- Food Ingredients & Additives

- Monosodium Glutamate Market

Monosodium Glutamate Market Size, Share, and Growth Forecast, 2026 - 2033

Monosodium Glutamate Market by Product Form (Granular, Liquid, Others), Application (Processed Food, Ready Meals, Others), Grade, and Regional Analysis for 2026 - 2033

Monosodium Glutamate Market Size and Trends Analysis

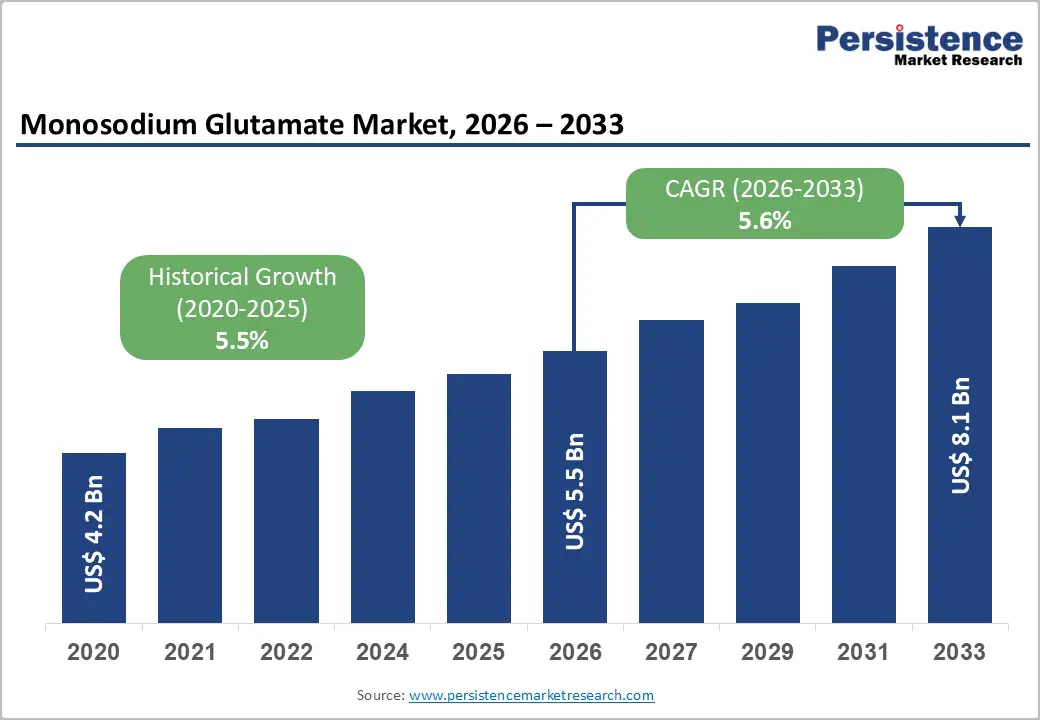

The global monosodium glutamate market size is likely to be valued at US$5.5 billion in 2026 and is expected to reach US$8.1 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033, driven by consistent demand from processed foods, ready meals, and foodservice channels, where MSG enhances umami flavor while enabling sodium-reduction strategies.

Regulatory acceptance across major markets and widespread industrial use in food manufacturing further support stable expansion. The market benefits from established production processes based on fermentation of carbohydrate feedstocks such as sugarcane, starch, and molasses. Increasing urbanization, rising consumption of convenience foods, and evolving dietary preferences toward savory and ready-to-eat products continue to expand the global demand base. As manufacturers prioritize cost-efficient flavor enhancement and sodium optimization, MSG remains a critical ingredient in large-scale food processing.

