- Beauty & Personal Care

- Tissue and Hygiene Market

Tissue and Hygiene Market Size, Share, and Growth Forecast, 2026- 2033

Tissue and Hygiene Market by Product Type (Paper Towels, Toilet Papers, Paper Napkins, Wipes, Incontinence Products, and Others), by End User (Commercial, Hospital and Healthcare, Food and Beverages Industry, and Other), by Distribution Channel (Health and beauty stores, Chemist/Pharmacies/Drugstores, Supermarkets, Convenient Stores, E-retailing, and Others)and Regional Analysis for 2026 – 2033.

Tissue and Hygiene Market Size and Trends Analysis

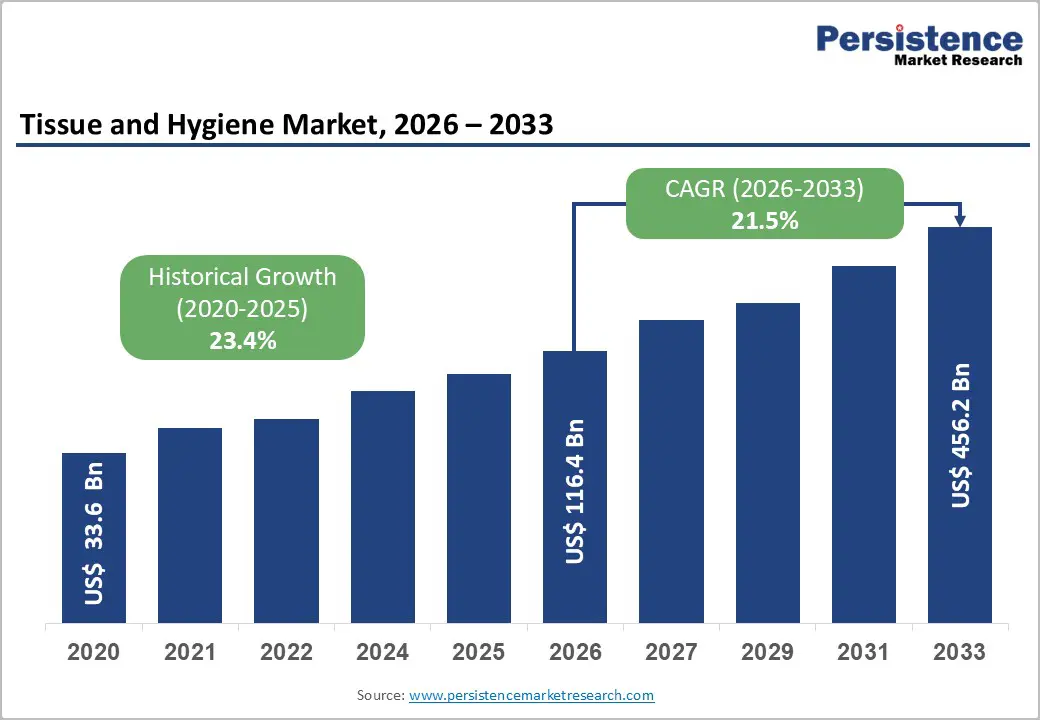

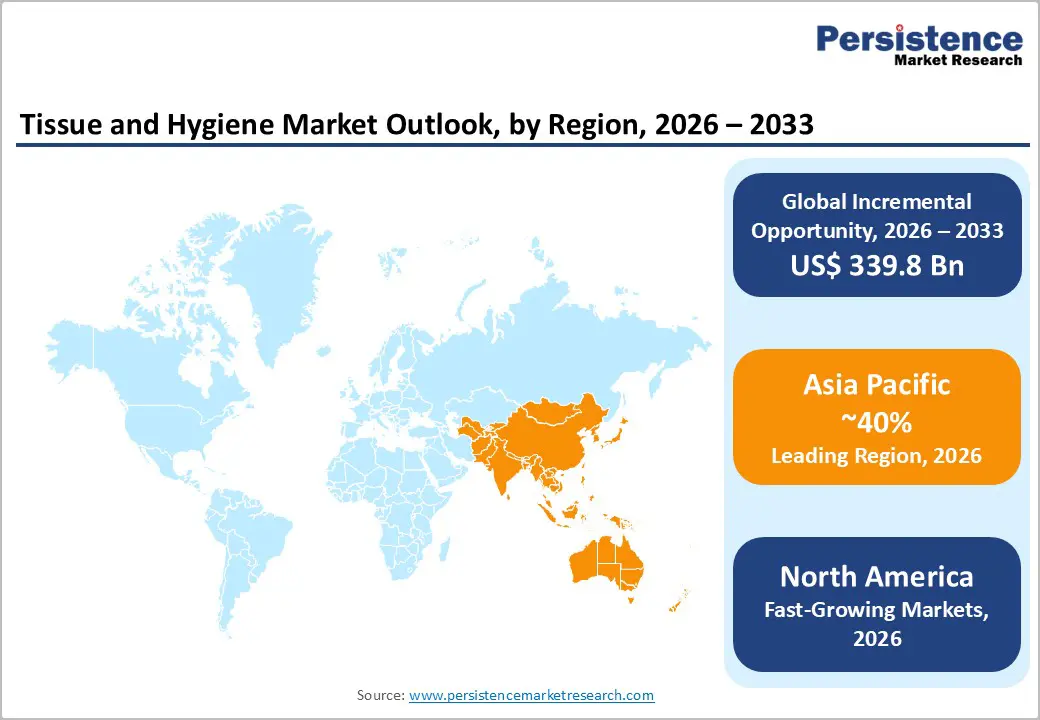

The global tissue and hygiene market size was valued at US$ 33.6 Billion in 2020 and reached US$ 116.4 Billion in 2026, projected to expand to US$ 456.2 Billion by 2033, growing at a CAGR of 21.5% during 2026-2033. This exceptional growth trajectory, supported by a historical CAGR of 23.4% (2020-2025), reflects accelerating demand driven by heightened hygiene consciousness post-pandemic, rapid urbanization in emerging economies, and expanding commercial and healthcare sector requirements. The market's expansion is underpinned by shifting consumer preferences toward premium hygiene products, increased institutional spending on sanitation infrastructure, and technological innovations in product formulation. With Asia Pacific commanding over 40% of global revenue share while North America exhibits the fastest expansion at 24.1% CAGR, the market presents substantial opportunities across both developed and emerging geographic markets through 2033.

Key Industry Highlights:

