- Metals & Minerals

- Sodium Metal Market

Sodium Metal Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Sodium Metal market by Product Type (Solid Sodium, Molten Sodium, Sodium Dispersed in Oil), Grade (Industrial Grade, Standard Grade, High-Purity Grade, Ultra-High-Purity Grade), Industry (Chemical Manufacturing, Pharmaceutical Industry, Textile & Dye Industry, Metal Processing & Foundries, Energy & Power, Research & Academic Institutions, Oil & Gas), and Regional Analysis, 2026 - 2033

Sodium Metal Market Size and Trend Analysis

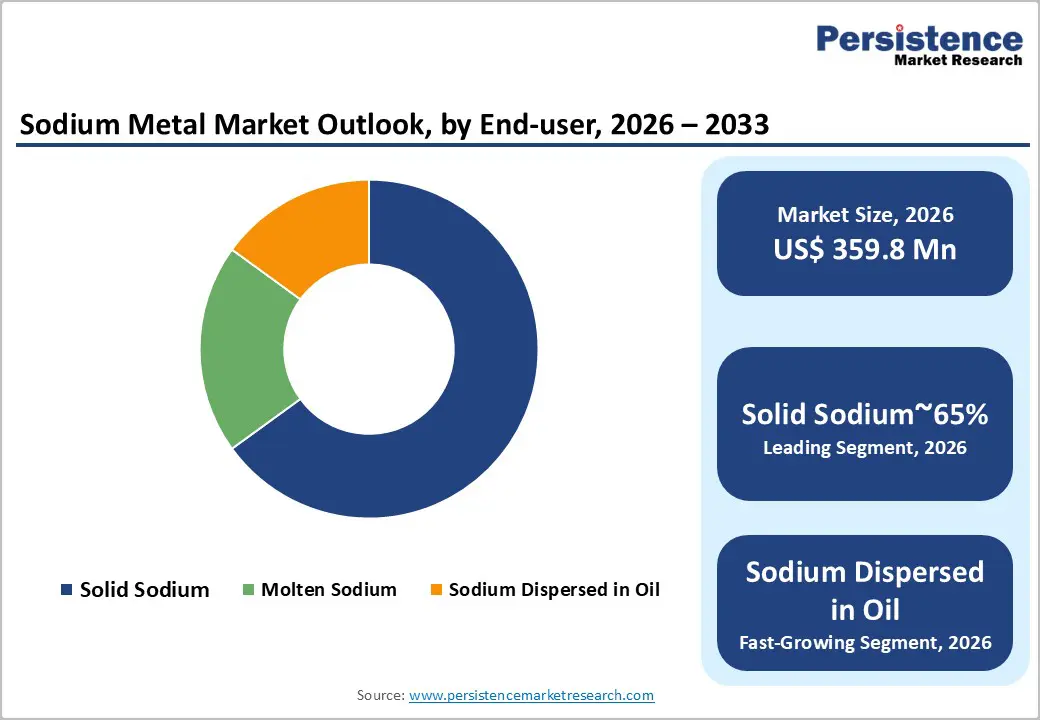

The global sodium metal market size is likely to be valued at US$ 359.8 million in 2026 and is expected to reach US$ 516.5 million by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033.

The rising demand from the chemical manufacturing and energy storage sectors has encouraged the need for sodium metal for chemical applications. Additionally, nuclear energy investments and expansion in sodium-ion battery technologies are also key factors fueling market expansion.

