- Specialty & Fine Chemicals

- Sodium Cyanide Market

Sodium Cyanide Market Size, Share, and Growth Forecast, 2025 - 2032

Sodium Cyanide Market By Form Type (Solid Sodium Cyanide, Liquid Sodium Cyanide), Application (Mining, Chemical Intermediates), End-user Industry, and Regional Analysis for 2025 - 2032

Sodium Cyanide Market Size and Trends Analysis

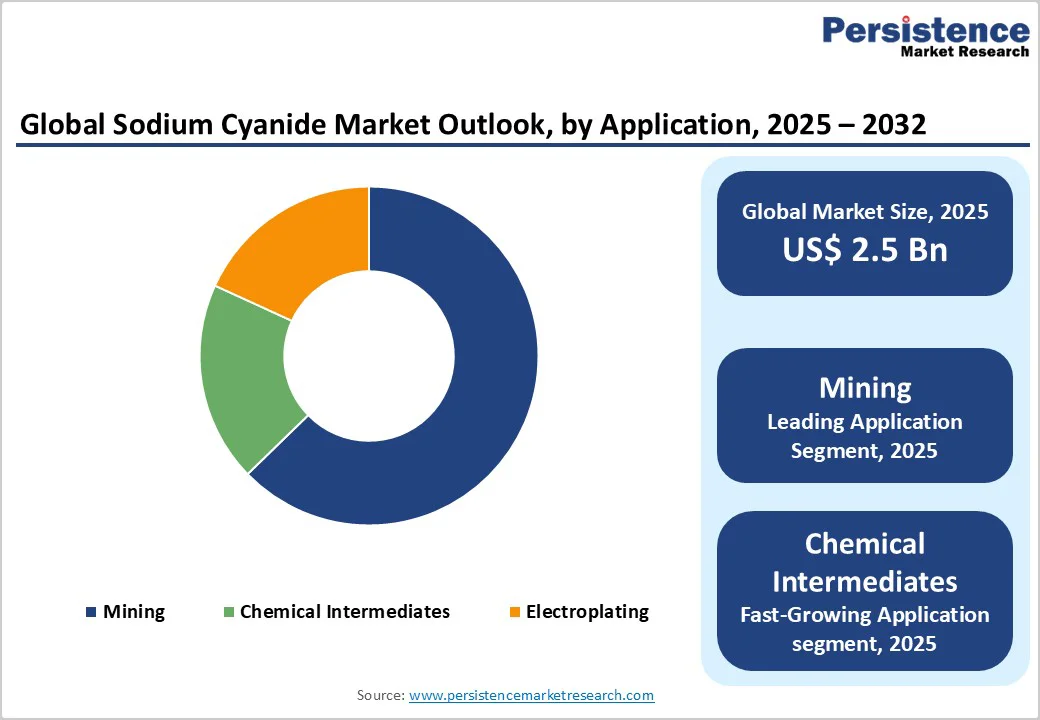

The global sodium cyanide market size is likely to be valued at US$2.5 Billion in 2025 and is expected to reach US$3.6 Billion by 2032, growing at a CAGR of approximately 5.7% during the forecast period from 2025 to 2032, driven by the strong expansion of the gold mining sector, rising demand for base metal extraction, and increased use of sodium cyanide in chemical intermediates. The market also benefits from improved production technologies and stringent quality control regulations, ensuring higher purity levels for industrial applications.