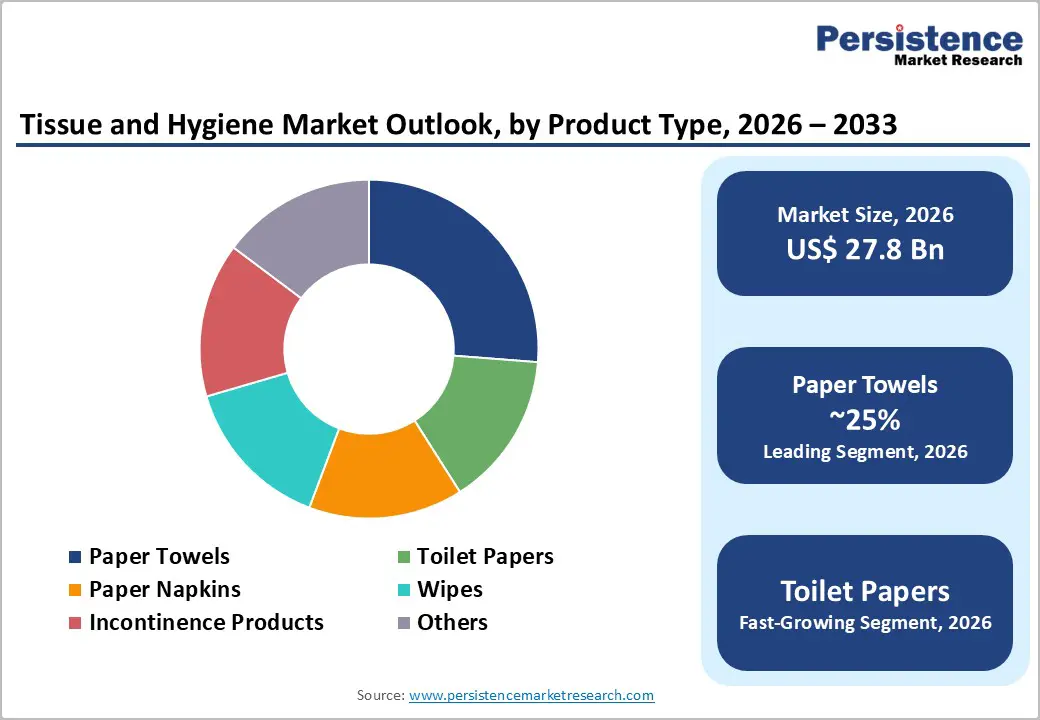

- Product Type Analysis: Paper towels dominate product segmentation at 25%+ revenue share, while toilet paper emerges as the fastest-growing category at 23.2% CAGR, reflecting consumer preference diversification and emerging market consumption growth.

- End User Analysis: Commercial end-users command 35%+ market share, while hospital and healthcare facilities represent the fastest-growing segment at 24.1% CAGR, driven by infrastructure expansion and elevated infection control standards.

- Distribution Analysis: Health and beauty retailers maintain 35%+ distribution channel share, with chemist/pharmacy channels expanding at 22.9% CAGR, reflecting consumer preference for specialized retail environments and healthcare professional guidance.

- Regional Analysis: Asia Pacific dominates global market position at 40%+ revenue share, while North America exhibits fastest regional growth at 24.1% CAGR, presenting investment opportunities across both developed and emerging market geographies.

- Competitive Analysis: Strategic market developments emphasize sustainability-driven innovation, direct-to-consumer channel expansion, and healthcare sector specialization, with major manufacturers investing US$ 250-300 million in emerging market infrastructure development during 2024-2025.

| Global Market Attributes | Key Insights |

|---|---|

| Tissue and Hygiene Market Size (2026E) | US$ 116.4 Bn |

| Market Value Forecast (2033F) | US$ 456.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 21.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 23.4% |

Key Growth Drivers

Post-Pandemic

Hygiene Consciousness and Behavioral Shifts

The global tissue and hygiene market has experienced sustained momentum following the COVID-19 pandemic, which fundamentally transformed consumer perceptions regarding sanitation and personal hygiene. According to the World Health Organization (WHO) and CDC guidelines, household consumption of toilet paper increased by 30-40% during pandemic lockdown periods, establishing new consumption baselines that persist in 2026. Consumers across developed nations have permanently elevated hygiene expenditures, with commercial establishments mandating increased tissue product availability in restrooms, food preparation areas, and healthcare facilities. This behavioral shift extends across institutional settings, where hospitals, schools, and food service operations have institutionalized enhanced sanitation protocols requiring sustained tissue and incontinence product purchases. Market analysis indicates that developed regions have maintained 15-20% elevated consumption levels compared to pre-pandemic baselines, while emerging markets are rapidly adopting similar hygiene standards as GDP growth enables increased consumer spending on health and wellness products.

Market Restraining Factors

Environmental Concerns and Supply Chain Sustainability Pressures

The tissue and hygiene industry faces substantial headwinds from environmental advocacy and sustainability pressures that constrain raw material sourcing and increase production costs. Tissue products account for approximately 10% of global paper consumption, requiring substantial virgin and recycled fiber inputs, which creates resource scarcity concerns in regions experiencing water stress and deforestation pressures.