Key Industry Highlights:

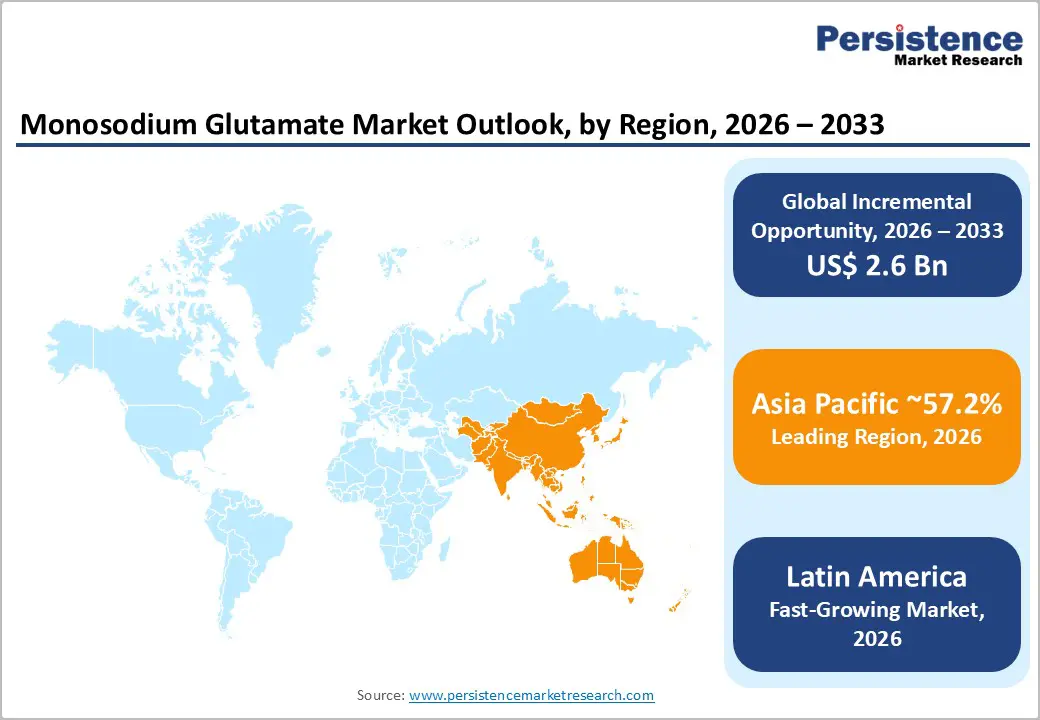

- Leading Region: Asia Pacific is projected to dominate the market, accounting for 57.2% of the market share, driven by strong manufacturing capacity, high consumption levels, and established culinary use of umami flavors.

- Fastest-growing Region: Latin America is the fastest-growing region, supported by rising urbanization, increasing processed food consumption, and regulatory-driven sodium reduction initiatives.

- Investment Plans: Key industry players are focusing on capacity expansions, sustainable raw material sourcing, and fermentation efficiency improvements, with notable investments in large-scale production facilities and agricultural supply chains to enhance cost competitiveness and supply stability.

