- Biotechnology

- Tissue Plasminogen Activator Market

Tissue Plasminogen Activator Market Size, Share, and Growth Forecast, 2025 - 2032

Tissue Plasminogen Activator Market By Drug Type (Alteplase (rtPA), Tenecteplase (TNK-tPA)), Indication (Ischemic Stroke, Acute Myocardial Infarction), Mode of Administration, End-user, and Regional Analysis for 2025 - 2032

Tissue Plasminogen Activator Market Size and Trends Analysis

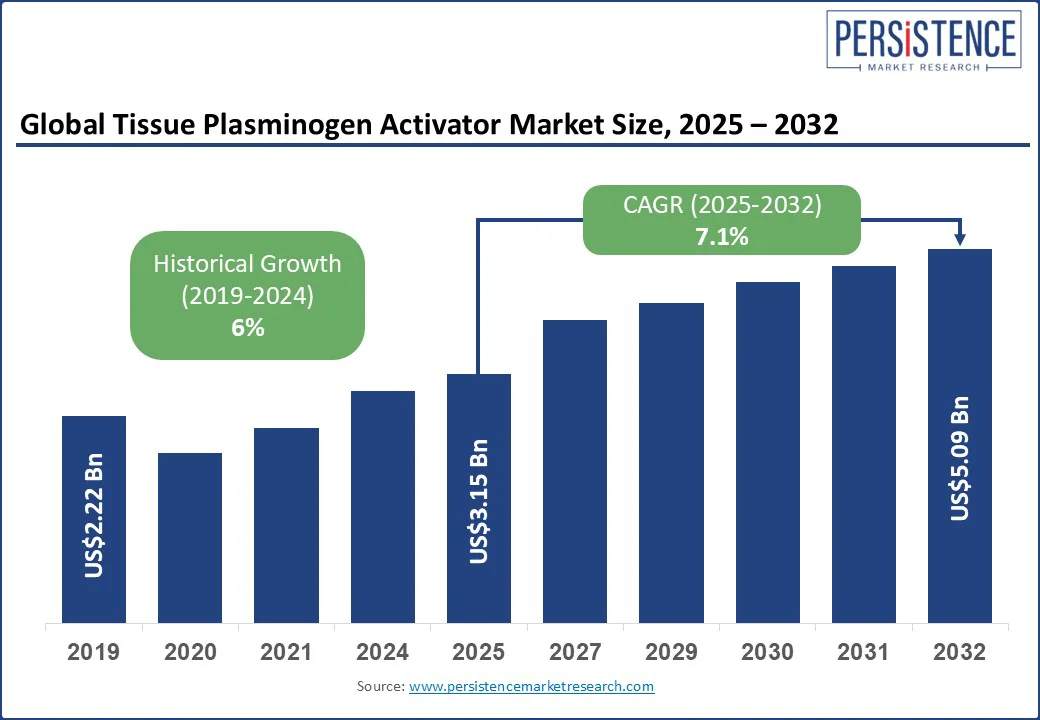

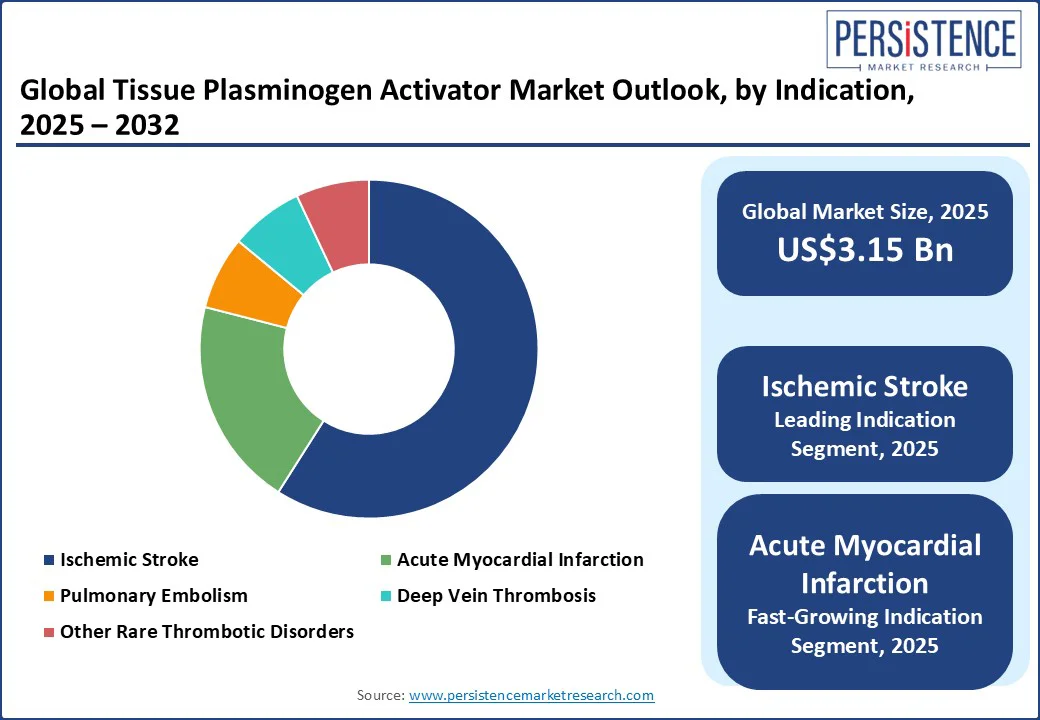

The global tissue plasminogen activator market size is likely to be valued at US$3.15 Bn in 2025 and is expected to reach US$5.09 Bn by 2032, growing at a CAGR of 7.1% during the forecast period from 2025 to 2032.

Key Industry Highlights:

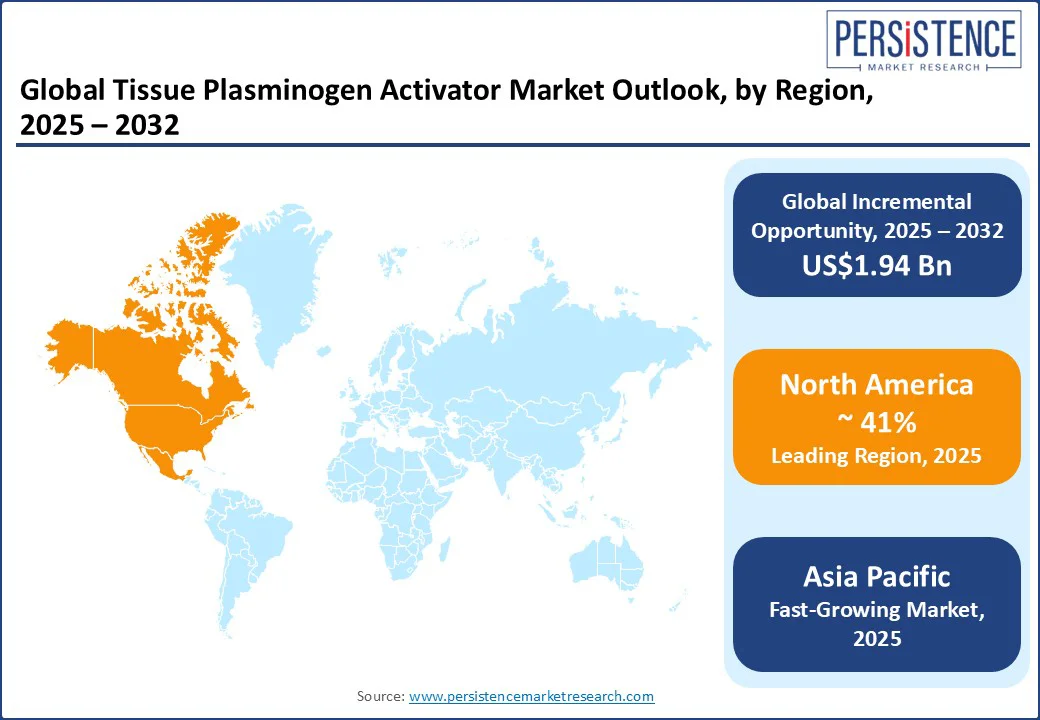

- Leading Region: North America is anticipated to lead with a market share of 41%, driven by high stroke prevalence, strong adoption of tenecteplase and alteplase, and recent FDA approvals expanding indications.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, supported by rising cardiovascular disease burden, rapid expansion of stroke care infrastructure in China and India, and increasing use of biosimilar tPA formulations.

- Dominant Drug Type: Alteplase (rtPA) continues to dominate the market with a share of over 54.8%, due to its widespread global acceptance, inclusion in clinical stroke guidelines, and hospital familiarity, though tenecteplase is rapidly challenging its dominance.

- Leading Indication: Ischemic Stroke is the leading therapeutic indication, accounting for nearly 59% of global tPA revenues, as it remains the primary condition where rapid thrombolysis has proven life-saving benefits.

| Global Market Attribute | Key Insights |

|---|---|

| Tissue Plasminogen Activator Market Size (2025E) | US$3.15 Bn |

| Market Value Forecast (2032F) | US$5.09 Bn |

| Projected Growth (CAGR 2025 to 2032) | 7.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 6% |

The tissue plasminogen activator (tPA) market is witnessing steady growth, driven by the rising prevalence of ischemic stroke, myocardial infarction, and thromboembolic disorders, where rapid clot dissolution is critical to patient outcomes. Increasing awareness of stroke management protocols, advancements in emergency care infrastructure, and supportive government initiatives are further boosting adoption across hospitals and specialty clinics.

Market Dynamics

Driver - AI-Driven Stroke Triage and Next-Gen tPA Delivery Transform Emergency Care

A major growth driver for the tissue plasminogen activator market is the adoption of AI-assisted stroke triage networks, which use advanced imaging and telestroke systems to rapidly identify eligible patients and administer tPA within its narrow therapeutic window. This significantly improves the efficiency of time-sensitive thrombolytic therapy, ensuring faster decision-making in emergency care.

