- Food Ingredients & Additives

- Food Processing Ingredients Market

Food Processing Ingredients Market Size, Share, and Growth Forecast, 2026 - 2033

Food Processing Ingredients Market by Application (Bakery & Confectionary, Dairy Products, Beverages, Cereal Products), End-User (Food Manufacturers, Nutraceutical Manufacturers, Beverage Manufacturers, Foodservice Industry), Source (Natural, Synthetic, Bio-Based), and Regional Analysis for 2026 - 2033

Food Processing Ingredients Market Share and Trends Analysis

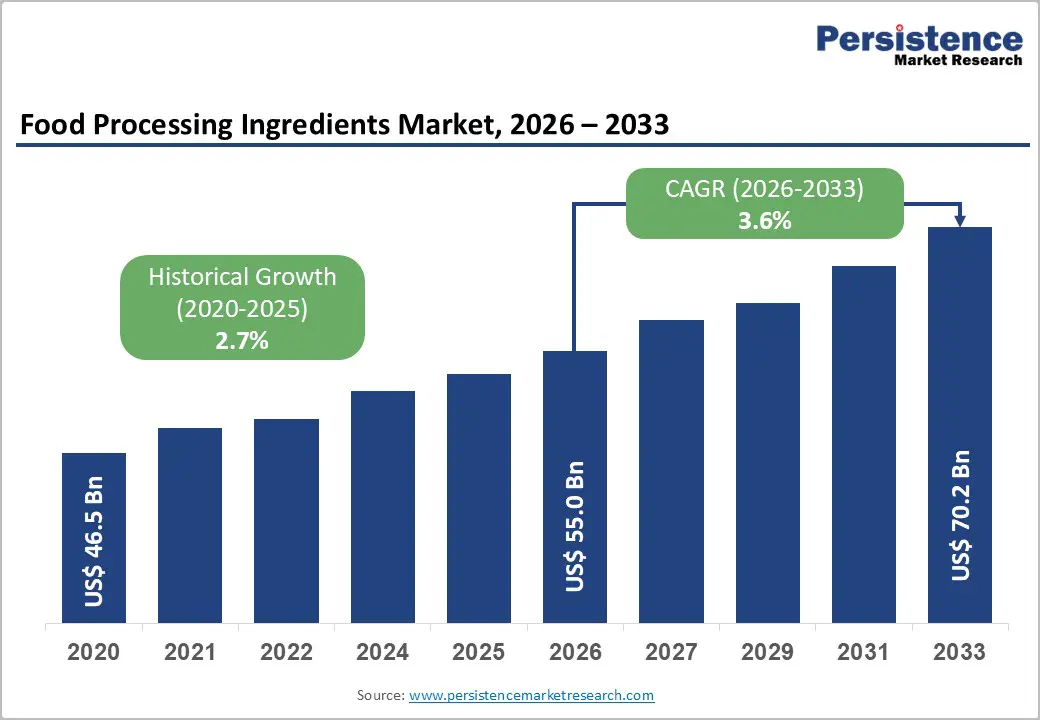

The global food processing ingredients market size is likely to be valued at US$ 55.2 billion in 2026, and is projected to reach US$ 70.2 billion by 2033, growing at a CAGR of 3.6% during the forecast period 2026 - 2033.

This market demonstrates sustained expansion driven by three primary catalysts: the accelerating consumer transition toward convenient, ready-to-consume food products that maintain nutritional integrity; increasingly stringent regulatory frameworks mandating the adoption of natural and clean-label ingredients; and continuous technological innovations that enhance ingredient functionality across diverse food applications. The sector's growth trajectory reflects fundamental shifts in global dietary patterns, particularly the rising preference for processed foods that deliver both convenience and health benefits while meeting evolving food safety standards.

