- Beverages

- U.S. Energy Drinks Market

U.S. Energy Drinks Market Size, Share, and Growth Forecast, 2026 - 2033

U.S. Energy Drinks Market by Product Type (Caffeinated, De-caffeinated), Packaging (Bottles, Cans, Pouches, Tetra Packs, Others), Sales Channel (Online Channel, Offline Channel), and Regional Analysis for 2026 - 2033

U.S. Energy Drinks Market Share and Trends Analysis

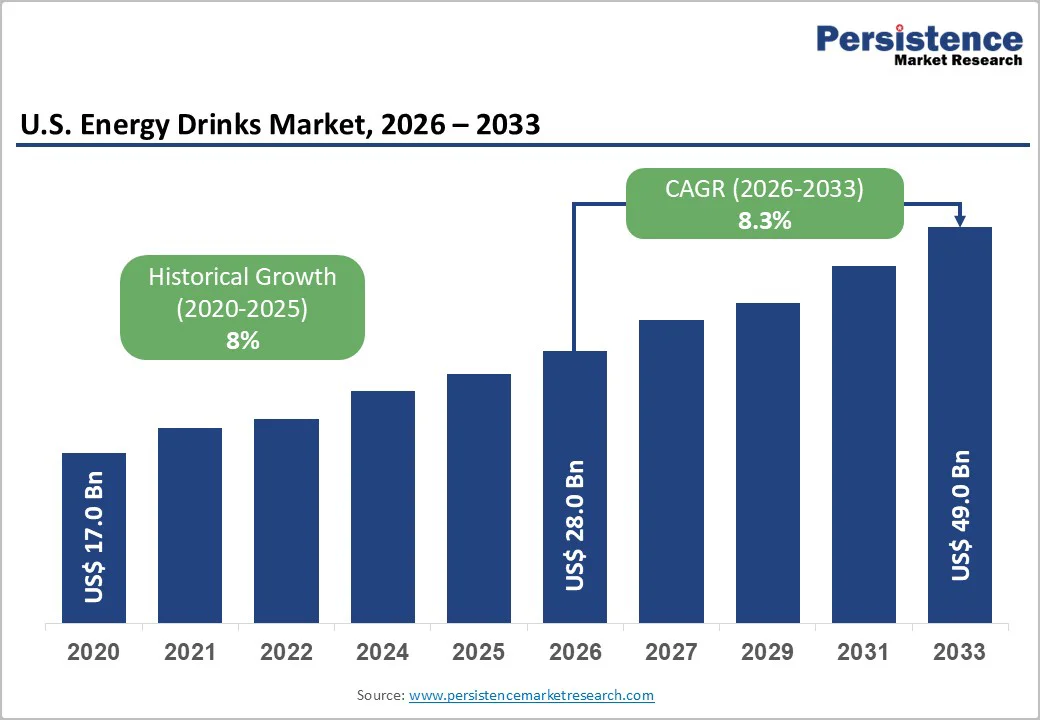

The U.S. energy drinks market size is likely to be valued at US$ 28.0 billion in 2026 and is projected to reach US$ 49.0 billion by 2033, growing at a CAGR of 8.3% during the forecast period 2026 - 2033.

Shifting consumer preferences toward functional beverages drive this expansion. Millennials and Gen Z lead adoption, seeking performance support for academic, professional, and fitness goals. Their demand for products that enhance mental alertness and physical endurance reshapes category expectations. This creates sustained revenue opportunities for manufacturers who align with these preferences.

Product innovation accelerates market momentum, with manufacturers prioritizing natural ingredients and reduced sugar content to align with health-conscious trends. Brands are reformulating with plant-based caffeine sources, botanical extracts, and clean-label sweeteners to differentiate offerings.

Targeted marketing campaigns aim to amplify reach among specific segments, such as fitness enthusiasts, e-sports participants, and professionals managing intensive workloads.

Key Industry Highlights

- Leading & Fastest-growing Product Types: Caffeinated beverages are likely to command approximately 76.5% market share in 2026, while decaffeinated drinks are set to post the highest CAGR during the 2026 - 2033 forecast period.