Another important factor is the development of nanoparticle-encapsulated tPA for enhanced clot-specific delivery, which increases precision by targeting clots more effectively while reducing the risk of bleeding. These innovations not only improve patient safety but also expand the number of patients who can benefit from tPA treatment.

The rising adoption of single-bolus tenecteplase (TNKase) in acute ischemic stroke is also shaping the market, as it simplifies administration compared to traditional infusion-based tPA and offers better accessibility in emergency settings.

Advancements in precision dosing algorithms integrated with genomic and biomarker data also help clinicians personalize tPA regimens, optimizing both efficacy and safety in patients with complex conditions such as obesity-related thrombotic disease.

Restraint - Short Circulation Half-Life and Neurotoxicity Limit tPA’s Therapeutic Reach

One of the major limitations of tissue plasminogen activator therapy is its short circulation half-life and limited clot penetration, which reduce its effectiveness in treating large or well-established clots. As tPA is cleared from the bloodstream within minutes, higher doses are often required, raising the risk of hemorrhagic conversion complications in ischemic stroke.

Another concern is the neurotoxic effects of exogenous tPA crossing the blood-brain barrier, as this can worsen ischemic injury in certain patients and restrict its safe application across broader stroke populations.

Challenges also arise with newer delivery innovations, such as magnetic nanoparticle systems for localized tPA release, which remain difficult to translate clinically, as magnetic fields cannot easily be directed to deeper blood vessels.

Researchers are still testing shear-activated nanotherapeutics designed for thrombus-triggered tPA release. As these systems rely on hemodynamic triggers such as elevated shear stress, they remain unpredictable in complex vascular anatomies, thereby delaying their adoption in routine clinical use.

