- Specialty & Fine Chemicals

- Silica Flour Market

Silica Flour Market Size, Share, and Growth Forecast, 2025 - 2032

Silica Flour Market By Product Type (Standard Industrial, Micronized/Precision), Application (Fiberglass & Glass Manufacturing, Foundry & Metal Casting, Others), Functionality, and Regional Analysis for 2025 - 2032

Silica Flour Market Size and Trends Analysis

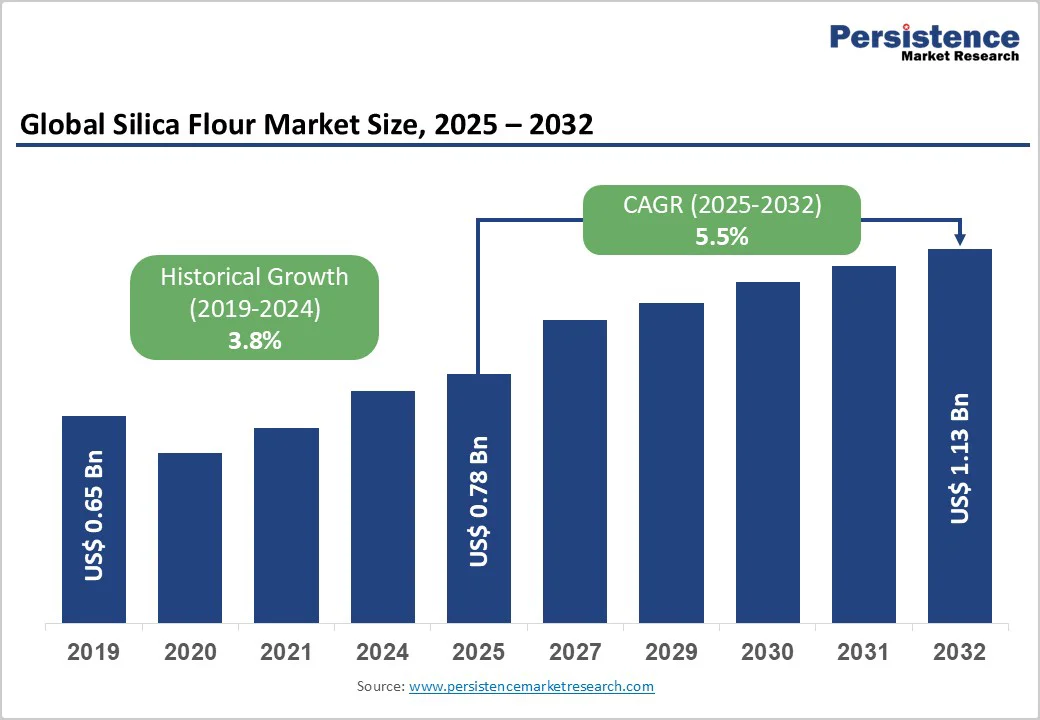

The global silica flour market size was valued at US$0.78 billion in 2025 and is projected to reach US$1.13 billion by 2032, growing at a CAGR of 5.5% during the forecast period from 2025 to 2032, driven by rising demand for high-purity fillers and functional additives in construction chemicals, fiberglass, specialty glass, and advanced composites.

Expanding infrastructure development in the Asia Pacific, combined with stricter product-quality regulations in North America and Europe, is shaping the industry toward high-grade, certified silica products.

