- Beverages

- Coffee Beverages Market

Coffee Beverages Market Size, Share, and Growth Forecast, 2026-2033

Coffee Beverages Market by Coffee Type (Instant, Filter, Bean-to-Cup, Ready-to-drink), Bean Type (Robusta, Arabica, Others), Distribution Channel (Hypermarkets/Supermarkets, Convenience Stores, Specialty Coffee Shops, Online Retail, Others), and Regional Analysis for 2026-2033

Coffee Beverages Market Share and Trends Analysis

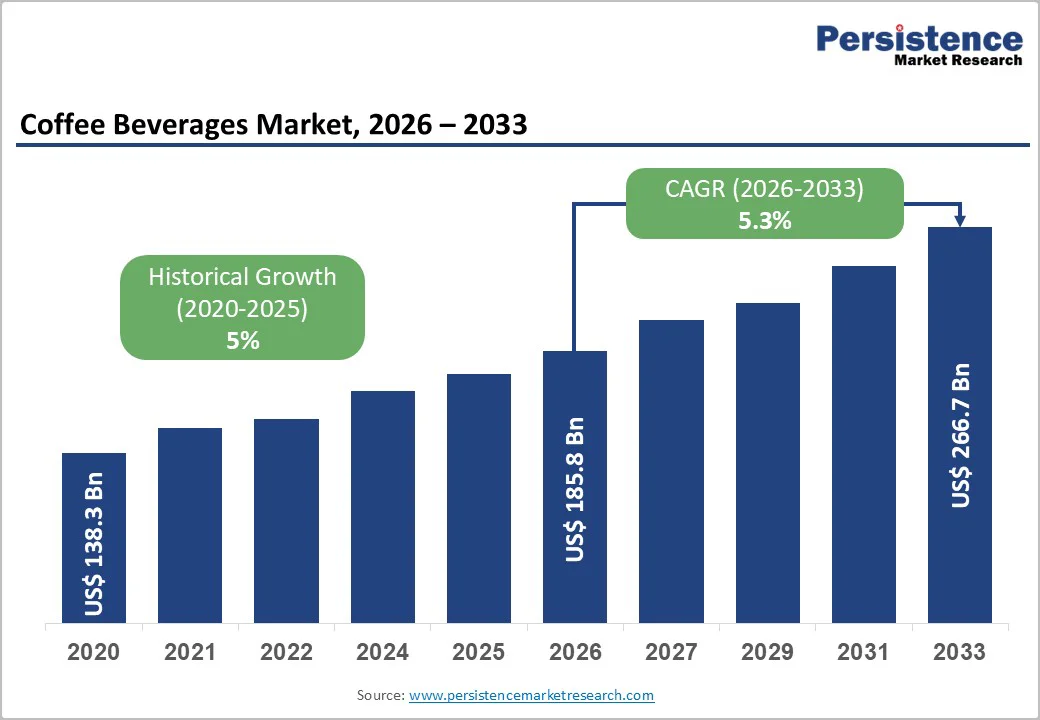

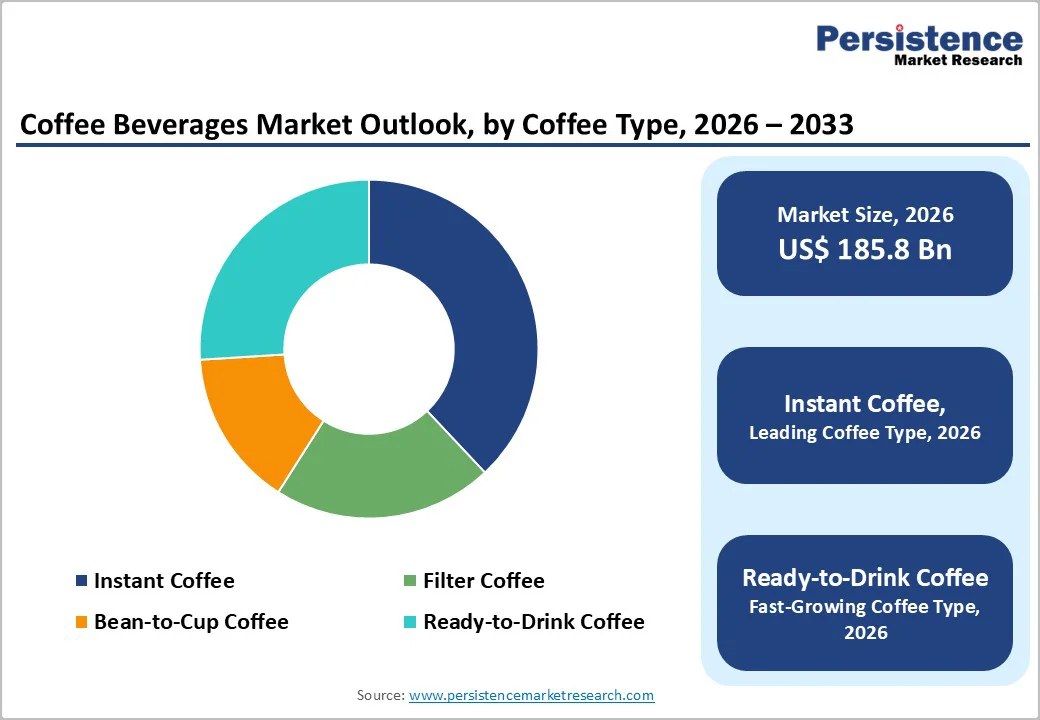

The global coffee beverages market size is likely to be valued at US$ 185.8 billion in 2026, and is projected to reach US$ 266.7 billion by 2033, growing at a CAGR of 5.3% during the forecast period 2026-2033. Market expansion is driven by consistently high global coffee consumption, accelerating urbanization, and the ongoing and growing trend toward high-quality, specialty beverages in everyday consumption. The increasing demand for ready-to-drink coffee, advancements in bean-to-cup coffee technologies, and deeper retail penetration across emerging markets are reshaping consumption behavior. The shifting consumer preferences toward convenience, product transparency, and distinctive flavor experiences, supported by stable demand from foodservice operators and workplace consumption channels, continue to strengthen market growth fundamentals.

Key Industry Highlights

- Leading Coffee Type: Instant coffee is expected to hold the largest share at 38% in 2026, while ready-to-drink coffee is projected to be the fastest-growing at a CAGR of about 7.1% through 2033.

- Dominant Bean Type: Arabica beans are set to dominate at approximately 60% in 2026, whereas Robusta beans are expected to register the fastest value growth at a CAGR of 6%, driven by rising demand for instant and mass-market coffee products.

- Primary Distribution Channel: Hypermarkets and supermarkets are poised to account for 40% in 2026, while online retail is anticipated to be the fastest-growing channel through 2033, fueled by digital engagement and subscription models.

