- Specialty & Fine Chemicals

- Sodium Borohydride Market

Sodium Borohydride Market Size, Share, and Growth Forecast 2026 - 2033

Sodium Borohydride Market by Form (Powder, Granules, Pellets, Solution), Application (Chemical Synthesis, Pulp & Paper Bleaching, Pharmaceutical, Fuel Cells & Hydrogen Storage, Others), and Regional Analysis for 2026 - 2033

Sodium Borohydride Market Size and Trend Analysis

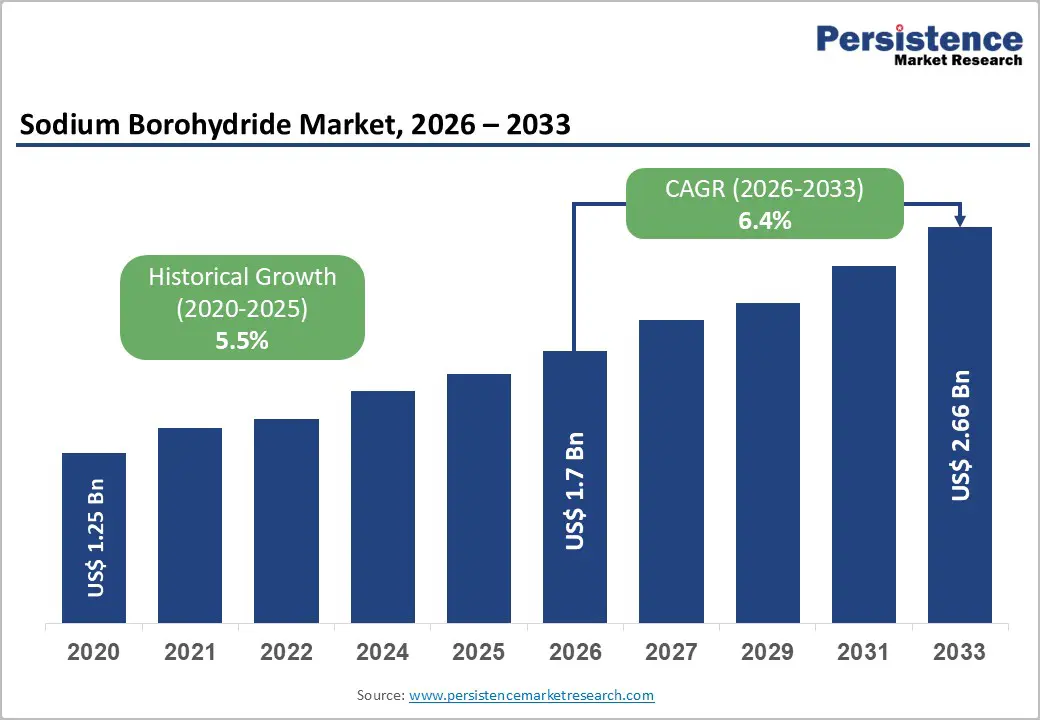

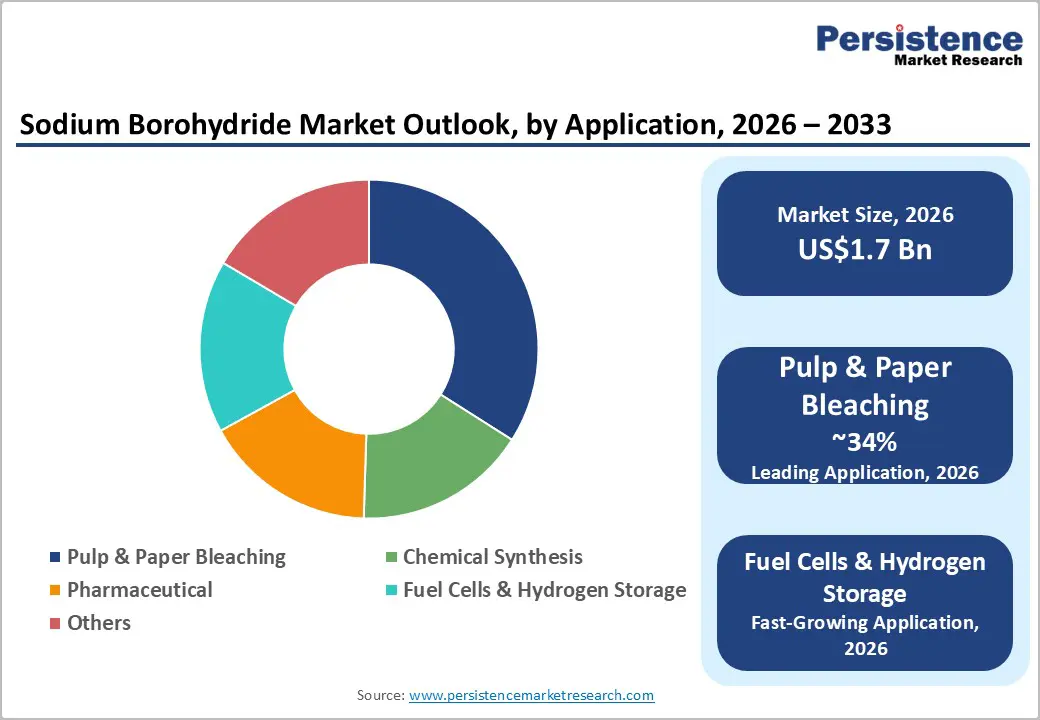

The global Sodium Borohydride market size is valued at US$ 1.72 billion in 2026 and is projected to reach US$ 2.66 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033.

Market expansion is primarily driven by rising demand for pharmaceutical API synthesis, the global transition to hydrogen energy, and sustainable processing in the pulp and paper industry. Sodium borohydride plays an essential role as a selective reducing agent in the production of life-saving drugs. Additionally, significant government investments in clean hydrogen infrastructure, such as the U.S. Department of Energy's Hydrogen Shot initiative and the European Union's REPowerEU Plan, are driving strong demand across various high-growth end-use segments through 2033.

Key Industry Highlights:

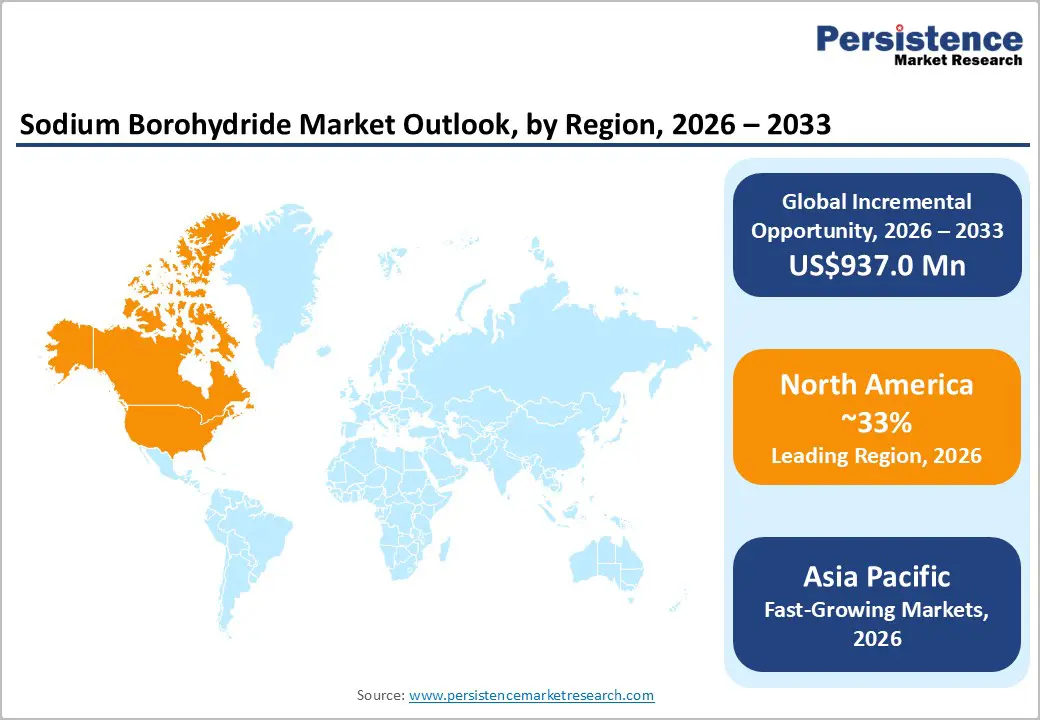

- Leading Region: North America leads the global sodium borohydride market, with 33% market share, underpinned by a world-class pharmaceutical manufacturing base, active U.S. DOE hydrogen economy investment programmes, and the presence of vertically integrated domestic NaBH producers such as Vertellus Specialties and Montgomery Chemicals.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by China's dominant large-scale production capacity, India's PLI-fueled pharmaceutical API expansion, and Japan's advanced hydrogen fuel cell vehicle and stationary energy applications, creating specialized high-purity NaBH demand.

- Dominant Segment: Powder form dominates the sodium borohydride market with approximately 48% share, favoured for its superior reactivity, cost efficiency, and broad compatibility across pharmaceutical API synthesis, industrial reduction, and pulp & paper bleaching applications globally.

- Fastest Growing Segment: Fuel Cells & Hydrogen Storage is the fastest-growing application, propelled by multi-billion-dollar government hydrogen economy mandates in the U.S., EU, and Japan, and NaBH's proven on-demand hydrogen release capabilities for portable and stationary fuel cell systems.

- Key Market Opportunity: Pharmaceutical API production expansion in India and China under national incentive programmes, including India's PLI Scheme, presents a high-value, long-term opportunity for NaBH suppliers to secure strategic supply partnerships across the world's largest generics manufacturing nations.

| Key Insights | Details |

|---|---|

|

Sodium Borohydride Market Size (2026E) |

US$ 1.7 Bn |

|

Market Value Forecast (2033F) |

US$ 2.66 Bn |

|

Projected Growth CAGR (2026–2033) |

6.4% |

|

Historical Market Growth (2020–2025) |

5.5% |

Market Dynamics

Drivers - Rising Pharmaceutical API Production and Speciality Chemical Demand

The global pharmaceutical sector’s growing demand for high-purity reducing agents serves as a significant catalyst for the expansion of the sodium borohydride market. Sodium borohydride functions as an essential reagent in asymmetric synthesis and chiral reduction processes critical to producing active pharmaceutical ingredients (APIs) across antiviral, cardiovascular, and oncological therapeutic classes. With global pharmaceutical sales surpassing US$1.6 trillion in 2023 and maintaining annual growth above 5%, the associated rise in API production directly supports increased consumption of sodium borohydride.