Opportunity - Nanotech-Enabled Precision Thrombolysis Paves Way for Safer, Smarter Stroke Therapy

One major opportunity for the tissue plasminogen activator market lies in the development of pH-sensitive antioxidant nanoparticle formulations. These advanced delivery systems protect tPA and extend its half-life in the bloodstream and also reduce oxidative stress during reperfusion, which often worsens ischemic injury.

Another promising innovation is the use of biomimetic platelet-membrane-coated nanovesicles for single-bolus administration. By mimicking the natural properties of platelets, these nanocarriers can deliver rtPA more safely, remain stable in storage, and minimize bleeding risks, making them highly attractive for rapid stroke interventions.

There is also a strong potential in discoidal polymeric nanoconstructs (tPA-DPNs), which replicate the shape and flexibility of red blood cells to shield tPA from degradation and deliver it directly to clots. This approach allows for effective thrombolysis at lower doses, improving safety while enhancing treatment efficiency. In addition, researchers are exploring theranostic nanoplatelets that combine targeted delivery with diagnostic tracking, enabling real-time monitoring of clot dissolution while reducing side effects.

Category-wise analysis

Drug Type Insights

In 2025, the largest drug segment is anticipated to be Alteplase (rtPA) with a market share of 54.8%. As the first recombinant tPA approved for clinical use, it remains the gold standard for thrombolytic therapy and continues to dominate global sales. Alteplase is recommended in leading treatment guidelines for ischemic stroke, myocardial infarction, and pulmonary embolism, which makes it the most widely adopted therapy.

It accounts for the majority share of the market, and studies suggest alteplase alone generates more than one-third of global revenues. Its long history of use, strong safety data, and inclusion on the WHO’s Essential Medicines list further reinforce its leadership. A prime example is Activase, marketed by Genentech and Boehringer Ingelheim, which has consistently delivered over US$1 Bn in annual sales.

The fastest-growing drug segment is Tenecteplase (TNK-tPA). Unlike alteplase, which requires a one-hour infusion, tenecteplase is given as a single bolus injection, making it much easier to administer in emergency settings. It also has a longer half-life and promising trial data showing equal or better outcomes compared to alteplase, with a lower risk of intracranial hemorrhage.

This practicality has fueled rapid adoption, especially in hospitals that manage high volumes of stroke and heart attack cases. Tenecteplase recently gained FDA approval for acute ischemic stroke in 2025, becoming the first new thrombolytic drug approved for stroke in decades. By 2023, it already held about one-quarter of the U.S. stroke thrombolysis market, generating nearly US$850 Mn in revenue.

Indication Insights

The largest indication segment is expected to be ischemic stroke, which accounts for the highest demand for tissue plasminogen activators worldwide, with around 59% of the market share in 2025. It is one of the most common thrombotic emergencies, and the timely use of tPA has been proven to reduce mortality and long-term disability.

Healthcare systems have invested heavily in stroke-ready hospitals, telestroke networks, and awareness campaigns, which have strengthened adoption. Market research indicates ischemic stroke represents the majority share of the overall tPA market.

Clinical studies continue to expand their relevance. For example, a 2025 trial in China demonstrated that alteplase could improve recovery even when administered up to 24 hours after stroke onset, potentially widening the treatment window and boosting usage further.

The fastest-growing indication segment is projected to be Acute Myocardial Infarction (AMI). While ischemic stroke remains dominant, rising global rates of heart attack have increased the demand for rapid reperfusion therapies. Thrombolysis remains particularly important in settings where catheter-based interventions are not immediately available.

Tenecteplase has gained strong traction here as its single-bolus administration is well-suited for emergency cardiac care. As tenecteplase is already FDA-approved for STEMI (ST-elevation myocardial infarction), its expanding role in AMI management makes it one of the most dynamic growth areas.