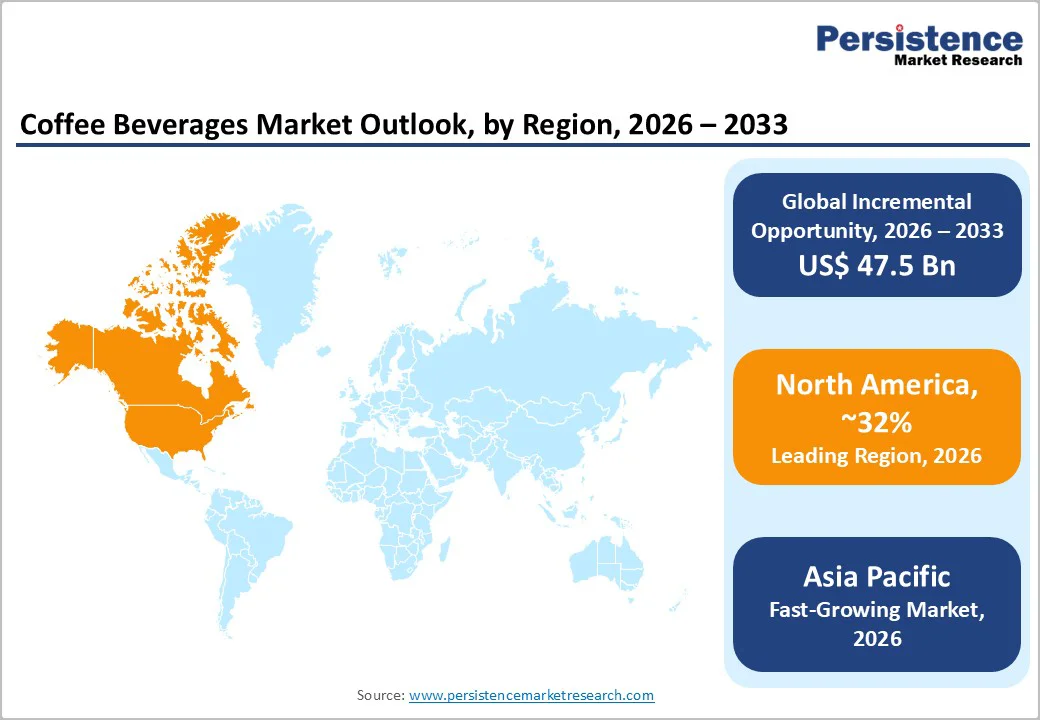

- Regional Leadership: North America is slated to hold around 32% market share in 2026, while the Asia Pacific market is projected to register a CAGR of 8.5% through 2033, supported by an expanding café culture.

- November 2025: The 24th Seoul Cafe Show hosted Asia’s largest coffee exhibition, providing a major platform for brands to showcase innovations and tap into business opportunities.

| Report Attribute | Details |

|---|---|

|

Coffee Beverages Market Size (2026E) |

US$ 185.8 Bn |

|

Market Value Forecast (2033F) |

US$ 266.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Urbanization and Product Innovation Boosting Coffee Market Growth

The coffee market continues to benefit from rapid urbanization and shifting consumer lifestyles. As of 2024, approximately 57.7% of the world’s population resides in urban areas, surpassing the 56% mark around 2020, according to the United Nations Department of Economic and Social Affairs (UN DESA) and the World Bank. Urban density, longer working hours, and dual-income households are driving increased consumption across instant, filter, and ready-to-drink formats. This structural trend is boosting per-capita intake in both mature and emerging markets, providing a robust foundation for sustained growth.

Product innovation and convenience-focused formats are reshaping demand, particularly in the ready-to-drink coffee segment, which is experiencing rapid adoption in markets like India, driven by quick commerce and evolving consumer lifestyles. Flavor diversification, including caramel, mocha, and other variants, is gaining traction, with major players such as Nestlé’s Nescafé expanding their ready-to-drink portfolios. Advances in bean-to-cup systems, cold-brew extraction, and functional formulations, such as low-sugar and plant-based options, enable brands to differentiate products while maintaining premium pricing. Shelf-stable packaging and wider availability through convenience stores and online channels further enhance scalability and revenue potential, reinforcing long-term resilience in global coffee markets.

Supply Instabilities and Health-Driven Moderation Affecting Market Growth

Despite strong global demand, the coffee beverages market growth faces significant supply-side challenges. The industry relies heavily on coffee bean production, with Arabica and Robusta cultivation concentrated in specific regions, making supply chains vulnerable to climate change, extreme weather, and geopolitical instability. These factors can trigger sharp price fluctuations, increase raw material costs, and disrupt production schedules, particularly in premium and specialty coffee segments. Even as overall consumption rises, such supply constraints could limit manufacturers’ ability to scale efficiently, maintain consistent margins, and respond quickly to growing market demand in both mature and emerging markets.

