclusivity can lead to price reductions, which may not always cater to the economic interests of innovators.

Opportunity Analysis - Wearable Sensors for Continuous Animal Health Monitoring

Wearable sensors are revolutionizing veterinary care by enabling real-time and continuous monitoring of animal health. Devices such as smart collars and ear tags equipped with sensors track vital signs, including heart rate, body temperature, and activity levels, providing veterinarians with immediate data to detect early signs of illness or distress. For instance, a recent study involving dogs with osteoarthritis demonstrated that smart collars could monitor activity and rest patterns over several weeks, aiding in the assessment of treatment efficacy. These technologies facilitate proactive care, allowing for timely interventions that can prevent the progression of diseases and improve animal welfare.

Nanomaterials for Targeted Drug Delivery and Vaccine Development

Nanomaterials are emerging as key tools in veterinary medicine, specifically in the development of targeted drug delivery systems and advanced vaccines. Nanoparticles such as liposomes, mesoporous silica, and chitosan-based carriers can encapsulate therapeutic agents, protecting them from degradation and facilitating controlled release at specific sites in the body.

This targeted approach refines the efficacy of treatments while minimizing side effects. In vaccine development, nanomaterials serve as adjuvants, improving the immune response and the stability of vaccines, which is essential for preventing diseases in livestock and companion animals.

Category-wise Analysis

Animal Type Insights

Production animals are predicted to account for approximately 56.2% share in 2025, owing to rising demand for animal protein, mainly from rapidly urbanizing populations in countries such as China and India. This demand has spurred increased livestock farming, leading to a rise in cattle, poultry, and swine populations. Consequently, there is a surging requirement for efficient feed production processes, with developments in feed technologies and the adoption of feed mixers playing a key role in meeting this demand.

Companion animals are expected to showcase a considerable CAGR through 2032 due to changing cultural attitudes and increasing disposable income. Urban populations, especially in Japan and South Korea, are increasingly adopting pets, viewing them as family members rather than mere animals. This shift is evident in the rising expenditure on pet care, including food, healthcare, and accessories. Developments in veterinary care, including the introduction of telemedicine services and specialized treatments, have improved the quality of life for companion animals.

Product Type Insights

Pharmaceuticals are estimated to record a share of nearly 61.4% in 2025, spurred by their established efficacy, regulatory approval pathways, and broad applicability across species. These chemically synthesized drugs, including antibiotics, anti-inflammatory agents, and antiparasitics, are rigorously tested for safety and effectiveness. Their production processes are well-defined, ensuring consistent quality and dosage forms, which is essential for treating a wide range of animal species.

Biologics are projected to witness a steady CAGR from 2025 to 2032, propelled by developments in biotechnology and a shift toward preventive and targeted therapies. These include vaccines, monoclonal antibodies, and gene therapies, which deliver precise mechanisms of action with fewer side effects compared to traditional pharmaceuticals. The increasing incidence of zoonotic diseases and a rising emphasis on animal welfare have accelerated the adoption of biologics.

Route of Administration Insights

Injectables are speculated to hold a share of about 54.7% in 2025 because of their rapid onset and precise dosing. They are beneficial for animals with compromised gastrointestinal function, such as those that are vomiting or debilitated, where oral administration would be ineffective. In addition, injectables bypass the digestive system, ensuring that drugs with poor oral bioavailability or those that are unstable in the gastrointestinal tract can be effectively delivered.

The oral route of administration remains a bedrock in veterinary practice due to its convenience and cost-effectiveness. It is advantageous for long-term treatments as it allows for easy administration of medications in food or water, facilitating mass treatment in livestock. The gastrointestinal tract provides a large surface area for drug absorption, making it suitable for administering a variety of medications.

Regional Insights

North America Veterinary Medicine Market Trends

North America is poised to account for approximately 28.5% share in 2025, backed by increased pet ownership, rising animal health awareness, and developments in veterinary care. Specialized treatments for both companion animals and livestock are in high demand, mainly vaccines, antibiotics, and anti-inflammatory medications. Technological developments such as biologics and digital diagnostic tools are improving treatment options and disease management. The prevalence of zoonotic diseases and a focus on preventive care further contribute to growth.