Environmental groups and regulatory bodies increasingly scrutinize tissue manufacturing's water consumption (approximately 37 liters per kilogram of tissue), creating pressure for process innovation that increases production costs by 8-15%. Supply chain disruptions affecting forest-based fiber supplies, particularly in North America and Northern Europe, have increased raw material costs by 12-18% during 2023-2026. Additionally, consumer segments in developed markets increasingly reject tissue products containing chlorine-based bleaching agents or virgin fiber sourcing, fragmenting market demand and limiting scale economies for conventional manufacturers.

Tissue and Hygiene Market Trends and Opportunities

Premium and Specialty Tissue Product Innovation

The tissue and hygiene market exhibits significant opportunities in premium and specialty product segments, where consumers demonstrate willingness to pay 40-80% price premiums for enhanced functionality and sustainability attributes. Specialized incontinence products incorporating odor-control technologies, moisture-wicking properties, and enhanced comfort features command growth rates exceeding 26% CAGR, driven by aging populations in developed markets and increasing institutional adoption in Asian healthcare facilities.

Eco-friendly tissue products manufactured from sustainable fiber sources (agricultural residues, bamboo) and utilizing water-efficient production processes represent emerging segments with 25%+ growth potential, supported by corporate sustainability procurement mandates. Antimicrobial and hypoallergenic tissue formulations targeting sensitive skin and healthcare applications represent untapped segments in emerging markets where dermatological product awareness is expanding. Market sizing indicates premium tissue segments could represent US$ 85-95 Billion by 2033, up from approximately US$ 15-18 Billion in 2026, representing 35-40% of total market growth opportunity.

Tissue and Hygiene Market Insights and Trends

Product Type Insights

Paper Towels Lead While Toilet Paper Accelerates Growth Across Global Tissue Markets

Paper towels hold a leadership position within the global tissue products market, accounting for more than 25% of total revenue. Their dominance is driven by widespread institutional adoption across commercial offices, hospitality venues, and healthcare facilities, where superior absorbency, rapid drying, and hygiene advantages over reusable cloth alternatives strongly influence procurement decisions. Demand for paper towels closely tracks commercial activity levels and disposable income trends, making the segment a reliable indicator of broader economic conditions. While the category is relatively mature in developed economies, growth opportunities remain substantial in emerging markets, where sanitation standards are increasingly aligning with global norms. In addition, premium paper towel offerings featuring quilted designs, higher absorbency, and sustainability certifications are supporting margin expansion and enabling 20–22% CAGR in select developed market niches.

In contrast, toilet paper represents the fastest-growing tissue product segment, registering a robust 23.2% CAGR through 2033. Growth is fueled by sustained post-pandemic consumption patterns in developed regions and rapid expansion of household sanitation infrastructure in emerging economies. Urbanization, population growth, and rising incomes—particularly in Asia Pacific and Africa—are driving sharp increases in per-capita consumption. Product innovations and deeper penetration into rural and tier-2 markets further strengthen long-term growth prospects, with a vast untapped addressable market ahead.

End User Insights

Institutional End Users Drive Tissue Market Through Regulation, Contracts, and Healthcare Expansion

The end-user landscape of the global tissue and hygiene market is strongly shaped by institutional demand, with commercial and healthcare segments playing decisive roles. The commercial sector—covering restaurants, hotels, office complexes, retail outlets, and educational institutions—accounts for more than 35% of total market revenue. This dominance is driven by standardized sanitation protocols, regulatory compliance requirements, and long-term contractual purchasing arrangements that ensure consistent, high-volume demand. For manufacturers, commercial customers offer margin-accretive opportunities, as B2B contracts typically span 12–24 months, feature stable pricing structures, and involve lower negotiation intensity than retail channels. Within this segment, hospitality and food service stand out, recording growth of 10–12% CAGR due to post-pandemic recovery in travel, dining frequency normalization, and rising service standards. Additionally, the gradual return of corporate office occupancy and expanding commercial real estate in emerging economies are generating incremental demand for institutional tissue supply agreements.

