- Animal Health

- Animal Feed Enzymes Market

Animal Feed Enzymes Market Size, Share, and Growth Forecast, 2026 - 2033

Animal Feed Enzymes Market by Enzyme Type (Phytase, Carbohydrases, Others), Animal Type (Poultry, Swine, Others), Source, and Regional Analysis for 2026 - 2033

Animal Feed Enzymes Market Size and Trends Analysis

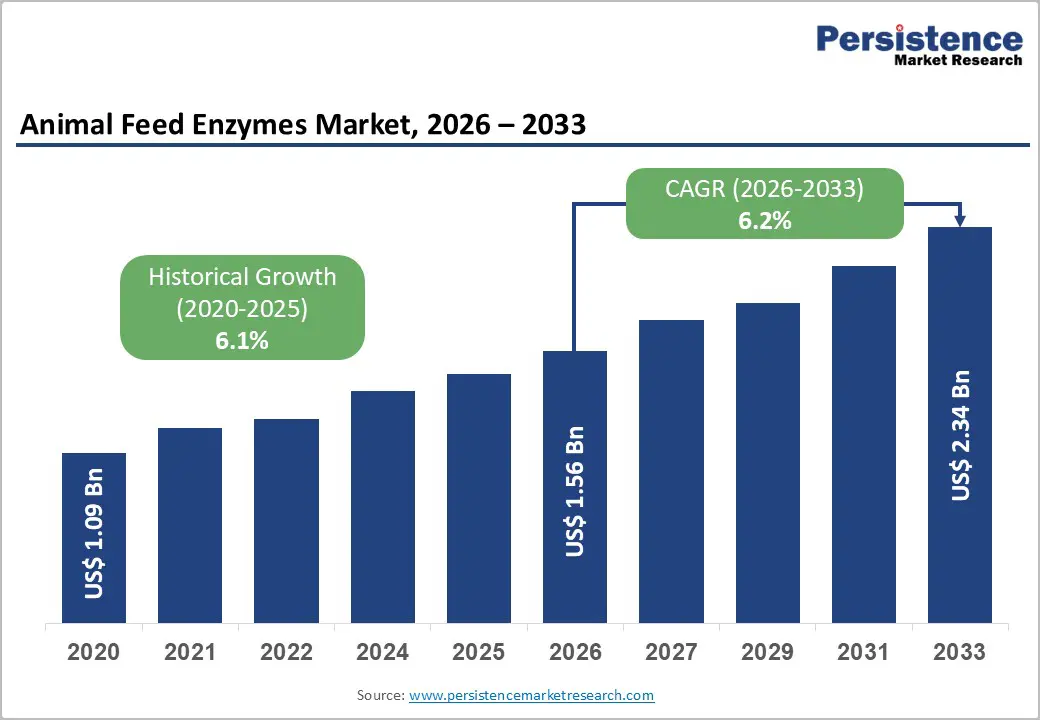

The global animal feed enzymes market size is likely to be valued at US$1.56 billion in 2026 and is expected to reach US$2.34 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033, driven by rising global consumption of animal protein, regulatory pressure to reduce antibiotic growth promoters in livestock production, and increasing emphasis on feed efficiency and nutrient utilization.

Technological advancements, including next-generation phytases, thermostable enzyme formulations, and multi-enzyme blends, are improving performance consistency and enabling the substitution of higher-cost feed ingredients. Sustainability mandates and feed-cost volatility are expected to further reinforce enzyme adoption across commercial livestock systems.

Key Industry Highlights:

