- Specialty & Fine Chemicals

- Specialty Silica Market

Specialty Silica Market Size, Share, and Growth Forecast for 2025 - 2032

Specialty Silica Market by Product Type (Precipitated Silica, Fumed Silica, Fused Silica, Silica Gel, and Colloidal Silica), Application (Rubber, Agrochemicals, Oral Care, Food Industry, Desiccants, Paints & Coatings, and Others), Regional Analysis from 2025 - 2032

Specialty Silica Market Size and Share Analysis

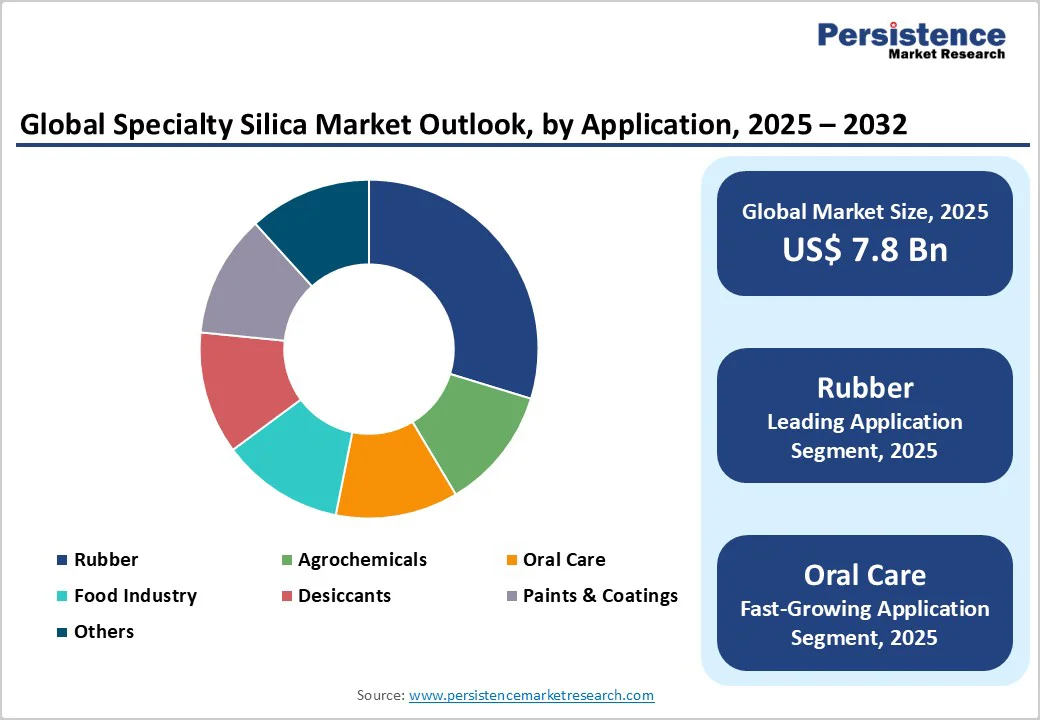

The global specialty silica market is likely to be valued at US$7.8 billion in 2025 and is projected to reach US$12.5 billion, growing at a CAGR of 7.0% between 2025 and 2032. Strong demand from the rubber and paints & coatings industries, advancements in manufacturing to enhance product performance and durability, and rising demand from emerging applications in oral care and agrochemicals are among the prominent factors driving the specialty silica market.

Key Industry Highlights:

