- Beverages

- Ready to Drink Coffee Market

Ready to Drink Coffee Market Size, Share, and Growth Forecast 2026 - 2033

Ready to Drink Coffee Market by Packaging (Bottles, Cans, Cartons), by Nature (Conventional, Organic), by Distribution Channel (B2C, B2B), and Regional Analysis, 2026 - 2033

Ready to drink coffee Market Share and Trends Analysis

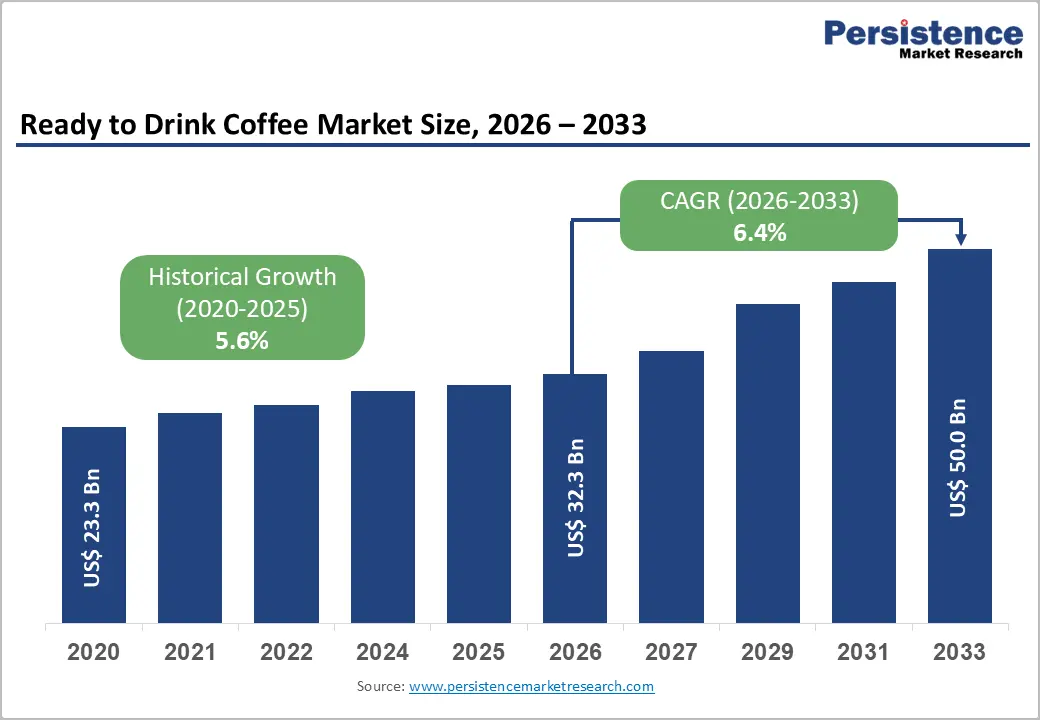

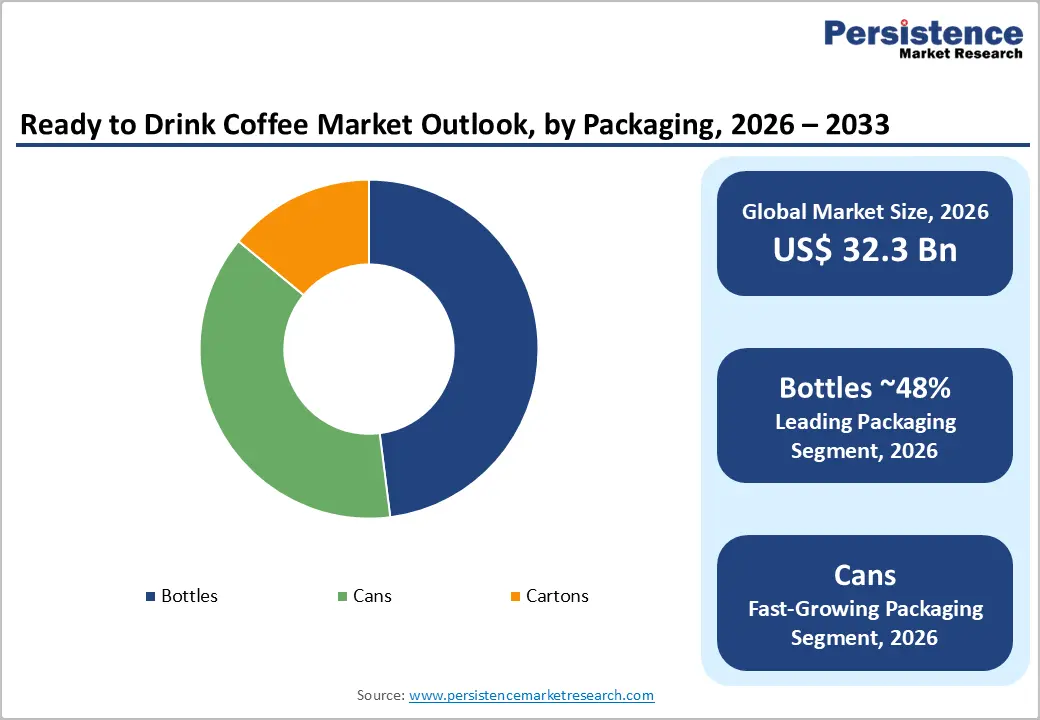

The global ready to drink coffee market size is expected to be valued at US$ 32.3 billion in 2026 and projected to reach US$ 50.0 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033. The ready-to-drink (RTD) coffee market is emerging as the fastest-growing segment within the global coffee industry, expanding at double-digit rates.

Growth is largely fueled by increasing consumption of cold coffee among Gen Z and millennial consumers who prefer convenient, on-the-go beverage options. RTD coffee offers a combination of taste, portability, and variety, making it highly attractive to younger demographics. Key markets such as India, the Middle East & North Africa (MENA), and Brazil present strong growth potential, supported by large youth populations. Manufacturers are expanding their RTD portfolios with diverse flavors and formats to capture evolving consumer preferences and lifestyle-driven demand.

Key Industry Highlights:

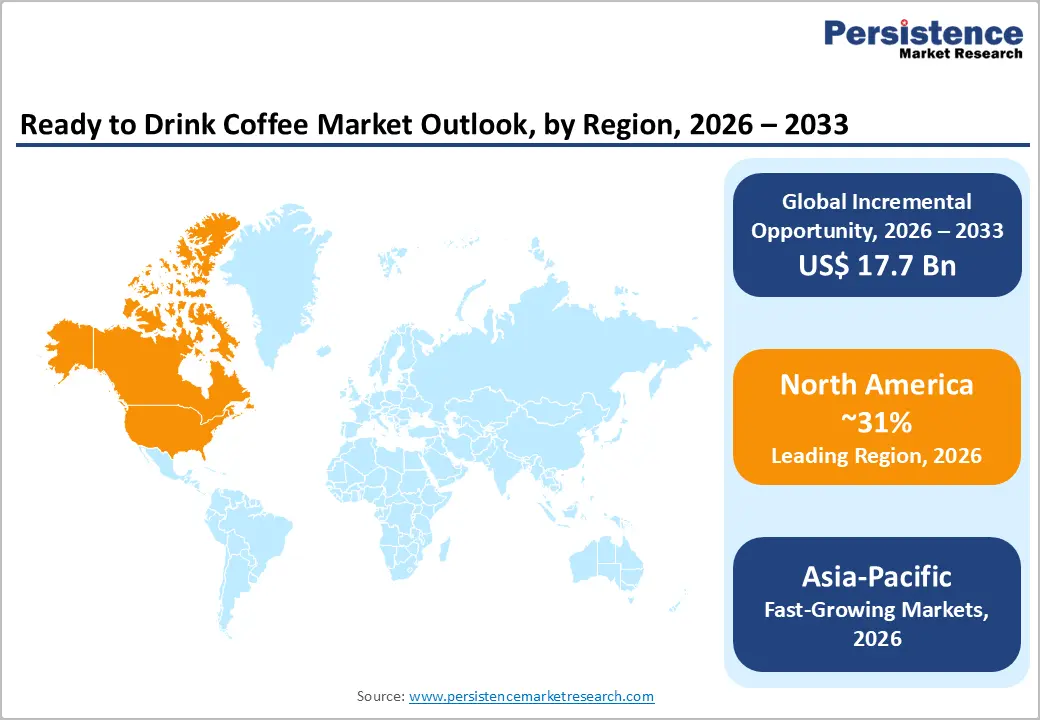

- Leading Region: North America leads the global ready-to-drink coffee market, supported by strong coffee culture, high product innovation, established retail networks, and significant investments by major beverage companies.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by rapid urbanization, rising disposable incomes, expanding café culture, and increasing adoption of Western beverage trends.

- Dominant Segment: Bottled packaging dominates the market, accounting for the largest revenue share due to resealability, convenience, premium appeal, and wide availability across retail channels.

- Fastest Growing Segment: Canned RTD coffee is the fastest-growing segment, fueled by rising demand for portable, lightweight, and highly recyclable packaging formats aligned with sustainability trends.

| Key Insights | Details |

|---|---|

| Ready to Drink Coffee Market Size (2026E) | US$ 32.3 billion |

| Market Value Forecast (2033F) | US$ 50.0 billion |

| Projected Growth CAGR (2026 - 2033) | 6.4% |

| Historical Market Growth (2020 - 2025) | 5.6% |

Market Dynamics

Driver - Rising Demand for Convenience and On-the-Go Consumption

The primary driver of the Ready-to-Drink (RTD) coffee market is the growing demand for convenience among urban consumers. Rapid urbanization, busy lifestyles, and longer working hours have significantly influenced beverage consumption patterns. Consumers increasingly prefer portable, ready-made options that eliminate preparation time while delivering consistent taste and quality. RTD coffee fits seamlessly into daily routines, particularly for working professionals, students, and commuters seeking quick energy boosts during travel or work breaks. The expansion of modern retail formats, vending machines, and convenience stores has further improved accessibility, making RTD coffee widely available across urban and semi-urban areas. Additionally, attractive packaging formats such as bottles and cans enhance portability and shelf life, encouraging impulse purchases. Premiumization trends, including cold brew and flavored variants, also allow brands to command higher price points while meeting evolving taste preferences.

Health-Conscious and Functional Beverage Innovations

Another major growth driver is the rising demand for healthier and functional beverage options. Consumers are increasingly seeking low-sugar, plant-based, and protein-enriched RTD coffee products that align with wellness-focused lifestyles. Growing awareness regarding calorie intake and clean-label ingredients has encouraged manufacturers to introduce organic, dairy-free, and fortified variants containing vitamins, natural caffeine, and adaptogens. Government dietary guidelines and sugar-reduction initiatives are further accelerating this shift. For instance, the UK government’s Soft Drinks Industry Levy (sugar tax) has pushed beverage manufacturers to reformulate products with lower added sugar, influencing innovation across coffee-based drinks as well. Similar public health policies in several countries promoting reduced sugar intake are indirectly supporting demand for low-calorie and functional RTD coffee variants.

Restraint - High Production and Raw Material Costs

One of the major restraints in the Ready-to-Drink (RTD) coffee market is the rising cost of raw materials and production. Fluctuations in global coffee bean prices, driven by climate change, supply chain disruptions, and geopolitical uncertainties, significantly impact manufacturing margins. Increased costs of packaging materials such as aluminum cans and PET bottles further add financial pressure on producers. Transportation and cold-chain logistics expenses also contribute to higher overall operational costs. As a result, manufacturers often face challenges in maintaining competitive pricing while preserving profit margins. Smaller and regional players are particularly vulnerable, as they may lack the scale advantages required to absorb cost fluctuations. This can limit product innovation, marketing investments, and geographic expansion.