Hospitals and healthcare facilities represent the fastest-growing end-user segment, expanding at a robust 24.1% CAGR through 2033. Growth is supported by healthcare infrastructure expansion, aging populations in developed markets, and stricter infection control standards established after COVID-19. Regulatory mandates and permanent elevation of hygiene protocols have made tissue products a non-discretionary requirement across global healthcare systems.

Distribution Channel Insights

Health Beauty Stores Lead While Pharmacies Drive Rapid Tissue Hygiene Distribution Growth

Health and beauty specialty stores represent the dominant distribution channel for tissue and hygiene products, accounting for over 35% of total revenue. Their leadership reflects strong consumer trust, curated premium product assortments, and the availability of knowledgeable staff who guide purchasing decisions. These retailers benefit from concentrated shopping experiences that encourage brand loyalty and repeat purchases. Well-established loyalty programs and direct consumer engagement also enable the development of private-label offerings, improving margin capture and shelf control. Moreover, aggressive geographic expansion into high-growth regions such as India, Southeast Asia, and Latin America is strengthening channel penetration, with organized chain growth exceeding 15–20% annually in several emerging markets.

In contrast, chemists, pharmacies, and drugstores constitute the fastest-growing distribution channel, expanding at a robust 22.9% CAGR. This growth is driven by rising healthcare awareness, pharmacy network expansion, and increasing consumer reliance on healthcare-professional recommendations. Pharmacies play a critical role in medical-grade tissue products, incontinence solutions, and condition-specific hygiene needs, supporting premium pricing and higher value sales. Their integration with healthcare systems, digital prescriptions, and patient management platforms enables targeted marketing and personalized recommendations, allowing pharmacies to capture market share from traditional retail formats at an accelerating pace.

Regional Insights and Trends

Asia Pacific Tissue and Hygiene Market Dominance Driven By Demographics Growth, Infrastructure

Asia Pacific holds a dominant position in the global tissue and hygiene market, accounting for over 40% of total revenue, supported by its vast population base, rapid urbanization, and rising hygiene awareness. The region is witnessing accelerated market expansion at a robust 22–24% CAGR, significantly outpacing growth in developed economies. This momentum is largely driven by the expanding urban middle class across China, India, Southeast Asia, and Indonesia, where disposable incomes and consumption of hygiene products are increasing steadily. China remains the largest market in the region, although its growth has moderated to 18–20% CAGR due to gradual market maturation. In contrast, India, Vietnam, and Indonesia are experiencing faster growth of 25–28% CAGR, reflecting their earlier-stage market development and lower penetration levels.

Regulatory harmonization efforts, including improved sanitation guidelines and water quality standards aligned with developed markets, are encouraging innovation and wider product adoption. Asia Pacific also benefits from strong manufacturing cost advantages and integrated supply chains, positioning it as a key global production and export hub for tissue products. Furthermore, government-backed infrastructure investments—such as water treatment expansion and sanitation requirements for commercial facilities—are generating sustained institutional demand, reinforcing the region’s long-term market leadership.

North America Tissue Market Leads Innovation Growth Through Premiumization And E-commerce Expansion

North America represents the fastest-growing regional market, expanding at a robust 24.1% CAGR through 2033, even while maintaining a substantial absolute market base. This accelerated growth is driven less by conventional retail expansion and more by premium product innovation, the rapid rise of private-label offerings, and deepening e-commerce penetration. The United States dominates regional demand, with a a market size estimated at approximately US$ 18–22 billion by 2026. Meanwhile, Canada and Mexico together contribute an additional US$ 2–3 billion.

A key structural driver is the expansion of the healthcare sector, including hospital network consolidation and the steady growth of long-term care facilities supporting aging population management. These dynamics are significantly boosting institutional demand for tissue and incontinence products. At the same time, regulatory frameworks such as FDA guidelines for medical-grade tissue applications and EPA water quality standards are encouraging innovation in specialized, high-performance product categories.