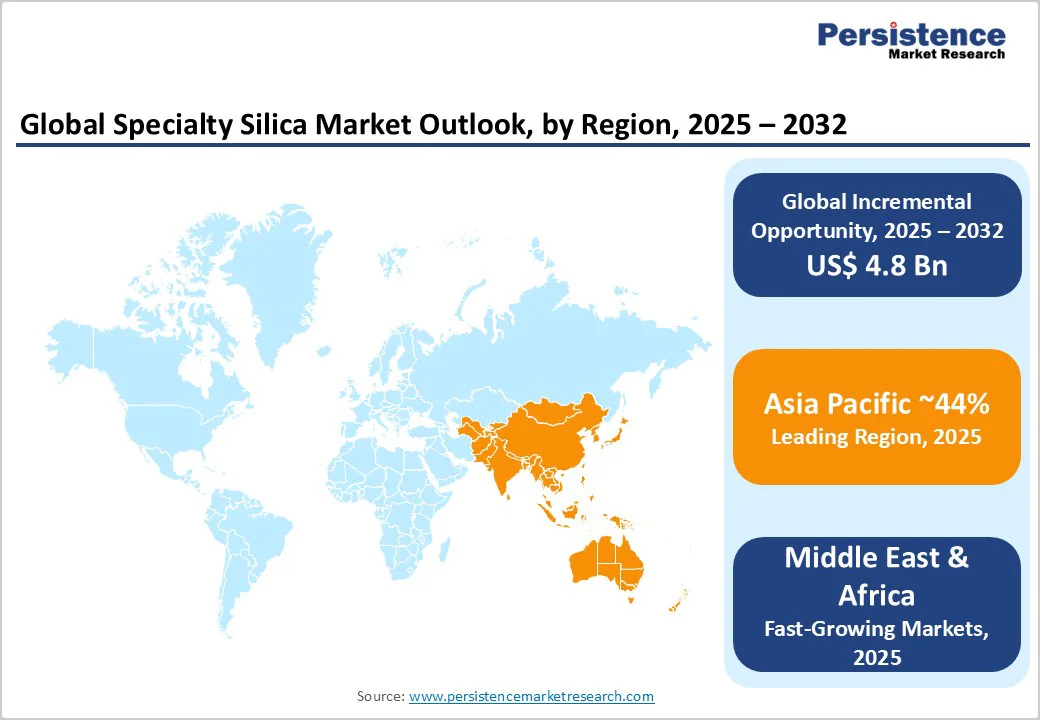

- Regional Leaders: Asia Pacific is the largest and fastest-growing region, holding a 44% market share in 2025, fueled by China, Japan, and India, supportive government policies, cost-competitive manufacturing, and rising demand in EVs, semiconductors, and renewable energy systems.

- Leading Segments: Precipitated Silica dominates the market with nearly 35% share in 2025, widely used for rubber reinforcement and specialty coatings due to its tunable particle size and surface chemistry.

- Industry Applications: Rubber leads with a 32% market share, primarily in tires and industrial rubber goods, where silica enhances tensile strength, reduces rolling resistance, and improves durability.

- Market Drivers: Rising adoption of durable, low-VOC paints and coatings, where specialty silica serves as a rheology modifier, filler, and matting agent.

- Market Restraints: High energy consumption during the production of fumed and fused silica, accounting for nearly 40% of total production costs.

- Market Opportunities: Renewable energy and personal care applications: Specialty silica supports premium whitening toothpastes and polishing products, with nano-scale grades improving performance while minimizing enamel wear.

| Key Insights | Details |

|---|---|

|

Specialty Silica Market Size (2025E) |

US$ 7.8 Bn |

|

Projected Market Value (2032F) |

US$ 12.6 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

7.0% |

|

Historical Market Growth Rate (CAGR 2019 to 2024) |

6.5% |

Market Dynamics

Driver - Rising Demand for High-Performance Rubber in Automotive and Industrial Applications

The emphasis on performance efficiency and durability in automotive and industrial rubber products is a key driver for the global specialty silica market. Specialty silica, particularly precipitated and fumed grades, plays a crucial role as a reinforcing filler in rubber compounds due to its high surface area and polar surface chemistry, which enable superior filler–polymer interactions. When used at optimal concentrations (typically 20–30 phr), precipitated silica significantly reduces tire rolling resistance by up to 10%, resulting in 3–5% fuel savings in passenger vehicles. This makes it a preferred choice for sustainable mobility and next-generation “green tire” technologies.

Specialty silica enhances the performance of industrial rubber goods, including conveyor belts, seals, and hoses, by improving tensile strength by 20–25% compared to traditional carbon black systems. This improvement directly translates into greater wear resistance, flexibility, and operational uptime in demanding environments such as manufacturing, construction, and mining. Emerging studies indicate that fumed silica-based formulations help reduce tire noise levels by approximately 5 dB, addressing consumer preferences for quieter and more comfortable electric and internal combustion engine (ICE) vehicles.

The shift toward energy-efficient, long-lasting, and low-emission rubber materials continues to accelerate the adoption of specialty silica, reinforcing its position as a critical performance enhancer in the global rubber industry.

Increasing Use of Specialty Silica in Paints and Coatings for Enhanced Durability

The rising demand for durable and sustainable coatings is a major driver for the global specialty silica market. In both architectural and industrial coatings, specialty silica serves as a rheology modifier, filler, and matting agent, improving performance and finish quality. When incorporated at 1–3 wt%, colloidal silica enhances scratch resistance by around 20% and improves weatherability, minimizing chalking and cracking under UV exposure.

Silica gel grades deliver superior matting effects while maintaining gloss control, ensuring uniform surface appearance. The transition toward low-VOC and solvent-free formulations has further boosted silica adoption, with formulators achieving up to 30% VOC reduction when replacing conventional organoclays. Its role in maintaining viscosity in high-solids coatings (above 60%) supports applications across metal, wood, and automotive refinish segments, cementing specialty silica’s importance in modern, high-performance coatings.