Key Industry Highlights

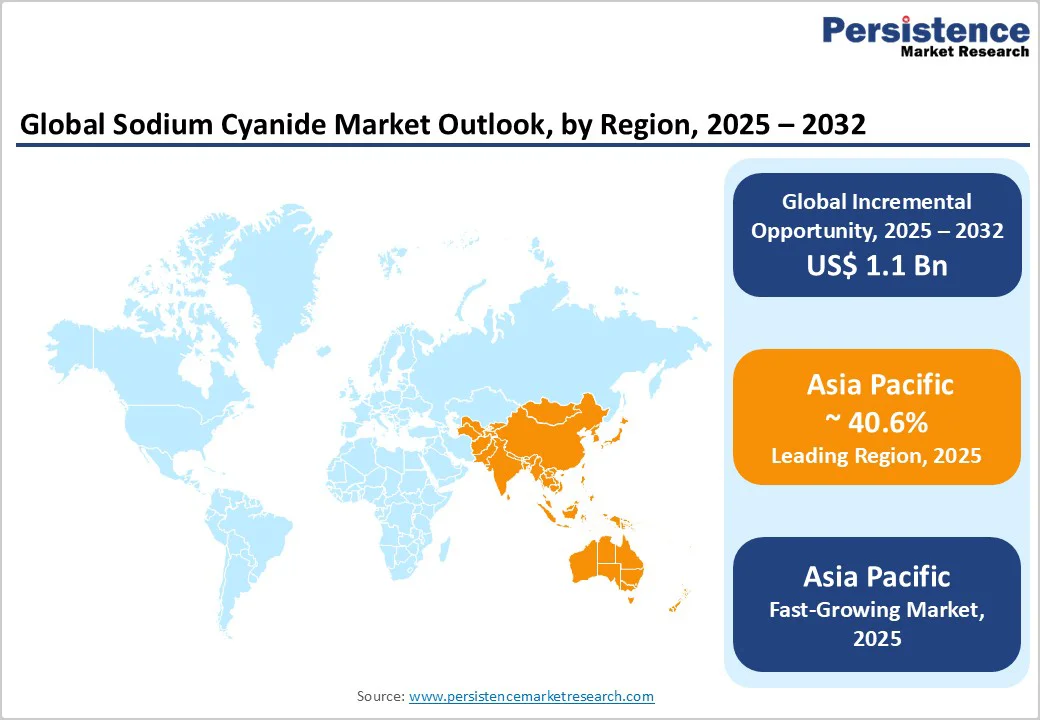

- Leading Region: Asia Pacific held over 40.6% of the global sodium cyanide market share in 2025, driven by large-scale gold mining operations and strong production bases in China and Australia.

- Fastest-Growing Region: Asia Pacific supported by growing mining investments, industrialization across India and Southeast Asia, and capacity expansions in Indonesia and Malaysia.

- Investment Plans: Major producers such as Orica Limited and Cyanco Corporation are investing in production plant expansions and on-site cyanide facilities near mining sites to reduce logistics costs and enhance supply reliability, with several new capacity projects announced in 2024–2025.

- Dominant Form: Solid sodium cyanide accounted for approximately 69.3% of global consumption in 2025, favored for its ease of transport, stability in storage, and suitability for remote mining regions in Africa and Australia.

- Leading Application: The mining application segment is projected to represent over 78.5% of total sodium cyanide demand in 2025, primarily utilized for gold and silver extraction through the cyanidation process, supported by rising exploration activities and higher precious metal prices.

| Key Insights | Details |

|---|---|

| Sodium Cyanide Market Size (2025E) | US$2.5 Bn |

| Market Value Forecast (2032F) | US$3.6 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Growing Demand from the Mining Industry

The primary demand driver for sodium cyanide is its widespread use in gold and silver extraction through the cyanidation process. Rising global gold production, particularly in countries such as China, Australia, and Russia, continues to elevate consumption levels. The global gold output exceeded 3,000 tons in 2024, with over 70% utilizing cyanide-based leaching. The expansion of mining activities in emerging economies, coupled with higher gold prices, is expected to sustain robust demand for sodium cyanide throughout the forecast period.

Expansion in Base Metal Extraction and Electroplating Applications

Sodium cyanide plays a crucial role in the extraction of base metals such as copper, zinc, and platinum, as well as in electroplating operations for the automotive and electronics sectors. The ongoing industrialization in developing economies has led to an increased requirement for metal finishing processes. As industries pursue improved surface coating efficiency, the demand for sodium cyanide-based electrolytes is projected to rise steadily. This trend will significantly contribute to the chemical’s volume growth across multiple end-use segments.

Technological Advancements in Production Efficiency

New manufacturing technologies have improved the efficiency and environmental sustainability of sodium cyanide production. Innovations in hydrogen cyanide synthesis, along with enhanced recovery and recycling systems, have reduced operational costs and environmental impact. Several large-scale producers are transitioning toward integrated facilities that minimize waste and enhance energy efficiency. Such developments are strengthening production capacity and ensuring supply stability in high-demand regions.

Barrier Analysis - Environmental and Safety Regulations

Sodium cyanide is a highly toxic compound subject to stringent environmental and occupational safety regulations. The handling, transportation, and disposal of cyanide-bearing substances are tightly controlled by government and international authorities. Compliance costs related to environmental monitoring, emergency response systems, and waste treatment significantly increase operational expenses for manufacturers. Stricter safety norms are also slowing down new plant approvals, particularly in developed regions.

Availability of Alternative Leaching Technologies

Emerging alternative extraction technologies, such as thiosulfate or bromine-based leaching, are gaining attention as safer and more sustainable options. While not yet cost-competitive, these substitutes are gradually advancing through pilot-scale deployments. Their future adoption could partially reduce sodium cyanide demand in mining operations, particularly in regions emphasizing eco-friendly metallurgical processes.