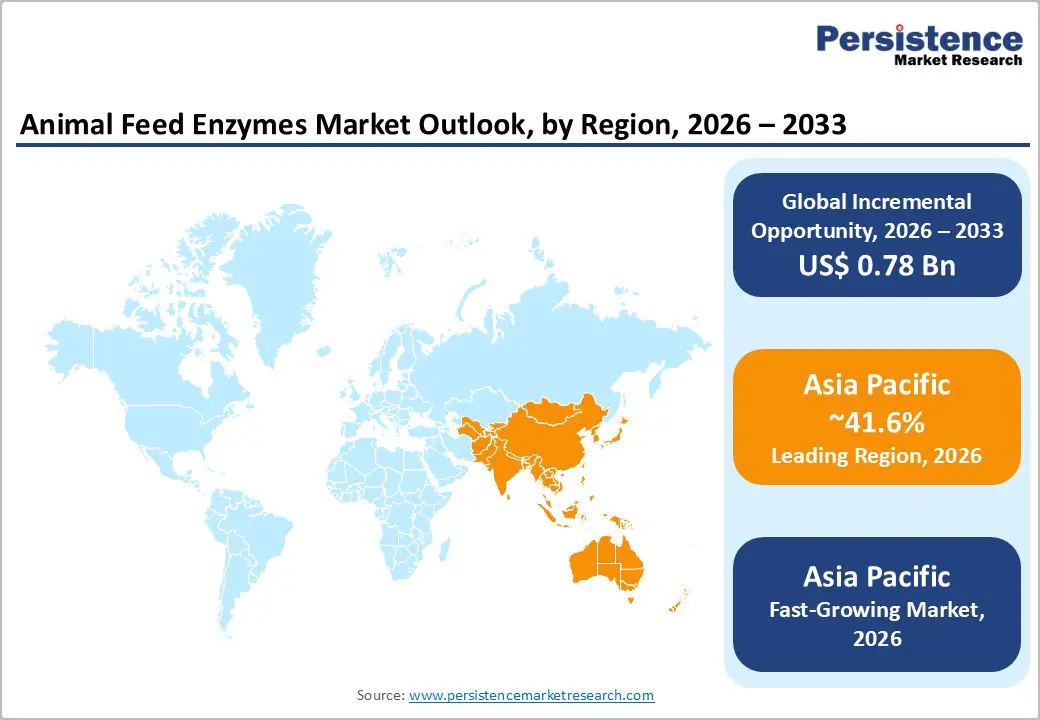

- Leading Region: Asia Pacific is projected to hold 41.6% of market share, driven by large-scale poultry and aquaculture production, rapid industrialization of the feed industry in China and India, and growing adoption of enzyme blends tailored to plant-based and by-product-rich diets.

- Fastest-growing Region: Asia Pacific, supported by expanding compound feed capacity, regulatory pressure on nutrient discharge, and increasing penetration of carbohydrases and multi-enzyme solutions in cost-sensitive markets.

- Investment Plans: Over 60% of major suppliers’ capital allocation is directed toward Asia Pacific and North America, with a focus on localized enzyme manufacturing, application laboratories, digital dosing systems, and technical service expansion to support integrators and feed mills.

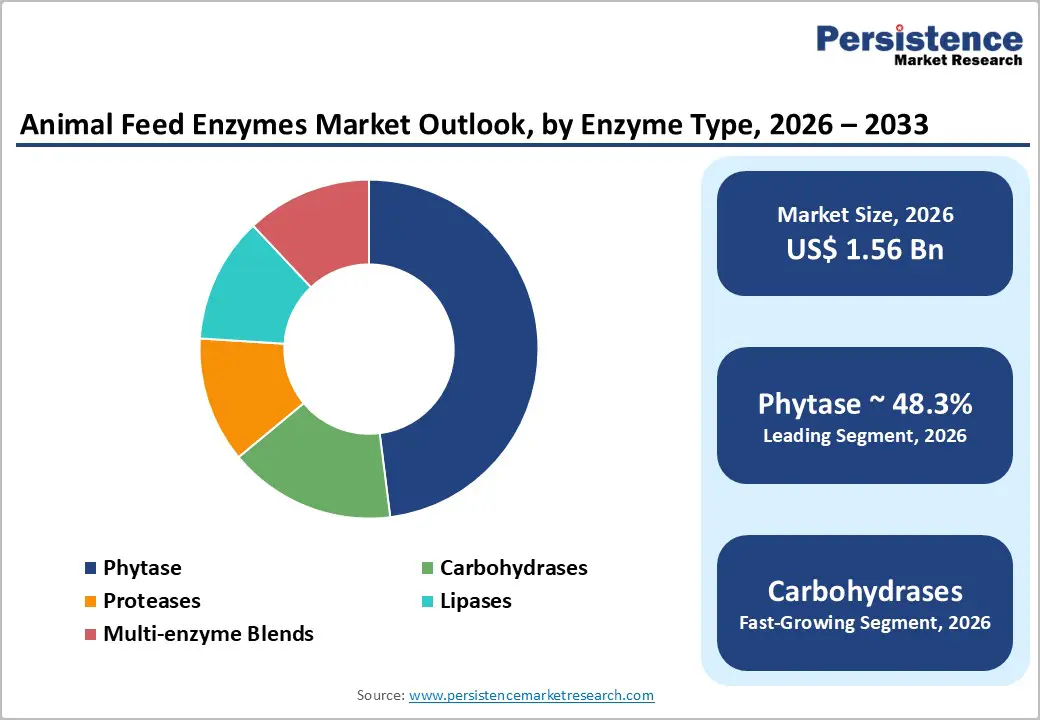

- Dominant Enzyme Type: Phytase, anticipated to hold 48.3% revenue share, remains dominant due to its universal inclusion in poultry and swine diets, measurable phosphorus-release efficiency, reduced inorganic phosphate use, and strong alignment with environmental compliance requirements.

