- Retail

- Bath and Toilet Tissue Market

Bath and Toilet Tissue Market Size, Share, and Growth Forecast, 2025 - 2032

Bath and Toilet Tissue Market By Product Type (Rolled, Folded), End-user (Residential, Commercial), Distribution Channel (Supermarket/Hypermarket, Specialty Stores, Online Retail), and Regional Analysis for 2025 - 2032

Bath and Toilet Tissue Market Size and Trends Analysis

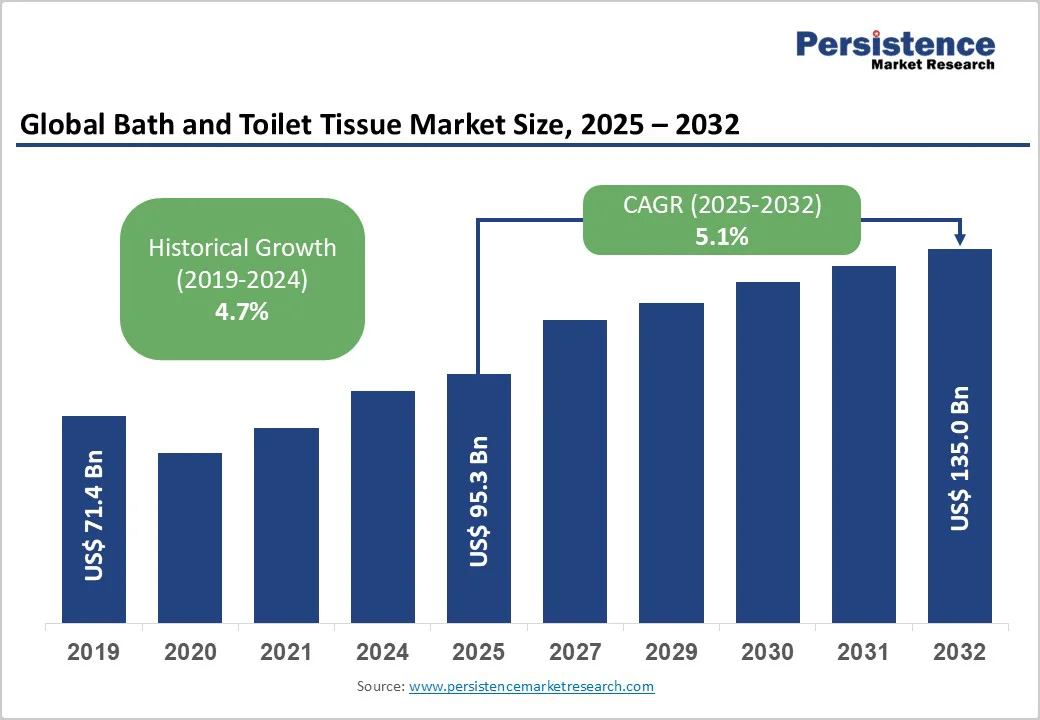

The global bath and toilet tissue market is expected to reach US$95.3 billion in 2025. It is estimated to reach US$135.0 billion in 2032, growing at a CAGR of 5.1% during the forecast period 2025 - 2032, driven by evolving hygiene habits, ongoing urbanization, and lifestyle improvements. Demand is also rising from hotels, airports, and commercial establishments.