Key Industry Highlights

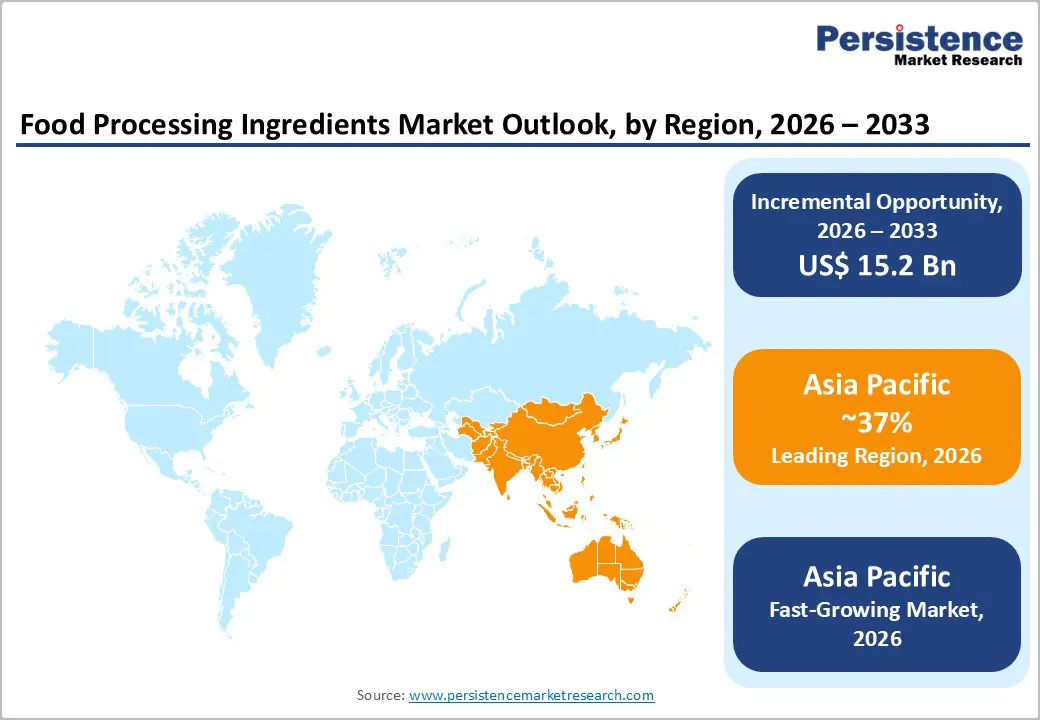

- Dominant & Fastest-growing Market: Asia Pacific is set to be the fastest-growing and leading market with a projected 37% share in 2026, supported by a shift toward packaged foods, frozen meals, beverages, and other convenience formats.