Restraint - High Energy Consumption in Specialty Silica Production

Fumed silica production via flame hydrolysis of silicon tetrachloride is energy-intensive, requiring temperatures above 1,000 °C and consuming significant electricity and natural gas. Energy costs account for nearly 40% of total production expenses, and fluctuations in fuel prices have led to feedstock costs rising 5–8% over the last three years. Similarly, fused silica manufacturing demands high-temperature electric arc processes. These energy dependencies not only raise production costs but also expose manufacturers to carbon pricing schemes in regions like the EU Emissions Trading System, where carbon allowances add US$ 30– US$ 40 per ton of CO2 emitted. Such cost pressures may be passed on to end users or lead to periodic supply constraints when energy prices spike.

Opportunity - Surging Use in Renewable Energy Systems

Colloidal silica’s fine abrasive action and compatibility with fluoride chemistry make it ideal for toothpaste and polishing products. Novel silica grades engineered with nano-scale particle size distributions (below 100 nm) provide effective stain removal while minimizing enamel wear. Recent clinical studies show a 15% improvement in tooth whiteness after four weeks of use compared to conventional calcium carbonate abrasives. Regulatory clearances for medical-grade silica in dental applications have encouraged personal care brands to launch premium whitening toothpastes featuring silica concentrations of 10–15 wt%. With global toothpaste consumption projected to increase at 3% CAGR, specialty silica suppliers can capture higher-margin opportunities by co-developing formulations with leading oral care companies.

Expansion in Agrochemicals and Desiccants Presents Growth Opportunities

Advances in microporous and mesoporous silica gels are unlocking controlled-release systems for agrochemical delivery. Custom pore structures enable encapsulation of pesticides and fertilizers, releasing active ingredients over 7–14 days, reducing application frequency by 25–30% and minimizing environmental runoff. Field trials in rice paddies and cornfields demonstrated 20% yield improvements with silica-based carriers compared with conventional sprays. In desiccant applications, high-porosity silica gels adsorb moisture capacities exceeding 300 g water per 100 g silica at 25 °C and 60% RH, outperforming zeolite and molecular sieves. Growth in cold chain logistics and pharmaceutical packaging, with stringent moisture-control requirements, offers a lucrative opportunity for silica gel suppliers to partner with packaging firms and expand market share in healthcare and food preservation.

Category-wise Insights

Product Type Analysis

Precipitated silica leads the product type category, commanding approximately 35% of the market. Its versatile particle size distribution and customizable surface chemistry make it the preferred choice for rubber reinforcement and specialty coatings. Industry data reveals that precipitated silica consumption exceeded 2.7 million tons in 2024, driven by stringent performance requirements in automotive and industrial sectors. Its cost-effectiveness relative to fumed silica further solidifies its position as the leading segment.

Fumed silica emerges as the fastest-growing product type, with a projected growth rate of 7.7% through 2032. This accelerated expansion is attributed to its superior performance characteristics in high-value applications, including adhesives, sealants, pharmaceuticals, and personal care products. Pharmaceutical sector adoption of fumed silica as a functional excipient in controlled-release matrices and orally disintegrating tablets has further propelled growth, as the material's exceptional surface area —often exceeding 200 m² per gram —enables precise flowability and dissolution control.

Application Analysis

In 2025, rubber dominates the global specialty silica market with an estimated 40% market share. Specialty silica's ability to enhance tensile strength and reduce heat buildup in tires has led to its widespread use among leading tire manufacturers. A survey of compounders indicates that rubber formulations with 20–25 phr (parts per hundred rubber) of precipitated silica deliver optimal performance, reinforcing its dominance over alternative fillers. This trend aligns with the rising global vehicle fleet and sustainability mandates.

Oral care is the fastest-growing application segment, with market projections indicating an 8.2% CAGR through 2032. Colloidal and hydrated silica grades have become indispensable in toothpaste formulations due to their gentle abrasive action that effectively removes plaque and stains while minimizing enamel wear. The segment benefits from regulatory clearances for medical-grade silica in dental applications and rising consumer demand for whitening and sensitivity-relief toothpastes.

Regional Insights

North America Specialty Silica Market Trends

North America is experiencing robust growth in the specialty silica market, driven by supportive regulatory environments and a mature automotive sector that demands high-performance materials. The region’s focus on sustainability and low-VOC formulations has intensified specialty silica adoption across multiple industries. Leading tire manufacturers in the United States are increasingly incorporating precipitated and fumed silica into their formulations to enhance fuel efficiency and reduce rolling resistance, with silica content reaching up to 30% in premium tire compounds.