Key Industry Highlights

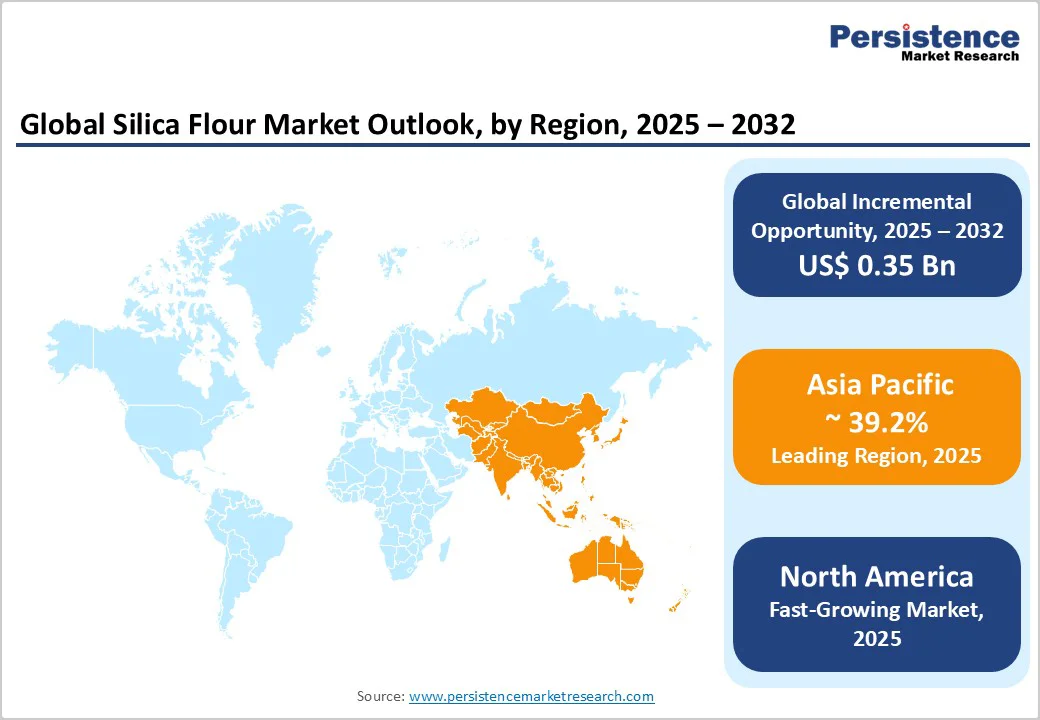

- Leading Region: Asia Pacific dominates the market, accounting for approximately 39.2% of total demand, driven by strong growth in glass, construction, and foundry applications across China, India, and Japan.

- Fastest-growing Region: North America is the fastest-growing regional market, supported by rising demand for high-purity micronized grades used in coatings, composites, and advanced materials.

- Investment Plans: Global producers such as Xinyi Glass Holdings, 20 Microns Ltd., and Denka Company Ltd. are collectively investing over US$250 million in new silica processing, micronization, and high-purity manufacturing facilities to strengthen supply capabilities and meet regulatory compliance standards.