Improving health consciousness among consumers is also influencing coffee consumption patterns. Narrative and systematic reviews published in 2025 indicate that moderate consumption (2–4 cups daily) provides benefits such as reduced risk of chronic conditions, improved cognitive function, and lower all-cause and cardiovascular mortality. However, research presented at the ACC Asia 2024 conference showed that habitual intake above 400 mg of caffeine per day can elevate heart rate and blood pressure, increasing the risk of cardiovascular events. Growing awareness of these potential risks, along with concerns about sugar content and stricter labeling regulations, is prompting some consumers to reduce intake or switch to alternative beverages.

Expanding Consumption and Innovative Channels Driving Market Growth

The market for coffee beverages can experience strong growth potential in emerging economies, particularly in Asia Pacific, Latin America, and Africa. Rising middle-class populations, urbanization, and expanding retail infrastructure are increasing per-capita coffee consumption, especially in markets such as India and Southeast Asia. Even modest gains in daily intake in these regions represent multi-billion-dollar opportunities for global manufacturers. Expanding café culture, workplace consumption, and household adoption of packaged coffee products further reinforce long-term demand growth and market penetration. In October 2025, for instance, the inaugural Laredo Coffee Festival in Texas highlighted rising local engagement, featuring competitions, specialty drink makers, and live events, demonstrating how experiential marketing supports consumer adoption.

Innovative distribution channels and sustainable practices can also opening new revenue streams. The rapid expansion of online and direct-to-consumer platforms allows brands to enhance margins, gather first-party consumer insights, and scale personalized offerings. Growing demand for ethically sourced and traceable coffee supports premium pricing and strengthens brand equity. Strategic moves by leading companies, such as Coca-Cola exploring options for Costa Coffee to unlock growth, Chobani raising US$ 650 million in equity for facility expansions, and Illycaffè partnering with Iberia Airlines to enhance travel retail offerings, illustrate how market players are leveraging partnerships, investments, and experiential initiatives to capture new consumers and reinforce long-term brand loyalty.

Category-wise Analysis

Coffee Type Insights

Instant coffee is expected to remain the leading coffee type by volume, accounting for approximately 38% of global consumption in 2026. Its affordability, long shelf life, and easy preparation make it particularly popular among price-sensitive and rural consumers. The segment enjoys widespread penetration across emerging markets in Asia Pacific and Eastern Europe, and is favored for household consumption due to convenience and compatibility with traditional brewing practices. Retailers also benefit from its stable demand, predictable inventory turnover, and broad availability across hypermarkets, supermarkets, and convenience stores.

Ready-to-drink (RTD) coffee is poised to be the fastest-growing segment, projected to expand at a CAGR of 7.1% from 2026 to 2033. The growth of RTD coffee is driven by widespread urbanization, increasingly mobile lifestyles, and an escalating number of convenience-seeking consumers. Innovations such as cold-brew formulations, functional enhancements, and sustainable packaging are increasing appeal among younger urban professionals. Major launches in 2025 include Starbucks Iced Energy and Frappuccino Lite in the U.S., along with Nestlé’s Starbucks-branded RTD coffee for Indian retail markets, highlighting the segment’s potential to create incremental revenue alongside traditional coffee formats.

Beans Type Insights

Arabica beans are projected to dominate in 2026, capturing roughly 60% of the coffee beverages market revenue share in 2026, on account of their superior flavor, aromatic complexity, and preference in specialty and premium coffee channels. Arabica is particularly favored in North America and Europe, where specialty coffee culture and café consumption drive higher per-unit prices. Its presence underpins the growth of bean-to-cup and high-quality instant offerings, reinforcing brand differentiation and enabling premium pricing. Consumers’ appreciation for traceability and single-origin products further strengthens Arabica’s market leadership.