Furthermore, the U.S. Food and Drug Administration's approval of more than 55 new molecular entities in 2023 underscores the growing reliance on borohydride-mediated reduction pathways. As generics manufacturing expands rapidly, especially in India and China under national incentive programs, demand for pharmaceutical-grade sodium borohydride is expected to accelerate, sustaining strong double-digit growth through 2033.

Expanding Hydrogen Economy and Fuel Cell Technology Adoption

Sodium borohydride’s capability to produce high-purity hydrogen through catalytic hydrolysis has attracted substantial attention across the global clean energy sector. Governments are making significant financial commitments to hydrogen infrastructure, exemplified by the U.S. Department of Energy’s Hydrogen Shot initiative, which aims to achieve green hydrogen production at US$1/kg by 2031, and the European Union’s REPowerEU Plan, which dedicates over €3 billion to advancing hydrogen technologies.

Sodium borohydride-based storage systems offer notable advantages for portable and off-grid fuel cell applications due to their controlled hydrogen-release characteristics and a high gravimetric H content of 10.8 wt%. With the continued expansion of fuel cell electric vehicles, portable power solutions, and stationary energy systems across major global regions, the Fuel Cells and Hydrogen Storage segment is anticipated to be the market’s fastest-growing category through 2033.

Restraints - High Production Costs and Geographic Concentration of Raw Materials

The production of sodium borohydride is highly energy-intensive and relies heavily on borax (sodium tetraborate), which is sourced from geographically concentrated deposits. As reported by the U.S. Geological Survey, Turkey holds nearly 73% of global boron reserves, creating notable supply chain vulnerabilities and exposing manufacturers to fluctuations in raw material pricing.