Key Industry Highlights:

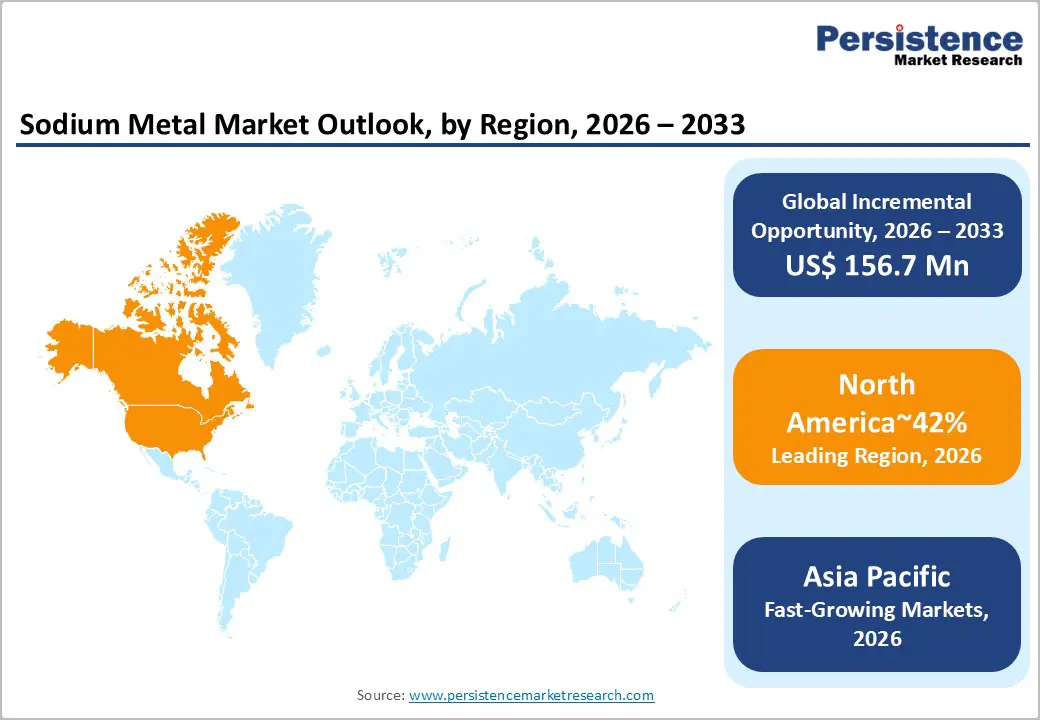

- Leading region: North America leads the global sodium metal market with 42% share, supported by advanced technology and a robust regulatory framework, with the United States being the largest consumer.

- Fastest Growing region: Asia Pacific is the fastest growing segment with a rising CAGR of 7.4%, due to investments in energy storage and nuclear power.

- Dominant segment: The solid sodium segment leads the sodium metal market, making up almost 65% of the total product-type share.

- Fastest Growing segment: Sodium-Ion Battery Applications, supported by government incentives and technological advancements.

- Key Market Opportunity: Expansion of sodium-ion battery technology and nuclear energy projects, creating new demand avenues for sodium metal.

| Key Insights | Details |

|---|---|

| Market Name Size (2026E) | US$ 359.8 Million |

| Market Value Forecast (2033F) | US$ 516.5 Million |

| Projected Growth CAGR (2026 - 2033) | 5.3% |

| Historical Market Growth (2020 - 2025) | 4.1% |

Market Dynamics

Drivers - Rising Adoption of Sodium-Ion Batteries Accelerates Sodium Metal Demand across Electric Vehicles and Grid-Scale Energy Storage Applications

The demand for sodium metal is rising strongly due to its expanding use in sodium-ion battery technology, which is emerging as a cost-effective and sustainable alternative to lithium-ion batteries. As governments and industries increase their focus on clean energy and renewable power solutions, sodium-ion batteries are gaining attention for applications in electric vehicles and grid-scale energy storage. Compared to lithium, sodium is more abundant and less expensive, making it attractive for large-scale deployment. Major battery manufacturers are actively investing in this technology, highlighting its commercial potential.

In 2024, BYD, the world’s largest electric vehicle manufacturer, began construction of a US$ 1.4 billion sodium-ion battery facility in Xuzhou, China. The plant has an annual capacity of 30 GWh and will mainly serve electric micro-vehicles and scooters. This investment clearly reflects confidence in sodium-ion batteries and directly supports growing demand for sodium metal used in battery cathodes and electrolytes.