Robusta beans are likely to represent the fastest-growing segment, with a projected CAGR of 5.5% between 2026 and 2033. Their high yield, lower production cost, and suitability for instant coffee formulations make it attractive in mass-market and emerging economies. Rising demand in ready-to-drink and affordable instant coffee products contributes to Robusta’s accelerated growth. The segment benefits from expanding retail penetration, streamlined supply chains, and broader adoption in value-conscious markets, supporting incremental volume and revenue alongside Arabica-driven premium segments.

Distribution Channel Insights

Hypermarkets and supermarkets are likely to be the leading distribution channels, accounting for approximately 40% of the coffee beverages market sales in 2026. These facilities benefit from high foot traffic, extensive shelf space, private-label offerings, and strong presence in urban and semi-urban regions. These channels serve as the primary purchase point for households globally, providing predictable demand patterns and stable revenue for manufacturers. Their widespread reach supports both premium and mass-market coffee products, maintaining consistent consumption volumes across established and emerging markets.

Online retail is projected to be the fastest-growing distribution channel, expected to achieve a CAGR of roughly 9% through 2033. The growth is fueled by increased smartphone adoption, digital payments, and convenience-focused shopping behavior, particularly among urban professionals and younger consumers. Subscription models, personalized product offerings, and direct-to-consumer engagement are further accelerating market expansion. The digital channel allows brands to capture first-party consumer data, optimize inventory management, and scale marketing initiatives, creating long-term opportunities in both mature and emerging coffee markets.

Regional Insights

North America Coffee Beverages Market Trends

North America is likely to lead in 2026, accounting for approximately 32% of the coffee beverages market share, with the United States at the forefront due to high per-capita intake and a mature café culture. The region benefits from strong adoption of ready-to-drink and specialty coffee formats, supported by urban lifestyles and workplace consumption. Regulatory oversight ensures product transparency and fosters consumer confidence, particularly in functional and fortified coffee variants. Premium retail formats and established distribution networks maintain stable value growth, while product innovation in cold brew, plant-based creamers, and functional beverages enhances differentiation.

Competitive intensity in North America is high, encouraging continuous investment in R&D and marketing initiatives. The presence of major international and regional players drives innovation and brand positioning, while private equity and institutional investment sustain expansion. Consumer preference for convenience, sustainability, and traceable sourcing is shaping product offerings. North America combines market maturity, high per-capita consumption, and strong innovation ecosystems, maintaining its leadership position in the global market for coffee beverages.

Europe Coffee Beverages Market Trends

Europe is anticipated to be a structurally strong market, with Germany, the U.K., France, and Spain leading adoption. Harmonized regulations across the European Union facilitate efficient cross-border trade and consistent labeling standards. Consumer demand is increasingly influenced by sustainability, ethical sourcing, and traceable coffee, particularly in premium and specialty segments. Specialty coffee culture, café chains, and premium retail formats support steady value growth, while private-label penetration influences pricing dynamics in Western Europe.

The region emphasizes innovation in product offerings, including plant-based variants, functional formulations, and single-origin specialty coffees. Competitive pressures drive product differentiation and investment in marketing campaigns that highlight quality, sustainability, and health-conscious positioning. Regulatory compliance ensures consumer trust while creating operational complexity for multinational brands. Europe’s mature market, sustainability focus, and premium coffee culture support consistent growth while enabling incremental market expansion through specialty and differentiated products.

Asia Pacific Coffee Beverages Market Trends

Asia Pacific is projected to be the fastest-growing coffee beverages market, expanding at a CAGR of around 8.5% through 2033, driven by key markets including China, Japan, India, and ASEAN countries. Rising urban populations, growing café chains, and increasing exposure to Western coffee consumption patterns are accelerating demand. Per-capita intake is rising in urban centers, supported by higher disposable incomes, changing lifestyles favoring convenience and premium formats, and proximity to coffee-producing countries. Government policies promoting food processing, retail expansion, and trade further strengthen market fundamentals.