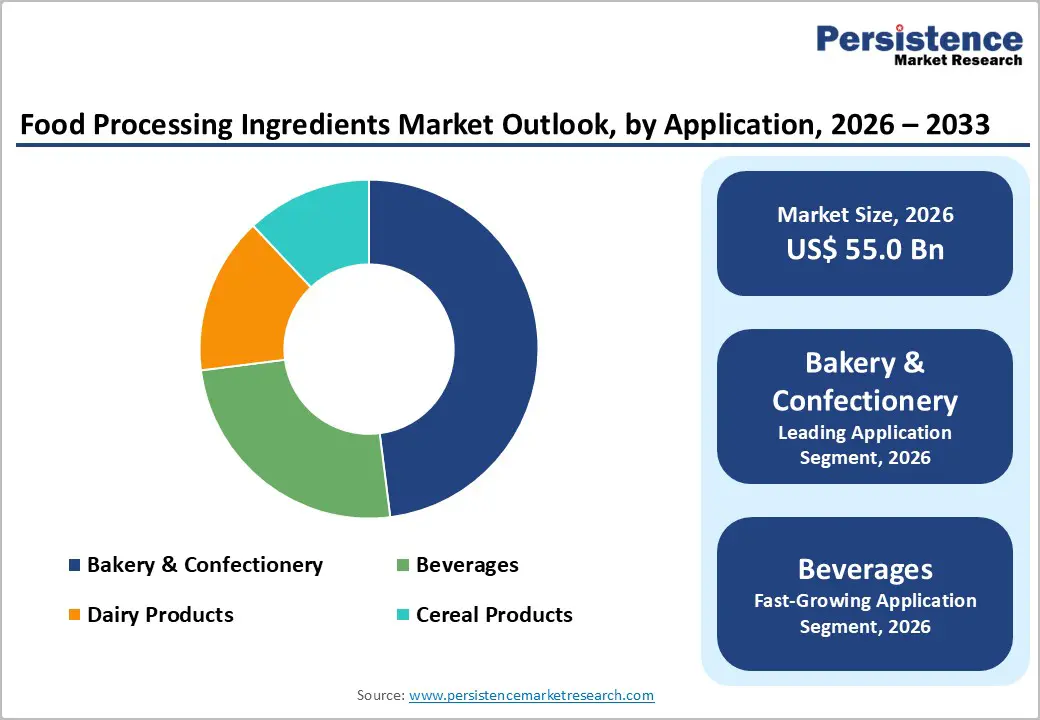

- Leading & Fastest-growing Applications: Bakery and confectionery are slated to dominate with an estimated 2026 share of about 48%, whereas beverages are likely to grow the fastest during the 2026-2033 forecast period.

- Leading & Fastest-growing End-Users: Food manufacturers are expected to lead with around 58% in 2026, while nutraceutical manufacturers are likely to be the fastest-growing from 2026 to 2033.

- Key Developments: The new Non-UPF Verified standard, developed by the Non-GMO Project, bans non-nutritive and bio-transformed sweeteners such as aspartame, sucralose, and saccharin.

| Key Insights | Details |

|---|---|

| Food Processing Ingredients Market Size (2026E) | US$ 55.2 Bn |

| Market Value Forecast (2033F) | US$ 70.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Technological Advancements in Enzymatic and Fermentation Solutions

Technological progress in enzymatic and fermentation solutions is reshaping the food processing ingredients landscape by enabling more precise, efficient, and sustainable production pathways. Food manufacturers are increasingly adopting tailored enzyme systems and fermentation-derived ingredients to enhance texture, flavor development, shelf life, and nutritional value across applications such as bakery, dairy, beverages, and plant-based products. These technologies help companies fine-tune process conditions, reduce reliance on synthetic additives, and create differentiated products that align with clean-label, health-focused, and sustainability-driven positioning. As regulatory authorities such as the European Food Safety Authority (EFSA) refine approval frameworks for new enzyme uses, ingredient suppliers that pair strong scientific validation with robust safety documentation are better positioned to build trust with brand owners and accelerate commercialization.

Biotechnology innovation also enhances strategic flexibility by enabling precision fermentation platforms that produce consistent ingredient quality, regardless of agricultural seasonality or geographic constraints. Companies that invest in integrated bioprocessing capabilities gain advantages in formulation versatility, innovation speed, and the ability to co-develop customized solutions with large food manufacturers. These capabilities support value creation beyond cost optimization, including improved functionality in plant-based proteins, targeted nutrient delivery systems, and next-generation flavor and aroma compounds.

Regulatory Compliance Complexity across Jurisdictions

Navigating diverse regulatory requirements across international markets creates significant operational complexity for ingredient manufacturers that distribute globally. Companies must interpret and comply with distinct safety, labeling, and documentation expectations in each jurisdiction, which places sustained pressure on regulatory affairs, legal, and quality teams. In the United States, processes such as the Generally Recognized as Safe pathway increasingly emphasize robust scientific substantiation, comprehensive dossiers, and transparent communication with authorities. In Europe, evolving guidance from bodies such as the EFSA places greater focus on data completeness, traceability, and structured pre-submission dialogue, which requires early planning and cross-functional coordination.