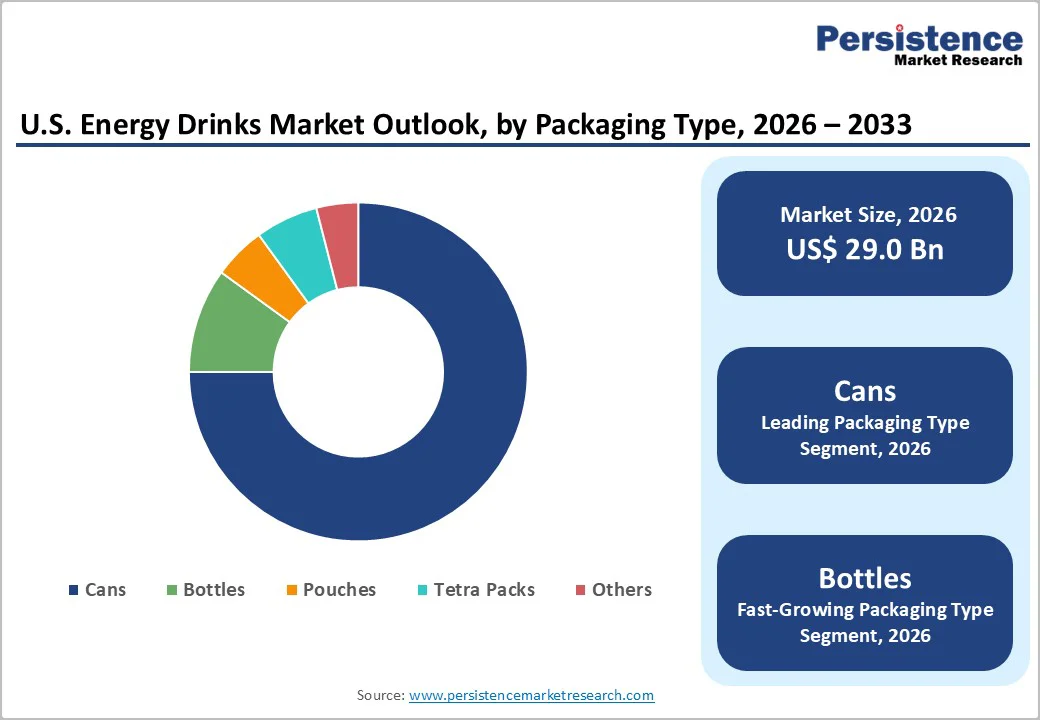

- Dominant & Fastest-growing Packaging Types: Cans are projected to dominate, accounting for approximately 92.5% of market revenue share in 2026, whereas bottles are expected to be the fastest-growing segment between 2026 and 2033.

- Leading & Fastest-growing Sales Channels: The offline channel is poised to capture around 84.5% of revenue share in 2026, while the online channel is expected to grow the fastest through 2033.

- December 2025: Unwell Energy by Alex Cooper launched exclusively at Target with four low-sugar caffeine drinks, featuring real juice, electrolytes, and B vitamins without artificial sweeteners.

| Key Insights | Details |

|---|---|

| U.S. Energy Drinks Market Size (2026E) | US$ 28.0 Bn |

| Market Value Forecast (2033F) | US$ 49.0 bn |

| Projected Growth (CAGR 2026 to 2033) | 8.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Health Consciousness and Functional Beverage Demand

The growing consumer preference for functional beverages is a key driver of growth in the U.S. energy drinks market. Energy drink consumption has become embedded in the daily routines of young adults and working professionals in the country, indicating that these products are now viewed as everyday performance enhancers rather than occasional novelty items.

This shift in behavior reflects broader lifestyle changes, as more consumers seek convenient solutions to support energy, focus, and endurance across work, study, and leisure activities.

Manufacturers are responding by launching products with enhanced nutritional profiles that incorporate vitamins, electrolytes, and natural caffeine sources to appeal to wellness-oriented consumers. This approach aligns with broader dietary shifts toward clean-label and minimally processed products, supporting innovation in organic and naturally formulated energy beverages.

