- Nutraceuticals & Functional Foods

- Wheat Fiber Market

Wheat Fiber Market Size, Share, and Growth Forecast 2026 - 2033

Wheat Fiber Market by Wheat Fiber Type (Soluble Wheat Fiber, Insoluble Wheat Fiber), by Nature (Conventional, Organic), by Application (Food & Beverages, Pharmaceuticals / Nutraceuticals, Animal Feed, Personal Care, Others), and Regional Analysis, 2026 - 2033

Wheat Fiber Market Share and Trends Analysis

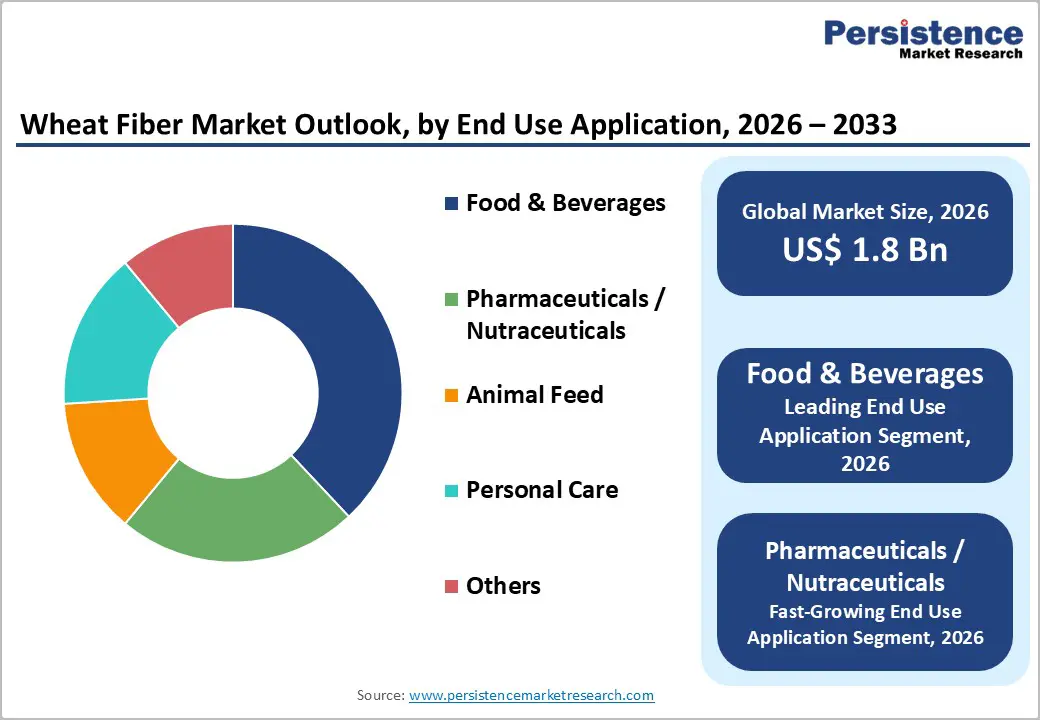

The global wheat fiber market size is expected to be valued at US$ 1.8 billion in 2026 and projected to reach US$ 2.5 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033.

This steady expansion is driven by rising consumer demand for functional foods enriched with dietary fiber, coupled with growing awareness of wheat fiber’s health benefits for digestive wellness and chronic disease prevention. Authoritative nutrition bodies highlight that whole wheat provides around 11 grams of dietary fiber per 100 grams, positioning wheat fiber as a premium natural ingredient for fortification across bakery, nutraceutical, and functional beverage applications. The clean-label movement, emphasizing natural and recognizable ingredients over artificial additives, further amplifies market adoption as consumers prioritize transparency in food sourcing and manufacturing processes.