The growth of the regional market is supported by modern retail channels, online platforms, and the ready-to-drink coffee segment, which is gaining traction among urban professionals. Starbucks’ milestone of opening its 500th coffeehouse in India underscores rapid retail expansion, while record coffee exports highlight opportunities in value-added products. Events such as the India International Coffee Festival 2025 in Bengaluru, featuring the National Barista Championship and National Filter Coffee Championship, are fostering coffee culture, skills development, and consumer engagement. Urban café culture, workplace adoption, and demand for premium, ethically sourced, and specialty beverages are driving both market penetration and high-value product growth.

Competitive Landscape

The global coffee beverages market structure is moderately consolidated, with key players including Nestlé, JAB Holding Company, Starbucks Corporation, Jacobs Douwe Egberts, and Tata Consumer Products capturing a substantial portion of revenue. These companies leverage strong brand recognition, wide distribution networks across retail, specialty cafés, and online channels, and diversified portfolios spanning instant, ready-to-drink, and premium coffee. Continuous innovation in product offerings, sustainability, and functional beverages helps maintain market leadership. Their direct-to-consumer and subscription models further enhance engagement and revenue.

Smaller and regional players focus on niche markets such as single-origin Arabica, specialty RTD products, and ethically sourced coffee. Entry barriers remain moderate due to brand loyalty, distribution reach, and quality consistency requirements. Digital channels and online subscriptions provide opportunities for emerging brands to grow. Market consolidation is expected over time as leading companies pursue mergers, acquisitions, and strategic partnerships to expand geographic presence, enhance product portfolios, and strengthen competitiveness.

Key Industry Developments

- In December 2025, Oatly launched two new ready-to-drink Barista Iced Macchiato and Barista Iced Flat White products in Tesco stores across the U.K., targeting the growing grab-and-go cold coffee segment among younger consumers, particularly Generation Z. The oat-based drinks, which combine barista oat milk with Arabica coffee, support Oatly’s broader profitable growth and sustainability strategy as it triples investment in British oats and positions itself as a certified Climate Solutions Company.

- In November 2025, Starbucks and Tata Starbucks announced a new Farmer Support Partnership (FSP) to support 10,000 Indian coffee farmers by 2030, focusing on sustainability, farm income, and productivity. The initiative includes technical model farms, 1 million Arabica seedlings, and agronomy training across Karnataka, Tamil Nadu, Andhra Pradesh, and Kerala.

- In August 2025, Keurig Dr Pepper (KDP) reached an agreement to acquire JDE Peet’s for approximately US$ 18 billion, aiming to create a global coffee champion with around US$ 16 billion in projected annual sales. Post-acquisition, KDP plans to split into two independent companies: a global coffee entity and a North America-focused beverage company, enhancing geographic reach and portfolio scale.

Companies Covered in Coffee Beverages Market

- Nestlé S.A.

- JDE Peet’s N.V.

- Starbucks Corporation

- The Coca-Cola Company

- Keurig Dr Pepper Inc.

- Luigi Lavazza S.p.A.

- Tata Consumer Products

- Strauss Group Ltd.

- Illycaffè S.p.A.

- Suntory Holdings

- UCC Holdings

- Dunkin’

Frequently Asked Questions

The global coffee beverages market is projected to reach US$ 185.8 billion in 2026.

Massive coffee consumption globally, high urbanization rates, widening adoption of convenience-led lifestyles, and increasing demand for premium and specialty coffee products are factors driving market growth.

The market is poised to witness a CAGR of 5.3% from 2026 to 2033.

Key opportunities include expansion of online retail and direct-to-consumer channels, rising demand for ethically sourced and sustainable coffee, and increasing preference for functional and innovative coffee formats.

Nestlé S.A., JDE Peet’s N.V., Starbucks Corporation, The Coca-Cola Company, and Keurig Dr Pepper are some of the key players in the market.