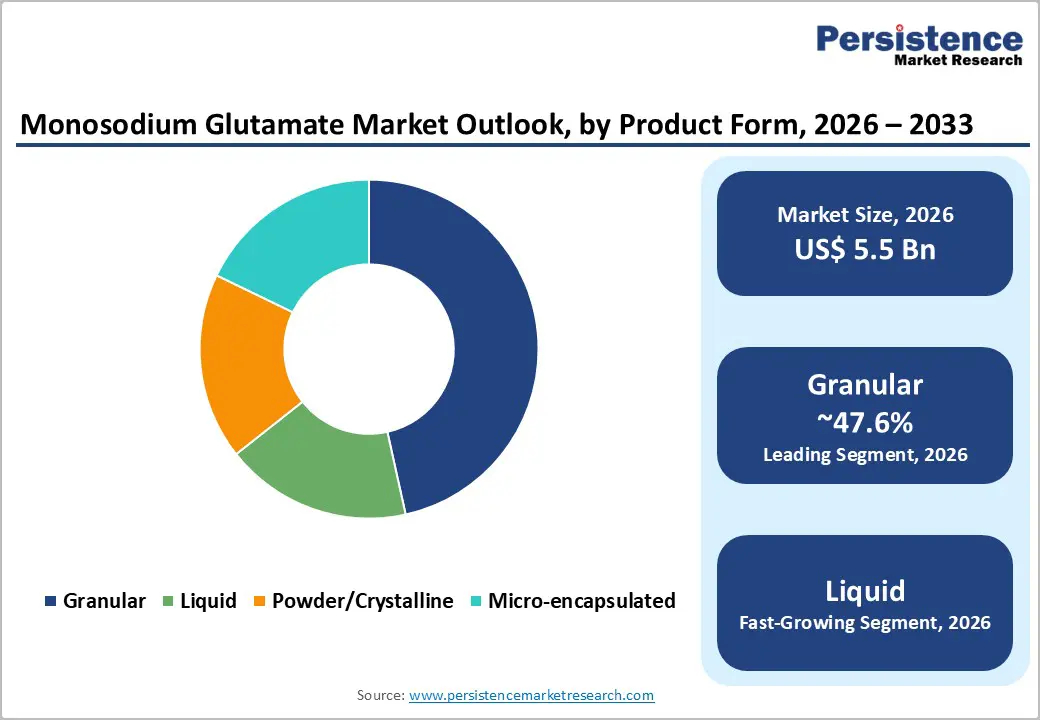

- Dominant Product Form: The granular segment leads the market with an anticipated 47.6% share, owing to its ease of handling, consistent quality, and widespread use across retail and foodservice applications.

- Leading Application: The processed food segment holds a leading position with an anticipated share of more than 40.7%, driven by high demand in instant noodles, snacks, sauces, and packaged food products.

| Key Insights | Details |

|---|---|

| Monosodium Glutamate Market Size (2026E) | US$5.5 Bn |

| Market Value Forecast (2033F) | US$8.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

Market Factors - Driver, Restraint, and Opportunity Analysis

Driver Analysis - Sodium Reduction Initiatives Supporting Reformulation Demand

Global health authorities continue to emphasize sodium reduction as a key public health priority, encouraging food manufacturers to lower salt content in processed foods. Since a significant portion of dietary sodium originates from packaged and processed foods, manufacturers are increasingly incorporating monosodium glutamate (MSG) to maintain flavor intensity while reducing overall sodium levels. This has transformed MSG from a traditional additive into a strategic formulation tool. The ability to deliver strong umami taste with lower sodium content positions MSG as a cost-effective solution in reformulation efforts, especially in regulated markets with stringent labeling requirements.

Rising Demand for Convenience and Processed Foods

Rapid urbanization and changing consumer lifestyles are significantly increasing demand for ready-to-eat meals, instant foods, and packaged snacks. Consumers increasingly prefer time-saving food options without compromising taste, which drives the use of flavor enhancers like MSG. Its widespread application in noodles, soups, sauces, snacks, and meat products highlights its versatility. From a business perspective, MSG offers a low-cost, scalable solution for maintaining consistent taste profiles across large production volumes, making it highly attractive to both multinational food manufacturers and regional processors.

Advancements in Fermentation Technology and Cost Efficiency

MSG production relies on fermentation-based processes using agricultural feedstocks, which provide scalability and cost advantages. Continuous improvements in fermentation efficiency, yield optimization, and process integration have reduced production costs and improved supply reliability. Major manufacturers are also integrating MSG production with downstream food products, enhancing value-chain efficiency. This combination of technological advancement and vertical integration strengthens competitive positioning and ensures stable supply, even in fluctuating raw material environments.

Restraint Analysis - Consumer Perception and Clean-Label Preferences

Despite regulatory approvals and scientific validation of safety, MSG continues to face perception challenges in certain markets. Consumer preference for “clean-label” and additive-free products has influenced purchasing decisions, particularly in developed regions. While awareness is improving, legacy concerns still impact product positioning and limit adoption in premium or health-focused segments. This perception gap requires manufacturers to invest in consumer education and transparent labeling strategies.