The enforcement of stringent emission standards by the U.S. Environmental Protection Agency (EPA) has further encouraged a shift toward mineral-based additives, boosting the use of silica-based rheology modifiers in coatings, adhesives, and sealants. Across Canada, market expansion is driven by the oral care segment, where leading personal care brands collaborate with silica suppliers to develop toothpaste formulations for whitening and sensitivity relief, driving rising demand for colloidal silica.

Europe Specialty Silica Market Trends

Europe’s specialty silica market benefits from advanced materials research and harmonized regulations that promote product safety and environmental compliance. Across the region, investment in electric vehicle (EV) supply chains and green building initiatives stimulates demand for high-purity silica grades.

In Germany, the automotive sector leads, with EV tire producers increasing silica usage by 20% to meet torque and noise reduction targets. Manufacturers like Evonik Industries AG have launched bio-based precipitated silica to lower carbon footprints. The United Kingdom and France show strong uptake of silica gel desiccants in pharmaceutical packaging, driven by EMA guidelines on moisture-sensitive drug storage. Spain’s burgeoning agrochemical industry is adopting colloidal silica carriers for controlled-release fertilizers, supported by EU subsidies for sustainable farming.

Asia Pacific Specialty Silica Market Trends

Asia Pacific specialty silica market is characterized by rapid capacity expansions and cost-competitive manufacturing, positioning the region as the fastest-growing globally. Investments in new facilities and technology upgrades are enhancing both production volume and quality.

In China, integrated producers are scaling up precipitated silica output, achieving a 15% increase in 2024 through process optimization in Shandong Province. Japan focuses on fused silica for semiconductor and electronics applications, supplying high-purity material critical for wafer fabrication. India’s tire and paint industries are emerging hotspots, with manufacturers incorporating specialty silica to meet stricter fuel-efficiency norms and low-VOC standards. ASEAN countries are leveraging lower production costs to explore specialty silica in cementitious coatings, sealants, and high-performance construction materials.

Competitive Landscape

The global specialty silica market exhibits a moderately consolidated structure, with the top five companies, such as Elkem, Evonik Industries AG, Solvay SA, Wacker Chemie AG, and PPG Industries, Inc., holding over 50% of global capacity. These leaders leverage extensive R&D investments and global production networks to maintain cost leadership and innovation.

Regional players such as Tata Chemicals and Madhu Silica Pvt. Ltd. are expanding downstream capabilities to capture local demand. Mergers, acquisitions, and strategic partnerships focused on sustainable production and specialty grade development are prevailing trends among market participants.

Recent Industry Developments:

- In March 2025, Nouryon completed a significant capacity expansion at its Alvin, Texas, fumed silica plant to address surging demand from the U.S. coatings and sealants sector. The upgrade added an extra 15,000 metric tons of annual capacity, incorporating advanced flame hydrolysis reactors with enhanced thermal recovery systems that cut energy consumption by 10%.

- In November 2024, Evonik Industries AG unveiled a breakthrough bio-based precipitated silica grade tailored for high-performance tire applications. Derived partially from sustainably sourced rice husk ash and processed via patented low-temperature precipitation, this new silica cuts cradle-to-gate CO2 emissions by 25% versus petroleum-derived counterparts.

- In June 2024, Elkem commissioned its state-of-the-art silica gel plant in Kristiansand, Norway, marking a major leap in sustainable specialty silica manufacturing. The facility leverages 100% renewable hydroelectric power, reducing carbon emissions by an estimated 60% compared to conventional production methods.

Companies Covered in Specialty Silica Market

- Elkem

- Evonik Industries AG

- Solvay SA

- Nouryon

- Akzo Nobel N.V.

- PPG Industries, Inc.

- PQ Corporation

- Sinosi Group Corporation

- Tosoh Corporation

- Wacker Chemie AG

- Madhu Silica Pvt. Ltd.

- Tata Chemicals

- Cobot Corporation

- Qingdao Makall Group Inc.

- Nissan Chemical Industries Ltd.

Frequently Asked Questions

The global specialty silica market is likely to value at US$ 7.8 billion in 2025 and is forecast to reach US$ 12.5 billion by 2032, growing at a CAGR of 7.0%.

Specialty silica enhances tire performance by reducing rolling resistance and improving wear resistance, with up to 30% higher silica loading cutting resistance by 10% and extending tread life by 15%.

Precipitated silica leads with approximately 35% market share due to its cost-effectiveness, tunable surface properties, and broad application across rubber and coatings sectors.

North America leads the market, driven by robust tire manufacturing, stringent environmental regulations, and innovation in low-VOC coatings applications.

Development of controlled-release agrochemical carriers using high-porosity silica gels presents significant opportunity, with moisture adsorption capacities exceeding 300 g per 100 g.