Key Industry Highlights

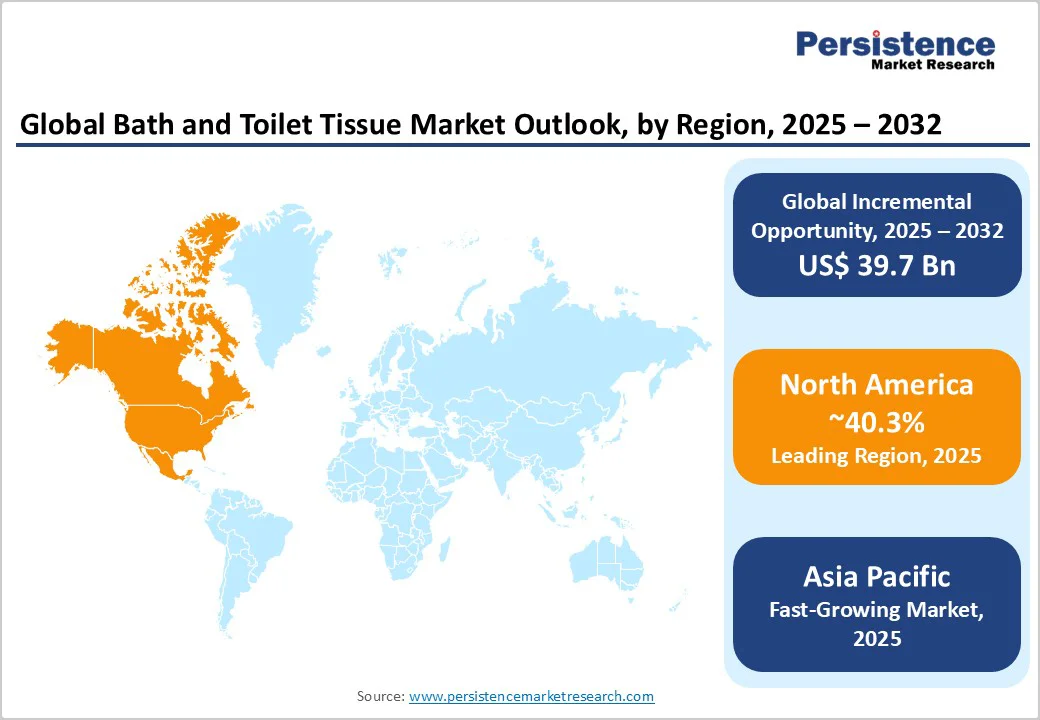

- Leading Region: North America, with about 40.3% share in 2025, driven by strong brand presence from players such as Kimberly-Clark and Procter & Gamble.

- Fastest-growing Region: Asia Pacific, owing to improved sanitation infrastructure and rising adoption of Western hygiene habits.

- New Product: In May 2025, Bashundhara Tissue launched the new 3-ply Bashundhara Toilet Tissue in Dhaka. It has three layers for improved softness, strength, and absorbency.

- Leading Product Type: Rolled formats hold nearly 76.8% share in 2025, since they provide convenience, easy dispensing, and compatibility with standard holders.

- Dominant End-user: Residential, approximately 66.4% of the bath and toilet tissue market share in 2025, boosted by rising awareness of personal hygiene.