Volatility in Raw Material Supply and Pricing

MSG production is dependent on agricultural inputs such as corn, cassava, and sugarcane, making it vulnerable to fluctuations in commodity prices and supply disruptions. Variations in feedstock availability, climate conditions, and global trade dynamics can affect production costs and margins. Manufacturers must optimize sourcing strategies, improve process efficiency, and maintain flexible supply chains to mitigate these risks. Profitability in the MSG market is closely tied to operational efficiency rather than pricing power alone.

Opportunity Analysis - Expansion in Emerging Markets, Particularly Latin America

Latin America presents significant growth potential due to increasing urbanization, rising disposable incomes, and expanding packaged food consumption. Rapid shifts toward modern retail channels and the growing penetration of supermarkets and hypermarkets are further accelerating demand for processed and convenience foods. Government-led sodium reduction initiatives and front-of-pack labeling regulations are encouraging food manufacturers to reformulate products, creating a favorable environment for MSG adoption as a cost-effective flavor enhancer. Countries such as Brazil and Mexico are witnessing strong growth in instant noodles, snacks, and quick-service restaurant offerings, which directly increases MSG consumption. As local and multinational food companies expand production facilities and distribution networks, the region is expected to emerge as a key revenue contributor over the forecast period.

Development of Advanced Product Formats

Innovations in MSG formats, including liquid and micro-encapsulated variants, are creating new application opportunities across industrial food processing. Liquid MSG is increasingly preferred in automated production environments and centralized kitchens, where it enables precise dosing, reduces manual handling, and enhances operational efficiency. This is particularly relevant in large-scale soup manufacturing, ready meal production, and foodservice chains. Micro-encapsulation technology, on the other hand, improves stability and allows controlled flavor release during high-temperature processing, making it suitable for applications such as processed meats, bakery fillings, and seasoning coatings. These advancements align with broader industry trends toward automation, process optimization, and product consistency, enabling manufacturers to differentiate their offerings and improve production efficiency.

Growth in Ready Meals and Plant-Based Foods

The rapid expansion of ready meals and plant-based food categories is creating new demand avenues for MSG. Increasing consumer preference for convenient, time-saving meal solutions is driving the growth of frozen meals, meal kits, and ready-to-eat products, where consistent flavor delivery is critical. MSG plays a key role in enhancing taste profiles in these products, especially in low-sodium formulations. In the plant-based segment, manufacturers are using MSG to replicate the depth of flavor typically associated with meat-based products, improving overall palatability and consumer acceptance. As alternative protein products gain traction globally and foodservice operators expand plant-based menu options, the demand for MSG as a functional ingredient is expected to rise steadily, supporting long-term market growth.

Category-wise Analysis

Product Form Insights

Granular is the leading segment, accounting for an anticipated 47.6% share of the market in 2026. Its dominance is attributed to ease of handling, controlled dispensing, and compatibility with both retail and foodservice applications. Granular MSG is widely used in seasoning blends, instant noodle sachets, packaged soups, and household cooking due to its uniform particle size and consistent solubility. For example, large-scale noodle manufacturers and seasoning brands prefer granular formats for pre-mixed spice packets, where dosing accuracy and shelf stability are critical. It also aligns well with consumer expectations for visually consistent and easy-to-use ingredients, particularly in emerging markets where retail pack formats are expanding.

Liquid is the fastest-growing segment, with its adoption increasing in industrial food processing and centralized foodservice operations, where automation and precision are essential. Liquid MSG is commonly used in large soup manufacturing facilities, ready-meal production lines, and quick-service restaurant supply chains, where it can be directly pumped into formulations, reducing manual handling and waste. This format improves batch consistency and operational efficiency, especially in high-volume environments. Other forms, including powder, crystalline, and micro-encapsulated variants, continue to serve niche applications such as dry seasoning blends, processed meats, and bakery fillings, where specific dispersion or controlled-release characteristics are required.

