- Biotechnology

- Tissue Culture Reagents Market

Tissue Culture Reagents Market: Size, Share, Trends, Growth, and Forecast 2025 - 2032

Tissue Culture Reagents Market by Product Type (Media, Growth Factors, Enzymes, Antibiotics, Buffers, Serum), Application Type (Plant Tissue Culture, Animal Cell Culture, Microorganism Culture, Stem Cell Research, Pharmaceutical Development), End-use (Research Laboratories, Biopharmaceutical Companies, Agricultural Companies, Contract Research Organizations (CROs), Academic Institutions), and Regional Analysis for 2025 - 2032

Tissue Culture Reagents Market Size and Trends Analysis

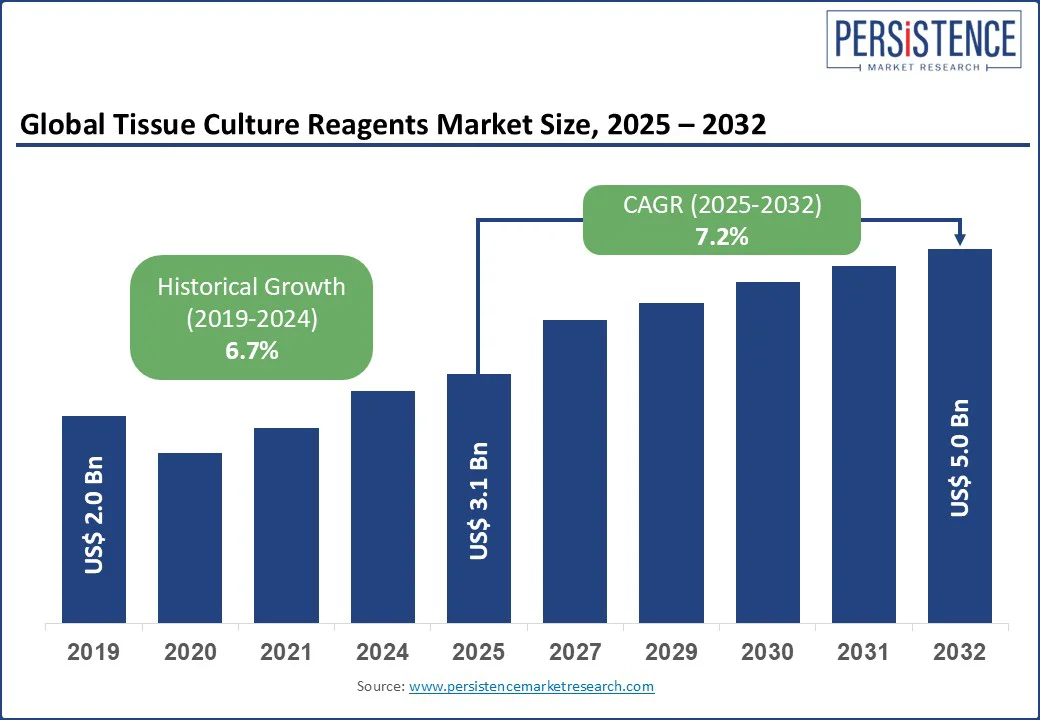

The global tissue culture reagents market size is likely to be valued at US$3.1 Bn in 2025 and is expected to reach US$5.3 Bn by 2032, growing at a CAGR of 7.2% during the forecast period from 2025 to 2032.

The market growth is fueled by increasing investments in cell-based research and breakthroughs in biopharmaceutical manufacturing. The surging demand for personalized medicine is projected to achieve a global value of $1.31 trillion by 2034. Additionally, advancements in CAR-T therapy workflows and supportive government-backed R&D initiatives are enhancing innovation, driving widespread adoption of tissue culture reagents worldwide.