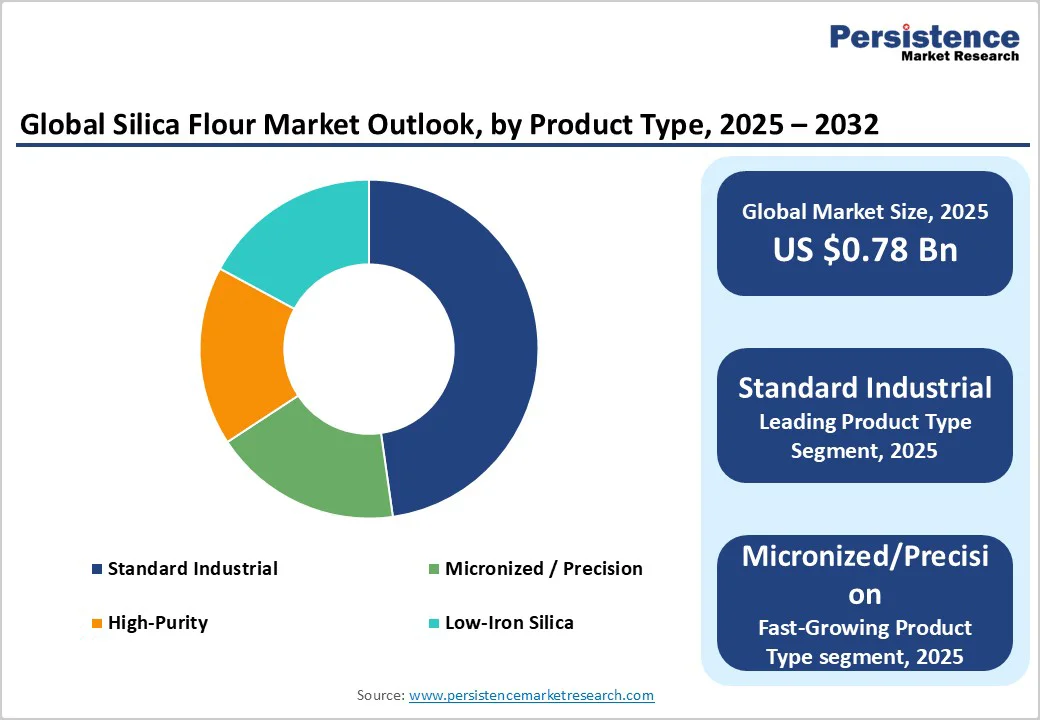

- Dominant Product Type: Standard Industrial Silica Flour remains the largest product category, representing about 53% of total market volume, primarily used in construction materials, mortars, and foundry molds, where cost efficiency and bulk availability are key.

- Leading Application: Fiberglass, Glass, and Foundry applications account for around 38.5% of total market value, owing to the high purity and thermal stability required for glass batching and mold formulations in the automotive and building sectors.

| Key Insights | Details |

|---|---|

| Silica Flour Market Size (2025E) | US$0.78 Bn |

| Market Value Forecast (2032F) | US$1.13 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Construction and Infrastructure Upcycle

The construction industry remains the primary consumer of silica-based fillers, driven by expanding use in concrete, mortar, and composite materials. Infrastructure growth across China, India, and Southeast Asia continues to boost demand for construction chemicals and fiberglass reinforcement, where silica flour enhances strength and surface finish. As global construction activity rises, construction-related applications account for the largest share of demand, supporting steady, volume-driven growth, though pricing remains restrained by its commodity nature.

Technical Substitution and Specialty Applications

Rising demand for advanced composites, specialty coatings, and engineered ceramics is driving growth in high-purity silica flour with controlled particle sizes. Manufacturers are replacing low-grade fillers with engineered silica for superior durability and heat resistance. This has created a fast-growing premium submarket, spurring investments in micronization and precision classification technologies by leading producers.

Regulatory and Quality Standards in Developed Markets

Stricter regulations in developed regions are boosting demand for certified, traceable silica flour. Occupational safety limits on crystalline silica and higher quality standards for food-contact and electronic-grade materials favor suppliers with documented, low-impurity products. Established producers benefit from analytical labs and traceability infrastructure, raising entry barriers for smaller firms and enabling premium pricing for compliant, high-quality silica flour.

Barrier Analysis - Feedstock and Energy Price Volatility

Silica flour production depends on consistent access to low-iron, high-purity quartz feedstock and energy-intensive milling operations. Variability in feedstock quality or price, coupled with fluctuations in energy costs, can significantly affect producer margins. In regions where high-quality quartz is scarce, producers must rely on more expensive processing methods, such as flotation and acid washing. Industry reports highlight that spikes in energy prices can compress gross margins by 100-200 basis points, especially for producers without integrated mining operations or long-term energy contracts.

Cyclical Demand and Substitution Risk

The market closely tracks the performance of the construction, foundry, fiberglass, and ceramics industries. Economic downturns or construction slowdowns can sharply reduce demand volumes. Some downstream users may switch to alternative fillers such as calcium carbonate, wollastonite, or engineered synthetic silicas when performance or cost considerations favor substitution. Historical downturn modeling suggests that extended contractions in global construction could push the market toward a negative single-digit CAGR during recessionary periods.

Opportunity Analysis - Premiumization of Product Mix

Manufacturers have a clear opportunity to transition from commodity-grade silica to micronized and certified high-value products targeted at electronics, coatings, and advanced composite applications. Market research indicates that premium grades could grow at 1.2 to 1.8 times the base market CAGR through 2030. Investing in micronization, analytical testing, and customer co-development facilities can help producers capture higher margins, lock in long-term supply agreements, and differentiate from regional low-cost competitors.

Geographic Expansion into APAC and MENA

Asia Pacific and parts of the Middle East and North Africa are expected to deliver the largest incremental demand growth, driven by large-scale infrastructure programs and local glass and foundry expansions. Regional reports suggest APAC could account for 35-45% of global silica flour demand by 2030. Establishing local micronization or toll-grinding facilities near key industrial zones reduces logistics costs and lead times, making it a strategic advantage for global suppliers seeking to capture regional market share.