Intense Competition from Alternative Beverages

The RTD coffee market also faces strong competition from alternative functional beverages such as energy drinks, ready-to-drink teas, flavored water, and protein drinks. These alternatives attract consumers seeking variety, unique flavors, and enhanced functional benefits like hydration or performance boosting. Established energy drink brands invest heavily in marketing and youth-oriented campaigns, which can shift consumer loyalty away from RTD coffee. Additionally, the growing popularity of healthier beverage substitutes with lower caffeine or sugar content poses competitive pressure. This intense competition can restrict market penetration and limit growth opportunities, especially among younger demographics.

Opportunity - Expanding Millennial and Gen Z Consumer Base

The growing population of millennials and Gen Z presents a strong opportunity for the ready-to-drink (RTD) coffee market. According to Qureos data published in August 2024, Gen Z accounts for nearly 32% of the global population, making them a highly influential consumer segment. This generation demonstrates a strong preference for convenient, portable, and trend-driven beverages that align with their fast-paced lifestyles. RTD coffee brands can capitalize on this demographic shift by introducing innovative flavors, functional variants, and visually appealing packaging tailored to younger consumers. The emphasis on social media presence and experiential branding further enhances engagement with this audience.

Additionally, industry insights indicate that Gen Z consumers show greater inclination toward RTD coffee compared to traditional hot brew formats, reflecting changing consumption habits. Their preference for cold brew, flavored, and ready-to-consume options creates opportunities for product diversification and premium positioning. By aligning offerings with evolving taste profiles and lifestyle needs, companies can significantly expand market penetration and strengthen long-term growth prospects.

Category-wise Analysis

By Packaging Insights

Bottled packaging is projected to hold the highest share in the ready-to-drink (RTD) coffee market in 2026, accounting for approximately 48% of total revenue. Bottles, including PET and glass formats, are widely preferred due to their resealability, durability, and premium shelf appeal. Consumers value bottles for their convenience, especially for multi-sip consumption during travel, office hours, or workouts. Transparent PET bottles also allow product visibility, strengthening consumer trust and purchase decisions. Additionally, bottles support a variety of product innovations, including dairy-based, plant-based, and protein-enriched RTD coffee variants. Strong presence across supermarkets, convenience stores, and vending machines further contributes to the segment’s leadership position.

Cans, on the other hand, are expected to be the fastest-growing packaging segment during the forecast period. Growth is driven by rising demand for lightweight, portable, and highly recyclable packaging solutions. Aluminum cans offer superior barrier protection against light and oxygen, helping maintain flavor freshness and shelf stability. Sustainability trends and increasing consumer preference for eco-friendly formats are accelerating adoption. Moreover, sleek can designs and compact sizes appeal strongly to younger, on-the-go consumers, supporting rapid market expansion.

By Distribution Channel Analysis

In 2025, B2C channels continue to dominate the RTD coffee market, contributing nearly ~80% of global revenue. Supermarkets and hypermarkets remain the primary sales outlets, offering extensive product assortments across flavors, formats, and price points. These retail formats benefit from high footfall, promotional pricing strategies, and strong brand visibility. Convenience stores also play a crucial role, particularly in urban centers, were impulse purchases and immediate consumption drive sales. The availability of chilled storage in retail outlets further supports product turnover.

Meanwhile, online retail and direct-to-consumer platforms are witnessing steady expansion, supported by growing e-commerce penetration and subscription-based beverage models. Digital channels allow brands to introduce limited-edition flavors and personalized bundles, strengthening customer engagement. Although B2B sales to cafés, airlines, and institutional buyers represent a smaller share, they are gradually increasing as RTD coffee becomes integrated into broader foodservice offerings.