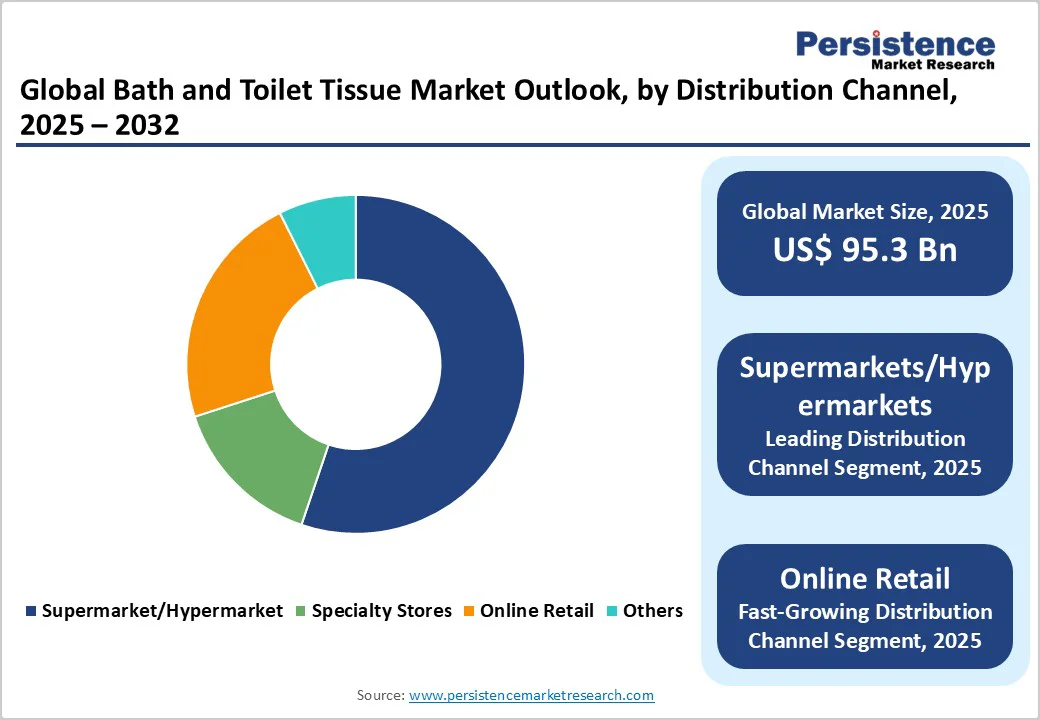

- Key Distribution Channel: Supermarkets/hypermarkets accounted for about 55.2% in 2025, driven by wide product availability and attractive discounts.

| Key Insights | Details |

|---|---|

| Bath and Toilet Tissue Market Size (2025E) | US$95.3 Bn |

| Market Value Forecast (2032F) | US$135.0 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Focus on Cleanliness and Expanding Urban Lifestyle

Increasing hygiene consciousness, combined with ongoing urbanization, is propelling the use of bath and toilet tissues, especially in developing regions. As more people move to cities, modern sanitation facilities are becoming commonplace, boosting demand for tissue products over traditional cleaning methods. Governments and NGOs have also intensified hygiene awareness campaigns.

India’s Swachh Bharat Mission and China’s Healthy China 2030 are major examples. In addition, the surging preference for convenient and disposable hygiene products among urban households is encouraging brands to introduce affordable yet high-quality options suited for mass consumption.

Recovery of Travel and Hospitality Sectors Supporting Demand

The revival of global travel, hotels, and restaurants after the pandemic has restored large-scale commercial consumption of bath and toilet tissues. Hotels are now emphasizing improved hygiene standards, thereby increasing the use of premium, soft, and sustainably sourced tissues.

According to the UN World Tourism Organization, international tourist arrivals rose by over 80% in 2024 compared to pre-pandemic levels, signaling a strong recovery. This rebound has prompted tissue manufacturers such as Essity and Kimberly-Clark to scale up their away-from-home product ranges catering to hospitality, aviation, and corporate facilities.

Barrier Analysis - Strict Forest-protection Rules Squeezing Supply Chains

New laws, such as the EU Deforestation Regulation, are increasing pressure on tissue makers whose pulp or raw paper fiber is linked to deforestation. Even though enforcement is postponed by a year to allow for compliance, the regulation requires traceability, due diligence, and documentation for products derived from wood, palm oil derivatives, and rubber.

Tissue companies exporting or selling into the EU must ensure the non-wood fiber in their products meets these deforestation-free standards. These could compel them to shift suppliers, change sourcing geographies, or absorb the high costs of verified sustainable fiber.

Surging Adoption of Water-spray Toilets Weakening Paper Demand

In many developed countries, bidets and spray-toilet systems are growing rapidly as people prioritize comfort, hygiene, and sustainability. Some reports suggest bidets are reducing reliance on toilet paper in bathrooms.

Since bidet adoption builds over time and becomes more normal, especially in Western Europe and Japan-influenced areas, design influenced by Japan and smart-home upgrades gradually eat into large-roll tissue demand. This shift compels tissue manufacturers to rethink their positioning, possibly leaning more on multipurpose wipes, adding more softness/comfort features, or exploring new formats as usage per person starts to drop.

Opportunity Analysis - Truly Flushable Rolls Becoming Viable after IP Barriers Lift

Patent fences around flushable or coreless roll technologies are loosening, allowing machine-makers and brands to commercialize consumer-ready, cardboard-free rolls and flushable cores finally. Recent collaborations show the concept moving from pilot to supermarket shelves, and market analysts explicitly flag patent expiries as the technical unlock that will enable wide-scale redesigns and flushable formats.