For example, Bubbl’r and Amez Infusions are capitalizing on rising demand for low-sugar, low-caffeine functional energy drinks that deliver sustained focus without jitters, targeting Gen Z and millennials with clean-label teas and sparkling waters. As a result, brands that can credibly combine performance benefits with cleaner ingredient profiles are well-positioned to capture emerging demand and strengthen their market differentiation.

Health Concerns and Regulatory Scrutiny

Energy drinks face increasing criticism for their high caffeine and sugar content, which health professionals link to issues such as cardiovascular problems, sleep disturbances, and anxiety. Mayo Clinic, for instance, warns that energy drinks pose cardiovascular risks from high caffeine, sugar, taurine, and stimulants like guarana, causing jitters, hypertension, and crashes, especially when mixed with exercise, alcohol, or medications.

Natural alternatives such as coffee, tea, yerba mate, or L-theanine provide safer caffeine with bioactive benefits. Rising health awareness has led to closer regulatory scrutiny from authorities that are considering stricter rules on ingredient limits and labeling practices.

The potential for litigation and negative media coverage also creates reputational risks that may discourage health-conscious consumers, especially as scientific discussions continue regarding the long-term effects of regular consumption.

This evolving regulatory environment requires manufacturers to invest significantly in compliance systems, product reformulation, and more transparent communication with consumers. It may also restrict certain marketing practices, particularly those aimed at younger audiences or focused on extreme performance claims, which can slow growth in sensitive demographic segments.

As expectations around health, safety, and labeling continue to tighten, brands that fail to adapt proactively risk losing market share to competitors that align more closely with new regulatory standards, medical guidance, and shifting consumer trust expectations.

Organic and Natural Product Segment Expansion

The organic energy drinks segment shows strong growth potential as more consumers seek healthier, natural beverage options that avoid synthetic pesticides, GMOs, and artificial additives.

Health-conscious buyers increasingly prioritize clean-label products made with organic ingredients that provide energy support without the negative associations linked to conventional formulations. This shift reflects a broader move toward products perceived as safer, more transparent, and aligned with long-term well-being goals.

This trend is reinforced by growing interest in functional beverages containing natural herbs, botanicals, and vitamins, which appeal to both young adults and professionals seeking sustained performance and support for managing everyday stress.

The organic segment also enables premium pricing, improving margin opportunities for manufacturers while aligning closely with sustainability-focused and wellness-oriented lifestyles. Brands that invest in credible organic product development and certification are well-positioned to capture this emerging demand and drive meaningful revenue growth.

Category-wise Analysis

Product Type Insights

Caffeinated beverages are expected to dominate in 2026, commanding approximately 76.5% of the U.S. energy drinks market revenue share. The strong position stems from caffeine's fundamental role as the primary stimulant ingredient, providing immediate alertness and energy enhancement that consumers expect from energy drinks.

Leading brands promote energy drinks as functional beverages that boost energy, reduce daily stress, and improve concentration and work efficiency. Manufacturers are incorporating B-vitamins, amino acids, alongside caffeine to provide comprehensive performance benefits, differentiating products within the caffeinated category while maintaining the core energy-boosting proposition.

De-caffeinated beverages are likely to be the fastest-growing segment during the 2026 - 2033 forecast period. This expansion reflects growing consumer awareness of the potential adverse health effects of caffeine and rising demand for alternative energy sources.

Decaffeinated formulations use natural ingredients such as B-vitamins, guarana, and taurine to provide sustained energy without caffeine-related side effects like jitters, sleep disruption, or cardiovascular strain. This segment is particularly attractive to caffeine-sensitive consumers, evening users, and individuals seeking a milder stimulation profile.

Packaging Insights

Cans are slated to account for approximately 92.5% of market revenue share in 2026. The superior functional performance and broad consumer appeal of cans across several key dimensions largely drive this dominance. Metal cans provide an effective barrier to light and oxygen, helping to preserve beverage freshness, flavor, and perceived quality over extended periods.

They also cool more quickly than most other packaging types, which is especially attractive for on-the-go consumption. In addition, aluminum cans are lightweight yet robust, supporting efficient transportation and shelf stocking while reducing logistics costs compared with bulkier or heavier formats.