Regional Insights

North America Tissue Plasminogen Activator Market Trends - Strong Stroke Care Infrastructure and Expanding Use of Tenecteplase

North America is projected to be the leading market, accounting for approximately 41% of total market revenue in 2025, driven by advanced healthcare infrastructure, a strong presence of pharmaceutical companies, and well-established stroke management networks. The U.S. dominates this regional market, accounting for a significant portion of global revenues, largely due to the rapid adoption of tenecteplase in both ischemic stroke and acute myocardial infarction care.

In 2025, the FDA approved Tenecteplase (TNKase) for the treatment of acute ischemic stroke, a major development that positioned the U.S. at the forefront of thrombolytic therapy innovation. Hospitals across the U.S. are also strengthening stroke telemedicine programs to ensure the timely administration of thrombolytics in underserved regions.

For instance, Mayo Clinic expanded its telestroke network in 2024, which significantly improved patient outcomes in rural states where immediate access to neurologists was previously limited.

Canada is another important contributor, particularly through its focus on national stroke care frameworks. The Canadian Stroke Best Practices guidelines strongly emphasize thrombolytic therapy within 4.5 hours of symptom onset, which has increased alteplase and tenecteplase utilization in hospital emergency settings.

A recent 2024 Canadian registry study found that tenecteplase was associated with shorter door-to-needle times compared to alteplase, prompting several provinces to pilot its wider adoption. Combined with government-led initiatives to expand stroke centers, Canada’s market is expected to grow steadily, supported by public healthcare reimbursement systems.

Asia Pacific Tissue Plasminogen Activator Market Trends - Rapid Market Expansion with Growing Stroke Burden and Healthcare Investments

Asia Pacific represents the fastest-growing market for tissue plasminogen activators, driven by an increasing incidence of ischemic stroke, rapid healthcare infrastructure development, and growing access to advanced therapies. China leads the region, fueled by a rising number of stroke-ready hospitals and government-backed initiatives such as the “Stroke Center Construction Program”, which aims to standardize acute stroke treatment nationwide.

In 2025, a multicenter trial in China expanded the clinical evidence for alteplase beyond the conventional 4.5-hour window, which is expected to significantly increase patient eligibility and market demand. With domestic companies also developing biosimilars to reduce therapy costs, China is positioned as one of the most dynamic growth markets.

India is another key country where the market is advancing rapidly, primarily due to the rise in stroke awareness and public-private partnerships aimed at improving access to emergency care. A notable development occurred in 2024, when several state governments partnered with private hospitals to establish stroke-ready centers that provide immediate thrombolysis.

While high treatment costs remain a barrier in rural regions, initiatives such as Apollo Hospitals’ expansion of its stroke telemedicine services are helping bridge gaps in care delivery. India’s large patient population and rising investments in emergency medicine training make it a critical growth engine for the Asia Pacific thrombolytic agent (tPA) market.

Europe Tissue Plasminogen Activator Market Trends - Strong Guidelines, Biosimilar Growth, and Expanding Stroke Networks

Europe has established itself as a highly structured market for tPA therapies, backed by comprehensive treatment guidelines and widespread use of thrombolytic agents in both stroke and cardiovascular emergencies. Germany leads the region with strong adoption rates, supported by its extensive hospital network and emphasis on clinical research.

In 2024, Boehringer Ingelheim launched pilot programs in several German hospitals evaluating next-generation biosimilars of alteplase, reflecting Europe’s openness to lower-cost alternatives that maintain therapeutic efficacy. Germany’s advanced reimbursement systems and large elderly population further sustain high demand.

The U.K. is also witnessing notable growth in thrombolytic adoption, particularly through its National Health Service (NHS) stroke care pathways. NHS England’s ongoing “Get It Right First Time” (GIRFT) initiative emphasizes reducing treatment delays and optimizing acute stroke therapy, where thrombolytics remain a core intervention.