Key Industry Highlights

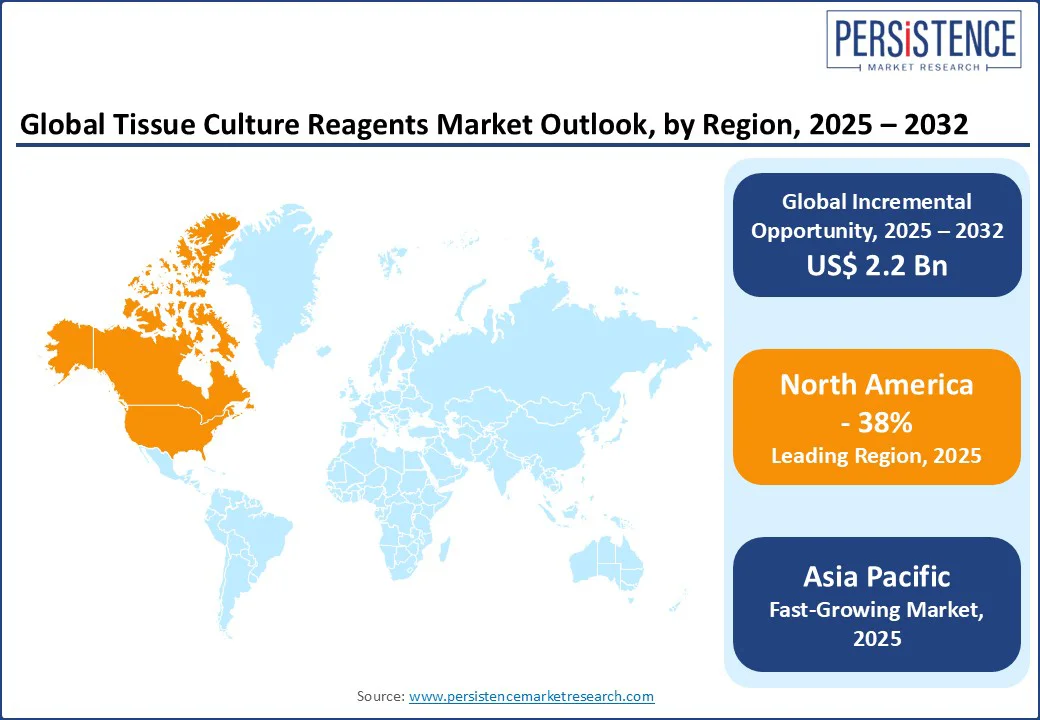

- Leading Region: North America, commanding a 38% market share of the global tissue culture reagents market in 2025, driven by strong R&D capabilities, government funding, and advanced biopharmaceutical infrastructure in the U.S.

- Fastest-Growing Region: Asia Pacific, witnessing rapid growth supported by expanding biotechnology sectors, rising investment in stem cell research, and increasing healthcare infrastructure in China and India.

- Leading Product Type: Media, holding a 43% market share in 2025, due to its essential role in supplying nutrients and maintaining optimal cell growth in culture systems.

- Dominant Application Type: Animal cell culture, capturing a 55% market share, fueled by its widespread use in biologics production, vaccine development, and pharmaceutical research.

- Leading End-use: Biopharmaceutical Companies, with a 45% share, driven by their reliance on tissue culture reagents for drug development, quality testing, and personalized medicine applications.

- Innovation Trends: Serum-free media formulations increased by 20% in 2025, aligning with ethical research practices, regulatory expectations, and demand for reproducible, high-performance culture systems.

|

Global Market Attribute |

Key Insights |

|

Tissue Culture Reagents Market Size (2019) |

US$2.0 Bn |

|

Market Size (2025E) |

US$3.1 Bn |

|

Market Value Forecast (2032F) |

US$5.3 Bn |

|

Projected Growth (CAGR 2025 - 2032) |

7.2% |

|

Historical Market Growth (CAGR 2019 - 2024) |

6.7% |

Market Dynamics

Driver - Rising demand for cell-based research

Rising demand for cell-based research is a major driver, driven by rapid advancements in regenerative medicine, stem cell therapy, and cancer research. Scientists increasingly rely on cell-based models to study disease mechanisms, test drug efficacy, and develop precision medicine solutions. This growing reliance fuels the need for high-quality reagents such as growth media, sera, and supplements, essential for maintaining and replicating healthy cell cultures in vitro.