Opportunity Analysis - Expansion of Mining Activities in Developing Economies

Rapid industrial development in regions such as Africa, Southeast Asia, and Latin America is driving investment in new gold and base metal mines. These markets are expected to register double-digit growth in cyanide consumption as production facilities expand. The establishment of localized sodium cyanide plants near major mining zones presents a strong opportunity for manufacturers to reduce logistics costs and ensure supply reliability.

Technological Innovation in Safe Handling and Recycling Systems

Innovations in cyanide detoxification and recovery technologies create new commercial opportunities. Advanced closed-loop systems that recover cyanide from tailings not only reduce environmental risks but also lower operational costs. The adoption of these systems in modern mines could increase the demand for high-quality sodium cyanide grades compatible with recovery processes, enhancing long-term market sustainability.

Increasing Use in Specialty Chemical Synthesis

Beyond mining, sodium cyanide serves as a precursor for a range of specialty chemicals such as cyanuric chloride, adiponitrile, and pharmaceuticals. As the global chemical sector diversifies, the potential for sodium cyanide utilization in high-value intermediate synthesis is expanding. This diversification helps offset cyclical downturns in the mining industry and enhances revenue stability for producers.

Category-wise Analysis

Form Type Insights

Solid sodium cyanide continues to dominate the global market, accounting for around 69.3% of total consumption in 2025. Its widespread adoption is driven by superior stability, convenient packaging, and ease of long-term storage. Typically supplied as briquettes or pellets, solid sodium cyanide ensures safer transport over long distances and reduces leakage risks, making it ideal for mining operations in remote locations. Countries, including Australia and several African nations, rely heavily on solid cyanide imports due to limited domestic production. Major producers supply the solid form in sealed containers or intermediate bulk packaging that complies with international transport regulations, including the International Cyanide Management Code (ICMC). These factors make solid sodium cyanide the preferred choice for geographically isolated gold mines, particularly where on-site production is not economically viable.

The liquid sodium cyanide segment is the fastest-growing form segment, driven by increasing adoption of on-site or near-site production facilities. This approach allows mining operators to receive liquid cyanide directly via secure pipelines or bulk tankers, eliminating the need to dissolve solid cyanide before use. This improves process efficiency and reduces worker exposure risks. Companies in North America and Asia Pacific are establishing local production units near major gold mines, such as those in Nevada and Western Australia, to minimize logistics costs and enhance safety, supporting the growth of liquid cyanide in the market.

Application Insights

The mining sector remains the largest consumer of sodium cyanide, accounting for over 78.5% of the global demand in 2025. Sodium cyanide is essential in gold and silver extraction via the cyanidation process, where it binds to precious metals, enabling efficient recovery even from low-grade ores. Rising gold exploration across Asia, Africa, and Latin America sustains high consumption levels. Major gold-producing countries such as China, Indonesia, and South Africa contribute significantly to global demand. Additionally, stable gold prices and advancements in metallurgical recovery techniques, including carbon-in-leach (CIL) and carbon-in-pulp (CIP) processes, have improved overall yields, reinforcing sodium cyanide’s pivotal role in mining operations.

The chemical intermediates segment is the fastest-growing application. Sodium cyanide is a key feedstock for producing organic chemicals such as adiponitrile, cyanuric chloride, and acrylonitrile, which are essential in nylon, resins, and agrochemicals. Rising demand for pharmaceutical intermediates and synthetic compounds further drives growth. Adiponitrile, for instance, is critical in nylon 6,6 production for the automotive and textile industries. Expanding agrochemical markets, particularly in India and China, have increased opportunities for cyanide-based intermediates in pesticides and herbicides. The higher profitability and stable pricing in specialty chemical applications are encouraging producers to diversify beyond mining, establishing dedicated lines targeting chemical manufacturers.

Regional Insights

Asia Pacific Sodium Cyanide Market Trends - Expanding Production Base and Mining-Led Growth

Asia Pacific remains the largest and fastest-growing regional market, accounting for 40.6% of global sodium cyanide revenue in 2025. The region’s dominance stems from extensive mining activity, large-scale gold processing, and integrated chemical manufacturing in China, Australia, and Japan. China leads both production and consumption, supported by a well-established domestic supply chain linking cyanide producers with gold mining and chemical industries. Australia is another major contributor, relying heavily on imported cyanide to sustain its high gold production levels, particularly in Western Australia.