Furthermore, the multi-step synthesis process, requiring inputs such as sodium hydride and trimethyl borate, necessitates substantial capital investment and advanced technical expertise, limiting the entry of new competitors. These inherent structural cost challenges constrain margin expansion and reduce producers’ ability to maintain competitive pricing, particularly in price-sensitive emerging markets.

Handling Hazards and Stringent Regulatory Compliance Requirements

Sodium borohydride is designated as a flammable solid under major international transport and safety regulations, including IMDG, IATA DGR, and ADR/RID codes. Its exothermic reaction with moisture generates flammable hydrogen gas, necessitating specialized storage, handling, and transportation systems to ensure operational safety.

The European Chemicals Agency classifies the compound under the CLP Regulation (EC No 1272/2008) with hazard categories such as acute toxicity and severe eye damage, further elevating compliance requirements. Adhering to these stringent and evolving regulatory frameworks imposes substantial logistical and operational costs, particularly in regions with limited chemical handling infrastructure, thereby constraining broader market penetration.

Opportunity - Green Chemistry Adoption in Pulp & Paper Bleaching Operations

The global pulp and paper industry’s accelerated transition toward sustainable, chlorine-free bleaching represents a significant growth avenue for sodium borohydride producers. As environmental regulations tighten, such as the EU’s Industrial Emissions Directive and EPA rules targeting chlorinated effluent levels, manufacturers are increasingly replacing chlorine dioxide with sodium-borohydride-based brightening agents. According to the FAO, global paper and paperboard production exceeded 400 million tonnes in 2022, driven in part by rising e-commerce packaging demand, which continues to spur capacity expansion.

The expanding recycled fiber processing segment, which depends on sodium borohydride for deinked-pulp brightening, further reinforces steady, high-volume consumption. Companies investing in high-purity, solution-grade sodium borohydride designed for continuous bleaching operations are positioned to secure substantial market share as sustainability requirements intensify.

Pharmaceutical API Expansion in High-Growth Emerging Economies

Emerging markets across Asia Pacific, Latin America, and the Middle East present significant untapped growth potential for sodium borohydride suppliers. These regions are witnessing rapid expansion in pharmaceutical manufacturing, particularly in India, whose pharmaceutical industry, the world’s third largest by volume, is projected to reach US$130 billion by 2030, supported by increased API production under the government’s Production Linked Incentive (PLI) Scheme.

Similarly, China’s “Made in China 2025” initiative continues to emphasize pharmaceutical self-sufficiency, driving substantial domestic demand for NaBH- across numerous API manufacturing facilities. Companies that develop strong regional distribution networks, establish contract manufacturing partnerships, or provide application-specific technical services in these high-growth markets are well-positioned to capitalize on this sustained structural demand through 2033.

Category-wise Analysis

Form Insights

Powder remains the dominant form in the global sodium borohydride market, accounting for approximately 48% of total revenue in 2025. Its leadership is supported by broad applicability across end-use industries, including pharmaceutical API synthesis and industrial chemical reduction, where its high reactivity, accurate stoichiometric dosing, and suitability for bulk handling in large-scale batch processes make it the preferred option.

The pulp and paper sector, along with specialty chemicals manufacturing, further reinforces this position, as powder-grade NaBH aligns well with established operational standards and seamlessly integrates into existing process infrastructure. The specialty chemicals industry alone represents more than one-quarter of U.S. manufacturing GDP, highlighting consistent, high-volume demand. Despite requirements for moisture control and dust management, powder continues to offer the most favorable cost-performance profile and is widely available from major producers across China, Europe, and North America.

Application Insights

Pulp & Paper Bleaching remains the leading application segment in the sodium borohydride market, accounting for roughly 34% of global demand. Sodium borohydride serves as a highly efficient reductive bleaching agent, effectively decolorizing lignin chromophores and enhancing the brightness of recycled mechanical pulp without the environmental drawbacks associated with chlorine-based chemicals. European paper mills recycled more than 59 million tonnes of recovered paper in 2022, with Scandinavian recycling rates surpassing 75%, reflecting sustained and increasing demand for NaBH based brightening solutions.