For instance, in 2023, the U.S. National Institutes of Health (NIH) allocated over $2.3 billion to cell and tissue engineering research. Such public funding promotes large-scale adoption of cell-based studies across academic, pharmaceutical, and biotech institutions. As a result, the sector is witnessing significant growth, driven by expanding research applications, supportive regulatory frameworks, and the global shift toward personalized and regenerative healthcare solutions.

Restraint - High R&D and production costs

High R&D and production costs pose challenges. Developing high-purity reagents costs up to 12% more in 2025 due to stringent quality standards, limiting affordability for academic institutions and small-scale labs. Contamination risks and ethical concerns over serum usage restrict adoption, with 25% of researchers switching to serum-free alternatives due to variability in results.

Regulatory hurdles for GMO-related reagents in plant tissue culture increase compliance costs by 10%, affecting agricultural applications. Supply chain disruptions, including a 15% shortage in key components such as growth factors, constrain production capacity, particularly in emerging markets with limited infrastructure.

Opportunity - Advancements in cell-based Therapies and Regenerative Medicine

Advancements in cell-based therapies and regenerative medicine present a significant growth opportunity. Innovations such as CAR-T cell therapies, stem cell treatments, and tissue engineering rely heavily on precise and reliable tissue culture reagents to cultivate, expand, and manipulate cells.

These therapies offer promising solutions for complex diseases such as cancer, autoimmune disorders, and degenerative conditions, driving heightened demand for specialized culture media, growth factors, and supplements.

The global push toward personalized medicine amplifies this trend, as customized cell therapies require tailored culture conditions to ensure efficacy and safety. Moreover, regulatory approvals for novel regenerative treatments continue to rise, accelerating market adoption. For example, the FDA’s increasing approvals of cell and gene therapies highlight this momentum. As research intensifies and clinical applications expand, tissue culture reagents become indispensable, making this segment a key growth engine within the broader life sciences and biopharmaceutical landscape.

Segmental Analysis

Product Type Insights

Media type dominates, capturing approximately 43% of the total market share. Their essential function in supplying nutrients and maintaining ideal conditions for cell growth makes them vital in applications such as stem cell research, drug discovery, and biopharmaceutical production. Continuous innovations, including serum-free and chemically defined media, further enhance their widespread use and market leadership.

In contrast, growth factors represent the fastest-growing segment. These reagents are crucial for regulating cell behavior, including differentiation and proliferation, which are key processes in regenerative medicine and personalized therapies. The increasing adoption of advanced cell-based treatments requiring precise cellular control is driving heightened demand for growth factors, positioning them as a significant growth opportunity.

Application Type Insights

Animal cell culture dominates, holding an estimated 55% of the tissue culture reagents market share. Its critical role in biopharmaceutical manufacturing, vaccine production, and drug development drives high demand for essential reagents such as culture media, enzymes, and growth factors. The expanding biologics and monoclonal antibody sectors further reinforce animal cell culture’s dominant position.

In contrast, stem cell research is the fastest-growing segment, benefiting from increasing focus on regenerative medicine and personalized therapies. The rising need for specialized reagents to support stem cell growth and differentiation is accelerating this segment’s expansion, making it a key growth driver.

End-use Insights

Biopharmaceutical companies dominate, accounting for approximately 45% of the tissue culture reagents market share. These companies extensively use tissue culture reagents in biologics production, vaccine development, and cutting-edge cell and gene therapies.

The surge in biopharmaceutical innovations and significant investments in drug discovery continuously drive demand for high-quality reagents such as media, growth factors, and enzymes. Their focus on developing personalized medicines and advanced therapies further reinforces their leading position as the primary end-users of tissue culture reagents.

On the other hand, contract research organizations (CROs) represent the fastest-growing segment. As pharmaceutical and biotech companies increasingly outsource research and clinical trial activities, CROs are expanding their capabilities in cell-based assays and drug screening.

This trend is accelerating their consumption of tissue culture reagents, making CROs a crucial growth driver. Growing demand for cost-effective, specialized research solutions positions CROs as a key opportunity for market expansion.