- Leading Animal Type: Poultry is estimated to account for 57.4% of revenue share, the largest end-use segment, driven by tight feed-conversion economics, standardized formulations, vertically integrated production systems, and rapid adoption of high-potency and thermostable enzyme products.

| Key Insights | Details |

|---|---|

| Animal Feed Enzymes Market Size (2026E) | US$1.56 Bn |

| Market Value Forecast (2033F) | US$2.34 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis-Rising Animal Protein Demand and Feed Volumes

Global demand for animal protein, including meat, dairy, and aquaculture products, is projected to increase steadily over the coming decade as population growth and rising incomes drive higher per-capita consumption in developing and middle-income economies. This expansion directly translates into higher compound feed production volumes, strengthening the addressable market for feed enzymes. As feed volumes scale, even marginal improvements in feed conversion ratios deliver significant absolute cost savings. A 1% improvement in feed efficiency can materially reduce total feed expenditure in large commercial operations, making enzyme inclusion economically attractive and accelerating adoption across industrial livestock systems.

Shift Away from Antibiotic Growth Promoters

Regulatory restrictions and voluntary industry initiatives aimed at reducing or eliminating antibiotic growth promoters have reshaped livestock nutrition strategies. Producers are increasingly adopting enzyme-based digestive and gut-health solutions to maintain animal performance under antibiotic-free production models. Enzymes such as phytase, protease, and carbohydrases improve nutrient digestibility, reduce anti-nutritional factors, and enhance gut health outcomes. This transition is particularly pronounced in poultry and swine production, where performance sensitivity and regulatory scrutiny are the highest. As a result, enzyme penetration in commercial feed formulations continues to rise.

Restraints Analysis-Price Sensitivity and Feed-Cost Volatility

Feed enzyme adoption remains sensitive to fluctuations in overall feed-ingredient prices, particularly corn and soybean meal. When raw-material prices decline, procurement decisions often prioritize short-term cost reductions, narrowing the perceived return on enzyme inclusion. In lower-margin production systems, a 1-2% swing in feed costs can significantly alter enzyme payback periods, increasing variability in purchasing behavior and slowing adoption in price-constrained regions.

Regulatory Complexity and Registration Costs

Feed enzymes are subject to additive registration and approval processes across multiple jurisdictions, each with distinct data, testing, and compliance requirements. Lengthy registration timelines and localized trial mandates increase development costs and delay commercialization, particularly for smaller and mid-sized suppliers. These barriers favor established multinational players with regulatory expertise and limit the pace of innovation diffusion in emerging markets, where adoption often lags despite demonstrated technical benefits.

Opportunity Analysis - Next-Generation Enzymes and Precision Blends

Advances in enzyme engineering, including thermostable phytases, tailored proteases for non-traditional feedstocks, and synergistic multi-enzyme blends, present strong opportunities for market expansion. These innovations support higher feed-ingredient flexibility, improved nutrient release, and consistent performance in pelleted and high-temperature feed processes. If next-generation products improve dosing efficacy by 10-20% across even 20% of global feed volumes, incremental market demand could reach tens to low-hundreds of millions of U.S. dollars annually by the end of the decade, depending on adoption rates.

Expansion in Emerging Markets

Rapid growth in poultry, swine, and aquaculture production across the Asia Pacific and Latin America represents the most actionable geographic opportunity. Increasing professionalization of feed mills and greater adoption of premix-based nutrition systems are creating favorable conditions for enzyme penetration. Commercial models that combine competitive pricing with technical support, localized trials, and premix partnerships are particularly effective in converting traditionally low-adoption farms to enzyme-enabled feeding programs.

Category-wise Analysis

Enzyme Type Insights

Phytase is expected to account for 48.3% of revenue share, representing a substantial share of total enzyme consumption during the forecast period. Its dominance is driven by its proven ability to release plant-bound phosphorus (phytate), reduce the need for inorganic phosphorus supplementation, and lower phosphorus excretion in manure. These benefits generate measurable feed-cost savings while supporting compliance with environmental regulations related to phosphorus runoff, making phytase a standard inclusion in commercial poultry and swine diets. Adoption is particularly strong in regions with stringent nutrient-management regulations and high-intensity feed-production systems.