Key Industry Highlights:

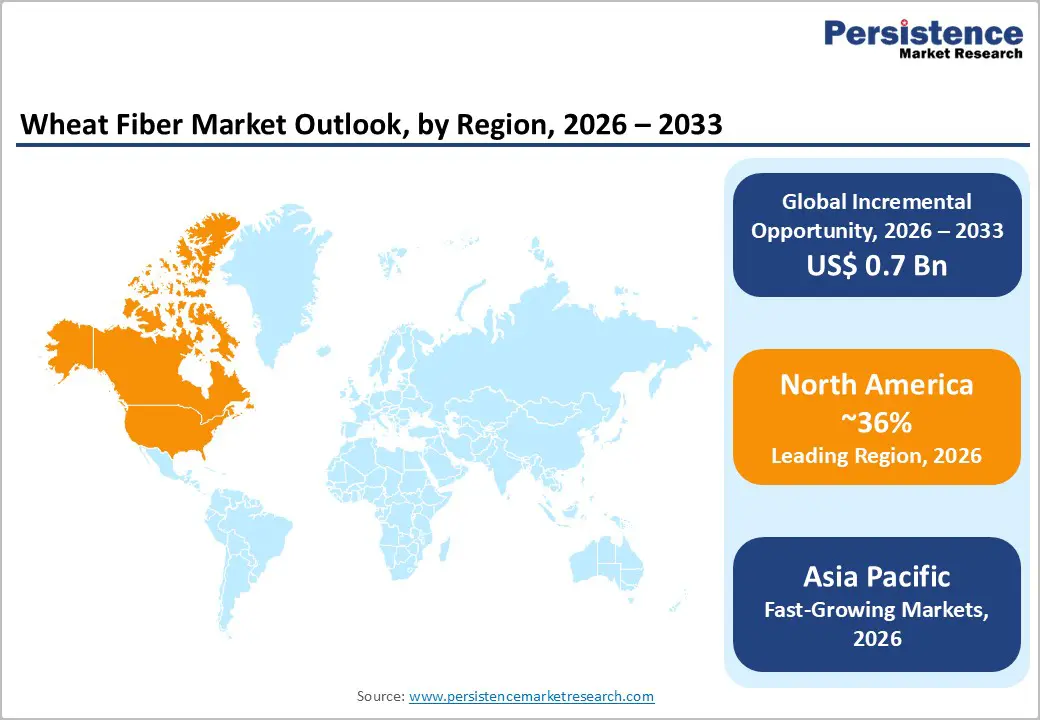

- North America is the leading region in the wheat fiber market, with about 36% share in 2025, supported by strong regulatory backing for fiber and whole-grain claims, a sophisticated food processing ecosystem, and high consumer awareness of digestive and cardiovascular health benefits that encourage adoption of fiber-fortified products.

- Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR above 5% between 2025 and 2032, driven by large-scale wheat production in China and India, rapid growth in processed foods and bakery consumption, and increasing focus on lifestyle disease prevention through improved dietary patterns.

- Insoluble wheat fiber is the dominant product type, accounting for around 62% of market share in 2025, due to its robust functional performance in bakery and cereal applications, superior water-binding and texturizing properties, and well-established role in promoting digestive regularity and bowel health.

- Key market opportunities lie in expanding high-value applications in nutraceuticals and functional foods, and in leveraging Asia Pacific’s manufacturing advantages and rising health awareness, enabling wheat fiber producers to build scale, capture premium pricing in organic and specialty segments, and embed their solutions into long-term reformulation roadmaps of global food and beverage brands.

| Key Insights | Details |

|---|---|

| Wheat Fiber Market Size (2026E) | US$ 1.8 Bn |

| Market Value Forecast (2033F) | US$ 2.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Dynamics

Drivers - Rising Health Consciousness Driving Functional Food Fortification

Rising global health consciousness is a primary driver for wheat fiber demand as consumers increasingly associate higher fiber intake with improved digestive health and long-term disease prevention. Large-scale epidemiological studies supported by organizations such as NIH show that higher dietary fiber intake is correlated with reduced risk of coronary heart disease, stroke, type 2 diabetes, and obesity. Wheat fiber, containing both soluble and insoluble fractions, supports bowel regularity, enhances satiety, and contributes to better glycemic control, especially important in markets with a high prevalence of diabetes. Clinical and regulatory guidance frequently recommends about 14 grams of dietary fiber per 1,000 kilocalories of intake, a threshold that several populations still fail to meet, creating a clear gap for fortified products. Food manufacturers leverage wheat fiber to enrich bread, cereals, snacks, and dairy analogues, with fortification levels often increasing fiber content in finished products by 20-30% while maintaining sensory acceptance, directly aligning with consumer intent to “get more fiber” from everyday foods.