Expanding Chemical Manufacturing Activities Drive Consistent Growth in Sodium Metal Consumption Across Industrial and Energy-Related End Uses

Sodium metal plays a vital role in the chemical manufacturing industry, where it is widely used as a powerful reducing agent. It is essential in producing key sodium-based compounds such as sodium hydroxide, sodium carbonate, and sodium hydride, which are used across detergents, glass, paper, textiles, and several other industrial applications.

As global industrial activity continues to expand, especially in the Asia Pacific, demand for these downstream chemicals is increasing steadily. Countries such as China and India are investing heavily in chemical production capacity and infrastructure, which further boosts sodium metal consumption. In addition, innovation in energy storage is indirectly supporting chemical demand.

In December 2023, Northvolt validated a sodium-ion battery cell with energy density above 160 Wh/kg at its Swedish research facility. The company plans commercial deployment for grid-scale battery storage from 2024 onward. This progress strengthens long-term demand for sodium metal, both from traditional chemical uses and emerging renewable energy storage applications.

Restraints - Strict Safety, Handling, and Environmental Regulations Increase Compliance Costs and Limit Market Expansion for Sodium Metal Producers

Sodium metal is highly reactive and flammable, which makes its handling, storage, and transportation complex and risk-intensive. As a result, governments in regions such as North America and Europe enforce strict safety and environmental regulations on sodium metal production and usage. Companies must invest heavily in specialized equipment, trained personnel, and compliant facilities to meet these regulatory requirements. Any accident or improper handling can lead to serious safety incidents, environmental damage, and legal liabilities.

These risks increase insurance costs and operational expenses for manufacturers and distributors. Smaller companies often find it challenging to absorb these additional costs, which can limit market entry and expansion. Furthermore, frequent regulatory inspections and compliance audits can slow operational efficiency and project timelines. While these regulations are essential for safety and environmental protection, they act as a significant restraint on market growth by increasing costs, reducing flexibility, and discouraging investment, particularly in regions with highly stringent regulatory frameworks.

Fluctuating Energy and Raw Material Costs Create Pricing Uncertainty and Profitability Challenges for Sodium Metal Manufacturers Globally

The production cost of sodium metal is highly sensitive to fluctuations in raw material and energy prices. Salt, which is the primary feedstock, and electricity, which is required in large quantities for electrolysis, significantly influence overall manufacturing expenses. Changes in global salt prices or sudden increases in power costs can directly impact sodium metal pricing and profit margins. In addition, geopolitical tensions, trade restrictions, or natural disasters can disrupt supply chains, further increasing cost volatility.

Energy price instability, especially in regions dependent on fossil fuels or imported electricity, adds another layer of uncertainty for producers. These fluctuations make long-term pricing contracts difficult and reduce cost predictability for both manufacturers and end users. As a result, companies may delay capacity expansion or capital investments. Persistent price volatility can also discourage new entrants and affect market stability, limiting consistent growth across the sodium metal industry.

Opportunity - Commercialization of Advanced Sodium-Ion Battery Technologies Unlocks Significant Long-Term Growth Opportunities for the Sodium Metal Market

The rapid development of sodium-ion battery technology presents a major growth opportunity for the sodium metal market. As governments and private players invest heavily in electric vehicles and renewable energy storage, sodium-ion batteries are becoming increasingly attractive due to their lower cost, abundant raw materials, and improved safety. Countries such as China and India are leading this transition, supported by strong policy backing and large-scale manufacturing capabilities.

In April 2025, CATL announced that it would begin mass production of its Naxtra sodium-ion EV battery packs by the end of 2025. These batteries offer an industry-leading energy density of 175 Wh/kg, over 500 km driving range, and a long cycle life of 10,000 charges. They also support ultra-fast charging and perform well in extreme temperatures. This breakthrough signals the shift of sodium-ion batteries from research to commercialization, significantly increasing long-term demand for sodium metal.