This shift cuts packaging waste and simplifies supply chains. However, it also forces firms to redesign dispensers and prove sewer safety. Hence, the industry is anticipated to see staged product launches and certified trials rather than an immediate market flood.

Premium Layering and Sensory Variants as a Margin Play

Brands are doubling down on high-value tissue by adding extra plies, engineered textures, and scent or tear-quality features to justify premium prices and offset private-label pressure. Charmin’s scalloped-edge Smooth Tear redesign and Kimberly-Clark’s lavender-scented Scott tube are recent examples of small but effective product tweaks that increase perceived value.

Trade coverage and testing labs that report these tweaks can lift shopper satisfaction and short-term sales. One press analysis credited a nearly 5% uplift to smoother-tear introductions. The market is predicted to experience more micro-innovations, including scent-infused cores, quilted structures, and feel claims, packaged as reasons to trade up.

Category-wise Analysis

Product Type Insights

Rolled formats are poised to dominate, with a share of around 76.8% in 2025, as they offer greater convenience, better storage efficiency, and longer usage per unit than folded sheets. Consumers prefer rolls for their easy dispensing and compatibility with modern bathroom fixtures. Manufacturers have also innovated around this format, introducing extra-long rolls, coreless designs, and embossed multi-ply versions to improve comfort and reduce replacement frequency.

Folded tissues continue to see steady demand, primarily in public and commercial settings such as offices, restaurants, and healthcare facilities. Their hygienic, one-sheet dispensing minimizes contact and waste, making them ideal for shared washrooms. Europe-based hygiene brands such as Katrin and Tork have expanded their folded tissue lines with touch-free dispensers to meet strict hygiene regulations in workplaces and hospitality venues.

End-user Insights

The residential segment will likely capture approximately 66.4% of the market in 2025, driven by the everyday nature of bathroom use and rising hygiene awareness. The pandemic reinforced the habit of purchasing tissues for routine home cleaning and personal care.

The expansion of premium products such as ultra-soft and scented variants has encouraged households to trade up. Rising disposable incomes in the Asia Pacific and increasing multi-bathroom homes in North America have boosted domestic demand.

The commercial sector remains a key consumer of bath and toilet tissues, spurred by the recovery of tourism, corporate offices, and educational institutions. The post-pandemic focus on sanitation in public restrooms has led facilities to stock high-capacity rolls and touchless dispensers for better hygiene management. Hospitality chains such as Marriott and Hilton have upgraded to soft yet cost-efficient bulk tissues to improve guest comfort while reducing refill frequency.

Distribution Channel Insights

Supermarkets/hypermarkets are speculated to lead with nearly 55.2% of share in 2025, owing to their extensive shelf space, visibility, and availability of multi-brand promotions. These stores allow consumers to compare quality and softness directly, influencing impulse and bulk purchases. Retail giants such as Walmart and Carrefour frequently provide combo discounts and eco-friendly tissue promotions, which help push both premium and private-label brands.

Online platforms are emerging as prominent distribution channels, fueled by the convenience of doorstep delivery and subscription-based restocking. E-commerce players, including Amazon, and regional marketplaces such as Shopee and Flipkart, have popularized bulk purchases of household tissues with auto-replenishment options. Several manufacturers now run direct-to-consumer websites or partner with e-retailers for exclusive product launches, reinforcing the surging importance of digital retail.

Regional Insights

North America Bath and Toilet Tissue Market Trends

In 2025, North America is expected to account for approximately 40.3% of the share. The market is highly mature and brand-driven, dominated by key players such as Procter & Gamble, Kimberly-Clark, and Georgia-Pacific. These companies continue to enjoy superior brand loyalty for products such as Charmin, Cottonelle, and Angel Soft. But they are also facing intense competition from private-label and regional brands.