Application Insights

Processed food is expected to dominate the application segment, contributing more than 40.7% of market share in 2026. MSG is extensively used in soups, instant noodles, sauces, snacks, and processed meat products due to its ability to enhance umami flavor while enabling sodium reduction. For instance, global instant noodle brands and snack manufacturers rely on MSG to maintain strong flavor profiles across mass production. In processed meats such as sausages and canned products, MSG helps improve taste consistency and palatability. This segment benefits from sustained demand for packaged and shelf-stable foods, particularly in urban markets where convenience and affordability drive consumption patterns.

Ready meals represent the fastest-growing application segment, supported by an anticipated strong CAGR driven by convenience trends. Increasing consumer reliance on ready-to-eat and heat-and-eat meals, along with the expansion of food delivery platforms and quick-service restaurant chains, is accelerating demand. MSG plays a critical role in maintaining consistent flavor across large-scale meal production, especially in frozen dinners, meal kits, and airline catering. For example, ready meal producers use MSG to enhance taste in low-sodium formulations and plant-based dishes, ensuring consumer acceptance. Other applications, including seasonings, savory snacks, and specialty areas such as pet food and pharmaceuticals, continue to diversify the market, though at a comparatively moderate growth pace.

Regional Insights

North America Monosodium Glutamate Market Trends - Sodium Reduction Strategies & Clean-Label Reformulation Demand

North America accounts for a significant share of the market, supported by a well-established food processing industry and high consumption of packaged foods. The U.S. leads the region, driven by strong demand from processed food manufacturers, restaurant chains, and snack producers. Large multinational food companies such as Nestlé and Kraft Heinz continue to reformulate products to balance taste and sodium content, which has indirectly supported MSG utilization in specific applications. Regulatory clarity and established food safety frameworks ensure that MSG remains widely accepted for use in food products.

Growth in the region is influenced by increasing focus on sodium reduction and healthier formulations. Manufacturers are leveraging MSG to maintain taste while reducing salt content, aligning with public health initiatives. For example, several U.S.-based snack and frozen food producers have introduced reduced-sodium product lines where MSG is used to preserve flavor integrity. The region also benefits from advanced research and development capabilities, enabling innovation in food processing and ingredient applications. Investment opportunities are concentrated in product reformulation, clean-label positioning, and expansion of plant-based and ready-to-eat food categories, where companies are actively improving taste profiles to meet evolving consumer expectations.

Latin America Monosodium Glutamate Market Trends - Processed Food Expansion & Regulatory-Driven Flavor Reformulation

Latin America is the fastest-growing region in the market, driven by rising urbanization, increasing disposable incomes, and expanding consumption of processed foods. Brazil and Mexico are the primary contributors, supported by growing foodservice industries and strong demand for convenience foods. Regional and multinational companies such as Unilever and Grupo Bimbo have expanded their packaged food portfolios, increasing demand for flavor-enhancing ingredients like MSG in snacks, sauces, and ready meals.

Government initiatives focused on sodium reduction and front-of-package labeling are encouraging manufacturers to adopt alternative flavor enhancement strategies, including MSG. For instance, Mexico’s implementation of front-of-pack warning labels has pushed food producers to reformulate products to reduce sodium while maintaining taste competitiveness. The region’s growth is also supported by the rapid expansion of retail infrastructure and quick-service restaurant chains such as McDonald’s and local fast-food brands, which rely on consistent flavor systems. Companies that offer cost-effective solutions, local production capabilities, and regulatory compliance support are well-positioned to capitalize on this growth, particularly in seasoning blends and instant food segments.