Feed manufacturers increasingly favor high-potency and thermostable phytase formulations, which maintain activity during high-temperature pelleting and allow flexible inclusion across different feed formulations. In large integrated poultry and swine operations, phytase is routinely embedded into baseline premix programs, reinforcing its position as the most commercially established enzyme category.

Carbohydrases and multi-enzyme blends are anticipated to register the fastest growth rate within the enzyme-type segment over the forecast period. Enzymes such as xylanase and beta-glucanase improve the breakdown of non-starch polysaccharides, enhancing energy release and nutrient availability from fiber-rich feed ingredients. This functionality supports greater use of alternative and lower-cost raw materials, including distillers' dried grains with solubles and rapeseed meal. Growth is the strongest in cost-sensitive markets and regions with high variability in feed ingredient quality, where feed formulation flexibility is critical.

Multi-enzyme blends are increasingly adopted to address multiple anti-nutritional factors simultaneously, delivering more consistent performance across diverse diets. Advances in enzyme stabilization, synergistic formulation design, and precision dosing systems at feed mills are accelerating adoption, particularly in the Asia Pacific and Latin America, where compound feed production continues to scale rapidly.

Animal Type Insights

Poultry is expected to remain the leading animal type segment, accounting for 57.4% of revenue. This leadership reflects the sector’s tight feed-conversion economics, high feed input costs, and relatively uniform diet structures dominated by corn and soybean meal. Enzyme inclusion is widely used to reduce feed costs, enhance nutrient digestibility, and support productivity under antibiotic-reduced or antibiotic-free production systems.

Large, vertically integrated poultry producers enable rapid adoption of enzymes through centralized procurement, standardized feed formulations, and rigorous technical validation. Phytase and carbohydrase inclusion is now considered a baseline practice in commercial broiler and layer feeds across major producing regions, reinforcing poultry’s position as the most mature and stable demand segment for feed enzymes.

Aquaculture is expected to be the fastest-growing animal-type segment in terms of enzyme adoption over the forecast period. In aquaculture, the shift toward plant-based feed formulations has increased reliance on enzymes to improve digestibility and reduce nutrient losses into water systems. Enzymes play a critical role in enhancing feed efficiency while supporting environmental sustainability in intensive fish and shrimp farming operations.

Enzymes are increasingly applied to improve fiber degradation, stabilize rumen function, and support milk yield and feed efficiency. Growth across both segments is reinforced by environmental regulations, disease-management priorities, and continued development of enzyme formulations tailored to complex digestive environments.

Regional Insights

North America Animal Feed Enzymes Market Trends - Precision Nutrition and Integrated Production Driving Premium Enzyme Demand

North America represents a mature, innovation-driven animal feed enzyme market, underpinned by highly integrated poultry and swine production systems and advanced feed-mill infrastructure. The U.S. accounts for the majority of regional demand, supported by premium pricing for differentiated enzyme solutions and well-established premix, integrator, and technical-service networks. Major integrators routinely embed phytase and carbohydrases into standardized feed programs, driving stable baseline demand and encouraging adoption of higher-value formulations.

Leading suppliers such as DSM-Firmenich (formerly DSM Animal Nutrition), IFF (Danisco Animal Nutrition), and AB Vista have expanded technical service teams and on-farm validation programs across the U.S. and Canada. These investments support adoption tied to antibiotic-reduction initiatives, precision nutrition strategies, and feed-conversion optimization. In swine and poultry systems, enzyme suppliers increasingly bundle products with digital dosing tools and performance monitoring, reinforcing long-term supplier relationships.

The regulatory environment remains science-based and relatively predictable, allowing efficient commercialization of new enzyme variants, although state-level procurement and labeling requirements can introduce complexity. Investment activity is focused on product innovation, precision dosing systems, application support, and selective acquisitions of niche technology developers, positioning North America as a testing ground for next-generation enzyme solutions before global rollout.

Europe Animal Feed Enzymes Market Trends - Regulatory Pressure Sustaining High-Value Enzyme Utilization

Europe commands a high value per tonne of enzyme consumption, reflecting stringent environmental regulations, advanced feed-mill automation, and widespread adoption of precision nutrition practices. Northern and Western Europe, particularly Germany, the Netherlands, Denmark, and France, lead in per-farm enzyme usage due to strict phosphorus-emission controls and retailer-driven sustainability standards.