Regulatory divergence between regions often results in fragmented market access strategies, as ingredients cleared in one geography may still require additional assessment in others, including Asia Pacific and Latin America. Industry associations highlight that smaller and mid-sized enterprises feel these pressures most acutely, as they have fewer internal resources to manage multiple, evolving approval pathways simultaneously. The burden is even higher for biotechnology-derived ingredients, where authorities frequently request detailed safety, allergenicity, and nutritional impact evaluations to reflect emerging scientific understanding.

Functional Food Fortification Addressing Nutritional Gaps

Functional food fortification is emerging as a strategic pillar for closing nutritional gaps and strengthening the value proposition of processed foods. By incorporating ingredients such as vitamins, minerals, probiotics, prebiotics, and other bioactive compounds, manufacturers can position products to support specific health outcomes, including digestive wellness, cognitive function, and immune resilience. This approach aligns with growing consumer interest in foods that provide meaningful health benefits as part of everyday diets rather than relying solely on supplements. For ingredient suppliers, fortification platforms create opportunities to deliver integrated solutions that combine efficacy, stability, sensory performance, and clean-label compatibility, which are critical for both brand owners and regulators.

Leading companies treat functional fortification as a cross-functional initiative that links research and development, regulatory affairs, marketing, and supply chain planning. They prioritize scientifically substantiated ingredients, invest in clinical or observational evidence where appropriate, and design fortification systems that perform consistently across different processing conditions and product formats. In parallel, they closely track evolving health-claim regulations in major markets, such as guidance from the United States Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA), to ensure that on-pack messaging remains compliant while still resonating with health-conscious consumers.

Category-wise Analysis

Application Insights

Bakery and confectionery are slated to occupy the apex position in 2026, holding approximately 48% of the food processing ingredients market revenue share. This segment's dominance reflects the essential role of starches, emulsifiers, enzymes, and texturizers in delivering dough stability, optimized texture, extended shelf life, and strong sensory appeal. The bakery category benefits from both established consumption habits and continuous innovation in artisanal, health-oriented, and indulgent products that require specialized solutions for gluten-free, protein-fortified, and reduced-sugar formulations.

Beverages is likely to be the fastest-growing segment during the 2026 - 2033 forecast period. The beverage industry represents a core demand center for food processing ingredients, spanning categories such as carbonated soft drinks, juices, alcoholic beverages, and dairy-based or plant-based drinks. Formulators rely on a combination of sweeteners, acidulants, stabilizers, and flavor systems to achieve consistent taste profiles, visual appeal, and product stability throughout shelf life. Growing interest in functional beverages is reshaping ingredient requirements, as products positioned for energy, hydration, digestive wellness, or immunity increasingly incorporate vitamins, minerals, botanicals, and fermentation-derived components.

End-User Insights

Food manufacturers are poised to hold the highest revenue share, estimated to reach 58% in 2026. This segment spans large industrial processors, mid-sized regional producers, and specialized manufacturers that focus on niche categories, reflecting the diversity of global processed food production. Its overall scale aligns with a wide spectrum of products, including packaged foods, frozen meals, beverages, and snacks, all of which rely on varied ingredient portfolios to support formulation performance, processing efficiency, and consistent quality standards. Across this segment, food manufacturers increasingly seek ingredient partners that offer deep technical expertise, proactive regulatory guidance, robust and resilient supply capabilities, and collaborative innovation support to respond effectively to shifting consumer expectations and intensifying competitive dynamics.

Nutraceutical manufacturers is expected to post the highest CAGR between 2026 and 2033. This end-user group produces functional foods, dietary supplements, fortified beverages, and health-oriented products requiring specialized ingredients including probiotics, plant-based proteins, vitamins, minerals, and bioactive compounds with documented efficacy. Regulatory developments enabling qualified health claims and the mainstreaming of personalized nutrition are creating expanded opportunities for ingredient suppliers capable of delivering scientifically validated functional ingredients meeting stringent purity, potency, and stability specifications required for health-focused applications.