Recent developments underscore the region’s growing production base. In February 2025, a new cyanide manufacturing facility became operational in Indonesia, aimed at reducing import reliance and improving local supply availability for Southeast Asian mines. Similarly, Australia witnessed capacity expansions among domestic producers to strengthen regional supply resilience. In 2024, a Japanese manufacturer introduced advanced containment systems for cyanide transport to align with new safety protocols. Environmental upgrades and safer logistics frameworks are expected to enhance sustainability and strengthen the region’s position as the global growth engine for sodium cyanide.

North America Sodium Cyanide Market Trends - Advanced Mining Infrastructure and Cleaner Production Initiatives

North America is being driven by extensive gold mining activity across the U.S. and Canada. The U.S. market benefits from advanced mining infrastructure, proximity to key production hubs, and robust regulatory oversight for cyanide handling. States such as Nevada, Alaska, and Colorado remain major consumption centers due to their concentration of gold extraction operations. Domestic production capacity from leading chemical manufacturers ensures a steady supply chain, reducing import dependence.

Growth in the region is supported by ongoing investments in cyanide detoxification and recovery systems, as miners adopt cleaner technologies to meet environmental standards. For instance, several producers have expanded production capacity in Nevada and Texas to meet increasing mining demand while ensuring compliance with EPA and OSHA guidelines. In April 2025, a U.S.-based producer announced a modernization project integrating real-time monitoring and closed-loop recovery systems to enhance operational safety.

Europe Sodium Cyanide Market Trends - Sustainable Manufacturing and Regulatory-Driven Innovation

Europe holds a moderate share, approximately 18% of global sodium cyanide revenue in 2025, constrained by limited domestic mining but supported by chemical and metallurgical end uses. Countries such as Germany, France, and the U.K. drive regional demand through applications in specialty chemicals, electroplating, and pharmaceutical synthesis. The European Union’s REACH framework enforces strict environmental and safety standards, encouraging the development of closed-loop cyanide systems and alternative leaching technologies in industrial processes.

Recent developments reflect a growing focus on circular production and sustainability. In March 2025, a major European chemical company launched a pilot project in Germany to produce low-emission sodium cyanide using renewable energy sources. Likewise, France-based firms are investing in cyanide derivative manufacturing to cater to the expanding demand for fine chemicals. Europe is driven by innovation in eco-efficient production, investment in high-purity cyanide intermediates, and demand for greener metal-finishing technologies. Germany remains the region’s key import hub and distribution center, ensuring access to compliant cyanide formulations across the continent.

Competitive Landscape

The global sodium cyanide market is moderately consolidated, with the top five producers accounting for over 55% of total global output. These companies operate integrated facilities and maintain long-term supply contracts with mining operators. Competition primarily revolves around pricing, product purity, supply reliability, and environmental compliance. Smaller regional suppliers compete by offering flexible logistics and localized technical support to mining clients.

Leading market participants are pursuing strategies centered on capacity expansion, sustainable production technologies, and strategic partnerships with mining firms. Emphasis is placed on cost efficiency, innovation in detoxification systems, and secure supply chains to maintain competitive advantage.

Key Industry Developments

- In March 2025, Cyanco Corporation launched a new on-site liquid sodium cyanide plant in Nevada, U.S., aimed at reducing transportation risks and improving supply efficiency for nearby gold mining operations.

- In June 2024, Evonik Industries AG announced a partnership with a leading European mining firm to supply high-purity sodium cyanide for gold extraction, supporting sustainable sourcing and improved waste management practices.

Companies Covered in Sodium Cyanide Market

- Asahi Kasei Corporation

- The Chemours Company

- Cyanco (Nevaada Chemicals, Inc.)

- Orica Mining Chemicals

- Sasol Ltd.

- Evonik Industries AG

- Taekwang Petrochemicals

- Korund Ltd.

- The PJSC Lukoil Oil Company

- SINOPEC Shanghai Petrochemical Company

- Imperical Chemical Corporation

- Tiande Chemical

- Draslovka Holding A.S.

Frequently Asked Questions

The global sodium cyanide market size was valued at US$2.5 Billion in 2025, driven by sustained demand from the gold mining and chemical manufacturing sectors.

By 2032, the market is projected to reach US$3.6 Billion, reflecting steady growth supported by increased mining activities and the expansion of chemical intermediate applications.

Key trends include on-site cyanide production near mining operations, the adoption of safer handling and detoxification technologies, vertical integration by mining companies, and environmentally compliant production practices across major regions.

The solid sodium cyanide segment leads the market with about 70% share in 2025, primarily due to its transport stability and suitability for remote mining locations.

The sodium cyanide market is expected to grow at a CAGR of 5.7% between 2025 and 2032.

Major companies include Orica Limited, Cyanco Corporation, Chemours Company, Australian Gold Reagents Pty Ltd (AGR), and Evonik Industries AG.