Category-wise Analysis

Product Type Insights

Standard industrial silica flour remains the largest product segment, accounting for roughly 53% of global demand. It is extensively used in mortars, cement additives, general-purpose composites, and foundry mold formulations, where high-volume consumption and cost efficiency are prioritized over particle fineness.

Its chemical inertness, thermal stability, and consistent granulometry make it a reliable additive across these applications. Leading producers, including U.S. Silica, Sibelco, and Covia, leverage integrated mining operations and robust logistics networks to ensure consistent product quality and supply reliability.

Demand is driven by ongoing infrastructure development and industrial production across the Asia Pacific and North America, although the commoditized nature of the segment keeps profit margins relatively narrow.

Micronized silica flour is the fastest-growing segment, featuring ultra-fine particles with high SiO2 purity and tightly controlled size. It is increasingly used in electronics, specialty coatings, precision glass, and advanced composites, where superior optical, thermal, and mechanical performance is essential.

Applications include high-performance sealants, printed circuit boards, solar glass, and aerospace composites. Producers such as Sibelco and U.S. Silica are investing in precision milling and air classification technologies to ensure the production of certified, traceable, low-impurity products. Compliance documentation and laboratory certifications are now critical for leadership in this premium segment.

Application Insights

The fiberglass, glass, and foundry industries form the largest application segment, representing roughly 38.5% of global silica flour consumption. Silica’s thermal stability, purity, and refractory properties are critical for glass batching, foundry cores, and fiberglass composites. In fiberglass production, high-purity silica enhances tensile strength and clarity for construction insulation, automotive parts, and wind turbine blades.

Leading companies such as Owens Corning, Saint-Gobain, and Nippon Electric Glass secure long-term contracts with suppliers such as Covia and Adwan Chemical Industries, sustaining robust demand driven by infrastructure expansion and renewable energy growth.

The high-performance coatings and composites segment is the fastest-growing application area, fueled by advances in automotive lightweighting, wind energy, and industrial coatings. Micronized silica flour improves abrasion resistance, film smoothness, and mechanical strength in paints, polymer resins, and composite laminates.

Key applications include wind turbine blades, automotive panels, and architectural finishes, where durability and performance are critical. Leading manufacturers such as PPG Industries, AkzoNobel, and BASF are using high-purity silica fillers, transforming silica flour from a basic additive into a functional enhancer that boosts structural integrity and extends product life in advanced composites.

Regional Insights

North America Silica Flour Market Trends - High-Purity Innovation & Industrial Upgrades Drive U.S. Growth

North America is the fastest-growing regional market, characterized by strong demand for high-purity and micronized grades. The U.S. remains the primary consumption hub, supported by well-established automotive, aerospace, electronics, and construction industries. The region’s focus on advanced materials, combined with innovation in coating and composite formulations, has created sustained growth opportunities for silica flour producers.

Demand is particularly robust for specialty silica used in protective coatings, sealants, and lightweight structural composites, where particle precision and purity directly influence performance outcomes. Manufacturers are increasingly incorporating silica flour to improve tensile strength, chemical stability, and thermal resistance in electric vehicle housings and wind turbine blades.

North America is upgrading silica processing to enhance precision and environmental compliance. In March 2025, U.S. Silica upgraded its Kosse, Texas facilities with advanced micronization equipment for high-purity applications, while Covia implemented a dust-mitigation system in Illinois to comply with regulatory and sustainability requirements. Canada is emerging as a secondary growth hub, with Ontario and Quebec producers focusing on low-iron silica for architectural glass and renewable infrastructure, supplying both North American and European markets.

Europe Silica Flour Market Trends - Sustainability & Regulatory Precision Shape Advanced Applications

Europe remains one of the most technically advanced and quality-driven markets for silica flour, with a clear emphasis on high-performance, low-impurity materials. Demand across the region is driven by automotive manufacturing, construction renovation programs, and specialty glass production, with Germany, the U.K., France, and Spain representing the core markets.