Source Insights

At roughly 61%, the natural segment is slated to lead the food processing ingredients market share in 2026. Growing awareness of the health and environmental benefits of natural ingredients is accelerating their adoption across a wide spectrum of food categories. Consumers are increasingly cautious about artificial additives and prefer products formulated with components sourced from plants, animals, and minerals that they perceive as familiar and minimally processed. This shift is encouraging manufacturers to reformulate legacy portfolios, develop clean-label product lines, and invest in more transparent communication about ingredient origin and processing. In parallel, it is pushing companies to strengthen sustainable sourcing, traceability, and responsible production practices to align with retailer expectations and corporate environmental, social, and governance (ESG) commitments.

The bio-based segment is anticipated to be the fastest-growing segment during the 2026 - 2033 forecast period. The growth is propelled by precision fermentation and biotechnology innovations enabling sustainable production of proteins, flavors, vitamins, and functional compounds from microbial or plant sources. Bio-based ingredients deliver equivalent or superior functional performance while meeting ESG criteria increasingly mandated by corporate procurement policies and consumer expectations for sustainable food systems. The segment's growth is further accelerated by technological advancements reducing production costs, with fermentation-derived ingredients approaching cost parity with conventional alternatives, enabling mainstream commercial adoption across food and beverage applications.

Regional Insights

Asia Pacific Food Processing Ingredients Market Trends

Asia Pacific market is the fastest-growing and leading with a projected 37% of market share in 2026. The region’s expansion reflects a structural shift toward greater consumption of packaged foods, frozen meals, beverages, and other convenience formats, as consumers in markets such as China, India, and the ASEAN move away from traditional home-prepared diets and toward modern retail and foodservice channels. Within this landscape, China anchors regional demand with its large consumer base and established manufacturing ecosystem, Japan drives value through premium, quality-focused innovation, and India contributes strong momentum through a rapidly modernizing food processing sector and the ongoing formalization of retail.

ASEAN economies such as Indonesia, Thailand, and Vietnam are also emerging as important growth hubs, supported by rising incomes, urban migration, and continued investment in cold chain and processing infrastructure that is transforming local food systems. The region’s appeal is reinforced by competitive manufacturing economics and progressive regulatory evolution that collectively support long-term ecosystem development. Proximity to agricultural raw materials, including crops used for starches, plant-based proteins, and natural colors, enables cost-effective sourcing and supports the growth of both volume and value-added ingredient categories. China’s ongoing food safety reforms, Japan’s mature quality frameworks, India’s strengthening role through the Food Safety and Standards Authority of India (FSSAI), and gradual regulatory harmonization within ASEAN are all raising the baseline for compliance while improving investor confidence.

Europe Food Processing Ingredients Market Trends

Europe has emerged as a pivotal hub for food processing ingredients, combining substantial market scale with strong regulatory influence and clear leadership in sustainable innovation. The region’s growth rests on highly discerning consumers who actively seek sustainable, clean-label, and nutritionally differentiated products, leading manufacturers to prioritize ingredients that deliver both functional performance and credible environmental credentials. Within Europe, markets such as Germany, the United Kingdom, France, and Spain play distinct roles, from technology-driven ingredient development to deep-rooted culinary traditions that increasingly incorporate healthier, reformulated product lines. For suppliers, success in this environment requires not only competitive pricing but also the ability to align with premium positioning, stringent quality standards, and retailer expectations around traceability and transparency.

The regulatory landscape further amplifies Europe’s strategic importance, as frameworks guided by the EFSA often set benchmarks that influence global ingredient approval and food safety practices. Rigorous assessment of novel foods and additives encourages companies to build robust scientific dossiers, which in turn strengthens the credibility and exportability of European-compliant ingredients. At the same time, policy agendas such as the European Green Deal are accelerating demand for solutions that support carbon reduction, circular economy models, and responsible sourcing across agricultural and processing value chains.