The broader adoption of circular economy principles, combined with rising sustainability reporting requirements among major paper producers such as International Paper, Smurfit Kappa, and UPM-Kymmene, is further accelerating the shift toward chlorine-free bleaching. Meanwhile, the pharmaceutical segment, representing approximately 28% of demand, is projected to experience the second-fastest growth, driven by expanding API manufacturing and global drug development activities.

Regional Insights

North America Sodium Borohydride Trends

North America continues to lead the global sodium borohydride market, with 33% market share, supported by the United States’ advanced pharmaceutical manufacturing base and well-developed specialty chemicals sector. The presence of major producers such as Vertellus Specialties and Montgomery Chemicals, combined with stringent FDA-enforced regulatory frameworks, sustains robust demand for high-purity, GMP-certified sodium borohydride and enables consistent price premiums over commodity-grade alternatives.

Regional growth is further reinforced by strong governmental commitment to clean hydrogen technologies. The U.S. Department of Energy’s allocation of more than US$9.5 billion for clean hydrogen hubs under the Infrastructure Investment and Jobs Act establishes long-term demand for NaBH in portable hydrogen generation and fuel cell applications. Furthermore, Canada’s expanding mechanical pulp and paper sector, particularly in British Columbia and Quebec, contributes to steady consumption, ensuring North America maintains its market leadership through 2033.

Europe Sodium Borohydride Trends

Europe is the second-largest regional market for sodium borohydride, supported by strong demand in Germany, France, the United Kingdom, and the Nordic countries. Germany’s advanced chemical sector, anchored by global leaders such as BASF SE and Solvay, drives substantial demand for high-purity NaBH used in specialty chemical synthesis and pharmaceutical manufacturing. The European Medicines Agency’s stringent GMP standards further reinforce reliance on certified, established suppliers.

Europe’s climate commitments add structural growth momentum, with the European Green Deal targeting a 55% reduction in greenhouse gas emissions by 2030 and positioning hydrogen as a critical enabler of the transition. Companies such as Finland’s Kemira continue to strengthen regional supply security through strategic partnerships with Nordic pulp mills and ongoing capacity enhancements at its Äetsä facility. Harmonized REACH regulations ensure consistent product quality and support predictable, cross-border market demand across the region.

Asia Pacific Sodium Borohydride Trends

Asia Pacific represents the fastest-growing regional market for sodium borohydride, supported by China’s position as both the leading global producer and consumer. Major Chinese manufacturers, such as Shandong Guobang Pharmaceutical, Nantong Hongzhi Chemicals, and Anhui Jin’ao Chemical, operate large-scale, vertically integrated facilities that ensure cost-efficient production. China’s 14th Five-Year Plan, emphasizing pharmaceutical self-sufficiency and clean energy infrastructure, continues to drive strong domestic demand for NaBH.

India’s rapid expansion of API manufacturing under the PLI Scheme is further creating a robust and recurring market for both imports and locally produced sodium borohydride. Japan’s advanced fuel cell industry, led by Toyota, Honda, and Panasonic, adds specialized demand for ultra-high-purity grades used in hydrogen energy applications. Additionally, rising industrial activity across ASEAN economies, including Vietnam, Indonesia, and Thailand, reinforces the region’s strong growth trajectory and solidifies Asia Pacific as the primary global demand engine through 2033.

Competitive Landscape

The global sodium borohydride market demonstrates a moderately consolidated competitive landscape, comprising major multinational chemical corporations alongside specialized regional producers. The top five companies, Vertellus Specialties, Shandong Guobang Pharmaceutical, Kemira, Nantong Hongzhi Chemicals, and Montgomery Chemicals, collectively generate an estimated 55% of global revenue. Strategic priorities among leading firms include expanding capacities for pharmaceutical-grade, GMP-compliant production, advancing stabilized formulations, and forming partnerships with fuel-cell technology developers. While Chinese manufacturers compete primarily through scale and cost efficiency, Western producers emphasize purity certification, regulatory compliance, and specialized technical support. Emerging trends also include long-term biopharma supply agreements and collaborative development initiatives within hydrogen storage technology ecosystems.