Bottles are expected to be the fastest-growing segment from 2026 to 2033. This segment is expanding rapidly because it aligns closely with evolving consumer preferences for convenience, sustainability, and a more premium brand experience.

Polyethylene terephthalate (PET) bottles offer resealability, portability, and strong recyclability credentials, making them particularly attractive to environmentally conscious, on-the-go consumers. Glass bottles further support growth by reinforcing premium positioning, perceived product purity, and strong brand aesthetics, which help justify higher price points in the market.

Sales Channel Insights

At 84.5%, the offline channel is anticipated to be the leading channel in 2026. This category encompasses supermarkets, hypermarkets, convenience stores, and online retail platforms that enable consumers to purchase products for off-premise consumption.

The immense reach through various intermediaries such as Walmart and Target, along with numerous convenience stores, provides consumers with the needed convenience for easy purchasing. These retail formats offer extensive shelf space displaying diverse brands and flavors, enabling consumers to evaluate ingredients, pricing, and nutritional information before purchasing.

The online channel is anticipated to be the fastest-growing during the 2026 - 2033 forecast period. E-commerce platforms provide unparalleled convenience through home delivery, subscription services, and one-click purchasing, which appeal to time-constrained consumers.

Leveraging B2C distribution channels enables energy drink companies to enter new markets and expand their customer base efficiently through digital marketing tools, social media platforms, and e-commerce websites. Online channels allow the access to detailed product information, customer reviews, competitive pricing comparisons, and promotional offers, enhancing purchasing decisions.

Competitive Landscape

The U.S. energy drinks market structure is moderately concentrated, with dominant players such as Monster Beverage Corporation, PepsiCo, Inc., The Coca-Cola Company, and AriZona Beverages collectively controlling 55% to 60% of the market revenues. This oligopolistic structure establishes high barriers to entry, allowing incumbents to command premium pricing and allocate substantial resources to marketing and brand development.

Established brands maintain their leadership through aggressive positioning, leveraging high-profile sponsorships in extreme sports, partnerships with e-sports organizations, and strategic social media campaigns to foster loyalty among core consumer groups. Their extensive reach and brand recognition provide a sustainable competitive advantage that is difficult for new entrants to overcome.

Mid-tier brands such as Celsius, Bang, and Rockstar differentiate themselves by focusing on product innovation, niche market segments, and targeted promotional strategies. These companies often appeal to health-conscious or performance-driven consumers by introducing unique formulations and messaging. Smaller regional brands and private-label products cater to price-sensitive shoppers by offering more affordable alternatives, often with localized branding.

Key Industry Developments

- In December 2025, Celsius announced that it will launch four zero-sugar, fruit-forward energy drinks - Sparkling Raspberry Peach, Mango Lemonade, Kiwi Guava, and Strawberry Watermelon - in the U.K. and Ireland from January 2026 across retailers, convenience stores, and gyms.

- In August 2025, PepsiCo deepened its push into energy drinks through a US$ 585 million deal that expands its long-term partnership with Celsius Holdings and strengthens its multi-brand energy portfolio alongside Rockstar and Alani Nu.

- In March 2025, Tilray Wellness partnered with Whole Foods Market to relaunch HiBall Energy nationwide in U.S. retail, bringing the clean-label sparkling energy seltzer back to shelves after revitalizing the brand online.

Companies Covered in U.S. Energy Drinks Market

- The Coca Cola Company

- PepsiCo

- Cellucor

- Red Bull GmbH

- Monster Energy Company

- BANG Beverage Company LLC.

- 5-hour Energy

- Celsius

- Keurig Dr Pepper

- ZOA Energy

- NOS Energy Company

- Congo Brands

- Zevia

- AriZona Beverages USA

- G FUEL

- Optimum Nutrition

Frequently Asked Questions

The U.S energy drinks market is projected to reach US$ 28.0 billion in 2026.

Rising demand for convenient functional energy, health-focused formulations, lifestyle marketing, and expanding distribution channels are driving the market.

The market is poised to witness a CAGR of 8.3% from 2026 to 2033.

Key opportunities include premium and organic formulations, health-focused positioning, and e-commerce expansion.