Although overall volume growth remains moderate, Europe’s shift toward sustainable materials and circular manufacturing is accelerating the consumption of engineered silica grades in advanced composites and eco-friendly coatings. The region’s silica flour market benefits from robust green building initiatives under the EU Energy Performance of Buildings Directive, which has increased the use of energy-efficient mortars and insulating materials.

Regulatory influence remains a central pillar of the European silica flour landscape. The REACH framework enforces extensive safety documentation, purity validation, and exposure risk assessments, raising compliance costs but ensuring consistent quality and safety across the supply chain. This has prompted producers to strengthen their testing infrastructure and traceability systems.

For example, in February 2025, Imerys Minerals Ltd. launched its “EcoSil™” product line in France, a low-carbon, high-purity silica flour series aimed at the green coatings and renewable energy sectors. Similarly, Sibelco’s R&D center in Antwerp introduced a new micronized silica product designed for high-transparency glass and electronics applications.

Asia Pacific Silica Flour Market Trends- Industrial Scale & Renewable Growth Cement Regional Dominance

Asia Pacific is the largest and most dynamic regional market for silica flour, accounting for an estimated 39.2% of global demand. The region’s dominance is driven by rapid industrialization, infrastructure expansion, and strong growth in glass manufacturing, foundry operations, and composite materials.

Countries such as China, India, Japan, and South Korea serve as major production and consumption centers, benefiting from abundant quartz reserves, lower energy and labor costs, and a continuously expanding downstream manufacturing base. The growing emphasis on renewable energy, construction modernization, and electronics production is further solidifying Asia’s leadership in the global silica flour industry.

China remains the core growth engine in the region, holding the largest share of both volume and capacity. The country’s silica flour demand is primarily driven by flat glass and fiberglass production, which supports its vast construction and automotive sectors. China’s rapid expansion of solar glass manufacturing, in line with its renewable energy goals under the 14th Five-Year Plan, has significantly boosted the need for high-purity silica grades.

In January 2025, Xinyi Glass Holdings Ltd. announced a US$120 Million investment in a new silica milling and processing plant in Anhui province, designed to supply ultra-clear silica for solar and architectural glass. The government’s continued push for eco-friendly infrastructure and energy-efficient building materials has enhanced domestic consumption of refined silica in mortars, coatings, and sealants.

Competitive Landscape

The global silica flour market is moderately concentrated by value. Integrated miners and processors, primarily U.S. Silica, Sibelco, and Covia, dominate high-margin product categories. Smaller regional producers cater to bulk, commodity-grade demand.

Concentration increases in the premium-grade segment, where high-capital micronization and laboratory facilities are prerequisites. Competitive advantage hinges on feedstock security, process technology, and technical support service.

Dominant strategies emphasize premiumization, vertical integration, and regional expansion. Producers are prioritizing micronized, high-value grades supported by technical service laboratories and compliance documentation. Geographic diversification toward Asia Pacific and MENA markets remains a core growth objective, alongside selective mergers or joint ventures to secure raw materials and enhance processing capability.

Key Industry Developments

- In March 2023, Sibelco Group acquired Kremer Zand en Grind B.V., a Dutch silica sand producer, to strengthen its reserves and supply footprint for silica-flour applications in glass, foundry, and construction markets in Western Europe.

- In February 2025, a leading Indian minerals company (20 Microns Ltd.) commissioned a new fine-particle silica flour line in Gujarat to serve the domestic coatings and polymer industries, enhancing its capability to supply micronized grades for high-performance applications.

Frequently Asked Questions

The global silica flour market size is valued at US$0.78 Billion in 2025.

By 2032, the silica flour market is projected to reach US$1.13 Billion.

Key trends include the shift toward micronized and high-purity silica grades, rising adoption in composite materials, solar glass, and advanced coatings, and a growing emphasis on sustainable, low-impurity production methods.

The standard industrial silica flour segment leads the market, accounting for approximately 53% of total volume, owing to its extensive use in mortars, foundry materials, and construction products.

The silica flour market is expected to grow at a CAGR of 5.5% from 2025 to 2032.

Major players with strong portfolios and global presence include U.S. Silica Holdings Inc., Sibelco Group, Imerys S.A., Covia Holdings LLC, and 20 Microns Ltd.