Clean Label and Natural Ingredient Trends Accelerating Adoption

Clean-label, minimally processed foods are now a mainstream expectation, especially in developed markets, and this trend substantially favors wheat fiber as a recognizable, plant-based ingredient. Consumer surveys in Europe and North America indicate that more than 60% of shoppers consistently read ingredient lists, and a significant share prefers short, familiar ingredient panels. Regulatory strategies, such as the European Commission's Farm to Fork Strategy and front-of-pack labelling initiatives, encourage manufacturers to improve nutritional quality, including fiber enrichment. Wheat fiber functions as a natural texturizer, water binder, and bulking agent, allowing it to replace or reduce synthetic stabilizers and modified celluloses in bakery and processed foods. In leading EU markets, clean-label and fiber-enriched claims appear on well over 25% of new product launches in relevant categories, with many products using cereal-derived fibers. This synergy between clean-label positioning and nutritional enhancement increasingly differentiates brands, embedding wheat fiber in reformulation pipelines for bakery, snacks, ready meals, and plant-based alternatives.

Restraints - Wheat Price Volatility and Agricultural Supply Risks

One of the major restraints for the wheat fiber market is exposure to wheat price volatility and agricultural risks, which can squeeze margins and complicate long-term contracting. Wheat prices are sensitive to climatic events such as droughts and floods, geopolitical disruptions in key exporting regions, and changes in subsidy and trade policies. For example, output fluctuations in major producers like China, India, and countries in the Black Sea region can move global prices by several percentage points in a single season. Such volatility directly impacts fiber processors who rely on stable raw material flows, making cost forecasting and pricing for long-term supply agreements more challenging. Climate change models also anticipate greater yield variability, raising structural concerns about the resilience of wheat-dependent ingredient chains. To manage this, manufacturers must diversify sourcing regions, invest in storage and logistics, and sometimes consider blending with other cereal fibers, all of which add complexity and operational cost that can temper market expansion.

Competitive Pressure from Alternative Dietary Fiber Sources

Wheat fiber competes in a crowded dietary fiber landscape that includes oat fiber, inulin from chicory root, psyllium, citrus fiber, and resistant starches, many of which have strong clinical evidence and specific health-positioning advantages. Clinical reviews, including those from gastroenterology associations, have shown that psyllium, for example, can outperform traditional wheat bran in certain indications of chronic constipation, influencing healthcare professionals’ recommendations and product formulation choices. In the weight management and prebiotic segments, inulin and fructooligosaccharides often receive attention for their documented effects on gut microbiota and satiety. Additionally, gluten-related concerns, even among non-celiac consumers, are driving some brands to avoid wheat-derived ingredients entirely in their gluten-free or “free-from” product ranges, creating structural demand for alternative fibers. As a result, wheat fiber suppliers must work harder to clearly communicate functional benefits, cost competitiveness, and versatile application performance, or risk losing share in high-value applications to these alternative, often more strongly clinically branded, fiber types.

Opportunity - Expanding Pharmaceutical and Nutraceutical Use in Digestive and Metabolic Health

The pharmaceuticals and nutraceuticals space offers one of the most compelling opportunity areas for wheat fiber, as demand grows for clinically supported, fiber-based solutions for digestive and metabolic health. Evidence-based reviews show that increased fiber intake is associated with better weight management, lower LDL cholesterol, improved glycemic control, and mitigation of constipation, all of which are key indications targeted by supplements. Nutraceutical formulators are increasingly using cereal fibers in combination with probiotics, herbal extracts, and bioactive compounds to deliver synergistic gut-health solutions. In global functional food and nutraceutical markets, which collectively already exceed US$ 300 billion and are projected to grow at mid-single- to high-single-digit CAGR through the next decade, fibers are considered core enabling ingredients. Wheat fiber can be granulated, milled, or agglomerated for inclusion in tablets, capsules, stick packs, and powdered drink mixes. Companies that offer highly standardized, low-dust, neutral-taste wheat fiber grades with documented technical and stability data are well-positioned to secure long-term contracts with supplement brands and pharmaceutical firms seeking scalable, plant-based excipients and actives that align with the broader “food as medicine” trend.