However, North America still faces significant workforce challenges. While the unemployment rate for veterinarians is low, at 0.7%, there is a misdistribution of professionals, with shortages specifically acute in rural areas. For instance, Washington state has requested funding to increase veterinary school enrollment to address these disparities. Additionally, the profession is grappling with high burnout rates and mental health concerns, worsened by factors such as high education costs and stressful working conditions.

Europe Veterinary Medicine Market Trends

Regulatory bodies in Europe are intensifying oversight in response to market dynamics. In the U.K., the Competition and Markets Authority (CMA) is investigating the veterinary sector due to concerns that market consolidation has led to high prices and reduced competition. The CMA's inquiry follows a significant public response highlighting issues such as a lack of pricing transparency and diminished consumer choice.

Veterinary practices across Europe are, however, grappling with substantial workforce shortages. The Federation of Veterinarians of Europe (FVE) reports that nearly half of veterinarians identify recruitment and staff shortages as important issues, with rural and remote areas being particularly affected. This shortage is leading to increased workloads and burnout among existing staff, raising concerns about the sustainability of veterinary services in underserved regions.

Asia Pacific Veterinary Medicine Market Trends

Asia Pacific is witnessing a steady growth due to rising pet ownership, increased livestock production, and surging awareness of animal health. China, India, and Japan are leading this growth with more pet owners seeking preventive care, specialized treatments, and wellness services. Workforce shortages remain a key challenge, particularly in rural areas, where qualified veterinarians are scarce.

High burnout and staff turnover in countries such as Australia are prompting practices to invest in training programs and technology to improve efficiency and retention. Technology is propelling development with AI-based diagnostics, machine learning for disease detection, and telemedicine platforms becoming more prevalent. For example, AI systems are used for swine disease detection, enabling faster and more accurate treatment planning.

Competitive Landscape

The global veterinary medicine market is characterized by consolidation, technological developments, and shifting consumer behaviors. Corporate entities and private equity firms continue to acquire independent veterinary practices, leading to increased service prices. Technological developments are transforming the market, with AI and telemedicine playing key roles. AI is being integrated into diagnostic tools and treatment planning, improving accuracy and efficiency. Telemedicine is expanding access to veterinary care, especially in underserved areas.

Business Strategies

The veterinary medicine sector is experiencing significant transformations propelled by innovation, cost leadership, and market expansion. Companies are adopting technology-driven solutions to refine service delivery and improve patient outcomes. For instance, AI-based diagnostic tools and telemedicine platforms are being integrated into veterinary practices, allowing for remote consultations and highly accurate diagnoses.

Key Industry Developments:

- In October 2025, countries in Latin America and the Caribbean established a consortium to collaboratively collect and generate data on veterinary drug residues used in food-producing animals. It will serve as a baseline for the establishment of Maximum Residue Limits (MRLs) aligned with Codex Alimentarius, thereby accelerating food safety.

- In July 2025, Washington State University’s College of Veterinary Medicine unveiled a new grant program to fund novel efforts aimed at boosting science and improving global health. The college recently awarded its first three grants through the newly established Pump Priming Research Program.

Companies Covered in Veterinary Medicine Market

- Zoetis Inc.

- Merck & Co., Inc.

- Boehringer Ingelheim International GmbH

- Biogénesis Bagó

- Bimeda Corporate

- Virbac

- Phibro Animal Health Corporation

- Ceva Santé Animale

- Dechra Pharmaceuticals PLC

- Elanco

Frequently Asked Questions

The veterinary medicine market is projected to reach US$55.8 Billion in 2025.

Key market drivers include the surge in pet ownership and the growth in livestock production.

The veterinary medicine market is poised to witness a CAGR of 7.7% from 2025 to 2032.

The development of smart monitoring devices and the emergence of personalized treatments are the key market opportunities.

Zoetis Inc., Merck & Co., Inc., and Boehringer Ingelheim International GmbH are a few key market players.