To strengthen their foothold, companies are investing heavily in domestic production. For instance, in 2024, Kimberly-Clark announced a multi-billion-dollar investment to expand and modernize its U.S. manufacturing facilities, aiming to boost operational efficiency and product development.

Retailers such as Costco, Walmart, and Target have also upgraded their private-label ranges with premium features, including multi-ply softness and eco-friendly materials. They aim to bridge the gap between branded and store-label products.

Asia Pacific Bath and Toilet Tissue Market Trends

In the Asia Pacific, the market is expanding steadily as hygiene awareness improves and lifestyles modernize. China, India, Indonesia, and Vietnam are witnessing a rise in tissue adoption driven by urbanization, surging middle-class incomes, and changing sanitation habits.

Local companies, including Vinda International in China and Asia Pulp & Paper (APP) in Indonesia, are leading the charge with large-scale production and brand diversification. For example, Vinda has introduced premium variants featuring antibacterial and moisturizing properties to appeal to health-conscious consumers.

A key trend in the Asia Pacific is the balance between affordability and quality. While demand for low-cost products remains high, the premium segment is surging fast in developed markets such as Japan, South Korea, and Singapore, where consumers are more willing to pay for softness, fragrance, or eco-friendly credentials.

Sustainability has become a priority, with manufacturers shifting toward bamboo-based or recycled tissue to reduce environmental impact. For instance, companies in China and Thailand have started promoting bamboo toilet rolls as biodegradable alternatives to wood-pulp varieties.

Europe Bath and Toilet Tissue Market Trends

Europe’s market is highly mature, but development and sustainability define its current scenario. Most households already have high consumption levels, so companies are competing through product differentiation and eco-friendly innovation rather than volume growth.

Essity, one of Europe’s most prominent tissue manufacturers, recently launched Zewa Eco Green, toilet tissue made with straw pulp and wrapped in paper rather than plastic. Modern consumers are highly eco-conscious, pushing brands to obtain FSC or PEFC certifications and adopt recyclable or compostable packaging.

Another notable trend in Europe is the growth of private-label brands from supermarket chains such as Lidl and Carrefour. They provide tissues with similar softness and durability as premium brands but at lower prices. However, inflation and energy costs have increased production costs, prompting several manufacturers to invest in energy-efficient machinery and local sourcing to reduce their dependence on imported pulp.

Competitive Landscape

The global bath and toilet tissue market is characterized by the dominance of multinational giants such as Procter & Gamble, Kimberly-Clark, Essity, and Georgia-Pacific, which control most of the branded segment globally. These companies compete through brand strength, development, and wide distribution networks.

The market also remains highly fragmented at the regional level, with high participation from local manufacturers and private labels, specifically in Asia Pacific and Latin America. Local players often capitalize on low production costs and price-sensitive consumers, creating a two-tiered competition between premium global brands and affordable domestic options.

Key Industry Developments

- In October 2025, Cheeky Panda launched two newly branded toilet tissues in Tesco, including a Silky Soft Toilet Roll 3-ply and Quilted Soft Toilet Roll 4-ply. All tissues are made from 100% FSC-certified bamboo, a fast-growing renewable resource.

- In August 2025, Cascades Inc. introduced Cascades Fluff Excellence. It is a unique bathroom tissue that has been specifically designed to meet consumer expectations for softness, thickness, and strength.

Companies Covered in Bath and Toilet Tissue Market

- Marcal Paper

- Lotus Tissues

- Orchid Paper Products Company

- Kruger Inc.

- Kimberly-Clark Corporation

- Georgia-Pacific LLC

- Hengan

- St. Croix Tissue

- Essity AB

- Sofidel Group

Frequently Asked Questions

The bath and toilet tissue market is projected to reach US$95.3 Billion in 2025.

Rising hygiene awareness and recovery of the hospitality sector are the key market drivers.

The bath and toilet tissue market is poised to witness a CAGR of 5.1% from 2025 to 2032.

Expiry of patents on coreless rolls and surging preference for eco-friendly tissue variants are the key market opportunities.

Marcal Paper, Lotus Tissues, and Orchid Paper Products Company are a few key market players.