Category-wise Analysis

Wheat Fiber Type Insights

Insoluble wheat fiber currently leads the market and is also the fastest-growing segment, accounting for an estimated 62% share in 2025 and expected to grow at around 4.8% CAGR between 2025 and 2032. Its dominance is linked to superior functional performance in bakery and cereal applications, where insoluble particles help build structure, improve crumb, and enhance water-holding capacity without significantly affecting taste. Technical dossiers submitted to regulators show that wheat-derived insoluble fibers can be incorporated at levels above 10 grams per 100 grams in certain baked products while maintaining acceptable sensory profiles. From a nutrition perspective, insoluble fiber’s ability to increase stool bulk and speed intestinal transit is widely recognized, supporting its use in products marketed for digestive regularity. Large bakeries and cereal manufacturers value wheat fiber for being label-friendly, cost-effective, and compatible with existing processing lines. As manufacturers reformulate to meet front-of-pack fiber claims or minimum grams-per-serving thresholds, insoluble wheat fiber often becomes the default choice, especially in markets where wheat is already the dominant grain in consumer diets.

Nature Insights

Conventional wheat fiber holds the majority share, at approximately 71% of the market in 2025, reflecting its long-established supply chains, broader availability, and more competitive pricing compared to organic variants. Conventional production benefits from large-scale wheat cultivation using modern inputs, allowing processors to secure consistent volumes and qualities suitable for industrial food and feed applications. Organic wheat flour markets, which share upstream supply with organic wheat fiber, are already valued in the hundreds of billions of US dollars globally and continue to expand as household penetration rises. Certified organic wheat fiber is particularly attractive to premium brands and retailers that require every ingredient in a product to meet USDA Organic, EU Organic, or equivalent regional standards, making this niche an important strategic focus for ingredient suppliers seeking higher-margin opportunities.

Application Insights

Food & Beverages is the leading application segment, accounting for about 38% of the wheat fiber market in 2025, as manufacturers increasingly deploy wheat fiber to fortify everyday products such as bread, rolls, tortillas, breakfast cereals, nutrition bars, meat analogues, and dairy alternatives. Its compatibility with existing flour-based recipes and low impact on flavor make wheat fiber a practical choice for incremental reformulation, especially where brand owners want to achieve relatable front-of-pack statements like “source of fiber” or “high in fiber.” Beyond basic bakery, fiber-enriched beverages, smoothies, and spoonable dairy snacks are also beginning to incorporate finely milled wheat fiber fractions to boost fiber content without excessive viscosity or grittiness.

Regional Insights

North America Wheat Fiber Market Trends and Insights

North America is the leading regional market, with an estimated 36% share in 2025, underpinned by the United States’ advanced food processing industry and strong regulatory framework around fiber and whole grain claims. The USDA and FDA both promote higher fiber intake as part of dietary guidelines, and the FDA allows health claims linking certain whole grain and fiber-containing foods with reduced risk of heart disease and some cancers, provided products meet specific composition criteria. This regulatory support encourages brands to invest in fiber-enriched formulations that can legitimately carry impactful, science-based claims on pack.

The region is also home to several of the largest grain and ingredient companies globally, which operate extensive R&D centers and pilot plants dedicated to cereal innovation. These companies are continually developing new wheat fiber grades with improved dispersibility, neutral flavor, and tailored particle size distributions that enhance performance in targeted applications ranging from high-fiber breads to low-sugar, high-protein nutrition bars. Consumer interest in digestive health and “gut-friendly” foods has surged, with survey data showing a significant proportion of US consumers actively seeking more fiber and probiotics in their diets. This aligns well with wheat fiber’s value proposition, and North America is expected to remain a key demand center and innovation hub through the forecast period, particularly in the overlapping areas of sports nutrition, weight management, and healthy snacking.