Premiumization remains a defining trend, with consumers demonstrating willingness to pay 50–70% price premiums for products offering sustainability credentials, enhanced functionality, and strong brand equity. Additionally, e-commerce accounts for 22–28% of tissue product sales in North America—far exceeding Europe and Asia Pacific—enabling advanced distribution models, dynamic pricing strategies, and stronger direct-to-consumer engagement.

Tissue and Hygiene Market Competitive Landscape

The tissue and hygiene market demonstrates moderate consolidation characteristics with the top 10 manufacturers commanding approximately 55-65% of global market share, while regional and local manufacturers retain substantial positions in emerging markets. Market leadership concentrates among vertically integrated multinational corporations including Kimberly-Clark, Essity, Procter & Gamble, and Georgia-Pacific, which leverage manufacturing scale, supply chain integration, and brand recognition to maintain competitive positioning.

Regional manufacturers in Asia Pacific, including Hengan International, Vinda International, and Oji Holdings, have developed substantial market positions through localized manufacturing, supply chain optimization, and emerging market consumer understanding. Competitive positioning emphasizes product innovation, retail channel relationships, and distribution network development, with branded products commanding 55-60% market share in developed markets versus 35-45% in emerging markets. Market consolidation trends reflect the acquisition of regional players by multinational corporations, R&D investment in sustainability-driven product innovation, and supply chain restructuring to improve resilience and cost efficiency.

Key Industry Developments

- In May 2025, Tamil Nadu Newsprint and Papers Limited (TNPL) partnered with ANDRITZ to launch an INR 300 crore tissue paper manufacturing project in Tamil Nadu. Through this initiative, TNPL marked its formal entry into the tissue segment by announcing the installation of a state-of-the-art tissue production line at its Unit II mill, strengthening its long-term strategy focused on sustainable, high-quality paper manufacturing and capacity diversification.

- In 2024, Singapore-based APRIL Group entered the Indian tissue paper and personal hygiene market by acquiring a controlling stake in Origami. This strategic acquisition enabled APRIL Group, one of the world’s largest fibre, pulp, and paper producers, to gain immediate access to India’s fast-growing consumer tissue and hygiene segment, leveraging Origami’s established brand presence and distribution network.

- In July 2023, UK-based supplier of cleaning, hygiene, and catering products Sybron partnered with eco-friendly bamboo specialist UniGreen to launch bamboo-based tissue paper featuring completely plastic-free packaging, reinforcing the industry’s shift toward sustainable materials and environmentally responsible packaging solutions.

Companies Covered in Tissue and Hygiene Market

- Asia Pulp and Paper Group

- Carmen Tissues S.A.E

- Clearwater Paper Corporation

- Georgia Pacific LLC

- Hengan International Group Co., Ltd.

- Johnson Johnson

- Kimberly-Clark Corporation

- Kruger Inc.

- MPI Papermills Inc.

- Others

- Procter Gamble Company

- Sofidel Group

- Svenska Cellulosa Aktiebolaget (SCA)

- Unicharm Corporatio

- Other Market Players

Frequently Asked Questions

The Tissue and Hygiene market is estimated to be valued at US$ 116.4 Bn in 2026.

The key demand driver for the Tissue and Hygiene market is the rising focus on hygiene, health awareness, and sanitation standards across households, healthcare institutions, and commercial facilities.

In 2026, the North America Pacific region will dominate the market with an exceeding 35% revenue share in the global Tissue and Hygiene market.

Among end users, commercials have the highest preference, capturing beyond 35% of the market revenue share in 2026, surpassing other end users.

Asia Pulp and Paper Group, Carmen Tissues S.A.E, Clearwater Paper Corporation, Georgia Pacific LLC, Hengan International Group Co., Ltd., Johnson Johnson, Kimberly-Clark Corporation, and Kruger Inc. There are a few leading players in the Tissue and Hygiene market.