Regional Insights

North America Ready to Drink Coffee Market Trends

The North America ready-to-drink (RTD) coffee market accounted for over 30% of global revenue in 2025 and continues to demonstrate steady growth in 2026. A deeply rooted coffee culture, combined with strong consumer preference for convenient beverage options, supports sustained demand across the U.S. and Canada. Millennials and Gen Z consumers significantly influence purchasing patterns, favoring premium cold brew, functional blends, and low-sugar variants. High product innovation, including plant-based and protein-enriched offerings, further strengthens category expansion. The region benefits from a well-established retail infrastructure, with supermarkets, convenience stores, and vending channels driving strong product visibility and accessibility.

In addition, major beverage manufacturers are investing heavily in expanding production capabilities and distribution networks. Large-scale manufacturing facilities and strategic partnerships enhance supply chain efficiency and support new product launches. E-commerce penetration and subscription beverage models are also gaining traction, enabling brands to directly engage consumers. Sustainability initiatives, including recyclable packaging and ethically sourced beans, further shape purchasing decisions and contribute to long-term market growth in North America.

Asia Pacific Ready to Drink Coffee Market Trends

The Asia Pacific RTD coffee market is projected to grow through 2033, supported by rapid urbanization and evolving lifestyle patterns. Increasing exposure to Western food and beverage trends, coupled with rising disposable income, is driving greater acceptance of coffee-based beverages across emerging economies. Countries such as China, Japan, South Korea, India, and Australia are witnessing expanding café culture and higher consumption of chilled coffee formats. The region’s warm climate further fuels demand for cold brew and ready-to-consume iced coffee products.

Digital influence and strong social media penetration are playing a vital role in shaping consumer preferences, particularly among younger demographics. Online retail platforms and convenience stores are expanding distribution reach, making RTD coffee more accessible in both metropolitan and tier-2 cities. Local and international brands are actively launching new flavors and functional variants tailored to regional taste preferences. Investments in marketing campaigns and product localization strategies are expected to further accelerate growth across the Asia Pacific market.

Competitive Landscape

The ready-to-drink (RTD) coffee market is highly competitive, characterized by the presence of global beverage giants, regional brands, and emerging specialty players. Companies compete through product innovation, flavor diversification, functional formulations, and premium positioning. Strategic partnerships, acquisitions, and capacity expansions are common approaches to strengthening market presence. Brands are increasingly focusing on sustainable packaging, clean-label ingredients, and plant-based offerings to attract health-conscious consumers. Strong distribution networks across supermarkets, convenience stores, and e-commerce platforms provide a competitive edge. Marketing campaigns targeting millennials and Gen Z further intensify rivalry, driving continuous innovation and brand differentiation in the market.

Key Industry Developments:

- In February 2026, Starbucks and Arla introduced a new range of playful ready-to-drink coffee SKUs, expanding their product portfolio with innovative offerings.

- In April 2025, Nestlé expanded its Nescafé Ready-to-Drink coffee portfolio into India, the Middle East & North Africa (MENA), and Brazil, focusing on young, on-the-go consumers looking for convenient cold coffee beverages.

Companies Covered in Ready to Drink Coffee Market

- Nestlé

- Starbucks Coffee Company

- Sleepy Owl Coffee

- Tata Consumer Products Limited

- Kings Coffee

- Rage Coffee

- Costa

- Tim Hortons

- Blue Bottle Coffee, Inc.

- Inspire Brands, Inc. (Dunkin’)

- Others

Frequently Asked Questions

The ready to drink coffee market is estimated to be valued at US$ 32.3 Bn in 2026.

Rising on-the-go consumption, premiumization trends, expanding café culture, innovative flavors, and increasing demand for convenience beverages.

The global ready to drink coffee (RTD) market is expected to witness a CAGR of 6.4% between 2026 and 2033.

A few of the prominent players operating in the market are Nestlé, Starbucks Coffee Company, Sleepy Owl Coffee, Tata Consumer Products Limited, Kings Coffee, and others.

North America is the leading region in the global ready to drink coffee market.