North America Food Processing Ingredients Market Trends

North America has established as a mature yet strongly innovation-driven hub for food processing ingredients, combining large-scale manufacturing capacity with sophisticated demand for advanced, value-added solutions. Regional growth rests on well-developed food manufacturing infrastructure, high per-capita food spending, and a regulatory environment that supports science-based innovation while still maintaining strict safety standards. The United States serves as the primary engine of demand, as consumers show strong preferences for clean-label, natural, and organic products, which encourages food manufacturers to reformulate portfolios and adopt ingredients that enhance transparency, support health-focused positioning, and improve on-shelf differentiation.

The competitive and regulatory context further strengthens the region’s strategic importance for long-term growth planning. The presence of large multinational ingredient companies, together with a dynamic ecosystem of specialty and start-up players, creates an environment where customers expect not only reliable supply but also deep technical support, co-development capabilities, and evidence-backed performance claims. Modernized approval processes overseen by regulators such as the USFDA, including mechanisms such as the Generally Recognized as Safe (GRAS) pathway, provide a clear and science-driven route for bringing new ingredients to market, particularly in categories such as enzymes, probiotics, plant-based proteins, and bio-fermented compounds.

Competitive Landscape

The global food processing ingredients market structure is moderately consolidated, dominated by leading players such as Cargill, Incorporated, Archer Daniels Midland Company, DuPont de Nemours, Inc., Kerry Group plc and Ingredion Incorporated. These players collectively capture 35-42% of market share. The competitive landscape in the food processing ingredients market is defined by a concentrated group of global leaders operating alongside a wide range of regional and niche specialists. Companies are competing aggressively by expanding their product portfolios, entering new geographic markets, and using strategic partnerships, joint ventures, and acquisitions to strengthen capabilities and customer access.

Rising demand for natural, clean-label, and functional ingredients is pushing manufacturers to increase investment in research and development so they can deliver more differentiated, value-added solutions tailored to specific applications and health-positioned products. At the same time, tightening regulatory expectations, coupled with growing scrutiny around transparency, sustainability, and responsible sourcing, are reshaping competitive priorities and rewarding players that can combine innovation depth with robust compliance and ESG-focused supply chain practices.

Key Industry Developments

- In November 2025, Al Ghurair Foods launched its first industrial food ingredients portfolio at Gulfood Manufacturing 2025, marking a shift from commodity trading to value-added B2B ingredient supply for manufacturers in bakery, confectionery, beverage, and baby food sectors.

- In October 2025, major food companies, including Coca-Cola, Kraft Heinz, General Mills, and Nestlé, formed Americans for Ingredient Transparency to lobby against state laws targeting artificial dyes and ultraprocessed foods amid U.S. Health Secretary Robert F. Kennedy's "Make America Healthy Again" (MAHA) push.

- In May 2025, KMC partnered with UK-based distributor Daymer Ingredients to accelerate the rollout of clean-label and specialized potato starch solutions for British food manufacturers, initially focusing on native potato starch and later expanding to modified starches.

Companies Covered in Food Processing Ingredients Market

- Cargill, Incorporated

- Archer Daniels Midland Company

- DuPont de Nemours, Inc.

- Kerry Group plc

- Ingredion Incorporated

- Koninklijke DSM N.V.

- Tate & Lyle PLC

- Corbion N.V.

- Givaudan SA

- International Flavors & Fragrances Inc.

- Ashland Global Holdings Inc.

- CHR. Hansen A/S

- Sensient Technologies Corporation

- Ajinomoto Co., Inc.

- BASF SE

Frequently Asked Questions

The global food processing ingredients market is projected to reach US$ 55.2 billion in 2026.

The market is driven by rising global demand for processed and convenience foods, health- and wellness-oriented products, and clean-label, sustainable formulations.

The market is poised to witness a CAGR of 12.5% from 2026 to 2033.

Plant-based and functional ingredients, clean-label and natural additives, and emerging-market processed food penetration and processing solutions are opening attractive opportunities.

Cargill, Incorporated, Archer Daniels Midland Company, DuPont de Nemours, Inc., Kerry Group plc and Ingredion Incorporated. are some of the key players in the market.