Southern and Eastern Europe show faster growth from a smaller base as modern compound feed capacity expands. European feed enzyme adoption has been strongly influenced by regulatory pressure, which has accelerated demand for high-efficacy phytase and multi-enzyme solutions capable of delivering measurable reductions in nutrient excretion. Companies such as Adisseo, AB Vista, and DSM-Firmenich have strengthened their regional footprint by collaborating with European feed mills and livestock research institutes on R&D. These partnerships focus on optimizing enzyme performance within highly automated milling environments and region-specific formulations.

While Europe’s regulatory framework raises entry barriers through rigorous scientific evaluation, it also provides long-term market stability and high customer trust. Opportunities increasingly lie in co-development partnerships, enzyme-process integration, and digital feed-mill optimization, where suppliers align enzyme solutions with energy efficiency, throughput improvement, and sustainability reporting requirements.

Asia Pacific Animal Feed Enzymes Market Trends - Volume-Led Growth Supported by Localization and Cost Efficiency

Asia Pacific is projected to lead the market, holding 41.6% of the market share, driven by large-scale poultry, swine, and aquaculture production alongside rapid industrialization of feed manufacturing. China and India are the primary growth engines, supported by expanding commercial livestock operations and increasing adoption of compound feed.

Southeast Asian markets such as Vietnam, Indonesia, and Thailand benefit from export-oriented poultry and aquaculture industries, where feed efficiency and environmental performance are becoming critical factors in competitiveness. The region has seen significant investment by both global and regional suppliers. Adisseo, which has a strong manufacturing and R&D presence in China, plays a key role in scaling enzyme adoption across domestic feed producers. Global players such as DSM-Firmenich, IFF, and AB Vista have expanded local application labs and technical teams to address diverse feed ingredients and variable raw-material quality. These efforts directly support the use of carbohydrases and enzyme blends tailored to rice bran, wheat, and by-product-heavy diets.

Regulatory environments vary widely across the Asia Pacific, requiring localized registration strategies, joint ventures, and distributor partnerships. Competitive pricing combined with strong technical support remains essential, particularly in emerging markets. Continued industry consolidation, strategic alliances, and localized R&D investment are anticipated as multinational suppliers deepen regional integration and adapt portfolios to high-growth, cost-sensitive production systems.

Competitive Landscape

The global animal feed enzymes market exhibits moderate concentration. A limited number of global suppliers control a substantial share through advanced R&D capabilities, regulatory expertise, and extensive distribution networks, while numerous regional and specialty providers compete in niche applications. Market dominance is the strongest in phytase and core carbohydrase segments, whereas proteases and specialty blends remain more fragmented.

Leading companies prioritize enzyme innovation, regulatory leadership, vertical market access through premix partnerships, and strategic acquisitions. Differentiation increasingly relies on performance validation, integrated technical services, and digital dosing capabilities rather than pricing alone.

Key Industry Developments

- In September 2025, Kemin Industries acquired CJ Youtell Biotech, the enzyme fermentation subsidiary of CJ Bio in China, expanding its global enzyme production capabilities and reinforcing its position in customized enzyme supply for feed, aquaculture, and industrial applications.

- In April 2025, Novus launched CIBENZA® XCEL, a new xylanase feed enzyme additive in India, designed to break down both soluble and insoluble fiber, enhancing energy availability, gut health, and overall feed efficiency in poultry.

Companies Covered in Animal Feed Enzymes Market

- Novonesis

- DSM-Firmenich

- BASF

- Kemin Industries

- Adisseo

- Novus International

- IFF (Danisco Animal Nutrition)

- AB Vista

- Cargill

- Archer-Daniel Midland (ADM)

- Evonik

- Alltech

- AB Enzymes

- Lallemand Animal Nutrition

- Koyo Chemical

- Zhejiang Huakang

- DuPont (Animal Nutrition division)

- Roal Oy

Frequently Asked Questions

The global animal feed enzymes market is estimated to be valued at US$1.56 billion in 2026.

By 2033, the market is projected to reach a value of US$2.34 billion.

Key trends include rising adoption of phytase and carbohydrase enzymes, increased use of thermostable and encapsulated formulations, growing penetration in aquaculture and ruminant nutrition, and a continued shift toward antibiotic-free feed strategies supported by enzyme-based efficiency solutions.

Phytase is the leading enzyme segment, driven by its proven ability to improve phosphorus availability, reduce feed costs, and support environmental compliance in poultry and swine production.

The animal feed enzymes market is projected to grow at a CAGR of 6.2% between 2026 and 2033.

Major players include Novonesis, DSM-Firmenich, BASF, Adisseo, and Kemin Industries.