Growing Investments in Sodium-Cooled Nuclear Reactors Strengthen Long-Term Demand for Sodium Metal in Clean Energy Infrastructure

Sodium metal offers excellent thermal conductivity and stability, making it a preferred coolant in sodium-cooled fast reactors used in advanced nuclear power generation. As countries seek reliable, low-carbon energy sources, nuclear energy is gaining renewed attention. Nations such as India, China, and Russia are actively investing in next-generation nuclear reactors that rely on sodium metal technology. These reactors support efficient power generation and align with long-term carbon neutrality goals.

In December 2025, India and Russia reaffirmed their cooperation in nuclear energy development, with India targeting nuclear capacity expansion to 100 GW by 2030 and beyond. Rosatom also announced preparations for new VVER-1200 reactor designs and potential small modular reactors in India. With multiple nuclear units under construction and new projects planned, demand for sodium metal as a reactor coolant is expected to grow steadily, creating strong long-term opportunities for the market.

Category-wise Analysis

Product Type Insights

The solid sodium segment dominates the sodium metal market, accounting for nearly 65% of the total product-type share. This strong position is mainly driven by its extensive use in chemical synthesis and metallurgical applications, where high reactivity and consistent purity are essential. Solid sodium enables better control over reaction conditions, making it suitable for precision-driven processes such as fine chemical manufacturing and specialty alloy production.

Its stable physical form also allows easier handling and storage under controlled conditions compared to other formats. As industries increasingly focus on efficiency, accuracy, and product quality, solid sodium continues to be the preferred choice across high-value industrial applications, supporting its long-term market dominance.

Grade Insights

Industrial-grade sodium is the leading segment within the grade category, representing around 70% of the overall market share. Its dominance is supported by widespread adoption in large-scale chemical manufacturing and metallurgical operations, where ultra-high purity is not always required. Industrial-grade sodium offers an optimal balance between performance, purity, and cost, making it highly suitable for bulk industrial processes.

Chemical producers and metal refiners rely heavily on this grade for reactions such as reduction, synthesis, and heat transfer applications. Its availability in large volumes and relatively lower production cost further enhance its appeal. As industrial output continues to expand globally, demand for industrial-grade sodium remains consistently strong.

Industry Insights

Chemical manufacturing is the largest Industry for sodium metal, accounting for approximately 40% of total market demand. Growth in this segment is driven by the critical role sodium metal plays as a reducing agent and as a key input in the synthesis of sodium-based compounds. These compounds are widely used across industries such as pharmaceuticals, agrochemicals, polymers, and specialty chemicals.

Sodium metal enables efficient production processes and supports the development of high-performance chemical formulations. As global demand for chemicals continues to rise, especially in emerging economies, manufacturers are increasing their reliance on sodium metal. This sustained demand reinforces the segment’s overall leading position.

Regional Insights

North America Sodium Metal Market Trends

North America holds a strong, dominant position in the global sodium metal market, supported by advanced technology adoption and a well-established regulatory environment. The United States is the largest consumer in the region, driven by consistent demand from the chemical, pharmaceutical, and emerging energy storage sectors. A strong research and development ecosystem encourages innovation, particularly in applications such as sodium-ion batteries and advanced metallurgical processes.

Regulatory clarity and safety standards further support the responsible adoption of sodium metal in both traditional and next-generation uses. The presence of leading manufacturers enhances supply reliability and technological leadership. American Elements, headquartered in Santa Monica, California, with production facilities in Salt Lake City, Utah, is a notable example, offering a wide portfolio of high-purity sodium metal products. As of its 2025 corporate profile update, the company serves over 30% of Fortune 50 companies, along with U.S. and international laboratories and universities. This strong industrial and innovation base continues to reinforce North America’s leadership.

Europe Sodium Metal Market Trends

Europe’s sodium metal market is shaped by strong regulatory harmonization, strict environmental standards, and a growing focus on sustainable technologies. Key countries such as Germany, the U.K., and France drive regional demand, mainly from chemical processing, energy storage, and nuclear-related applications. European industries are increasingly adopting sodium-ion batteries and advanced energy systems as part of long-term decarbonization strategies. Government-backed green energy initiatives and funding programs further support the development of sodium-based technologies.