A 2023 NHS audit reported that alteplase remained widely used, but tenecteplase was increasingly being adopted in specialized stroke units due to its ease of administration and encouraging trial results. The U.K.’s strong research ecosystem, including the University of Glasgow’s 2024 trial on TNK-tPA in prehospital settings, underscores the region’s commitment to pushing the boundaries of thrombolytic therapy.

Competitive Landscape

The global tissue plasminogen activator market is moderately consolidated, with a few multinational pharmaceutical players dominating global sales. Companies such as Boehringer Ingelheim, Genentech (Roche), and Bristol Myers Squibb remain market leaders due to their established product portfolios, strong clinical trial data, and wide hospital networks.

These players are also actively investing in expanding indications for existing drugs, such as extending the treatment window for alteplase and tenecteplase, while simultaneously exploring next-generation biosimilars to strengthen market positioning.

At the same time, competition is intensifying with the entry of regional and generic manufacturers, especially in the Asia Pacific and Europe, where biosimilars and cost-effective alternatives are gaining traction.

Partnerships between academic institutes and biotech firms are driving innovation in nanoparticle-based tPA delivery systems to improve safety and efficacy, signaling a shift toward precision medicine. This competitive push is expected to accelerate product differentiation, increase accessibility in emerging markets, and create new opportunities for collaboration across the healthcare ecosystem.

Key Industry Developments:

- In March 2025, the U.S. Food and Drug Administration approved TNKase (tenecteplase) as the first major new stroke medication in nearly 30 years, offering a single five-second IV bolus as a faster, simpler alternative to the 60-minute infusion of alteplase. Tenecteplase had already been approved for STEMI and now reinforces Genentech’s leadership in stroke care.

- In November 2024, DiaMedica expands the Phase 2/3 ReMEDy2 stroke trial protocol, submitting updates to the FDA to include patients unresponsive to initial thrombolytic therapy (tPA or tenecteplase) and increasing the sample size for interim analysis, with top-line results anticipated in Q4 2025.

Companies Covered in Tissue Plasminogen Activator Market

- Genentech, Inc. (Roche Holding AG)

- Boehringer Ingelheim International GmbH

- Bristol Myers Squibb Company

- Pfizer Inc.

- Grifols S.A.

- Teva Pharmaceutical Industries Ltd.

- Sanofi S.A.

- Eli Lilly and Company

- CSL Behring

- Johnson & Johnson (Janssen Pharmaceuticals)

- Dr. Reddy’s Laboratories Ltd.

- Zydus Lifesciences Ltd.

- Biocon Ltd.

- Intas Pharmaceuticals Ltd.

- Cadila Pharmaceuticals Ltd.

- Shenzhen Tongde Pharmaceutical Co., Ltd.

- Hainan Poly Pharm Co., Ltd.

- Wuhan Hualong Bio-Pharmaceutical Co., Ltd.

- Reliance Life Sciences Pvt. Ltd.

- Sun Pharmaceutical Industries Ltd.

Frequently Asked Questions

The tissue plasminogen activator market size is estimated at US$3.15 Bn in 2025.

By 2032, the tissue plasminogen activator market is projected to reach US$5.09 Bn.

Key trends include the rising adoption of tenecteplase as an alternative to alteplase, the development of biosimilar tPA formulations, integration of AI-based stroke detection systems to expand timely administration, and innovations in nanoparticle-based delivery systems to enhance safety and efficacy.

By drug type, Alteplase (rtPA) leads the market with more than 55% share due to its widespread clinical use and guideline inclusion. By indication, Ischemic Stroke dominates with nearly 60% of revenues, as it is the primary condition treated with tPA.

The tissue plasminogen activator market is expected to grow at a CAGR of 7.1% from 2025 to 2032.

Major players with a strong portfolio include Boehringer Ingelheim, Genentech (Roche Group), Bristol Myers Squibb, Grifols, S.A., and Abbott Laboratories.