Regional Insights

North America Tissue Culture Reagents Market Trends

North America is projected to dominate the Tissue Culture Reagents Market with a 38% market share in 2025, driven by its robust biopharmaceutical sector and cutting-edge research facilities. Strong government funding, particularly from the NIH, fuels growth in cell-based research and regenerative medicine.

The region’s leading pharmaceutical and biotech companies extensively use tissue culture reagents for drug development, personalized medicine, and vaccine manufacturing. Additionally, increasing regulatory approvals for advanced cell therapies and rising investments in stem cell research boost market demand. North America remains a global leader and key growth region for tissue culture reagents.

Europe Tissue Culture Reagents Market Trends

Europe holds a significant share, supported by its strong focus on biopharmaceutical research and regenerative medicine. The region benefits from substantial funding initiatives by the European Union and national governments to advance cell-based therapies and stem cell research.

Leading pharmaceutical companies and research institutions drive demand for high-quality tissue culture reagents used in drug discovery, vaccine development, and personalized medicine. Additionally, Europe’s stringent regulatory framework ensures high standards for product safety and efficacy, boosting market confidence. With growing investments and innovation, Europe remains a vital and expanding market for tissue culture reagents.

Asia Pacific Tissue Culture Reagents Market Trends

Asia-Pacific is emerging as the fastest-growing region in the Tissue Culture Reagents Market, driven by rapid expansion in biotechnology, increased R&D investments, and strong government support. Countries such as China, India, South Korea, and Japan are investing heavily in stem cell research, regenerative medicine, and biopharmaceutical manufacturing.

Growing demand for personalized therapies, rising clinical trials, and the presence of cost-effective manufacturing capabilities are accelerating reagent consumption. Additionally, the establishment of biotech hubs and favorable regulatory reforms further contribute to the region's growth. Asia-Pacific is expected to lead future expansion in tissue culture innovation and applications.

Competitive Landscape

The global tissue culture reagents market is characterized by intense competition, driven by rapid advancements in cell-based research, biopharmaceutical production, and regenerative medicine. Companies are focusing on developing high-performance, serum-free, and chemically defined reagents to meet evolving research and clinical needs. Innovation, product differentiation, and expansion into emerging markets-especially in Asia-Pacific-are key competitive strategies.

Additionally, increased investment in R&D and automation in cell culture workflows is enhancing production capabilities. With the growing global demand for personalized medicine and stem cell applications, the landscape is becoming increasingly dynamic, pushing manufacturers to improve quality, scalability, and regulatory compliance.

Key Developments

- April 2024 - Thermo Fisher Scientific: Launched Gibco™ CTS™ OpTmizer™ One Serum-Free Medium to improve scalability and consistency in T-cell therapy manufacturing.

- December 2022 - FUJIFILM Irvine Scientific (Shenandoah Biotechnology): Expanded CTGrade™ cytokine and growth factor portfolio, offering cGMP-grade, animal-free proteins for cell therapy applications.

- November 2022 (operations 2025) - FUJIFILM Irvine Scientific: Announced a US $188 million investment in a new cell culture media facility in North Carolina, set to boost global supply from 2025.

Companies Covered in Tissue Culture Reagents Market

- Thermo Fisher Scientific Inc.

- Corning Incorporated

- Becton, Dickinson and Company (BD)

- HiMedia Laboratories Pvt. Ltd.

- PromoCell GmbH

- Biological Industries Israel Beit-Haemek Ltd.

- Bio-Rad Laboratories, Inc.

- FUJIFILM Irvine Scientific, Inc.

- Stemcell Technologies

- Sigma-Aldrich (Merck)

- Cytiva (Danaher Corporation)

- Others

Frequently Asked Questions

The tissue culture reagents market is projected to reach US$ 3.1 Bn in 2025, driven by demand in biopharmaceutical and stem cell research.

Key drivers include cell-based research investments, personalized medicine, and communicable disease research.

The tissue culture reagents market is expected to grow at a CAGR of 7.2% from 2025 to 2032, reaching US$ 5.3 Bn.

Opportunities include 3D cell culture, biopharmaceutical manufacturing, and e-commerce expansion.

Leading players include Thermo Fisher Scientific Inc., Corning Incorporated, Becton, Dickinson and Company, and Cytiva.