Asia Pacific Monosodium Glutamate Market Trends - Global Production Hub & High-Consumption Umami Market

Asia Pacific is projected to dominate the market, holding 57.2% of market share in 2026, driven by strong manufacturing capabilities, abundant raw material availability, and deep-rooted culinary traditions that favor umami flavors. China remains the largest producer and consumer, supported by extensive production capacity from companies such as Fufeng Group and Meihua Holdings. These companies have continued to expand production facilities and improve fermentation efficiency, strengthening the region’s position as the global supply hub for MSG.

Japan, India, and Southeast Asian countries also contribute significantly to regional growth, supported by increasing demand for processed foods and rapid urbanization. In Japan, Ajinomoto continues to innovate in both consumer and industrial MSG applications, including integration into ready meals and seasoning solutions. In Southeast Asia, the expansion of instant noodle brands such as Indofood (Indomie) and Nissin Foods has significantly increased MSG consumption due to the need for strong, consistent flavor profiles.

India is also witnessing rising demand for packaged snacks and ready-to-cook products, where MSG is used in seasoning mixes. The presence of major manufacturers, ongoing capacity expansions, and integration of agricultural supply chains, such as cassava and sugarcane sourcing, further reinforces the Asia Pacific’s leadership. The region functions as both the primary production base and the largest consumption market, making it central to global MSG industry dynamics.

Competitive Landscape

The global monosodium glutamate market is characterized by moderate fragmentation with medium concentration, featuring a mix of global leaders and regional manufacturers. Key players maintain a competitive advantage through large-scale production, cost efficiency, and integrated supply chains. Market competition is primarily driven by pricing, production efficiency, and distribution reach rather than brand differentiation.

Key players focus on cost leadership, production efficiency, sustainability, and geographic expansion. Companies are investing in advanced fermentation technologies, strengthening supply chain integration, and promoting MSG as a functional ingredient for sodium reduction. Strategic emphasis is also placed on improving consumer perception and expanding applications across emerging food categories.

Key Industry Developments:

- In August 2025, Ajinomoto Co., Inc. announced an investment in v2food Pty Ltd, a company focused on next-generation plant-based foods, to expand its presence in alternative protein applications where MSG plays a role in enhancing flavor profiles.

- In May 2025, Fufeng Group confirmed the full-scale commissioning of new MSG production capacity, strengthening its supply capabilities and cost competitiveness amid increasing global demand and competition from Chinese manufacturers.

Companies Covered in Monosodium Glutamate Market

- Ajinomoto Co., Inc.

- Fufeng Group Limited

- Meihua Holdings Group Co., Ltd.

- Ningxia Eppen Biotech Co., Ltd.

- COFCO Biochemical (Anhui) Co., Ltd.

- Vedan International (Holdings) Limited

- Daesang Corporation

- CJ CheilJedang Corporation

- Shandong Qilu Biotechnology Group Co., Ltd.

- Henan Lotus Flower Gourmet Powder Co., Ltd.

- Sichuan Mianyang Yuxing Bio-Engineering Co., Ltd.

- Fujian Wuyi MSG Co., Ltd.

- Anhui BBCA Biochemical Co., Ltd.

- Shandong Xinle Bioengineering Co., Ltd.

- Angel Yeast Co., Ltd.

- Global Bio-chem Technology Group Company Limited

Frequently Asked Questions

The global monosodium glutamate market is estimated to be valued at US$ 5.5 billion in 2026.

The monosodium glutamate market is projected to reach US$ 8.1 billion by 2033.

Key trends include increasing adoption of sodium reduction in processed foods, rising demand from ready meals and convenience foods, and growing use in plant-based and alternative protein products. There is also a shift toward liquid and advanced MSG formats for industrial efficiency and automation.

The granular product form segment leads the market, accounting for 47.6% share, due to its ease of use, consistent quality, and widespread application in both retail and foodservice sectors.

The monosodium glutamate market is expected to grow at a CAGR of 5.6% from 2026 to 2033.

Some of the major players include Ajinomoto Co., Inc., Fufeng Group, Meihua Holdings Group, COFCO Biochemical (Anhui) Co., Ltd, and Cargill, Incorporated.