Asia Pacific Wheat Fiber Market Trends and Insights

Asia Pacific is emerging as a high-growth region in the wheat fiber market, driven by rapid urbanization, rising disposable incomes, and increasing awareness of digestive health. Countries such as China, India, Japan, and Australia are witnessing growing demand for fiber-enriched bakery products, functional beverages, breakfast cereals, and dietary supplements. The expanding middle-class population and shifting dietary patterns toward healthier and fortified foods are significantly supporting market expansion. Additionally, government initiatives promoting balanced nutrition and preventive healthcare are encouraging food manufacturers to incorporate wheat fiber into mainstream products. The region’s strong wheat production base and improving food processing infrastructure also enhance local manufacturing capabilities and reduce dependency on imports. Growth in e-commerce and organized retail channels further supports product accessibility and consumer awareness. Moreover, rising cases of lifestyle-related disorders such as obesity and digestive issues are driving demand for nutraceutical applications. Overall, the Asia Pacific is positioned as one of the fastest-growing and strategically important markets for wheat fiber globally.

Competitive Landscape

The competitive landscape of the wheat fiber market is marked by intense rivalry as manufacturers focus on product innovation, quality enhancement, and expanded distribution networks to capture a larger market share. Companies are investing in research and development to introduce customized fiber solutions addressing specific functional and nutritional needs across industries. Strategic partnerships, mergers, and acquisitions are increasingly employed to strengthen global presence and streamline supply chains. Additionally, emphasis on organic and clean-label offerings is driving differentiation. Competitive pressure also comes from alternative dietary fiber sources, prompting firms to optimize cost structures and improve value propositions to maintain an edge.

Key Developments:

- In March 2025, Allied Pinnacle and Woolworths developed and launched a new high-fibre wheat ingredient brand called Wise Wheat, the result of over 20 years of research and breeding, which produced wheat with about six times the fibre of regular flour. The ingredient was introduced in a range of white and seeded bread loaves and rolls sold through Woolworths supermarkets’ in-store bakeries in Australia, aimed at helping consumers increase daily fibre intake without sacrificing taste or texture.

Companies Covered in Wheat Fiber Market

- Cargill, Incorporated

- Archer Daniels Midland Company (ADM)

- Tate & Lyle PLC

- Roquette Frères S.A.

- Ingredion Incorporated

- J. Rettenmaier & Söhne GmbH + Co KG

- Grain Processing Corporation

- SunOpta Inc.

- BENEO GmbH

- Südzucker AG

- InterFiber Sp. z o.o.

- JELU-WERK J. Ehrler GmbH & Co. KG

Frequently Asked Questions

The global wheat fiber market is projected to reach about US$ 1.8 billion in 2026, reflecting increased adoption of fiber-fortified foods and growing awareness of the role of dietary fiber in digestive, metabolic, and cardiovascular health across major consumer markets.

Key demand drivers include rising consumer health consciousness, the desire to close the dietary fiber intake gap, strong regulatory and guideline support for fiber-rich diets, and the clean-label trend encouraging replacement of synthetic ingredients with natural, cereal-derived fibers in bakery, snacks, beverages, and plant-based products.

North America is the leading region, holding roughly 36% share in 2025, supported by the United States’ advanced food manufacturing base, a supportive regulatory framework for fiber and whole-grain claims, and widespread consumer recognition of the benefits of fiber-enriched foods and supplements.

A key opportunity lies in expanding the use of wheat fiber in pharmaceuticals and nutraceuticals, where clinically backed digestive and metabolic health benefits can be leveraged in supplements, functional foods, and beverages, as well as in capturing fast-growing demand in the Asia Pacific through localized production and tailored, high-fiber formulations for bakery, noodles, and snacks.

Major players include Cargill, Incorporated, Archer Daniels Midland Company (ADM), Tate & Lyle PLC, Roquette Frères S.A., Ingredion Incorporated, J. Rettenmaier & Söhne GmbH + Co KG, BENEO GmbH, Südzucker AG, SunOpta Inc., InterFiber Sp. z o.o., and JELU-WERK J. Ehrler GmbH & Co. KG, alongside other regional and specialty fiber producers.