Key Developments:

- June 2025: Kemira announced investment in capacity expansion at its Äetsä facility in Finland, targeting increased pharmaceutical-grade sodium borohydride output to serve growing demand from European and Indian pharmaceutical manufacturers, reinforcing its GMP-certified supplier positioning.

- September 2024: Kemira and IFF (International Flavors & Fragrances) announced the successful completion of a market-entry scale industrial renewable polymer plant, located within Chemigate Ltd.'s Finnamyl biorefinery in Kokemäki, Finland, operated by Chemigate, a member of the Berner Group.

- January 2023: Next Generation Shipyards in the Netherlands began building Neo Orbis, a 20-meter fuel-cell hybrid port vessel utilizing sodium borohydride as a solid-state hydrogen storage medium.

Top Companies in the Sodium Borohydride Market

Vertellus Specialties (Indianapolis, U.S.) is the global revenue leader in sodium borohydride, operating vertically integrated production facilities across the United States. Its flagship products, including PIC Solution™ SBH and Reductase Ultra, serve major pharmaceutical and industrial clients, including Pfizer and International Paper. The company's proprietary process technology, strong regulatory credentials, and broad product portfolio underpin its leadership position in North American and global markets.

Shandong Guobang Pharmaceutical (Shangyu, China) is the dominant Chinese producer with deep vertical integration across the boron chemicals value chain. Serving domestic and international API markets with pharmaceutical-grade NaBH, including GB-Hydride 99 and PharmaBor™, the company has achieved a strong 9.1% five-year revenue CAGR through aggressive capacity expansion and growing exports targeting the global generics pharmaceutical supply chain.

Kemira (Helsinki, Finland) is Europe's primary sodium borohydride supplier, leveraging a strategic joint venture with Borregaard for EMEA-wide distribution. The company's expertise in pulp & paper chemicals and expanding pharmaceutical supply capabilities position it as a leading GMP-compliant supplier for European mills and regulated pharmaceutical manufacturers, with continued investment at its Äetsä production facility in Finland strengthening regional supply security.

Companies Covered in Sodium Borohydride Market

- Vertellus Specialties

- Shandong Guobang Pharmaceutical

- Kemira

- Nantong Hongzhi Chemicals

- Montgomery Chemicals

- Guangxi Guilin Pharmaceutical

- Shanghai Shenyu Pharmaceutical & Chemical

- Anhui Jin'ao Chemical

- Qingdao KYX

- Jiangsu Huachang Chemical

- JSC Aviabor

- Ningxia Best Pharmaceutical

- BASF SE

- Solvay SA

- Ascensus Specialties

Frequently Asked Questions

The global Sodium Borohydride market is valued at US$ 1.7 Bn in 2026 and is forecast to reach US$ 2.66 Bn by 2033, expanding at a CAGR of 6.4% during the 2026–2033 forecast period, up from a historical CAGR of 5.5% recorded between 2020 and 2025.

The two principal demand drivers are rising pharmaceutical API production and the expanding global hydrogen economy. Increasing NaBH₄ adoption in fuel cell applications supported by government clean energy mandates, combined with growing API synthesis demand from pharmaceutical manufacturers, particularly in India and China, are the primary market growth catalysts.

Powder is the leading form segment, accounting for approximately 48% of the global Sodium Borohydride market. Its versatility, high reactivity, precise dosing capability, and established use across pharmaceutical synthesis and industrial reduction applications underpin its dominant market position.

North America is the leading regional market, supported by a mature pharmaceutical industry with stringent FDA quality requirements, strong hydrogen economy investments under the U.S. Infrastructure Investment and Jobs Act, and the presence of major producers including Vertellus Specialties and Montgomery Chemicals.

The most significant opportunity lies in pharmaceutical API manufacturing expansion across emerging economies, particularly India and China, where government incentive programmes, including India's PLI Scheme, are driving large-scale pharma production. The fuel cells & hydrogen storage segment also represents a high-value emerging opportunity backed by global clean energy policy momentum.