According to the European Salt Producers’ Association (EUsalt), which represents 18 members responsible for about 80% of Europe’s salt production, the region is the second-largest salt producer globally. In 2023, total EU salt consumption reached approximately 51 million tonnes, with a significant portion used for captive chemical production. By July 2025, the European salt industry was actively advancing sustainability-driven innovation projects. These regulatory and environmental priorities directly influence sodium metal production quality and its adoption in advanced sectors.

Asia Pacific Sodium Metal Market Trends

Asia Pacific is the fastest-growing region in the global sodium metal market, led by China, India, and Japan. Rapid industrialization, a strong manufacturing base, and increasing investments in energy storage and nuclear power are the main growth drivers. China dominates the region as both the largest producer and consumer of sodium metal, with substantial demand from chemical manufacturing and battery development. Expanding infrastructure projects and favorable production economics further support regional growth.

India is also strengthening its position through domestic manufacturing expansion and export-oriented production, supported by government recognition and trade incentives. The region’s momentum is highlighted by major technological advancements, such as the July 2025 launch of mass production of 720V high-voltage solid-state sodium salt batteries by Inner Mongolia Jianheng Aoneng Technology Co., Ltd. With a total investment of 3.5 billion yuan and a planned capacity of 3GWh annually, this milestone positions China among the few countries with commercial-scale sodium battery production, reinforcing Asia Pacific’s strategic importance.

Competitive Landscape

The sodium metal market is moderately fragmented, with several global and regional players competing for market share. Leading companies focus on strategic expansion, research and development, and partnerships to strengthen their market position. Key differentiators include product purity, supply chain reliability, and technological innovation. Emerging business models such as vertical integration and sustainability-driven production are gaining traction, helping companies capture new opportunities in the evolving market landscape.

Key Market Developments:

- In January 2024, BYD began construction on its first sodium-ion battery manufacturing facility in Xuzhou, China, with a planned annual production capacity of 30 GWh, marking a major step in scaling lower-cost, sodium-based energy storage technologies.

- In November 2023, Northvolt announced it had developed a sodium-ion battery cell that contains no lithium, nickel, cobalt, or graphite, advancing more sustainable and cost-effective energy storage solutions with backing from major investors including Volkswagen, BlackRock, and Goldman Sachs.

Companies Covered in Sodium Metal Market

- Inner Mongolia LanTai Industrial Co., Ltd

- Wanji Holdings Group Limited Ltd

- MSSA S.A.S.

- Shandong Moris Tech Co., Ltd.

- American Elements

- North Metal & Chemical Co.

- Central Drug House

- Otto Chemie Pvt. Ltd

- Sihauli Chemicals Private Limited

- SALT Minerals GmbH

- KPL International Limited

- Shanghai Freemen Chemicals Co., Ltd.

- Alkali Metals Ltd

- Nippon Soda Co., Ltd

- China Salt Inner Mongolia Chemical

Frequently Asked Questions

The global sodium metal market is expected to reach US$ 359.8 Million in 2026 and is projected to grow to US$ 516.5 Million by 2033, with a CAGR of 5.3% during the forecast period.

Key drivers include expanding applications in chemical manufacturing, energy storage (sodium-ion batteries), and nuclear energy projects.

Solid Sodium dominates the market due to its widespread use in chemical synthesis and metallurgy, accounting for around 65% of total product type share.

North America leads the global sodium metal market, supported by advanced technology and a robust regulatory framework, with the United States being the largest consumer.

The expansion of sodium-ion battery technology and nuclear energy projects is creating significant new demand avenues for sodium metal.

Leading companies include Inner Mongolia LanTai Industrial Co., Ltd, Wanji Holdings Group Limited Ltd, MSSA S.A.S., Shandong Moris Tech Co., Ltd., American Elements, North Metal & Chemical Co.